Nomura Insights: TSMC Target Price Raised, AI Infrastructure Cycle Not Yet Peaked

TL;DR

· Nomura raises target price for AI hardware stocks such as TSMC, believing the AI infrastructure investment cycle has not peaked yet.

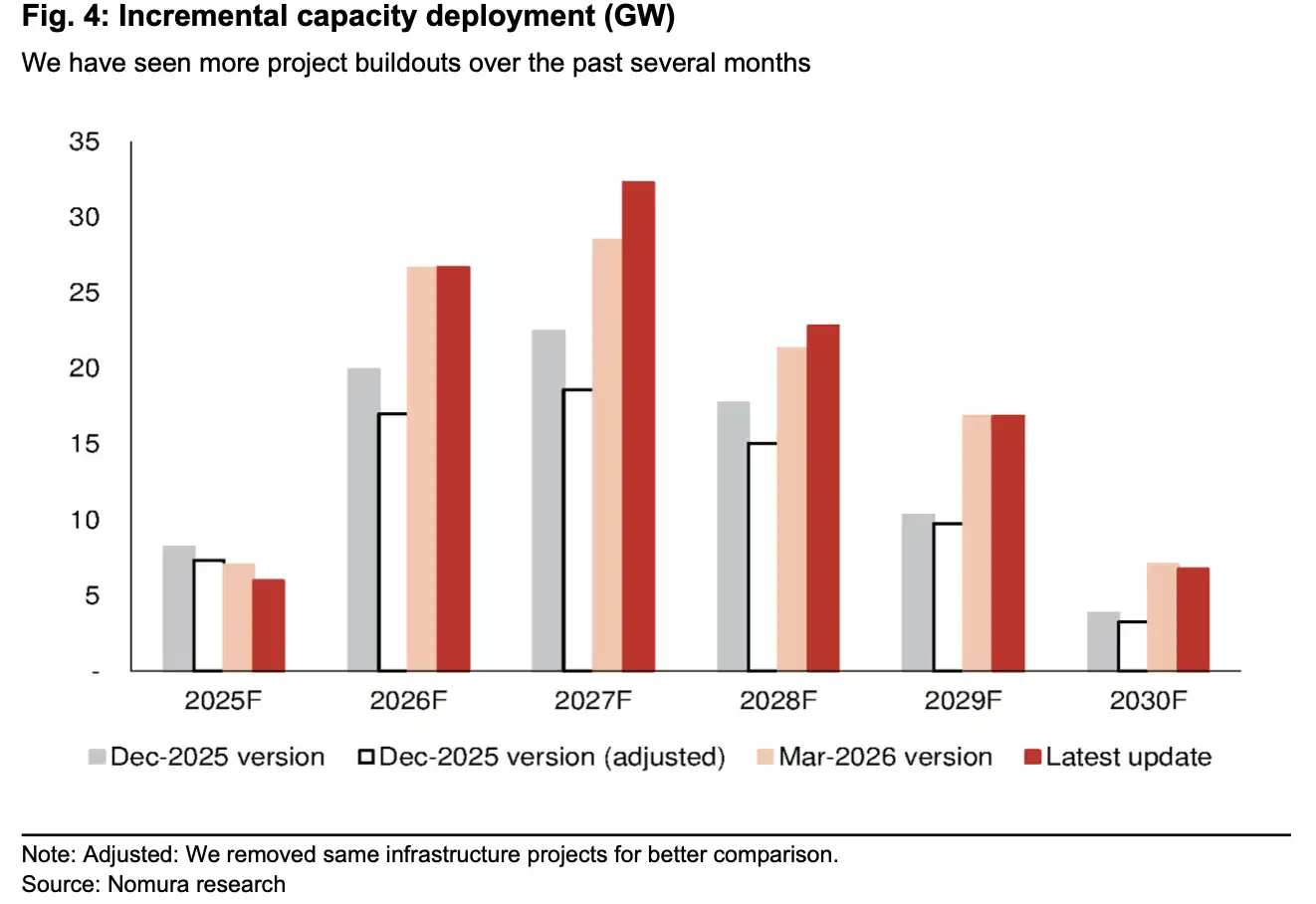

· The 2027 additional data center capacity has been revised upwards to around 32GW, indicating continued rise in AI chip demand.

· Advanced packaging bottleneck is overflowing to WoS and components, with cash flow pressure remaining a risk in 2027.

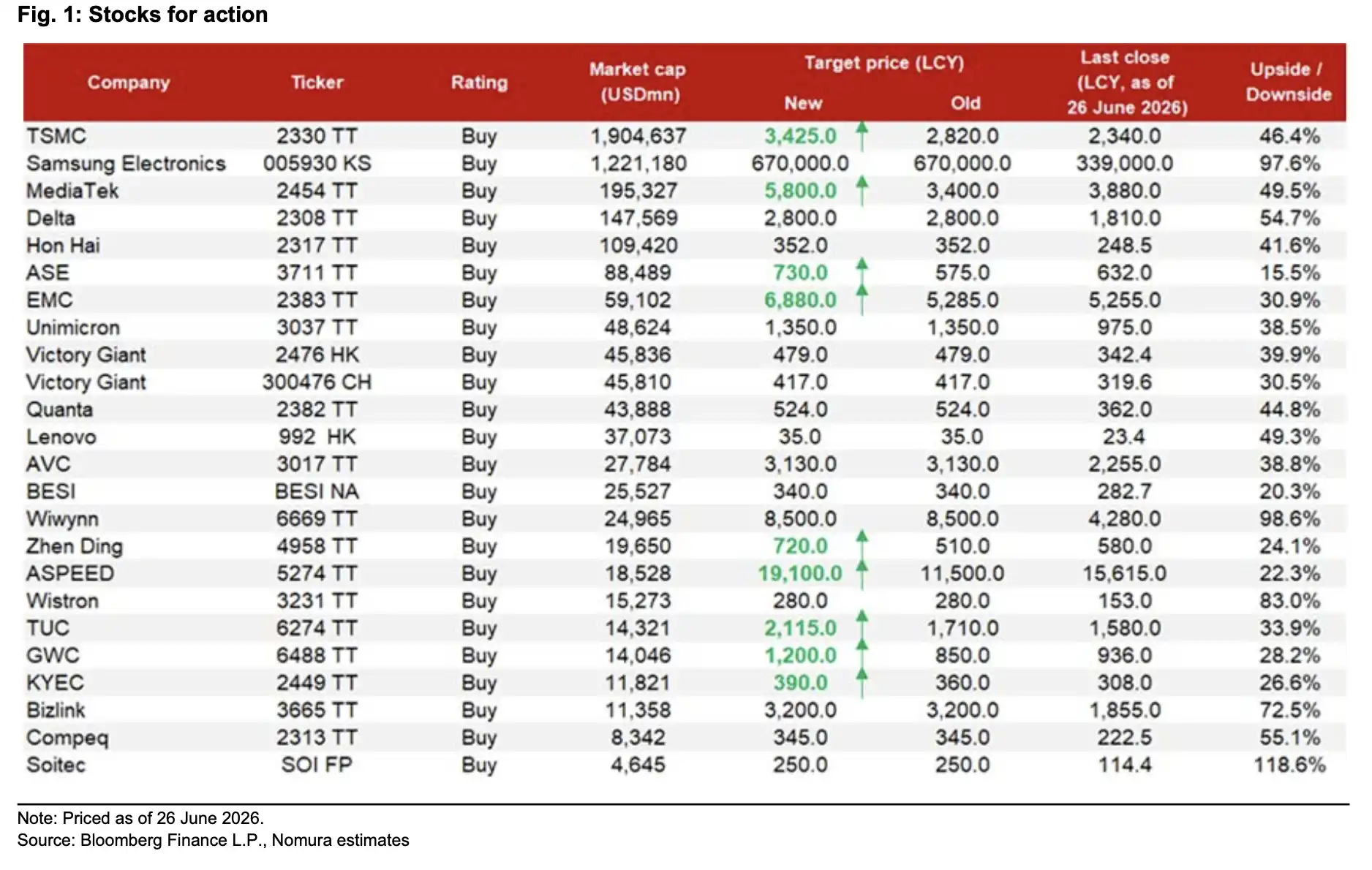

In an Anchor Report released by Nomura on June 30, the target price for several AI semiconductor and hardware stocks was raised, with the key action being the adjustment of TSMC's target price from 2,820 NT to 3,425 NT.

According to a report by Investing.com on the same day, Nomura believes the AI infrastructure investment cycle has "not yet peaked." Based on TSMC's closing price of 2,340 NT on June 26, the new target price represents approximately a 46.4% upside.

The main theme of this report is straightforward: the AI semiconductor market has already seen significant gains, but data center construction, AI chip demand, server revenue, and advanced packaging demand continue to rise. The SOX index has risen by about 85% since the March cycle update and about 211% since the AI theme was reintroduced in May 2025. Despite recent pullbacks, institutions are still lifting demand forecasts.

In addition to TSMC, Nomura also raised target prices for companies in the AI semiconductor and hardware supply chain such as MediaTek, ASE, EMC, and ZDT. Individual stock target prices are just the surface; what supports this round of upward adjustments is a larger assumption about data center capacity and tighter supply of advanced packaging and components.

TSMC's new target price is 3,425 NT with approximately 46.4% upside, along with the target price increases for multiple AI hardware stocks.

2027 Additional Data Center Capacity Raised to Around 32GW

How long the AI hardware cycle can continue depends first on whether data centers continue to be built.

Based on Nomura's criteria, in the global tracked self-owned data center projects, the total number of new data center projects has increased from about 240 at the end of March to around 280, with GW-scale projects increasing from over 40 to around 50. The additional deployment capacity for 2027 has been raised to approximately 32GW, up from the previous 28GW. The capacity for 2028 has also been revised upwards from 21GW to around 23GW.

The key significance of this number is that data center capacity will continue to transform into AI chips, advanced packaging, and server revenue demand. According to Nomura's estimates, the additional capacity could correspond to an annual demand for approximately 4 to 6 million AI chips.

The focus of market debate is no longer just "whether there is demand for AI servers," but whether power, cabinets, GPUs, TPUs, advanced packaging, and components can keep up with the construction pace.

Server revenue forecasts have also been raised. Based on the report's assumptions, global server revenue growth rates for 2026 and 2027 have been revised up to 74% and 65% year-on-year, compared to the previous prediction of 43% for 2026. Specifically, AI server revenue growth is expected to be 78% and 76%, and general/CPU server revenue growth has also been raised to 67% and 43%.

This will not only expand AI infrastructure beyond GPU servers but will also drive CPU servers, networking, power supplies, cooling, PCBs, and peripheral hardware. The report also mentions that the 2026 GB/VR cabinet shipment assumption has been increased from 50,000 units to 54,500 units, with an estimated 62,000 units in 2027. This term is based on the report's methodology, and a unified expression has not yet been seen in public data.

Global incremental data center capacity for 2027F is revised up to about 32.3GW, and 2028F is about 22.85GW.

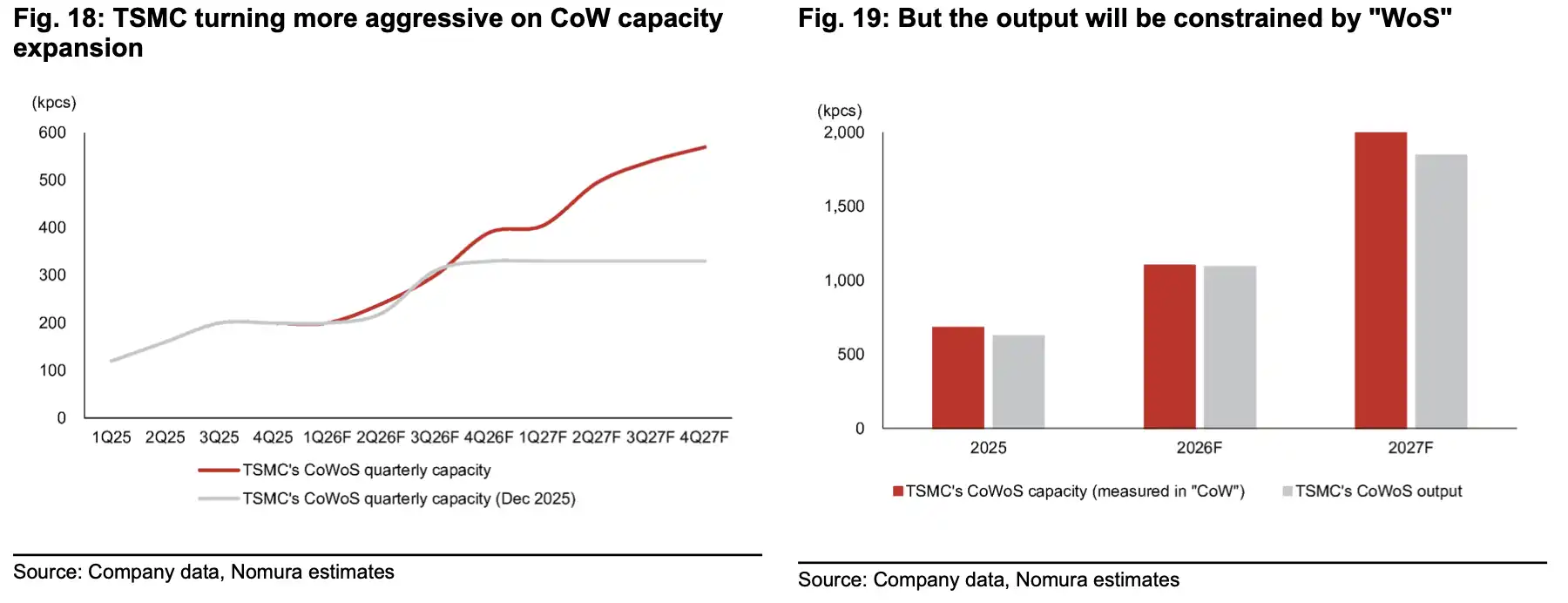

CoWoS Targeting 2 Million Pieces, Chip-on-Wafer-on-Substrate (CoWoS) Expanding to Wafer-on-Substrate (WoS) and Components

Following the continued increase in AI chip demand, TSMC's advanced packaging remains the market's most concerning supply constraint.

By Nomura's estimates, TSMC's CoWoS capacity will be about 1.1 million pieces in 2026, with a targeted capacity of 2 million pieces in 2027. To match the compound growth rate in the higher end of AI revenue from 2024 to 2029, long-term capacity reaching 2.5 to 3.5 million pieces may be needed by 2029.

It is important to distinguish the methodology. TSMC's official disclosures usually do not reveal specific CoWoS production figures, and different brokerages may handle monthly, yearly, capacity, output, piece, or wafer metrics differently. The above numbers should be understood as Nomura's model assumptions, not official capacity guidelines.

More importantly, the model does not directly calculate full production at 2 million pieces in 2027 but assumes actual output of about 1.8 million pieces. This is because the bottleneck may no longer be solely concentrated on the TSMC-controlled CoW process but Wafer-on-Substrate (WoS) and a series of small components may become new constraints.

These components include CCL, IC substrates, high-end capacitors, PMIC, and optical components. If supply chain misalignment worsens starting from the second half of 2026, it will bring short-term uncertainty in delivery, pricing, and order allocation. In the medium term, strong demand squeezing deeper-level component supply will also expand the beneficiary scope from wafer foundries and the GPU chain to assembly testing, PCB, substrates, capacitors, power supplies, and optical components.

CoWoS capacity is projected to increase from about 680,000 units in 2025 to a target of 2 million units in 2027, but the model is calculated based on 1.8 million units output, highlighting the WoS bottleneck.

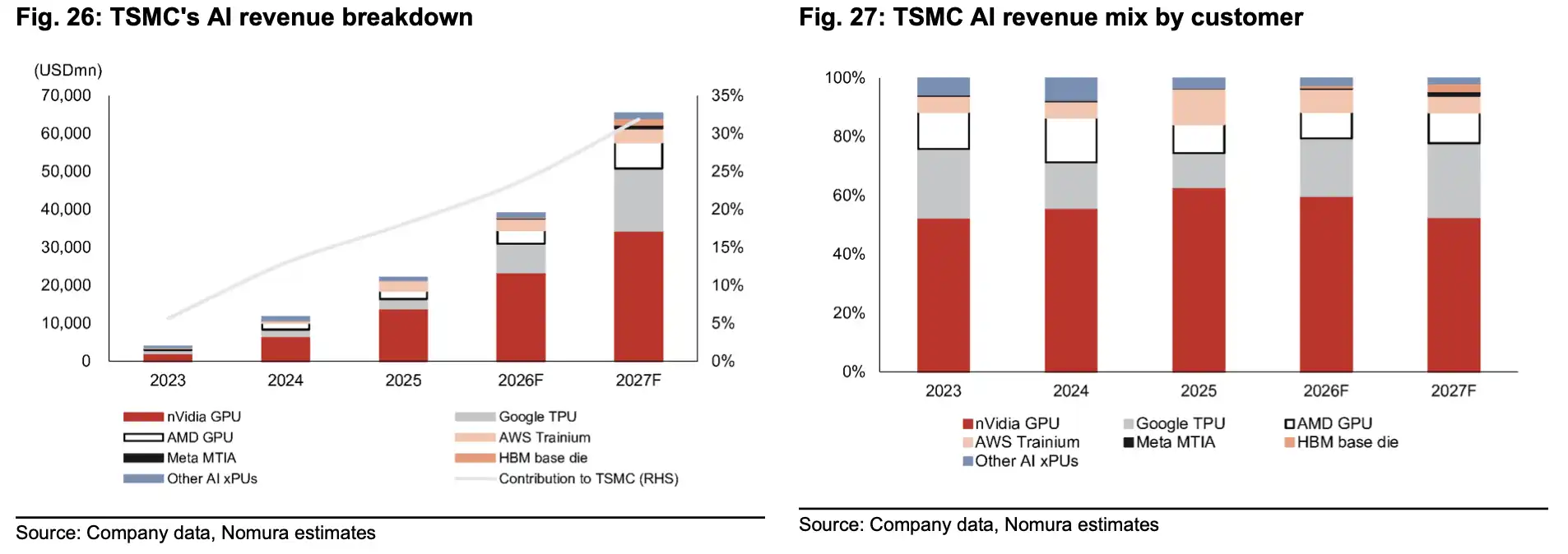

Nvidia Still Holds the Largest Share, Followed Closely by Google TPU

How advanced packaging capacity is allocated will determine which companies can access AI computing power more quickly.

According to Nomura's assumption, in the 2027 TSMC CoWoS capacity allocation, Nvidia is expected to continue to hold about 55%, but Google TPU's share will increase to around 26%, up from about 23% in 2026. AMD's share may see a slight improvement, while AWS's share is expected to decline year-on-year.

Behind this are large cloud providers and chip companies vying for advanced packaging resources. Nvidia remains the largest customer, and the increase in Google TPU demand indicates that in-house AI chips are receiving more capacity allocation. For MediaTek, the TPU outsourcing-related share is expected to increase from about 15% in 2026 to over 30%, which is also one of the reasons for the significant upward revision of its target price.

Nomura has raised MediaTek's target price from NT$3,400 to NT$5,800, representing approximately a 49.5% upside. ASE's target price has been raised to NT$730, EMC to NT$6,880, and ZDT to NT$720. These companies correspond to chip design, packaging testing, CCL, and PCB, reflecting the diffusion of AI infrastructure demand from "buying GPUs" to the entire hardware supply chain.

A stock price increase does not mean that all links will synchronize in realization. Capacity allocation, customer orders, material prices, and shipping pace will still determine the actual profit distribution. When customers such as Google TPU, AMD, AWS compete for packaging and component resources simultaneously, strong sections in the supply chain may experience price hikes, while weaker customers may be pushed to the back of the line.

The Cycle Hasn't Peaked, Cash Flow Pressure Persists

The premise of this round of expansion is that major cloud players will continue heavy reinvestment. Competition in AI models, growth in inference demand, and self-developed chip expansion will drive capital expenditure to remain high in 2027, even surpassing previous market expectations.

But risks lie in the same place.

The soaring cost of memory may lead some hyperscalers to face free cash flow pressure in 2027. If capital expenditure continues to rise and AI revenue realization lags behind hardware investment, investors will reevaluate the balance sheets and return cycles of cloud providers. Rising yields will also amplify this pressure, as higher interest rates will increase the funding costs of long-cycle construction projects.

Another frontier is the technology implementation beyond 2028. For advanced packaging to further expand, technologies such as EMIB-T, CoPoS, GPU-on-GPU SoIC, CPO, higher-speed SerDes, and next-generation PCB materials need to mature gradually. Any delays in key areas could impact the extension of the AI hardware roadmap.

The report does not present a conclusion of "risk-free AI hardware growth." A more realistic assessment is that current data center and server demand is still on the rise, TSMC's advanced packaging and component supply remain tight, and the AI infrastructure cycle has not yet seen a clear peak. However, beyond 2027, the cash flow of cloud providers, component bottlenecks, and technical execution will determine how far this cycle can go.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia