140 companies join forces to release OpenUSD, Circle's stock price plunges 16% in one day

On June 30, an organization called Open Standard announced the launch of the US dollar stablecoin Open USD (OUSD). The news itself was not uncommon. In the 2026 stablecoin race, new projects appear almost every week. What really made the market nervous was the names on the sign-up page.

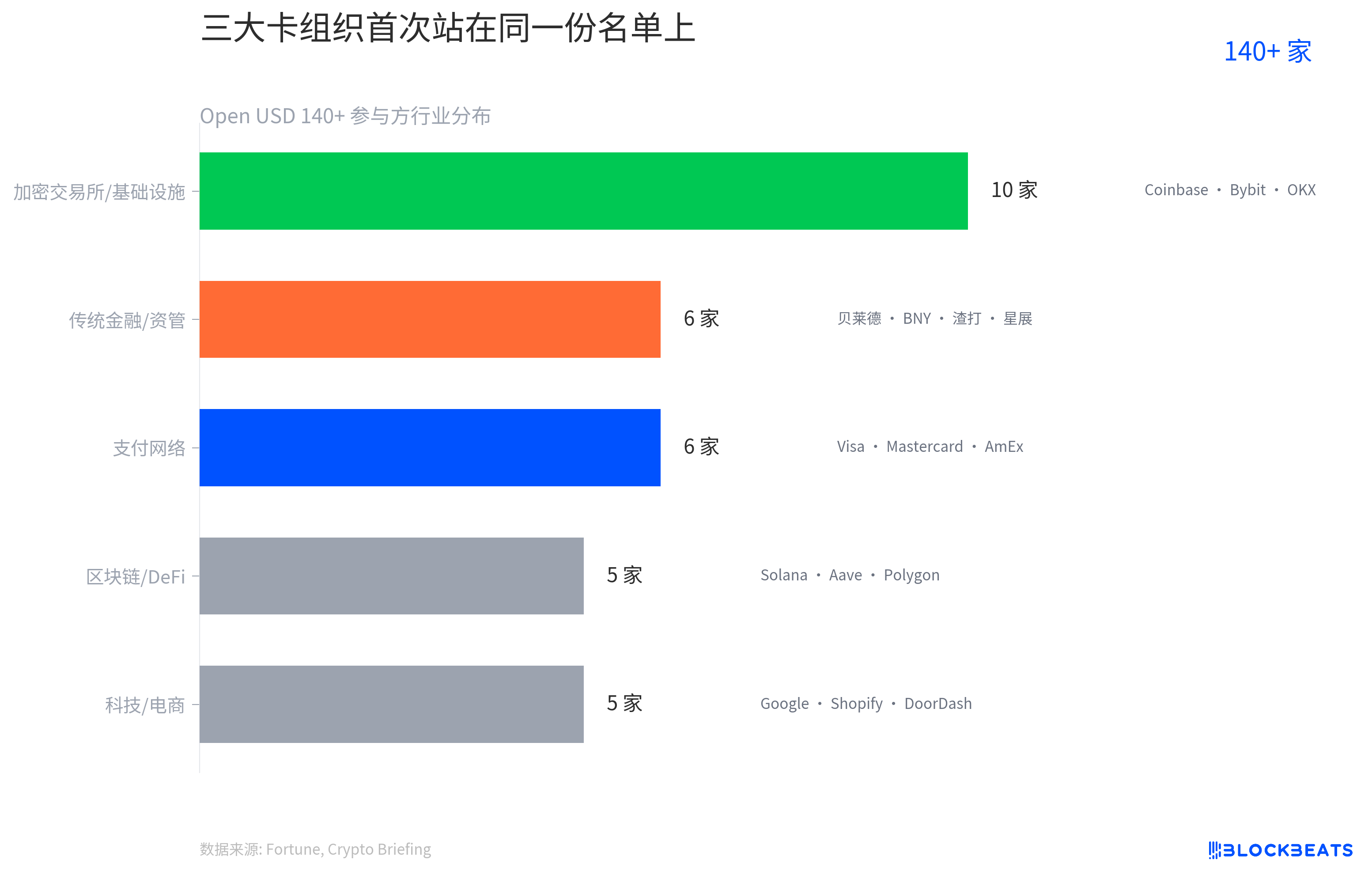

The initial participants in OUSD exceed 140, spanning the four major industries of payments, banking, crypto, and tech. Visa, Mastercard, and American Express, the three major card networks, appeared on the same alliance list. BlackRock, BNY Mellon, Standard Chartered, and DBS Bank represented traditional finance. Coinbase, Bybit, and OKX represented crypto exchanges. Google, Shopify, and DoorDash represented tech and e-commerce.

Following the announcement, Circle's stock price fell by about 16.5% on the same day, accumulating a 39% decline over the past month.

What Is Open USD?

The interim CEO of OUSD is Zach Abrams, the co-founder of Bridge. Bridge is a stablecoin payment infrastructure company that was acquired by Stripe for $1.1 billion in February 2025, marking Stripe's largest acquisition in history. Bridge currently processes over $10 billion in stablecoin payments annually, with clients including SpaceX. In February 2026, Bridge obtained a conditional national trust bank charter from the Office of the Comptroller of the Currency (OCC), gaining federal-level qualifications for stablecoin issuance and digital asset custody.

In other words, behind OUSD is not just a PowerPoint team but an infrastructure company that has already established a payment ecosystem, obtained a federal charter, and processes billions of dollars in payments annually. Stripe has brought the core asset it acquired for $1.1 billion to the forefront.

OUSD is scheduled to launch officially in the second half of 2026, initially deployed on the Solana, Polygon, Stellar, and Base (Coinbase's L2 network) blockchains. The participants in OUSD cover five industry sectors, forming a complete chain from issuance to usage.

This list is worth dissecting layer by layer. At the payment network layer, Visa, Mastercard, and American Express brought a merchant network covering over 100 million global acceptance points. In the traditional finance layer, BlackRock manages over $11 trillion in assets, BNY Mellon is the world's largest custodian bank, Standard Chartered and DBS cover key Asian markets. In the crypto infrastructure layer, Coinbase, Bybit, and OKX provide both trading liquidity and fiat on/off-ramp channels. In the tech and business layer, Google, Shopify, and DoorDash represent end-user scenarios.

Each layer did not come to the table empty-handed. They each brought their own existing network, users, and regulatory compliance to the alliance, giving OUSD a distribution capability that other stablecoins would take years to build.

This alliance structure has a historical mirror. In the 1970s, major U.S. banks faced a similar choice: each wanted to launch its own credit card, but the cost of building individual networks far exceeded a unified standard. They eventually merged their respective credit card projects into a member-governed alliance, which later became known as Visa. OUSD is doing the same for stablecoins. The difference is that this time even Visa itself sits at the alliance members' table.

Falling for a Month, Why Is Circle Nervous?

The business logic of stablecoins is not complicated. A user deposits 1 U.S. dollar, the issuer mints 1 stablecoin, invests this 1 U.S. dollar in U.S. Treasury bonds or other low-risk assets to earn interest. The interest goes to the issuer. When redeemed, the issuer burns the stablecoin and returns 1 U.S. dollar. The profit for the issuer comes from the time difference between minting and redemption.

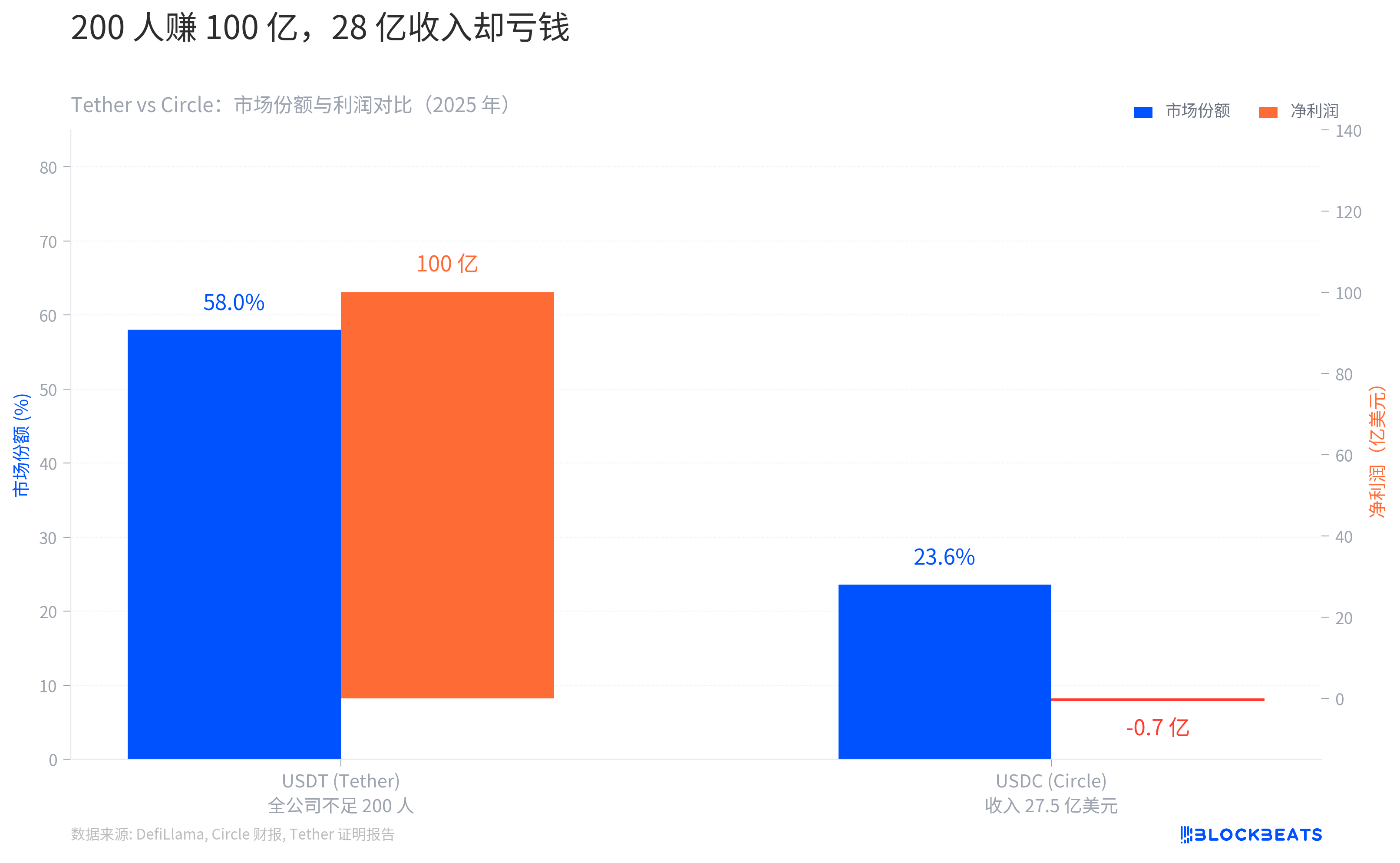

This model allowed Tether to earn over $10 billion in net profit by 2025. According to Bloomberg, this figure is higher than Goldman Sachs' profit for the same period, with Tether having fewer than 200 employees.

Circle's situation is different. According to Circle's 2025 financial report, total annual revenue was $2.75 billion, with approximately 96% coming from reserve interest. Revenue grew by over 60%, but the net profit was a loss of $70 million.

Why would a nearly $2.8 billion revenue company be losing money? The answer lies in distribution costs. In 2024, Circle paid Coinbase over $908 million in distribution fees, accounting for more than half of total revenue. Circle is essentially spending money to "rent" channels to promote USDC.

OUSD's design precisely hits this pain point.

OUSD's economic model has three core rules. First, minting and redemption are completely free, with no minimum amount. Second, the interest income generated by the reserves, after deducting a management fee, is proportionally distributed to all participants driving OUSD circulation. Third, governance belongs to the alliance, not a single company.

The power of this design lies in transforming "distribution" from a cost item into a revenue item. Circle needs to pay Coinbase to help promote USDC. In contrast, OUSD's participants come with their own channels, so promoting it earns them interest. Channel partners are no longer hired distributors but profit-sharing partners.

For Coinbase, this means a fundamental choice: whether to continue receiving Circle's distribution fee to promote USDC, or to promote OUSD and directly earn yield from reserves? Coinbase is already listed as a participant in OUSD.

However, OUSD was just the last straw that broke Circle's back, and the stock price has been falling for far more than just this one day.

According to Yahoo Finance data, after going public in June 2025, Circle reached a historical high of $263. One year later, OUSD announced a closing price of around $62 on the same day, marking a more than 75% decline from its peak.

The market cap of USDC has also shrunk, dropping from a year-to-date high of $800 billion to around $740 billion.

The market is pricing in three structural risks.

The first is interest rates. As mentioned earlier, about 96% of Circle's revenue comes from reserve interest, making its revenue essentially an interest rate derivative. According to Mizuho analysts, if the Fed continues to cut rates, Circle's forward revenue expectations could be reduced by 20% to 30%.

The second is the Coinbase renewal. The distribution fee-sharing agreement mentioned earlier is reported to expire and be renewed in August 2026. This timing coincides with the release of OUSD, with Coinbase already listed as a participant on the other side.

The third is regulation. According to CoinDesk, in March 2026, a Clarity Act bill was introduced in the U.S. Congress to restrict stablecoins from paying interest to holders, causing Circle's stock price to plummet by 18% in a single day. If this legislation is passed, it would directly narrow Circle's future space to attract institutional clients with interest-sharing.

With all three threads tightening simultaneously, OUSD became the biggest one-time acceleration in Circle's downward trend.

In the Face of the OUSD Impact, What Does Circle Have Left?

First, let's look at the competitive landscape. According to Tether's official attestation report, Tether's net profit exceeded $10 billion in 2025. According to DefiLlama data, USDT and USDC together account for nearly 90% of the stablecoin market share.

OUSD's Impact on Tether is Limited. Tether's moat is the emerging market's small-value payment network. According to DefiLlama data, in Q4 2025, USDT processed 2.33 billion small-value transfers, capturing 73% of the market. These transactions took place on the streets of Nigeria, Turkey, Argentina, not the main battleground of Visa and BlackRock.

Circle faces a more direct threat. The alliance members mentioned earlier, BlackRock, BNY Mellon, Standard Chartered, DBS, were originally Circle's target clients. When they participate in governing a stablecoin project themselves, Circle's narrative of "institutional trust" is diluted. Coupled with the fragility of the financial structure: the higher the revenue, the more money paid to the channel, the profits are actually compressed.

But Circle is not without a counterattack.

First, cross-border compliance. Circle is the first issuer globally to obtain the EU's MiCA stablecoin license, and in Europe, USDC has no short-term alternatives in terms of compliance. OUSD currently only has the U.S. OCC license, and cross-border regulation remains a blank slate.

Second, protocol embedding. USDC is the largest compliant stablecoin in the Ethereum DeFi ecosystem, integrated into hundreds of lending and trading protocols. This protocol-level integration is not something that can be duplicated by just issuing a statement.

Third, public company transparency. Circle is listed on the NYSE, publishes monthly reserve attestations, and undergoes audits by the Big Four accounting firms. In an increasingly stringent regulatory environment, this level of transparency is a real threshold.

According to McKinsey data, stablecoin payment transaction volume will reach $390 billion in 2025, doubling year-on-year. OUSD may not necessarily need to snatch market share from Circle. The real question is whether Circle can hold onto incremental markets.

When the channel itself becomes the issuer, the middleman's story becomes hard to tell.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia