Ethereum Falls Victim to Chinese Delisting Frenzy

Original Title: "Ethereum Falls as Chinese Concept Stock"

Original Source: Lord Wai Neck Mountain

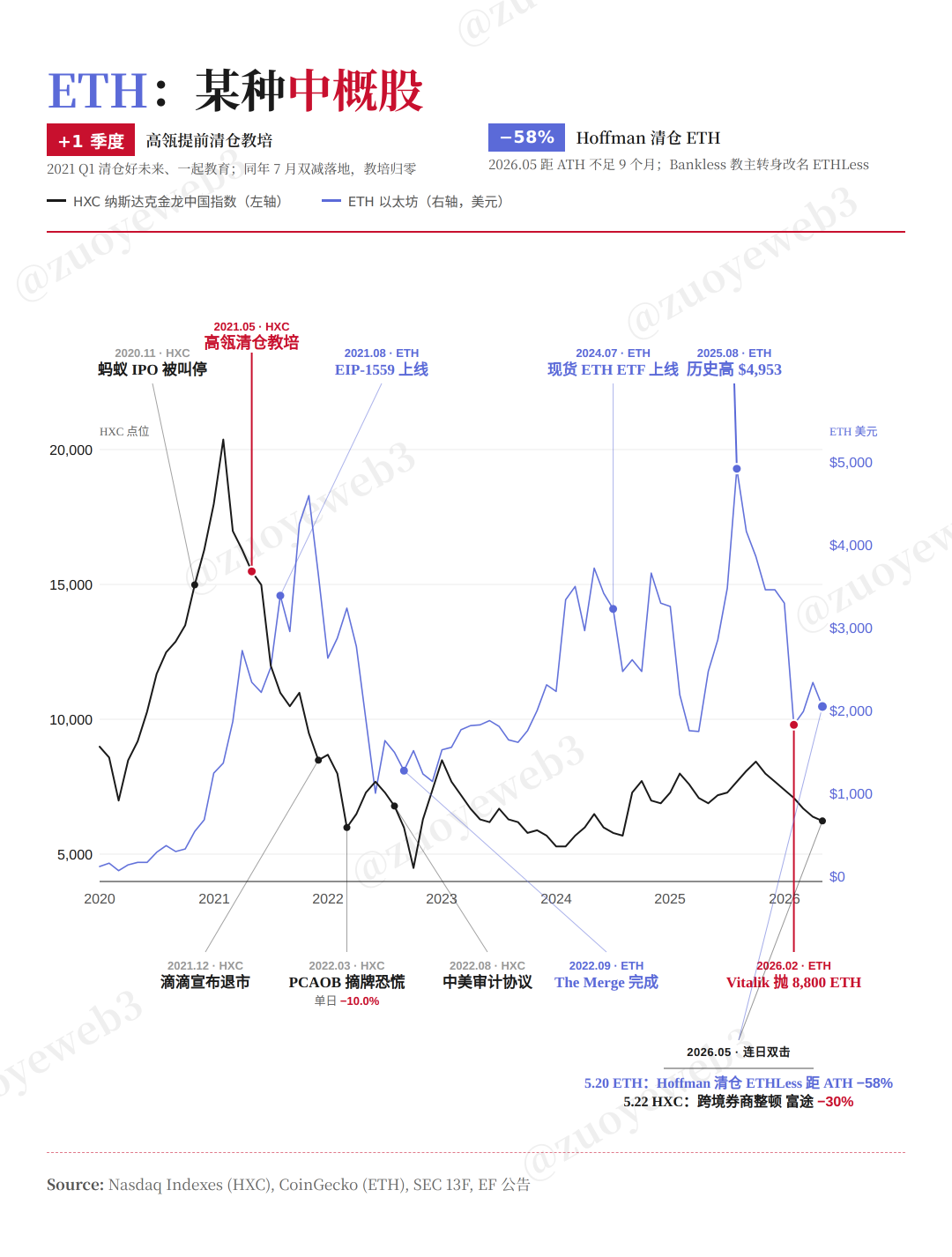

In 2023, the early Ethereum investment institution Pan-Asian sold off coins multiple times at an average price of $2,047. In May 2026, Bankless founder Hoffman liquidated his ETH holdings at a similar average price of around $2,000.

Bankless can be described as the Ethereum External Relations Department, single-handedly amplifying the top-tier meme concept "ETH is Money." During the 2021 bull market, the enthusiasm for ETH was equivalent to a strong bullish outlook on the future of blockchain.

Perhaps due to its significant status or the continuous departure of 8 members from the Ethereum Foundation, Ethereum's founder and spiritual leader Vitalik expressed his love in a lengthy post, admitting that the Ethereum Foundation only holds 0.16% of the ETH supply and should not have a position surpassing other ecosystem nodes. He also mentioned that he would gradually withdraw from operations, leaving Ethereum to its freedom.

Ethereum Has No Killer

ETH is Money?

Believe it or not, I choose to believe.

However, how did all this vanish? I am referring to the market's confidence in $ETH's price, holders' trust in the Ethereum Foundation and Vitalik. Currently, even in Ethereum's most dominant phase, why is there so much dissatisfaction, solely because of the coin's price?

If BTC experiences a major drop, it's a great buying opportunity. If SOL undergoes a significant drop, the extreme rebound after FTX has already proven its value. If HYPE faces a large drop, you can follow Arthur Hayes for swing trading.

Classifying it as a reason related to Vitalik personally is valid. Still, the abstract nature of public chain founders and foundations is not uncommon. Solana's founder Anatoly would actively associate with the Hyperliquid community to promote the Perp DEX concept. Ripple's multiple founders engaged in massive sell-offs of $XRP, not to mention the prevalent L2 era, where most founders are egotistical TGE maestros, as seen in the Movement community.

Upon closer comparison, while Vitalik may be abstract and the EF may be "inefficient," it is challenging to say that they caused Ethereum's current predicament. If they are not at fault, then it is the broader environment that is problematic.

Image Description: ETH is Money?

The most typical example is Chinese concept stocks, with an offshore structure, USD funding, and a U.S. stock IPO, creating a wealth myth of the past 20 years. Apart from trial products like Brilliance Auto and China.com, the true first Chinese concept stock was Sina.com in the year 2000, officially kicking off the Chinese concept stock wave.

The "U.S. concept + China implementation" division of labor model we see today is precisely the legacy of this system, and even Ethereum itself is a form of Chinese implementation moving towards global adoption, the last remnant of this legacy.

In 2014/15, Vitalik first stayed with Shen Bo, then received a $500,000 investment from Wanxiang led by Xiao Feng. Different from the mining model of $BTC, Ethereum's funding through an ICO, PoW mining, and then PoS staking brought three waves of passengers on board the same vehicle.

Or rather, ETH was a highly institutionalized system from the beginning. I do not mean to say that ETH is a strong whale coin, and indeed Vitalik hopes that the Ethereum Foundation (EF) will only become an ordinary node. However, the Ethereum ecosystem absolutely does not have an equal distribution of nodes, not in the past, not now, and not in the future.

In this situation, blockchain founders and foundations actually have to take on more functions, unrelated to token price. Precisely because of the warlordism within Ethereum, someone must step forward with relatively strong appeal to restrain the system's chaotic entropy increase.

But Vitalik chooses to first let the EF become bloated. From the Infinite Garden to the Ladder Theory, excessive abstraction has already left token holders at a loss, especially in the rsETH incident, where Aave founder Stani essentially acted as Duke Huan of Qi, suppressing the rebels.

Even the Solana Foundation set aside past grievances and actively supported DeFi United, only to receive the EF's usual selling pressure and Vitalik's silence.

Doing too much is a form of centralization. However, doing nothing, excessive restraint, is also a misuse of dominant status, a deliberate suppression of oneself, with the precondition of "considering oneself very important."

Therefore, Vitalik's choice to make the EF smaller in scale is a mistake. The correct approach would be for Vitalik to become an elusive youth, entrusting the foundation to a strong institutional entity, and acting more practically for Ethereum's future.

Apart from Bitcoin, all other public chains need to face the reality-based metrics of ecosystem development and adoption. In this regard, the Ethereum Foundation does not have a special status. The community's enthusiasm for DeFi and ETH is a memory of the past rather than a pure wealth effect.

From the perspective of ecosystem prosperity and real-world adoption, Ethereum's competitors have never succeeded. Solana may be anxious about Hyperliquid, but Ethereum is not, just as BTC is not anxious about Ethereum.

However, this favoritism is fading. The crisis does not come from external factors but from within. The real difference lies in who is responsible for ETH's price and who is responsible for Ethereum's direction?

Now Vitalik chooses to focus on privacy, but he should not "prevent" others from being responsible for the coin's price.

A New Narrative Awaits Valuation

Commodity or Productive money?

After the launch of $rsETH and Staking ETF, projects like BitMine are rapidly building Staking services, while players like Lido are more focused on the productive ETH narrative. For example, Spark only recognizes Lido's $wstETH product.

Everything is being reassessed. Lido is not as relaxed as it claims. With ETH's price lingering around 2000 for an extended period, the marginal-effect of scaling continues to diminish, and the pressure on maintaining APR returns increases, casting a shadow on the productive narrative.

This is the importance of price, or rather, who is responsible for ETH's price. The current situation is that the EF is not responsible, Lido cannot be responsible, and the entire Ethereum PoS system is operating in this awkward environment.

Continuing with a comparison to Chinese concept stocks, after effectively being unable to serve as exit routes on the U.S. stock market, Changxin Storage followed the AI concept, DeepSeek became state-owned, and the aerospace and robotics concepts swung between the A and H shares. Whether you like it or not, this is the new narrative architecture.

Image Description: Return to Mainnet.

After Ethereum transitioned to L1, Ethereum's mainnet activity surged, but you don't feel that the ETH ecosystem is truly improving, let alone the price going up. There must be a problem, but people cannot define the problem.

So what is the current Ethereum narrative?

1. Privacy: Everything can be ZK, which is also the last vestige of decentralization philosophy;

2. AI: The dAI team is bringing centralized architecture onto the chain, focusing on small model edge deployment and Agent invocation;

3. L1: Completely abandoning L2 centrality, all speed and revenue return to the L1 battle.

Compared to the "world computer" and smart contract technology collaboration, Ethereum is already establishing more connections with reality. In addition to the above three, there are also narratives such as stablecoins, RWAs, and many more. However, these are not the world in Ethereum's eyes, but Ethereum in the world.

The reversal of subject and object, or rather the lack of clarity about its position in the new world, everything can be put on the chain. The blockchain's grand ambition to battle the future is no longer there. However, there is always a feeling that blockchain can do more. This contradiction, entanglement, and back-and-forth constitute the triple wave of market sentiment today. People hope to see a better Ethereum, but it is unlikely to see a good Ethereum.

After more than a decade of struggle, Ethereum has not become a world computer, but it is indeed an open computer where any activity and concept can be experimented and run. At the time of Bankless promoting ETH is Money, Vitalik insists that ETH is a Commodity, a digital product that carries specific functions.

On this point, people cannot accuse Vitalik of lying. In February 2026, Vitalik sold 8800 coins. He also slowly sold on CowSwap, not like the Curve founder who staked $CRV to mint stablecoins, or like Sun who manipulated $USDD to liquidate retail.

But just like in the Chiang Mai dialogue of January 2026, if time were to go back ten years, and everyone had to choose between blockchain and AI, Vitalik did not give a firm answer. However, the fact is certain that more and more projects in the crypto world are shifting towards AI, operating with a proficient GTM methodology.

· The Hermes Agent has come out to mainstream AI developers, with the founding team coming from Nous Research;

· xBubble developed by DappOS, combining AI + intent execution framework;

· OpenRouter, founded by Alex Atallah from OpenSea.

You will find that the marketing capabilities of crypto projects are not limited to on-chain activities. Even in the midst of the globally acclaimed AI trend, they can keep up with the pace time and time again. They are also involved in pathways such as stablecoins, traffic distribution, and operational entanglement.

However, all of this has a weak connection to Ethereum. Although dAI and virtuals jointly proposed ERC-8183, attempting to define the Agent's autonomous economic activity framework, it cannot be said that the team is inactive. It is more like a proactive adaptation rather than a leadership posture.

If we consider the present as a bottom-fishing moment in terms of narrative, the key question is: What value does a public chain bring in the AI era?

Claude repeatedly strikes at SaaS, security, and external Agent frameworks. We can imagine an absurd scenario: What if Claude were to create its own blockchain? How would Ethereum react?

Under the PoS mechanism, the cost of asset migration is sufficiently low. However, in terms of compliance costs, Claude would still be subjected to human legal limitations. The unfettered playground of free finance is perhaps Ethereum's most unique value proposition.

Just as Mythos severely impacted Palantir's stock, Qi An Xin will rise against the tide, because hitting one's opponent triggers an arms race among peers across the ocean, leading to an infinite loop.

Or perhaps, in today's world where antagonistic emotions are on the rise, the demand for global connectivity will persist in the long term. While Canton belongs to Wall Street, Ethereum belongs to all humanity. Just like people in the Sahara Desert without shoes, pessimists withdraw while optimists rejoice.

However, the golden age of $ETH will not return. Wanxiang, EF, and other institutions may sell, but 2000 ETH is at least 10 times the value of 200 ETH. We are standing at a new starting point; all we need is a clear direction.

Conclusion

Fatefully similar, Ethereum's destiny truly mirrors that of Chinese concept stocks. Both are assets of Country A, invested in by Country B's capital, and exit on Country B's secondary market, with Country A only bearing market and corridor value.

This is the best of times; under fragmentation, new markets will emerge. By taking cues from Country B's dynamics, assets similar to Country A's will undergo a similar cycle. Under fragmentation, both Country A and Country B will need new connecting points, and Ethereum remains the best choice.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia