Citi Interpretation: NVIDIA still has 47% upside, can Rubin and CPO deliver?

TL;DR

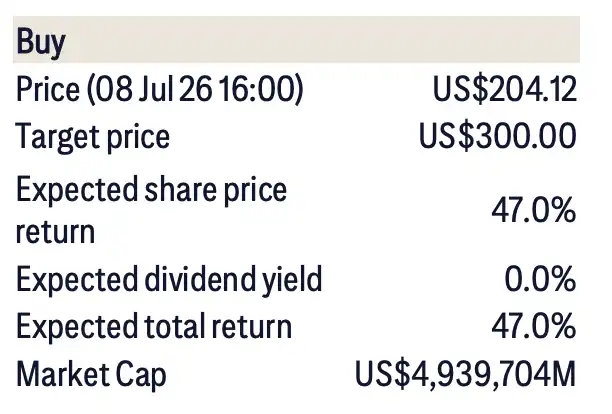

· Citi maintains NVIDIA at Buy with a $300 price target, implying about 47% upside from July 8th closing price.

· Communication notes AI demand remains strong, Rubin roadmap largely unaffected, CPO now in early production.

· The $100 billion revenue per GW is not a direct income forecast, non-cloud demand, CPO adoption, and AI payback still need validation.

Following discussions with NVIDIA's investor relations team, Citi has reiterated its Buy rating on NVIDIA and $300 price target. Based on the July 8th closing price of $204.12, this target price represents about 47% potential upside. For an AI leader with a market cap approaching $500 billion, the market's focus is not only on whether GPUs are still in demand but also on whether AI capital expenditures can continue to translate into revenue, if the next-generation platform will face delays, how network and power efficiency bottlenecks will be addressed, and whether high gross margins and buybacks can sustain the valuation. It is important to note that specific expressions such as Rubin, CPO, and revenue per GW intensity mainly come from Citi's communication notes and are not part of NVIDIA's officially disclosed full narrative.

NVIDIA Buy Rating Key Data. July 8th closing price $204.12, target price $300, expected return approximately 47%, market cap around $494 billion.

$300 Price Target Betting on Sustained Demand

Citi's $300 price target is primarily based on growth expectations in the data center business. Their valuation approach indicates that the target price is based on the FY2027 earnings outlook and a valuation multiple close to NVIDIA's average over the past three years. In other words, this assessment does not heavily rely on a higher valuation but rather on the belief that there is still room for earnings growth.

The demand outlook is relatively strong. Regarding the market's focus on the Meta cloud plan, NVIDIA did not provide specific customer-level comments, but emphasized in the communication that overall demand remains robust, with the company's current focus still on meeting customer needs to the best of its ability.

The demand structure is also evolving. While large-scale cloud providers dominated past AI infrastructure deployments, the past two years have seen an increase in AI labs, sovereign nations, and on-premise enterprise deployments. The assessment in the communication notes is that as "Physical AI" applications develop, the market beyond large-scale cloud providers may become even larger in the future.

This is still a projection, not a realized outcome. For investors, the more direct question is whether AI labs, sovereign AI, and on-premise enterprise deployments can generate ongoing orders, rather than providing only temporary supplements outside of peaks in cloud provider capital expenditure.

Rubin Delays Unchanged Roadmap, CPO Moves to Early Production

The market's concern about NVIDIA's roadmap is focused on whether the next-generation GPU platform and system interconnect solution can proceed as planned. A Citigroup communication note stated that the management indicated that the delay related to Kyber Rubin Ultra does not impact the overall roadmap, and the NVLink domain configuration showcased at Computex remains unchanged.

This is crucial for NVIDIA. In the AI server competition, it is no longer just about the performance of a single GPU, as the cost of training and inference is determined by the entire cabinet, cluster, network interconnect, and energy efficiency. If there is a significant roadmap delay, it will affect cloud providers' procurement pace, customer migration plans, and the market's assessment of NVIDIA's long-term gross margin.

Another focus is on CPO, i.e., Co-Packaged Optics technology. By bringing optical interconnect closer to the chip package, it reduces the power consumption and latency of high-speed data transmission, making it a key technology for future AI cluster expansion. According to Citigroup's note, NVIDIA stated that CPO has entered scale-out production with Spectrum-X, and customer adoption willingness is high.

However, this is not yet a full commercial deployment. The note mentioned that a clearer choice may start to emerge from the 2028 fiscal year Feynman platform, where customers can choose between NVLink combined with CPO or continue to use a copper cable solution. In other words, CPO is transitioning from concept validation to early production, but further disclosure is still needed regarding customer adoption rates, cost advantages, and large-scale delivery cadence.

This statement is more restrained than simply emphasizing a "CPO breakout." It indicates that NVIDIA is paving the way for the next-generation AI clusters in advance, but the technical roadmap is optional, and it does not mean that customers will immediately switch on a large scale.

"$1 Trillion per GW" Cannot Be Directly Interpreted as Revenue Forecast

The most misinterpreted figure in the communication is the long-term "1 Trillion per GW" proposition previously put forward by Jen-Hsun Huang. The explanation in the Citigroup note is that this should be understood more as a long-term trend in efficiency and revenue intensity, rather than a revenue forecast that can be directly applied in any given year.

The current level is around $300 to $400 billion per GW. If the GPU's energy efficiency continues to improve with each generation in the future, allowing for more powerful computing under the same power constraints, the revenue density generated by AI infrastructure will also increase. The note mentions that the Blackwell GPU delivers a 25x improvement in power efficiency compared to Hopper, which is a key foundation for the increased revenue intensity per GW.

This logic is based on two premises. First, chip, network, cooling, and system design have indeed continued to increase power efficiency. Second, customers can obtain sufficient returns from AI applications and are willing to translate higher performance into more capital expenditure. If the ROI on AI investments improves, the revenue density per GW may increase. If the monetization of applications falls below expectations, the realization of this long-term goal will be delayed.

Therefore, the "per GW $100 billion" is more like NVIDIA's depiction of long-term infrastructure efficiency and should not be simply understood as a fixed revenue target.

Gross Margin and Buybacks Support Valuation, but High Growth Needs to Materialize

From a financial perspective, NVIDIA's latest official guidance indicates that the Q2 FY2027 gross margin is expected to be in the mid-70% range, with a GAAP gross margin of 74.9% and a non-GAAP gross margin of 75.0%, fluctuating up and down by 50 basis points. For a nearly $5 trillion company, the ability to maintain a high gross margin is a key factor the market is willing to keep a high valuation for.

Capital return is also being given more importance. In Q1 FY2027, NVIDIA returned approximately $20 billion to shareholders and added an $80 billion buyback authorization, raising the quarterly dividend to $0.25. Citigroup notes that the management's goal is to return 50% of operating cash flow to shareholders this year.

The recent $25 billion bond issuance has also attracted attention. Public filings and media reports indicate that this is NVIDIA's first bond issuance since 2021. The company and the market interpret this move more towards enhancing financial flexibility rather than a signal of deteriorating cash flows.

However, risks have not disappeared. Citigroup's listed downside factors include gaming business competition leading to market share loss, slowing adoption of new platforms, volatility in automotive and data center sales, and changes in crypto mining demand. For the current NVIDIA, the biggest constraint is still whether the AI infrastructure construction can sustain high-intensity advancement and translate into real customer revenue.

Frontier Vision Adds Points, but Short-Term Focus Remains on Orders and Deliveries

In addition to the main issues, NVIDIA has also addressed some cutting-edge and tangential topics. The company recently released open models such as Nemotron, Cosmos, and Alpamayo, aimed at helping sovereign nations and enterprises accelerate AI adoption rather than directly competing with cutting-edge closed-source models.

Space computing is also part of the long-term narrative. NVIDIA has officially released the NVIDIA Space-1 Vera Rubin module for orbiting data centers and space computing. Similar directions still face significant engineering challenges and are not the primary basis for supporting the $300 price target in the short term.

On the external technology integration front, the Citi report mentioned that NVIDIA has not officially announced a partnership with d-Matrix yet, but management has stated that the company is always willing to evaluate and integrate external technology. The related statements are still in line with the communication strategy and should not be seen as a concrete collaboration in place.

Citi has given nearly a 50% upside potential, with the key support remaining in AI demand, platform roadmap, network upgrades, and high gross margins. In the end, the market will be looking at the details of CPO adoption, delivery cadence ahead of the Feynman platform, whether non-hyperscale customer orders can continue to increase, and whether the revenue strength per GW can be validated in real AI application returns.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia