Storage Export Data Surges, Market is Resetting Storage Valuation Anchor

TL;DR

· According to Citrini analyst Jukan's summary, on June 20th, South Korea saw a significant year-on-year increase in the export value and per kilogram price of various types of storage, but this data is still considered preliminary based on social media summaries.

· This dataset further strengthens the assessment of AI memory overflow demand, but MCP cannot be directly equated to HBM, and the per kilogram price is not equivalent to a several-fold increase in the price of a single chip.

· Related companies: SK Hynix, Samsung, Micron, Nvidia.

On June 20th, the significant year-on-year increase in the export value and per kilogram price of various types of storage in South Korea has sparked a market discussion on whether storage manufacturers are benefiting from an AI infrastructure bottleneck premium.

The importance of this event lies not only in the addition of another set of semiconductor export figures but also in its simultaneous impact on two variables that investors are most concerned about: an increase in shipment value and a corresponding increase in export value per unit weight. The former points to demand strength, while the latter indicates a shift in price and product structure towards higher-value products. For storage stocks, this is more substantial than simply "selling more," as it will affect revenue, gross margin, and EPS upside potential.

Over the past year, the market has acknowledged that HBM (High Bandwidth Memory) is a scarce resource in AI servers. The controversy lies in whether this scarcity is only leading to price increases for a few high-end products or has already begun to overflow into a broader spectrum of the DRAM, NAND, SSD storage chain. If it is the former, storage stocks still resemble more of a cyclical recovery trade. If it is the latter, the valuation anchor of SK Hynix, Samsung, and Micron may shift from a "inventory cycle" to a "AI infrastructure bottleneck" narrative.

The data from South Korea provides a strong signal, not a conclusion. Especially the export data for specific categories and per kilogram price on June 20th are currently more suitable as preliminary observations under a social media summary calibre and cannot be directly used as official complete confirmation. Its value lies in advancing a narratively biased issue to a stage where trade value, price indicators, and company guidance can be cross-validated.

South Korea's Export Provides a Price Signal to the Market

The most direct implication of this dataset is that the storage prosperity may not only involve shipment volume recovery but also increasing prices and product portfolios.

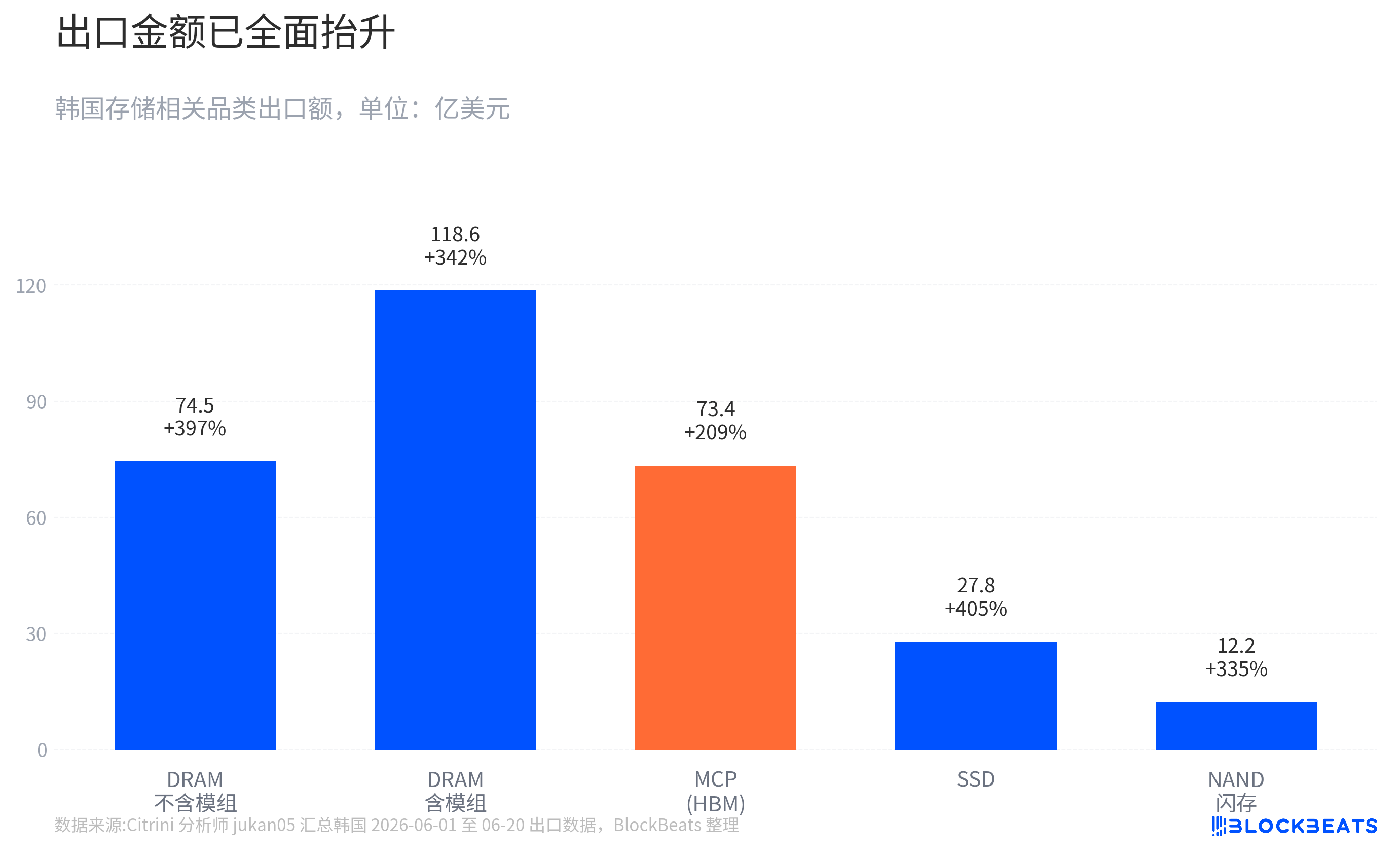

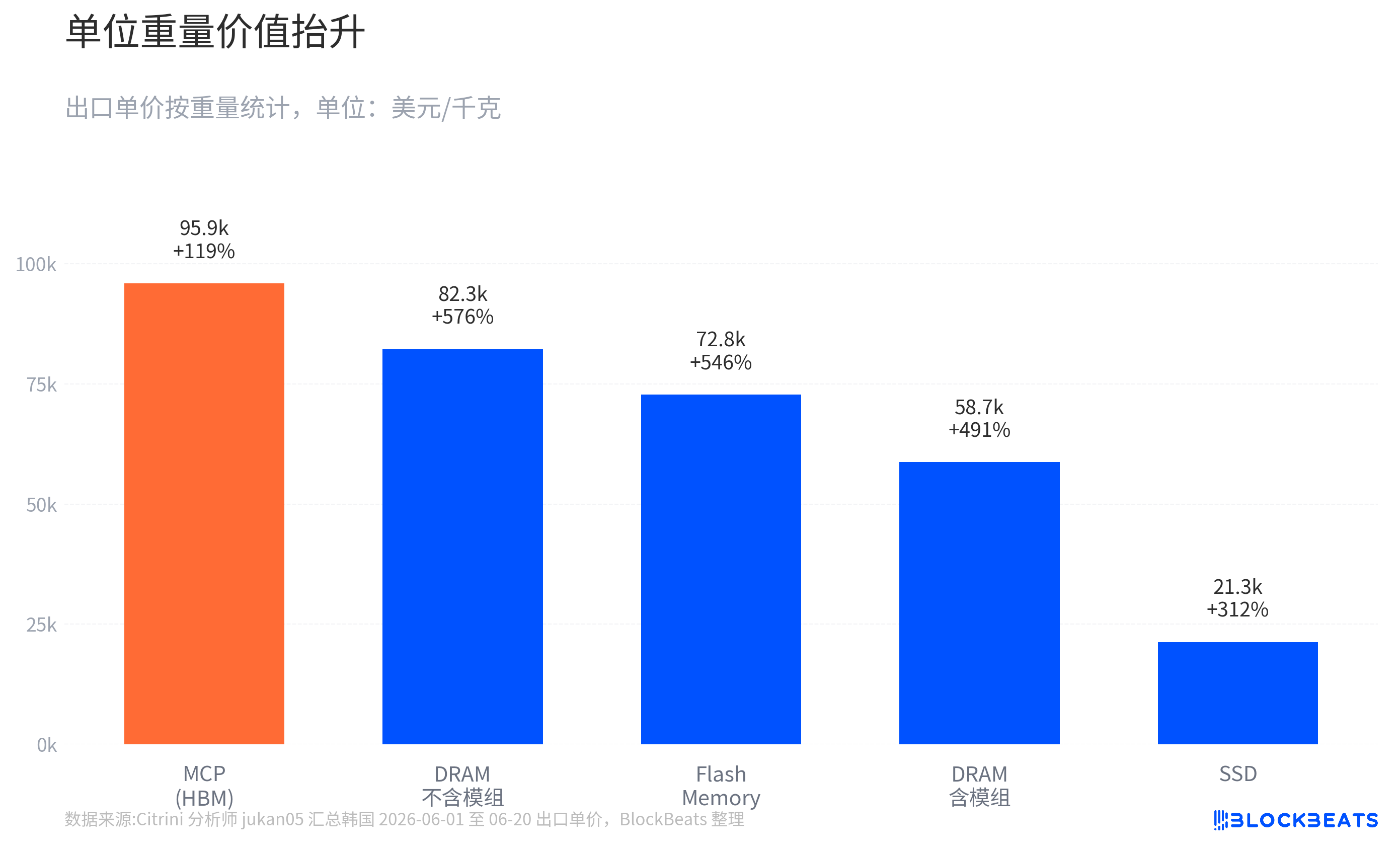

Preliminary export data from South Korea for the period of June 1st to 20th shows that the export value year-on-year growth for multiple categories such as DRAM, NAND/Flash, MCP, and SSD are all in a high-growth range. Among them, the export value of non-module DRAM saw a nearly fourfold year-on-year increase, while the export value including the module grew by over threefold year-on-year. NAND/Flash and SSD export values also saw significant growth. Of greater market interest is the per kilogram price, with some categories related to DRAM and NAND experiencing year-on-year growth rates exceeding 500%.

These numbers need to be taken with a grain of salt. The data for the first 20 days is more like a mid-month snapshot of South Korean trade data, which can provide a directional trend and slope but is not the final monthly data. The classification of detailed product categories may also not align perfectly with the product categories investors understand, so it is not suitable for directly extrapolating into an annual profit model.

A more stable reference comes from the already published May data. According to reports from South Korean media based on official data, South Korea's total exports in May were $87.75 billion, a year-on-year increase of 53.2%; semiconductor exports were $37.16 billion, a year-on-year increase of around 169%, reaching a new monthly high and accounting for 42.3% of total exports. Exports of computers and related equipment also saw significant growth, with the media linking it to AI server and SSD demand. Preliminary exports from June 1st to 10th were also strong, with total exports at $28.6 billion, an 86% increase year-on-year, and semiconductor exports around $11 billion, more than tripled from the previous year.

This validates the social media summary data from the first 20 days of June as no longer just an isolated signal. It aligns with the previous official export trends. For investors, continuity is more important than a one-time spike because it determines whether earnings upgrades can shift from a one-time surprise to a multi-quarter model adjustment.

Sharp Increase in Kilogram Price Does Not Equate to Fivefold Chip Price Increase

The most easily misunderstood aspect of this dataset is interpreting the sharp increase in kilogram price as a direct translation to "several times increase in chip price per unit." A more accurate statement would be that the kilogram price reflects a combination of price increases, product structural upgrading, and statistical nuances.

Some categories in South Korea's export data calculate the average price based on weight. For commodities, this metric is easily understood. However, for semiconductors, the value difference per kilogram of the same product can vary widely. The value density of one kilogram of low-end memory chips is not comparable to one kilogram of HBM, high-capacity DRAM, or complex packaged products. The rise in kilogram price could be due to price increases in similar products or a shift in the export structure towards higher-value products.

This is precisely the core of AI trading. AI servers require memory systems with higher bandwidth, larger capacity, and lower latency. The value density of HBM and high-end DRAM far exceeds that of ordinary storage products. As the proportion of these products in the export structure increases, the average export value per kilogram is elevated. The market is not witnessing a uniform fivefold price increase in all memory chips but rather an increase driven by the rise in high-end product share coupled with price hikes, which is transforming the revenue quality of the memory chain.

Special care is also needed regarding MCP metrics. The market often uses MCP as a proxy indicator for HBM because HBM often involves multi-chip stacking and packaging. However, MCP (multi-chip packaging) is not equivalent to strict HBM, as it may also include other multi-chip packaged products. While the strengthening trend in MCP exports in both amount and price can support the assessment of "strong demand for high-end memory packaging," it should not be directly equated to HBM export value.

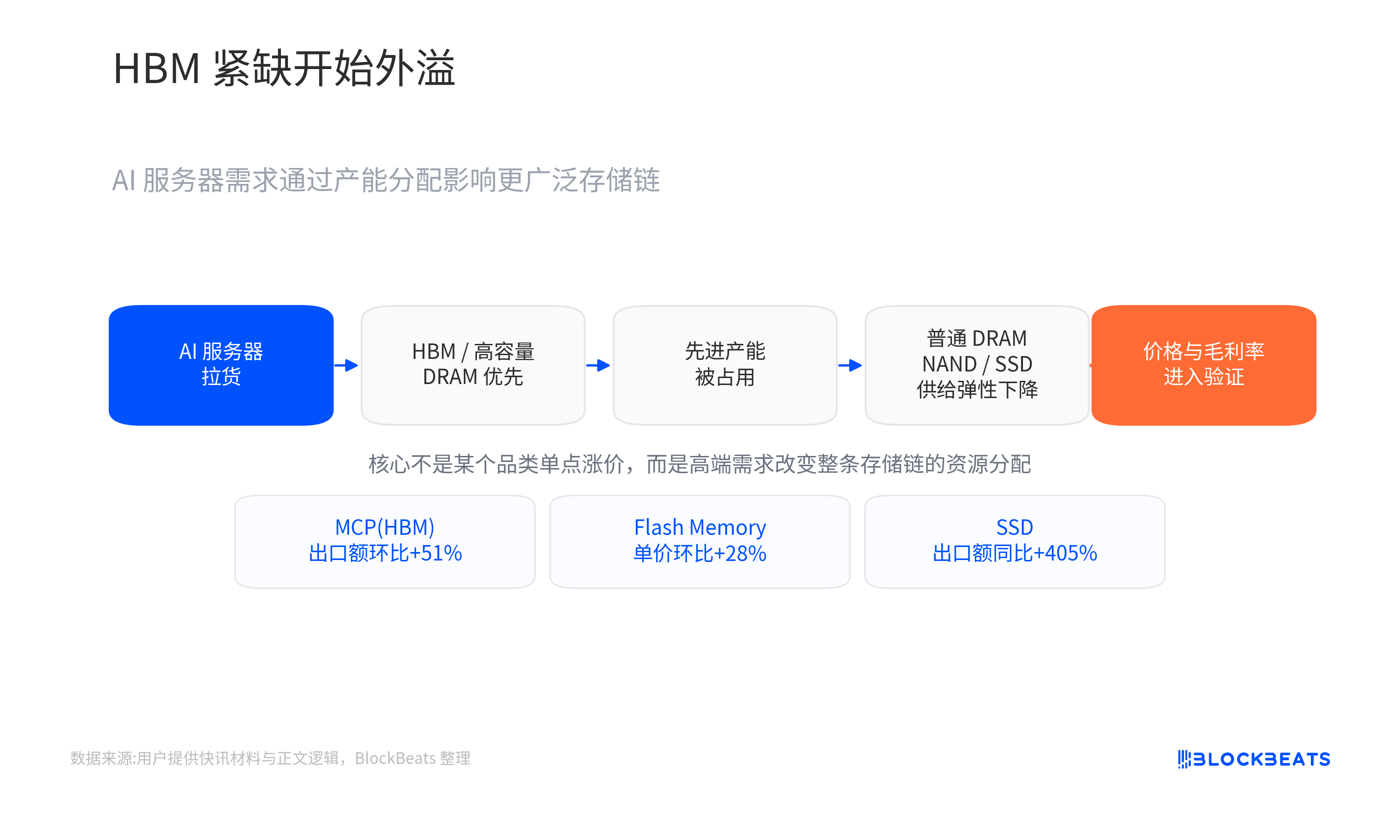

This constraint does not weaken the value of the data; instead, it makes it more suitable for investment analysis. The truly useful conclusion is not the precise increase in the price of a certain product category but the simultaneous increase in both the amount and unit value of multiple storage categories. This demonstrates that the demand for AI may no longer be limited to just HBM. It is influencing a broader storage pricing system through capacity allocation, product structure, and customer procurement.

HBM Shortage Alters Storage Vendors' Pricing Position

If we only look at HBM itself, the market has long been aware of its shortage. The new question is why the HBM shortage is affecting DRAM, NAND, and SSD.

The mechanism is not complicated. Storage vendors have limited advanced capacity, R&D resources, and customer certification capabilities. When NVIDIA and cloud vendors continue to lock in HBM, high-capacity DRAM, and other high-value products, vendors prioritize allocating resources to directions with higher returns and stronger order visibility. This will keep the supply of high-end products tight and may indirectly squeeze the supply elasticity of mainstream DRAM, NAND, and SSD.

SK Hynix is the most direct beneficiary of this logic. It is widely believed in the market that its HBM market share is in a leading position. According to industry reports and brokerage reports, SK Hynix's 2026 HBM capacity has high visibility, customer demand exceeds supply, and sales of high-value-added products are growing. For a storage vendor, customer pre-allocation of capacity and the growth in high-end product sales will change not only the revenue for the next quarter but also the market's assessment of its pricing power. The core issue for a traditional cyclical stock is how much prices can rise, and the core issue for a bottleneck asset is how much premium customers are willing to pay for a guaranteed supply.

Samsung and Micron have slightly different logics. Samsung has a larger scale in NAND and overall storage capacity and is still chasing after high-end HBM customer certifications. Micron benefits from the expansion of high-end memory demand and a diversified supply chain. For these two companies, the market is not trading whether they have completely replicated SK Hynix's HBM pricing power, but if the HBM shortage spills over to high-end DRAM, enterprise SSD, and NAND prices, their gross margin elasticity will be stronger than in the previous cycle.

Intel CEO Pat Gelsinger mentioned in a No Priors interview that the AI infrastructure bottleneck is shifting from GPUs to memory, CPUs, optical interconnects, power conversion, advanced packaging, materials, and other areas. The key point here is not to rewrite the issue as part of Intel's strategy but to illustrate a broader context: the constraints of AI data centers are no longer just about a GPU. Any bottleneck that restricts cluster expansion and efficiency could gain new pricing power.

Memory is one of the earlier links observed in trade data. No matter how powerful the GPU is, it still needs sufficient memory bandwidth and capacity to feed data. With the increasing demands of inference and AI agent tasks, the system's requirements for memory, storage, and scheduling resources will become more complex. The value of South Korea's export data lies in its ability to translate the somewhat macro-level judgment of "AI infrastructure bottlenecks diffusion" into changes in storage export amount and unit value.

Memory Stocks Still Subject to Cycle Constraints

For investors, this round of storage price increases is more like a combination of "accelerated reality prosperity and future profit revaluation" rather than just storytelling. The export data indicates that demand and prices already have real-world support, and what the market is truly buying into is whether the 2026 revenue, gross margin, and EPS will continue to improve.

If subsequent financial reports validate this trajectory, the premium valuation for SK Hynix is most easily explained: leading HBM share, customer lock-ins, and the ramp-up of high-value-added products together contribute to higher visibility. For Samsung, the key lies in whether the catch-up in high-end HBM can translate into actual orders, and whether NAND and SSD prices can form a broader support. Micron needs to demonstrate that the price increases in high-end DRAM and data center storage can penetrate through to gross margins and guidance.

Risks are also present here. Storage remains a cyclical industry, where supply expansion, inventory changes, and customer procurement pace can all influence prices. Preliminary export data for the first 20 days can indicate a steepening slope, but cannot prove year-long certainty. The rise in kilogram unit price can indicate increased value density but cannot entirely separate the proportion of average selling price increase from product structural changes. The strengthening of MCP can serve as a proxy signal for HBM, but is not directly equivalent to HBM exports.

Another risk comes from AI capital expenditures themselves. If there is a slowdown in investments in power, cooling, packaging, or overall computing power, storage demand will also be affected. The diffusion of bottlenecks is both the reason why storage receives a premium and a potential constraint. When other parts of the system bottleneck first, the pace of memory demand release may also be delayed.

Earnings Reports Will Determine Whether Valuation Anchors Can Shift

This round of revaluation will ultimately come down to company financial statements rather than just staying at the level of trade data. The official full-month export data for June will first provide the market with a more comprehensive confirmation: whether the high growth in the first 20 days continues, whether price indicators remain at elevated levels, and whether the strength in NAND and SSD is merely a short-term spike driven by large orders.

A more critical validation will come from SK Hynix, Samsung, and Micron's Q2 and Q3 earnings reports. The market needs to see HBM shipments and prices continue to materialize, improvement in both DRAM and NAND average selling prices, data center SSD demand driving gross margin expansion, rather than just reflecting in revenue scale. If gross margins and guidance fail to keep up with the slope indicated by export data, the revaluation will quickly revert to cyclical trading.

The current and more prudent assessment is that South Korea's pre-20th-day export data has been strong enough to support market expectations for memory manufacturers' profit resilience and to revisit the AI infrastructure bottleneck premium. However, it is still not sufficient to prove that the memory industry has emerged from the cycle. The key to determining whether the valuation anchor can shift is not how high a specific year-on-year number is, but whether prices, product structure, and profit margins can hold up simultaneously over the next few quarters.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia