The silver moon shines brightly, how much longer will the silver rise?

Original Article Title: Silver Moon

Original Article Author: @abcampbell, Ex Bridgewater

Original Article Translation: SpecialistXBT, BlockBeats

Editor's Note: This article analyzes how irreversible industrial demand, a rigid supply bottleneck, and strategic capital inflows have become the driving force behind the silver price surge, while calmly pointing out potential risks such as a dollar rebound and technological substitutes, providing investors with a "compass" to observe the true strength and weakness of the market.

The following is the original content:

It has been a month since we last discussed silver.

A month ago, the annual price increase for silver was 45%.

Do you still remember when I said the situation was about to become "alarming"?

Over the past year, silver trading has gone from being quietly unnoticed to a prominent bull market, and then to a significant historical turning point. The driving factors we pointed out years ago—such as the rigid demand brought about by solar energy, the rigid supply caused by mining dynamics, Volcker-style speculative fund flows, investors' strategic purchases to diversify dollar risk, the worrying capital outflows from the banking system in emerging markets, and strategic hoarding behavior—are now all evident and in full force.

However, this upward trend is not like a celebration but more like a doomsday clock ticking. It is not aimed at silver itself but at the U.S. dollar and the global order it supports. It is a signal, foretelling a world where our descendants will live, vastly different from the world of our ancestors.

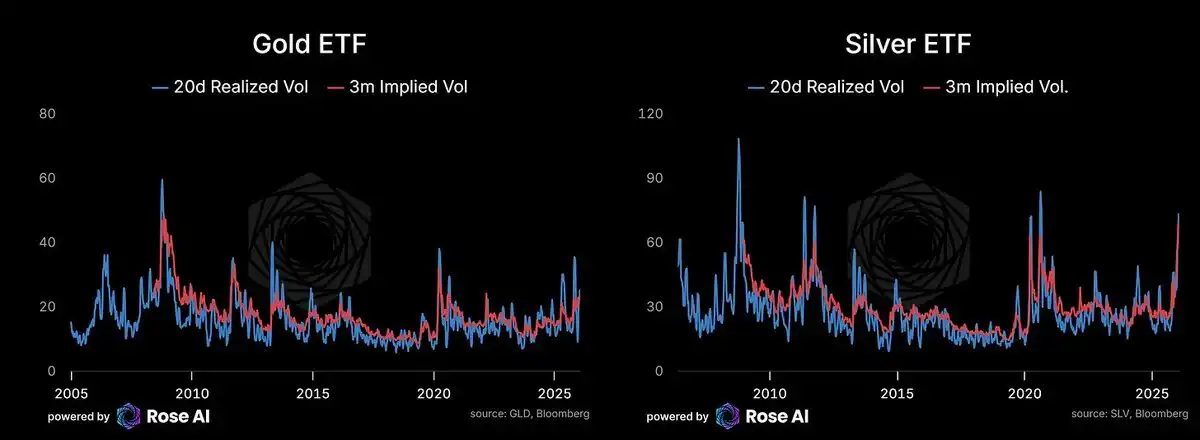

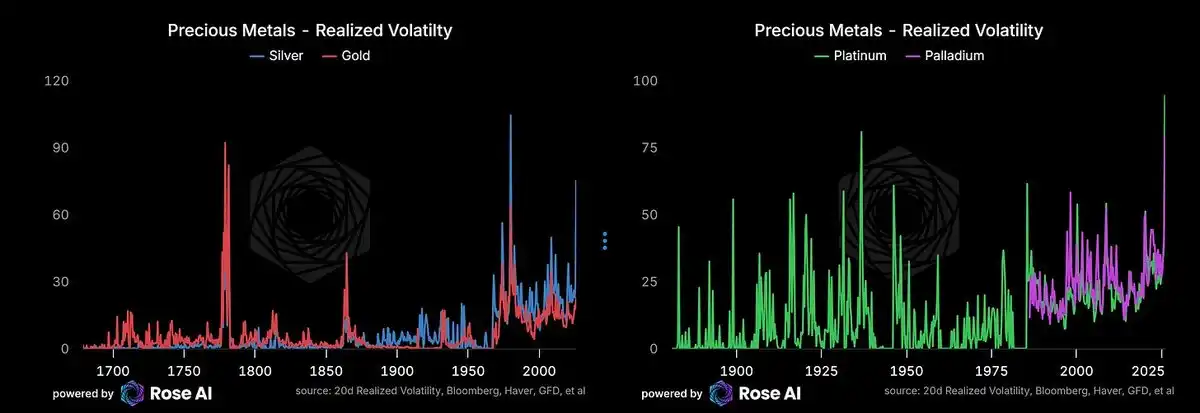

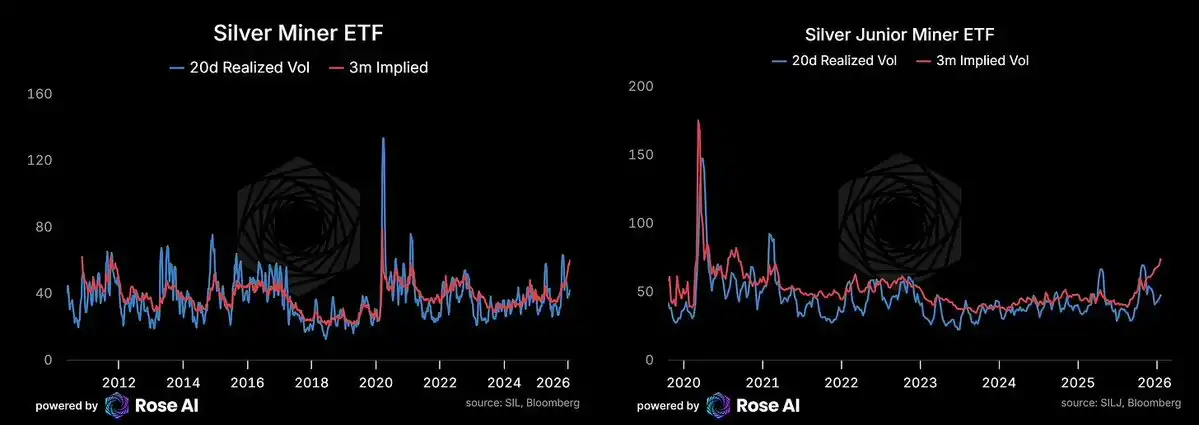

The options market is pricing in a future daily volatility of over 4% for the coming months, expected to remain at 3% volatility for the foreseeable future. This has been corroborated by realized volatility. In recorded history, there have only been two periods of higher silver volatility: during the Hunt Brothers' squeeze in 1981 and during the American Revolutionary War (where the volatility stemmed from the local currency's collapse against the pound, not from metal price changes).

Gold volatility has also risen, aligning with broader currency debasement trades, diversified outflows from emerging market currencies, and the trend of countries seeking treasury alternatives in their reserve portfolios.

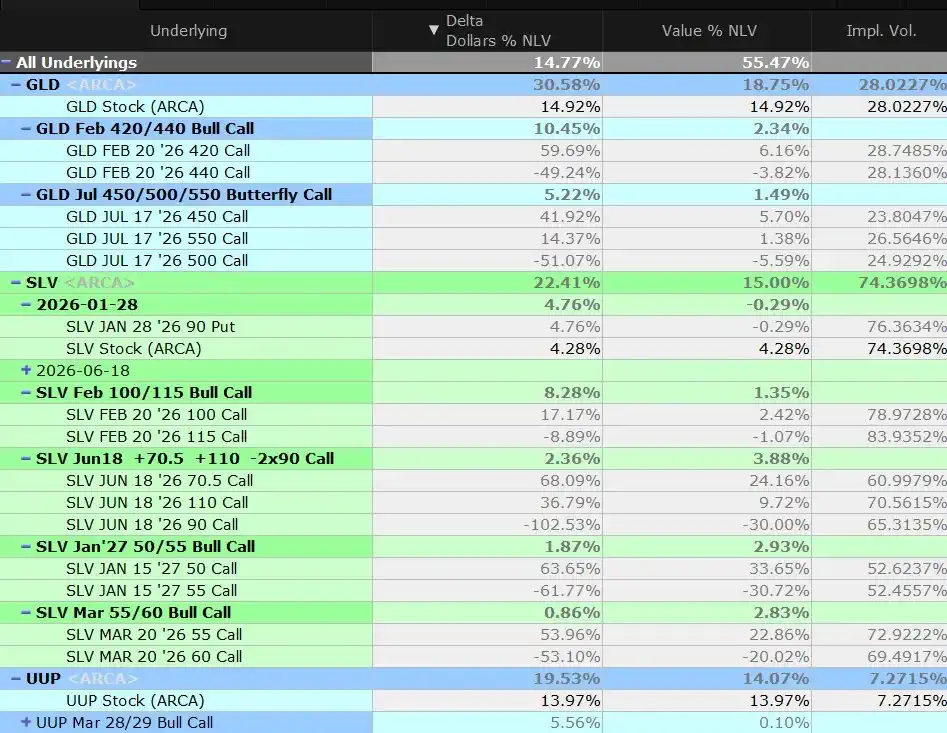

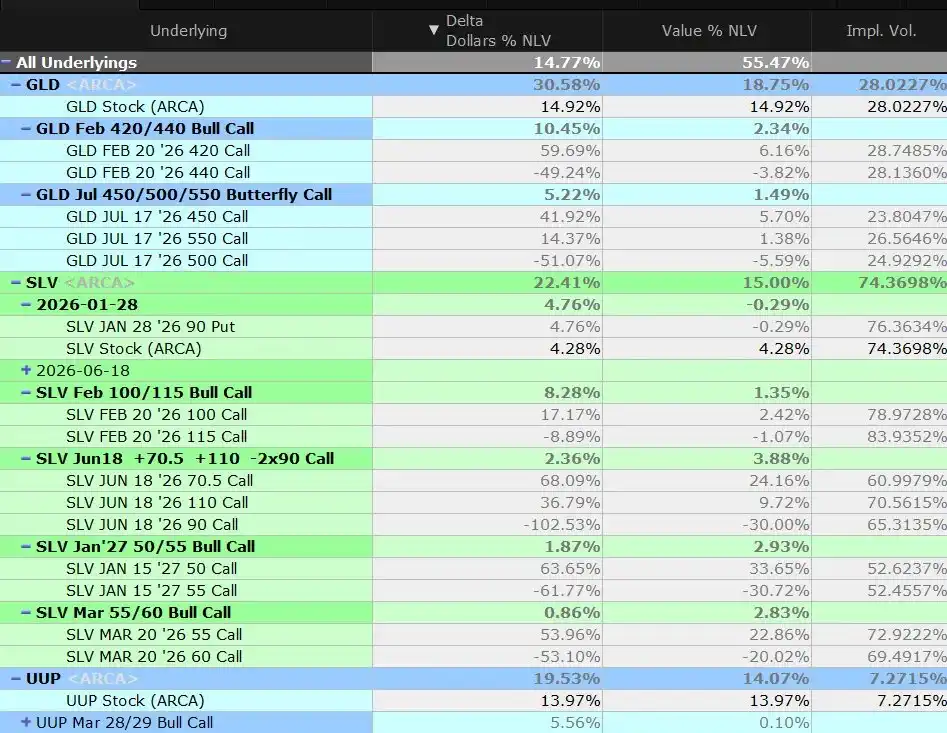

In short: we have repositioned gold, and last week, when the spot price broke through the mid-strike price, we closed slightly over half of our butterfly arbitrage position and currently maintain a long position.

At the same time, we maintain a short position on US equities, US bonds/credit, and a small amount of US dollar long position to hedge part of the US dollar short risk in the metal holdings.

What's Driving This

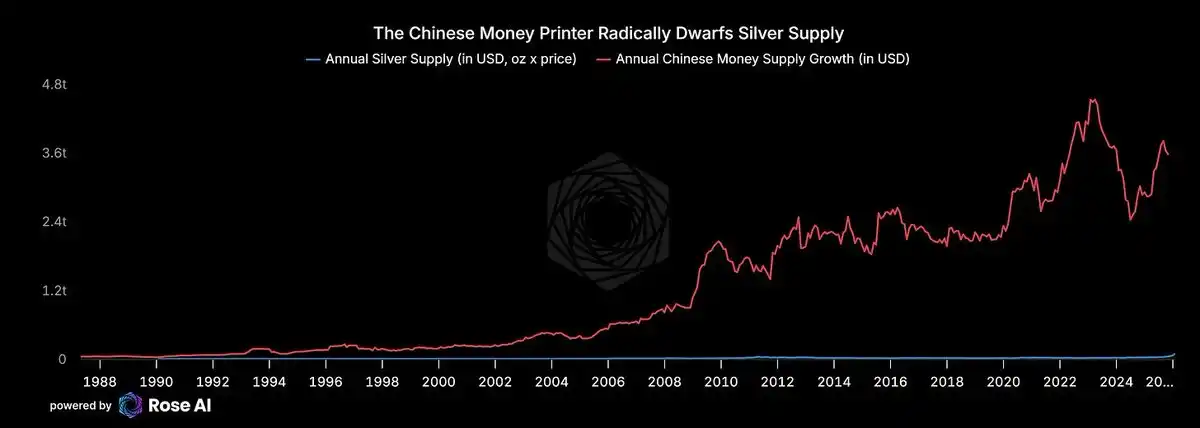

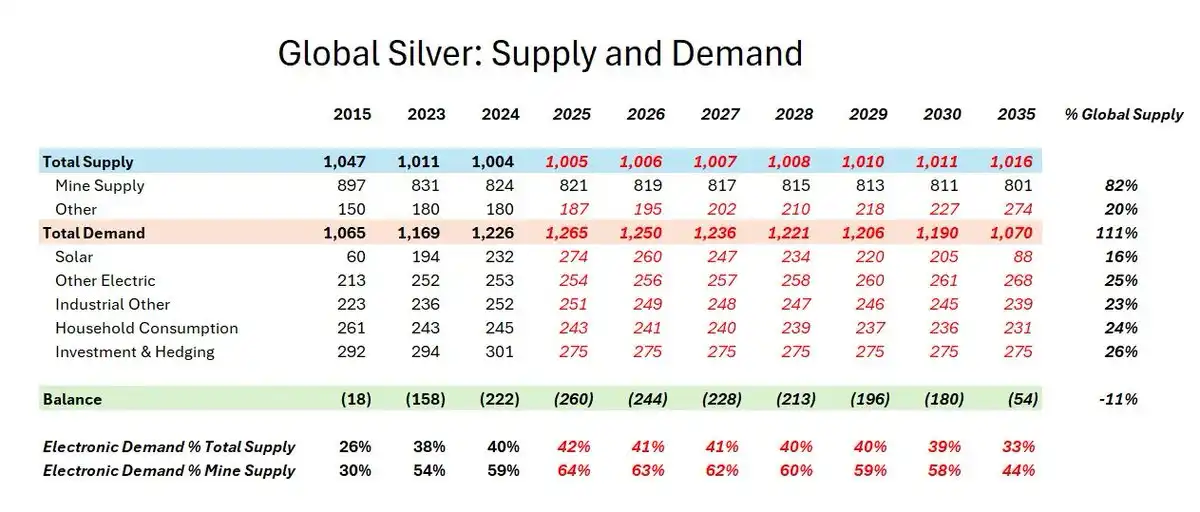

In a market where solar/AI demand has led to a structural supply shortage, Chinese capital flight remains a core short-term driver.

Looking back at why we entered this trade – seeking assets that could appreciate due to Chinese capital flight. Including recycling, the global annual silver supply is only about 1 billion ounces. At $100/ounce, this is a market of around a hundred billion dollars. Meanwhile, China's "money printer" adds about $3 trillion in bank deposits annually. With the widely known fact that real estate is no longer a secure wealth storage vehicle, a slight shift in savings behavior is enough to disrupt the silver market.

This is what you are witnessing right now.

If you were a wealthy Chinese household, would you prefer to keep more money in a zombie banking system with trillions in hidden losses? Or would you rather buy physical silver at a high price and endure a 30% drawdown risk? When your other option is to deposit into a technically insolvent bank, the answer is clear.

Chinese real estate bonds are being sold off again. Stocks in our "worst Chinese banks" basket are also tumbling.

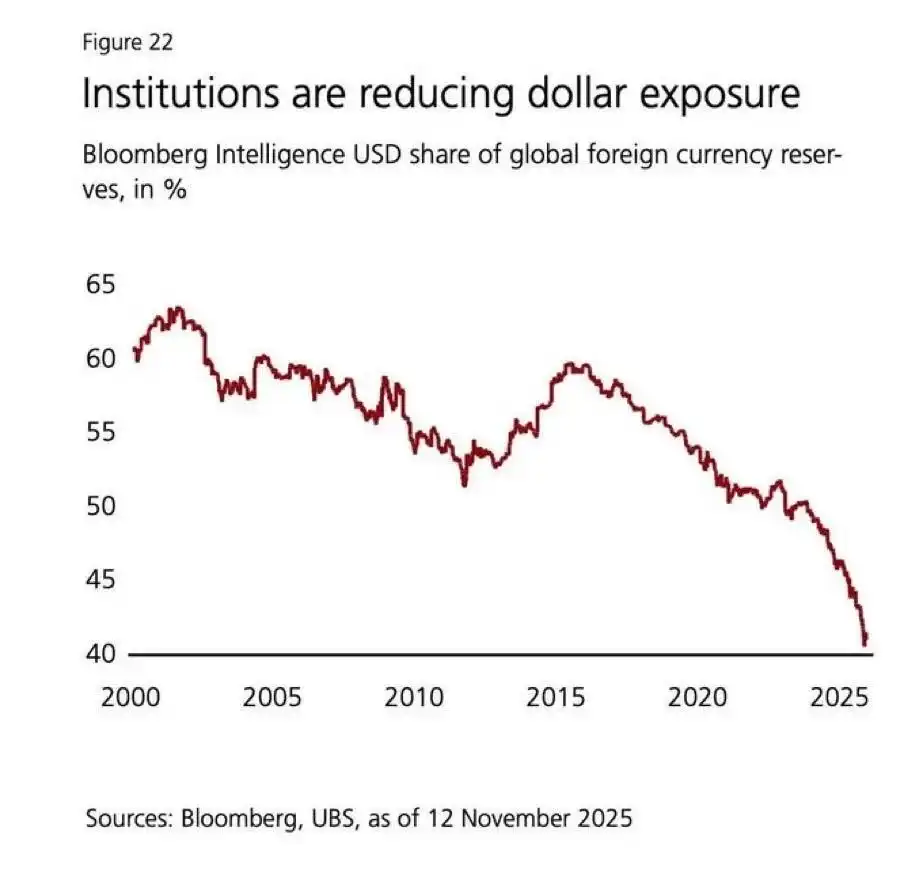

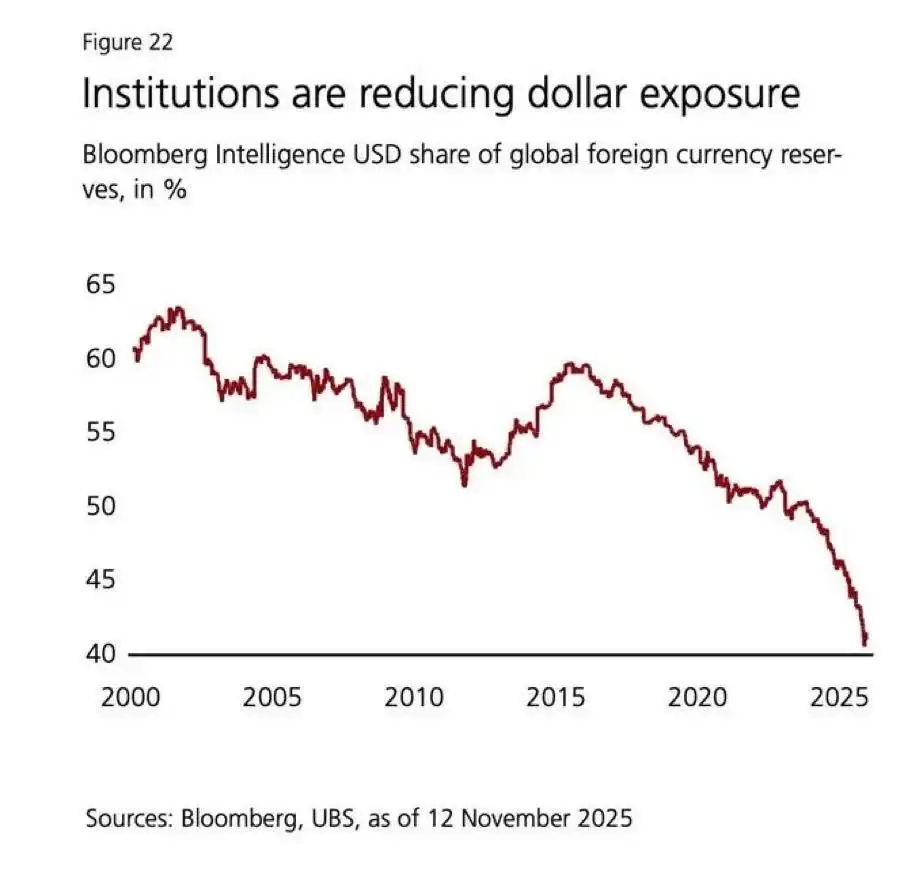

Funds from India and the Middle East are also flowing in. If you were an Indian tycoon, would you want to hold a currency wealth that has devalued over 20% against the US dollar since 2020?

European institutions are finally waking up. If you are a European pension fund with 40% of your assets allocated to US bonds and stocks (many illiquid and overvalued – such as private equity, venture capital, private credit), you have been underweight metals for years. Now, you have both political diversification reasons, and your investors are questioning why you missed this rally.

Official purchases seem inevitable. Asian demand seems insatiable. Rebalancing trades that suppressed retail demand at the end of last year are now a thing of the past. ETF inflows are strong but still below historical highs.

Right now, the question seems to have shifted from whether governments will establish a strategic silver reserve to when they will start.

Why We Remain Long

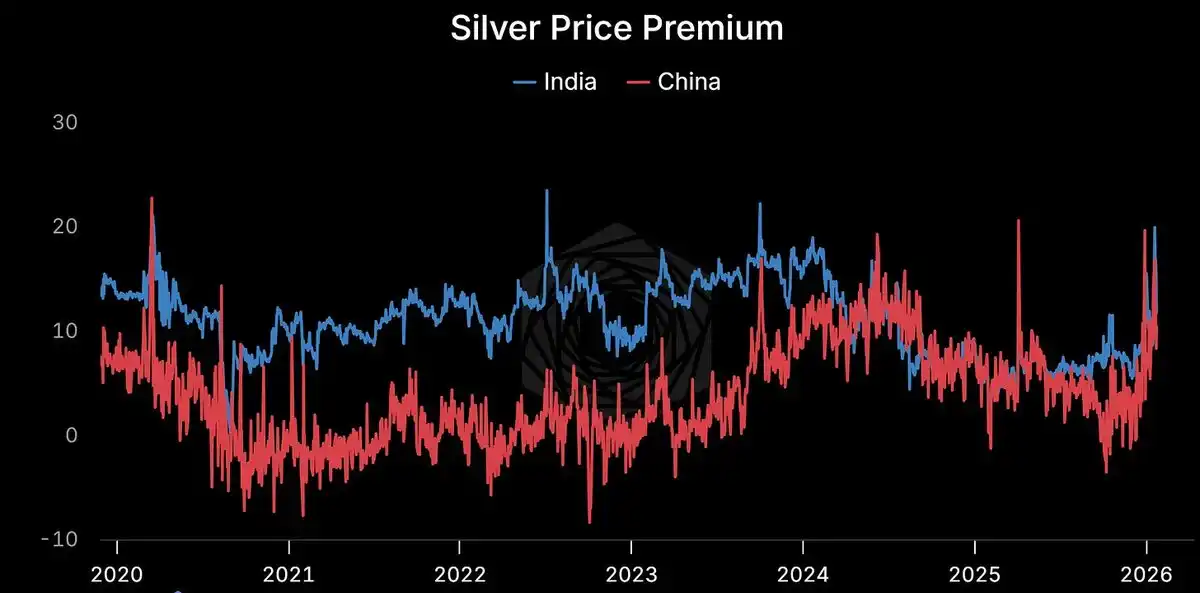

Premium continues to persist.

Shanghai: $114/oz. COMEX: $103/oz. Premium over 10%. Continues to persist. Structural.

When the physical price and paper price diverge so significantly, one side must be wrong. History tells us, it's usually not the physical.

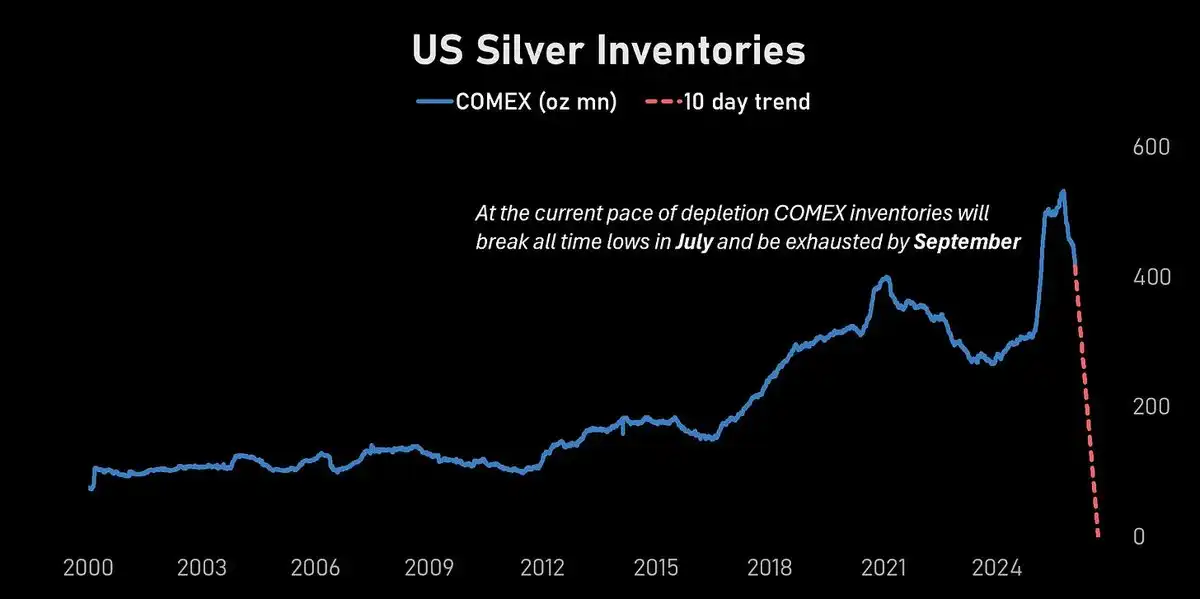

COMEX inventories are plummeting.

At the current rate of consumption, COMEX inventories will hit historic lows in July and be functionally exhausted by September.

In a market with a 70% annualized volatility, it's hard to see that far out. But the direction is clear.

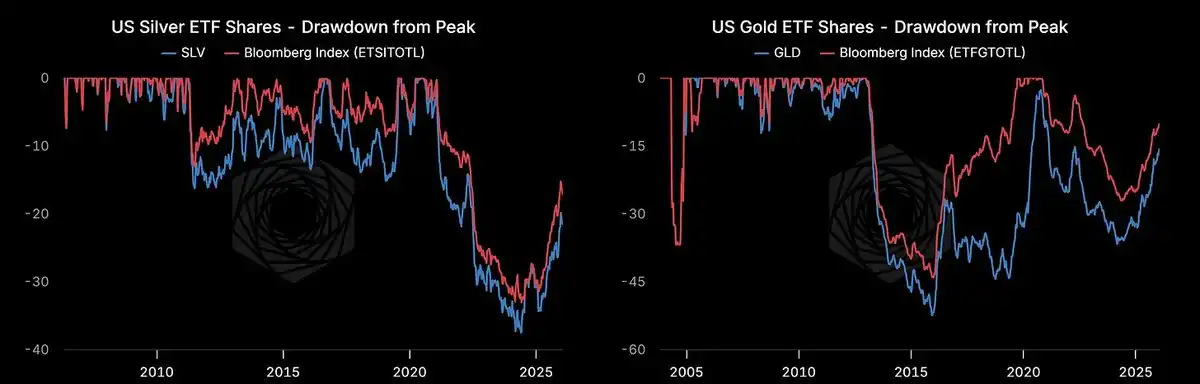

ETF fund flows still have room.

U.S. Silver ETF holdings are rising but still about 20% below the peak in 2021. We are not yet at a fever pitch.

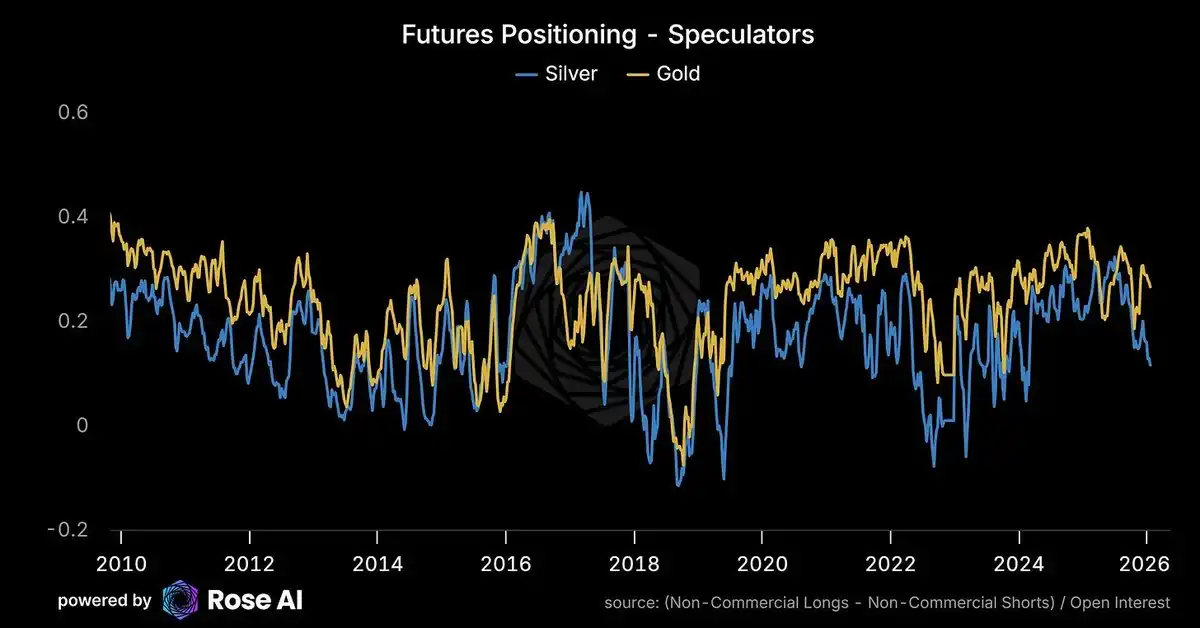

Speculative positioning is not crowded.

Western speculators have actually reduced longs and attracted shorts as the price broke historical highs. Positions are not extreme.

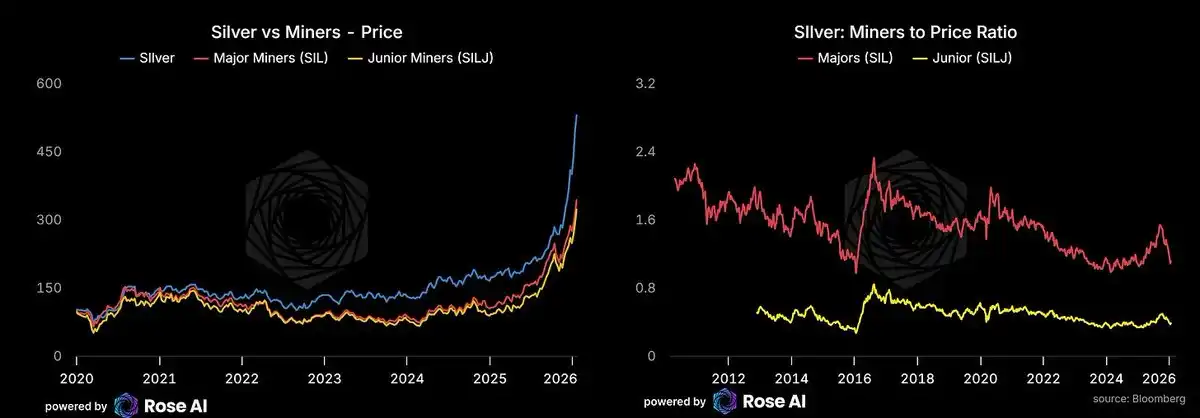

Mining stocks are lagging.

Mining stocks are catching up but still underperforming the underlying commodity. If energy prices remain low (watch the Strait of Hormuz), mining stocks could have a catch-up rally. We are long junior miners via stocks rather than options—the volatility of mining stock options appears expensive relative to realized volatility.

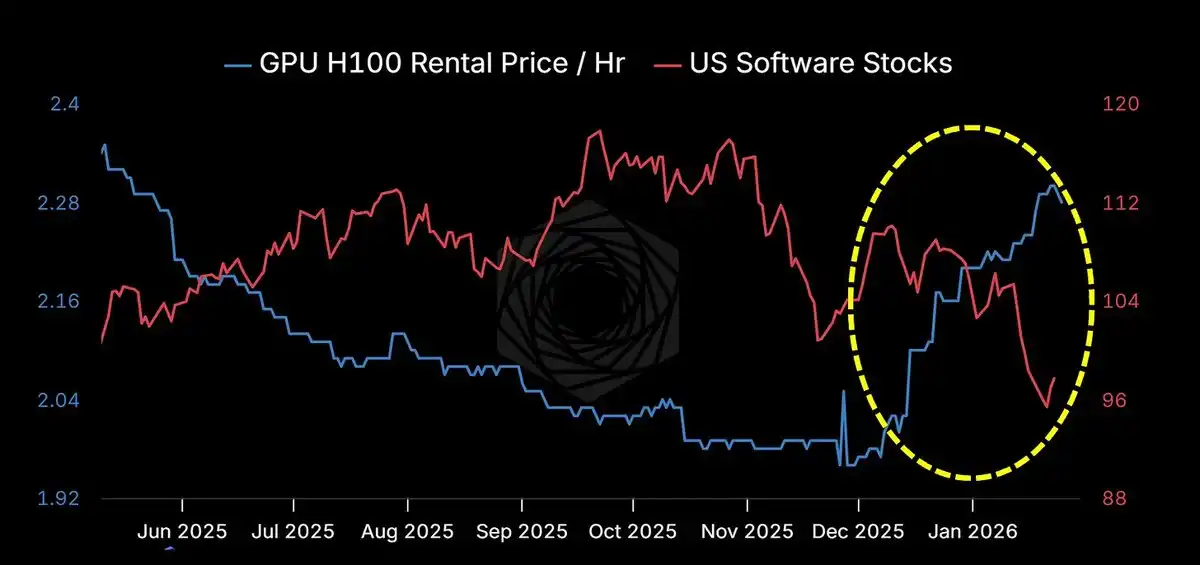

AI Acceleration Re-Accelerated

Claude Code and its mimics/branches (Codex, Ralph Wiggins, Clawdbot) are showing the true face of the "agent." The emphasis is not on complex workflows but on crossing the trust threshold: giving the machine complete access to your computer, files, and apps. Hackers and enthusiasts are rushing to buy Mac Minis. I've built an agent framework (hoping to release this month). RAM chips are sold out. Rental prices are skyrocketing, while traditional SaaS businesses are languishing. Perhaps software ate the world, then GPUs ate the software.

The manifestation of cash flow is still pending, but the era of machines has arrived. More machines mean more data centers. More data centers mean more electricity demand. More electricity demand means more solar energy.

More solar energy means more silver.

Potential Risk

A strong US dollar is a recent risk.

The recent rise has been exacerbated by a weak dollar. If the US economy continues its robust growth, the significant rate cut expectations implied in the two-year rate curve may be removed, boosting the dollar. The recent weakness in the dollar over the past few days has undoubtedly exacerbated this recent uptrend.

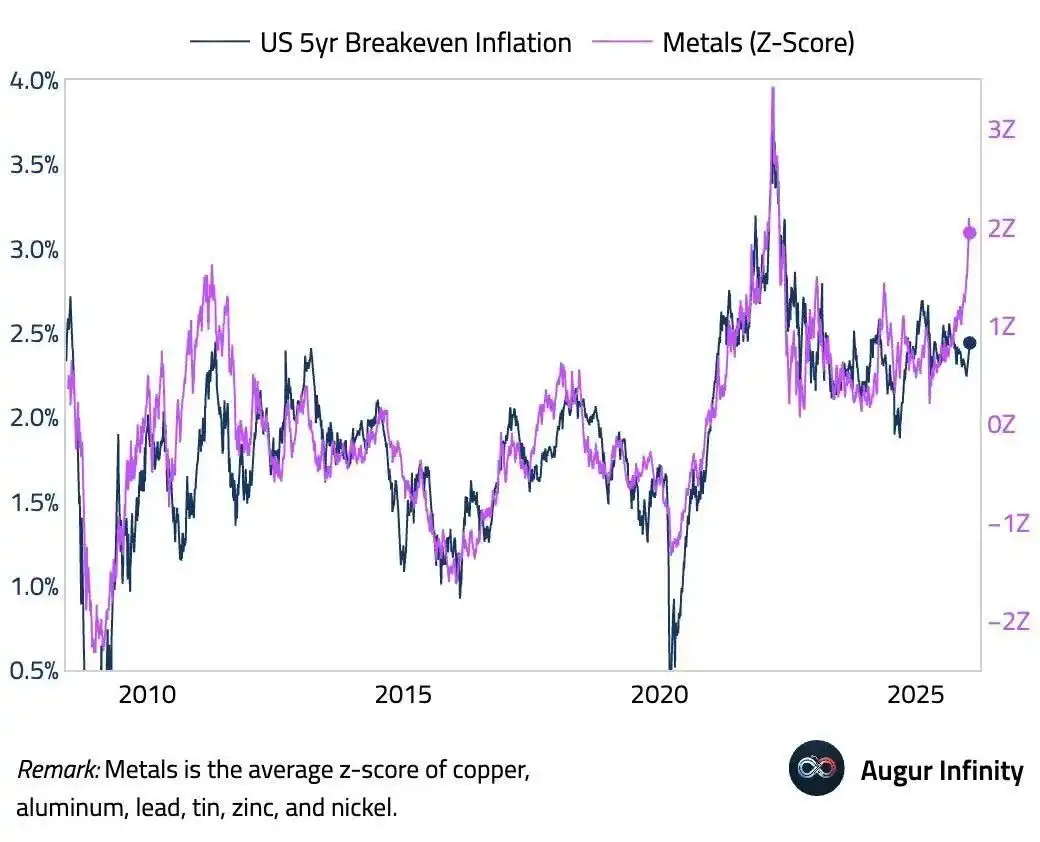

Strong US dollar + high prices = panic selling by weak holders. Speculators who bought above $100, unlike Chinese households who started accumulating from $30, will cut their losses in a sharp reversal. If the chart below is correct, we are seeing an extreme dislocation between metal prices and the breakeven inflation rate. This could realign through rate hikes/dollar strength and metal price declines.

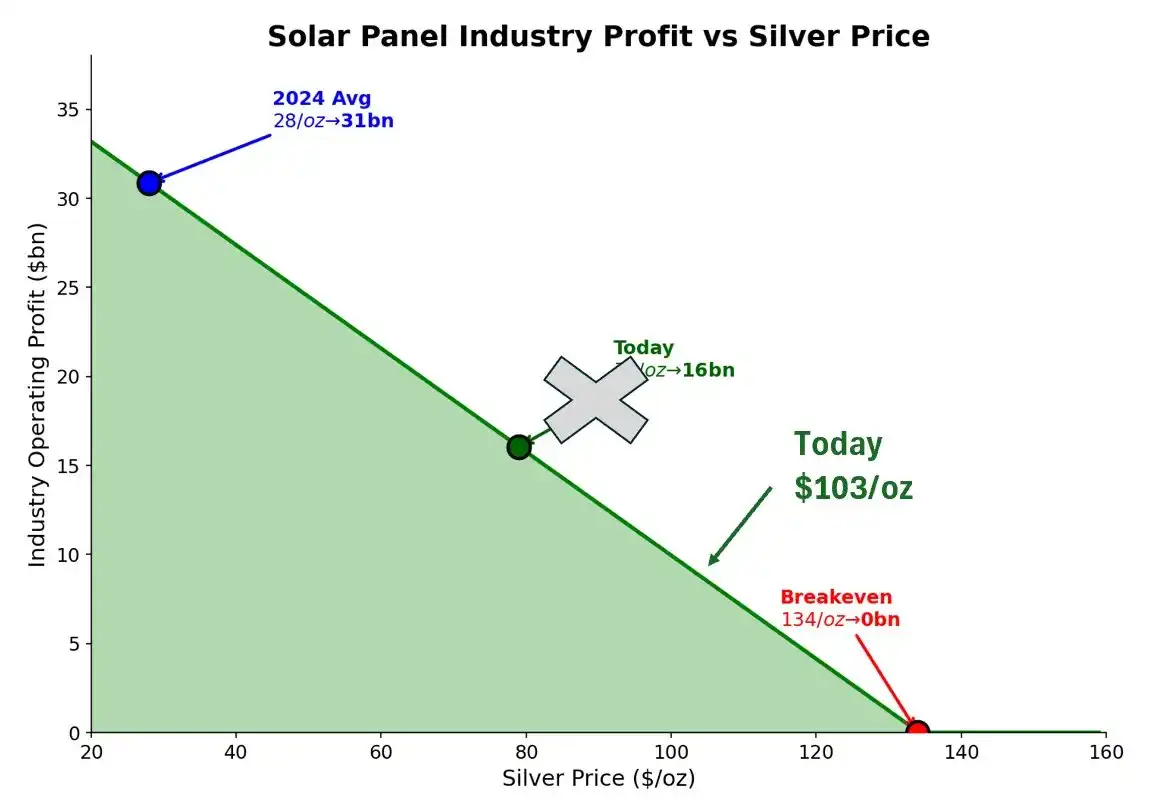

Silver prices are beginning to erode solar industry profits.

At $103/oz, this is no longer a negligible error for panel manufacturers. We are nearing a pain threshold.

At $28/oz (2024 average price), industry profits were $31 billion. At today's $103, profits could shrink to $80-100 billion. The breakeven point is at $134/oz—just 30% above the current price. In a market with 70% annualized volatility, this is not a comfortable cushion.

Copper substitution is accelerating.

Currently, the price is $22 below $125 (the point at which the investment payback for copper substitution falls below one year). Boards will discuss the conversion issue at every meeting by then.

The economics are crying out for an "immediate conversion." But physics tells us that to reach half conversion, it will take at least a few more years. This is the time window.

Where is the marginal supply coming from?

Not a Miner - The Supply Is Rigid and Takes Years to Scale. Not a Short Seller - This Is a Physical Market, You Can't Dilute Metal Like High-Priced Stock Issuances. That Leaves Only Jewelry Recycling and Melting. If Anyone Knows of Good Silver Recycling Companies, Please Contact Me.

Key Focus Areas

Signals:

Persistent Premium in Shanghai = Structural Demand, Not Noise

COMEX Inventory Depletion Rate = If Accelerating, Near-Month Contracts Face Short Squeeze Risk

USD Direction = Strength in the US Economy Boosting the Dollar Index, Shaking Out Weak Hands

Miner Stocks Playing Catch-Up = When Miner Stocks Start Outperforming Spot, Retail Is Coming In

Official Statement = The First Central Bank Announcing Silver Reserves Will Trigger a Buying Frenzy

Framework:

Focus on Fund Flows, Not Price.

If Eastern Physical Demand Keeps Buying While Western Speculators Exit Due to Dollar Strength, That's Accumulation. Buy the Dip.

If Eastern Premiums Collapse While COMEX Inventory Stabilizes, the Short Squeeze Scenario Is Unwinding. Take Profits.

Trading Strategies

Prices Are High. Upward Volatility Still Has Demand.

Upon Spot Price Breaking the Mid-Strike, We Closed Half of the Iron Butterfly Arbitrage. This Structure Was Designed for This Scenario, and We Have Profited.

Remaining Positions:

Long Gold via Stock and Call Spreads

Long Silver via Stock, Call Spreads, and Contango Iron Butterfly Arbitrage

Long Junior Miners via Stocks (No Options - Too Expensive)

Long USD via UUP to Hedge Metal Exposure

Short SPY, HYG, TLT via Put Options and Stocks

Long COMEX Near-Month (March) Contracts, Short June Contracts - Betting on Inventory Decrease. Rollover may be needed.

Net Exposure: Maintain Longs But Through Options. As Spot Price Rises, Raise Strike Prices. Await Official and Institutional Buyers to Catch Up with Prices.

Core Conclusions

As Prices Go Parabolic, We Are Gradually Reducing Delta Risk Exposure. But Not Until We See Any One of the Following Combinations:

a) China Actively Addressing Real Estate Debt Crisis

b) US Transitioning to Fiscal Responsibility

c) World Becoming More Peaceful (Ukraine, Taiwan, Iran)

d) Non-US Western Elite Reaching Some Agreement with the US

... We will maintain a long position. Although some downside protection will be implemented.

The driving forces that brought us here—capital flight, currency debasement, solar demand, supply constraints—have not changed. They are still accelerating.

Silver at $103 is not the end. It might not even be the midpoint.

We are starting to see these same dynamics spreading to other metals. Especially copper, which is getting a lot of attention from those who missed the silver move and are making rough estimates. While the situation is not as dramatic as silver—copper does not have the same monetary/squeeze characteristics—the story of AI electric demand is real, and the supply constraint is similar. We are also long on copper. More on this later.

Silver moon above, everyone.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia