$HYPE Skyrockets: An In-Depth Look at the Current Perp DEX Market Landscape, Who Is the Biggest Winner?

Original Title: perps market landscape: winners and losers

Original Author: @tradinghoex

Original Translation: SpecialistXBT, BlockBeats

Editor's Note: The article deconstructs the core advantages and business models of four representative Perp DEXs, providing a clear evaluation framework: focusing on liquidity depth, fee structure, capital efficiency, and unique mechanisms.

Trading perpetual contracts is not a team sport that requires taking sides. However, just browse the crypto community for five minutes, and you'll get the opposite impression. An extremist mindset has consumed most traders, eroding the advantage they could have gained simply by remaining curious.

If you post about trying a new Perp DEX, the replies are often filled with extremism rather than curiosity. Ironically, the attacked party usually just seeks a better option to improve their trading, but in extremist thinking, exploration is seen as betrayal.

The Real Winners and Losers

In the perpetual contract market landscape, there are no winners and losers as extremists imagine. Multiple platforms can coexist and be profitable because they serve different needs: sometimes targeting different traders, sometimes catering to the same trader's needs at different times.

However, there are winners and losers among traders, distinguished by whether they pursue optimizing their trading outcomes, not based on which platform they use.

Market Landscape: Specialization, Not Dog-Eat-Dog

Understanding the perpetual contract market landscape requires abandoning the winner-takes-all mindset. These platforms are evolving through specialization, not cutthroat competition.

Hyperliquid

Hyperliquid is a decentralized exchange running on its proprietary Layer-1 blockchain HyperEVM, designed for high performance and scalability. By adopting a fully on-chain order book model, it overcomes the limitations of automated market makers and off-chain matching engines.

Source: HyperFoundation

HyperBFT Consensus Mechanism: HyperLiquid utilizes a custom consensus algorithm called HyperBFT, inspired by HotStuff and its successors. Both the algorithm and network stack are optimized from scratch to support L1's unique requirements, enabling the network to process up to 200,000 orders per second with a latency of approximately 0.2 seconds.

Dual Chain Architecture: HyperLiquid is divided into two main components: HyperCore and HyperEVM.

HyperCore: The native execution layer that manages key functionalities of the trading platform. It operates as a highly efficient engine capable of supporting a deep order book and necessary liquidity.

HyperEVM: An EVM-compatible layer that allows any developer to deploy smart contracts, enabling the building of decentralized applications while natively benefiting from HyperLiquid's liquidity and performance.

The key to this architecture is the state unification between HyperCore and HyperEVM: no cross-chain bridge, no risk of inconsistency, no delays. Applications built on HyperEVM can seamlessly read and write to HyperCore's deep liquidity in real time.

HyperEVM Ecosystem

The HyperEVM ecosystem has already attracted a large number of foundational protocols covering areas such as lending, derivatives, yield, and infrastructure.

In this landscape, core protocols like HypurrFi, Felix, Harmonix, Kinetiq, HyperBeat, HyperLend, and Project X anchor cross-chain capital flows.

To understand HyperEVM, one must start with the capital on-ramps.

Protocols like HypurrFi and Felix provide debt infrastructure through lending markets, synthetic dollar tools (USDXL, feUSD), and cash-flow-supporting products.

Kinetiq converts locked HYPE into liquid staking tokens (kHYPE) while maintaining staking rewards, enabling composability in DeFi. The platform also supports permissionless deployment of HIP-3 exchanges through validator crowdfunding.

Harmonix transforms idle capital into productive liquidity through automated delta-neutral strategies and validator staking management, providing stablecoins with an 8-15% annualized yield.

Project X operates as an AMM DEX with cross-chain aggregation capabilities, offering zero-fee transactions across EVM chains (finality in 50 milliseconds) and a simplified liquidity provision user experience.

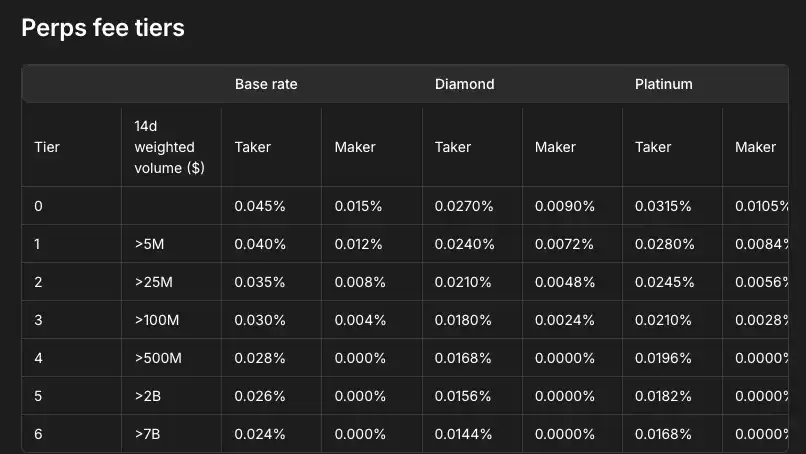

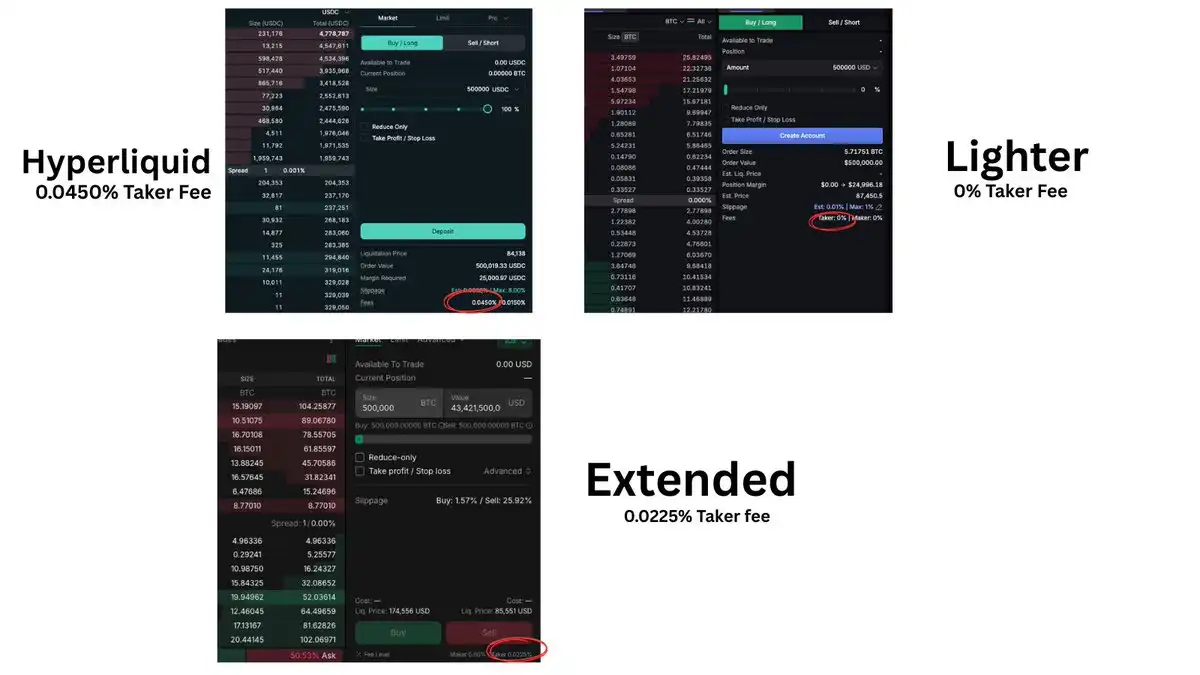

Fee: The fee rate for Perpetual Contracts is a variable transaction fee based on your 14-day trading volume on the Perpetual Contract. Your maker and taker fees will decrease accordingly based on your tier and total trading volume.

Perpetual Contracts and Spot have separate fee schedules. The trading volumes of Perpetual Contracts and Spot will be aggregated to determine your fee tier, with Spot trading volume counted twice. That is, (14-day weighted volume) = (14-day Perpetual Contract volume) + 2 * (14-day Spot volume).

For each user, all assets (including Perpetual Contracts, HIP-3 Perpetual Contracts, and Spot) share a common fee tier.

HyperLiquid Treasury: The Hyperliquid Treasury is a feature that allows users to collaborate and profit by following a trading strategy. There are primarily two types: Protocol Treasury and User Treasury.

Treasuries like Hyperliquidity Provider (HLP) are operated by the platform itself. HLPs perform functions like market-making and liquidation, earning a portion of the trading fees. Anyone can deposit USDC into an HLP and share in its P&L.

The other type is User Treasury, managed by Treasury Leaders. Anyone can become a Treasury Leader by depositing at least 100 USDC and taking 5% of the Treasury's total value as their equity. Treasury Leaders trade the funds in the Treasury and receive a 10% profit share as a reward.

For example, if you deposit 100 USDC into a Treasury that already has 900 USDC, you own a 10% share. If it grows to 2,000 USDC, you can withdraw 190 USDC (your share of 200 USDC minus the leader's 10 USDC cut).

There is no DMM scheme, special rebate/fee, or front-running advantage. Everyone is welcome to participate in market-making.

Team: Hyperliquid was created by Hyperliquid Labs. The platform is led by two Harvard alumni, Jeff Yan and lliensinc, who founded Hyperliquid.

Other team members come from Caltech and MIT and have previously worked at Airtable, Citadel, Hudson River Trading, and Nuro.

Jeff Yan brought his expertise in high-frequency trading systems from Hudson River Trading and later founded the cryptocurrency market maker Chameleon Trading. lliensinc then added a deep understanding of blockchain technology.

Finally, Hyperliquid Labs is self-funded, having not accepted any external capital, allowing the team to focus on building the product they believe in, free from external pressures.

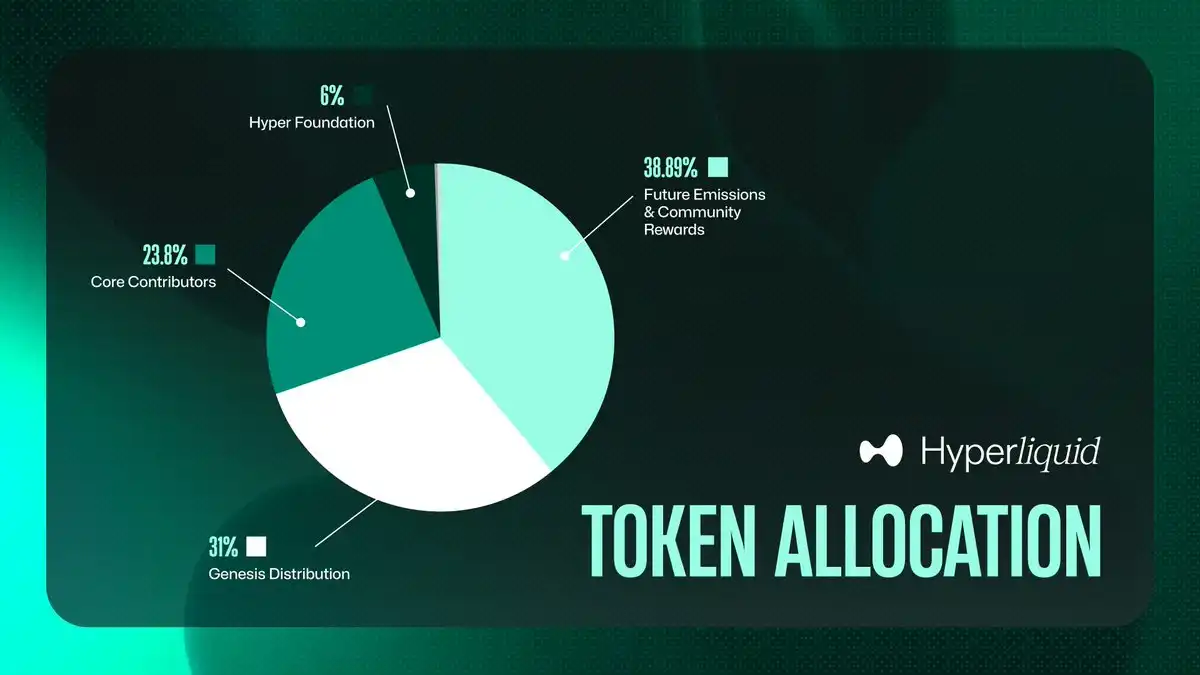

Tokenomics: Hyperliquid's native token HYPE powers its ecosystem with a total supply of 1 billion tokens. The exchange distributed HYPE through an airdrop to 94,000 users, releasing 310 million tokens (31% of the total supply).

The utility of HYPE includes governance (allowing holders to vote on platform upgrades) and staking rewards (approximately 2.37% APY).

Tokenomics breakdown:

38.888% (388.88 million tokens) reserved for future releases and community rewards

31% allocated to Genesis Distribution

23.8% designated for Core Contributors (vesting until 2027-2028)

6% for Hyper Foundation Budget

0.3% for Community Grants

0.012% for HIP-2 Allocation

HIPs: HyperLiquid Improvement Proposals

The governance of the Hyperliquid ecosystem is driven by its native token (HYPE).

Token holders participate in platform decisions through on-chain proposals called Hyperliquid Improvement Proposals (HIPs). Any eligible participant can submit a HIP, which is then voted on by HYPE holders—usually proportional to their staking amount. If a proposal garners enough support, the core team will implement it.

HIP-3: Builder-Deployed Perpetual Contracts

The HyperLiquid protocol supports permissionless builder-deployed perpetual contracts, a key milestone in achieving fully decentralized perpetual contract listings.

Indeed, HIP-3 allows anyone staking 1 million HYPE tokens to create a new perpetual contract market on the Hyperliquid blockchain (not the Hyperliquid DEX).

If a perpetual contract market behaves maliciously or dishonestly, the HIP-3 system can punish the misbehavior by seizing the deployer's staked HYPE.

Tradexyz

Tradexyz is a decentralized, non-custodial perpetual contract platform built on the Hyperliquid HIP-3 infrastructure. It enables users to trade leveraged perpetual contracts for cryptocurrencies, stocks, indices, forex, and commodities 24/7 without depositing funds into a centralized entity.

XYZ is the first platform deployed on Hyperliquid with HIP-3, and XYZ perpetual contracts trade here.

The XYZ perpetual contract is modeled after traditional (non-crypto) asset class perpetual contracts. Like all perpetual contracts, the XYZ perpetual contract is cash-settled and uses funding payments to keep the price in line with the underlying asset. The same trading mechanisms for Hyperliquid perpetual contracts (including collateral management, leverage adjustment, and margin modes or order types) also apply to XYZ perpetual contracts.

The XYZ100 Index Perpetual Contract is the first perpetual contract on XYZ. It tracks the value of a rebalanced market capitalization-weighted index consisting of 100 large non-financial companies listed on U.S. exchanges. Like other Hyperliquid perpetual contracts, it uses oracle prices to calculate funding rates, mark prices for margin, liquidation, stop-loss/take-profit triggering, and unrealized P&L calculation.

The difference between HIP-3 and HIP-1 & HIP-2:

HIP-1 and HIP-2 were early governance proposals focusing on spot trading, while HIP-3 targets perpetual contracts. HIP-1 introduced token listing standards and a governance-based new spot token listing process. Under HIP-1, the community could create new tokens on Hyperliquid and bid HYPE to list them on the spot market. HIP-2 then added a protocol-native liquidity engine that automatically provides liquidity to the order book, giving new tokens deep liquidity from day one.

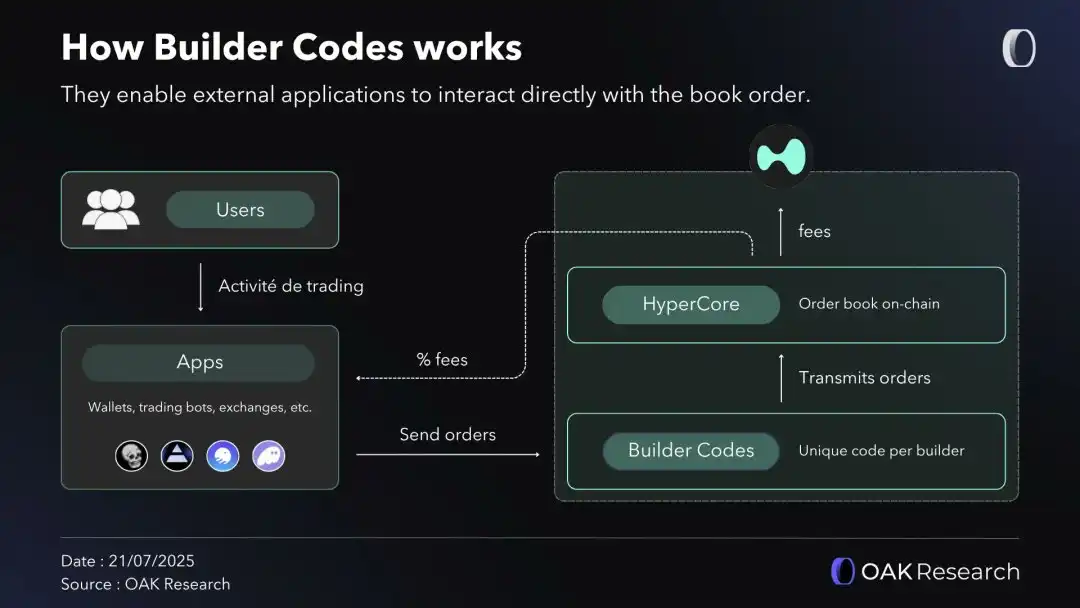

Builder ID

The Builder ID is a unique identifier that enables any developer to connect their frontend to Hyperliquid's backend. As a result, every transaction executed through this identifier will route through Hyperliquid's order book and automatically pay a certain percentage of the transaction fee to the developer. The maximum builder fee collected is 0.1% for perpetual contracts and 1% for spot.

In practice, this means that any trading bot, mobile app, or wallet can choose to use Hyperliquid as its backend infrastructure to offer cryptocurrency trading to its users while also earning a portion of the generated fees.

Adoption and Key Metrics

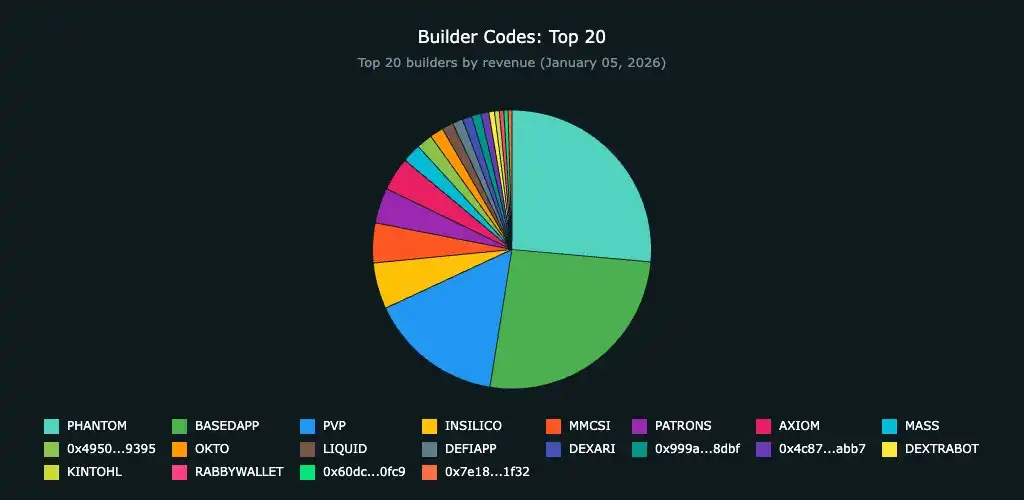

The Builder ID was launched by the Hyperliquid team in October 2024 and saw accelerated adoption in the following months.

The chart below compares the protocol revenue from implementing the Builder ID, highlighting the top 20 earners.

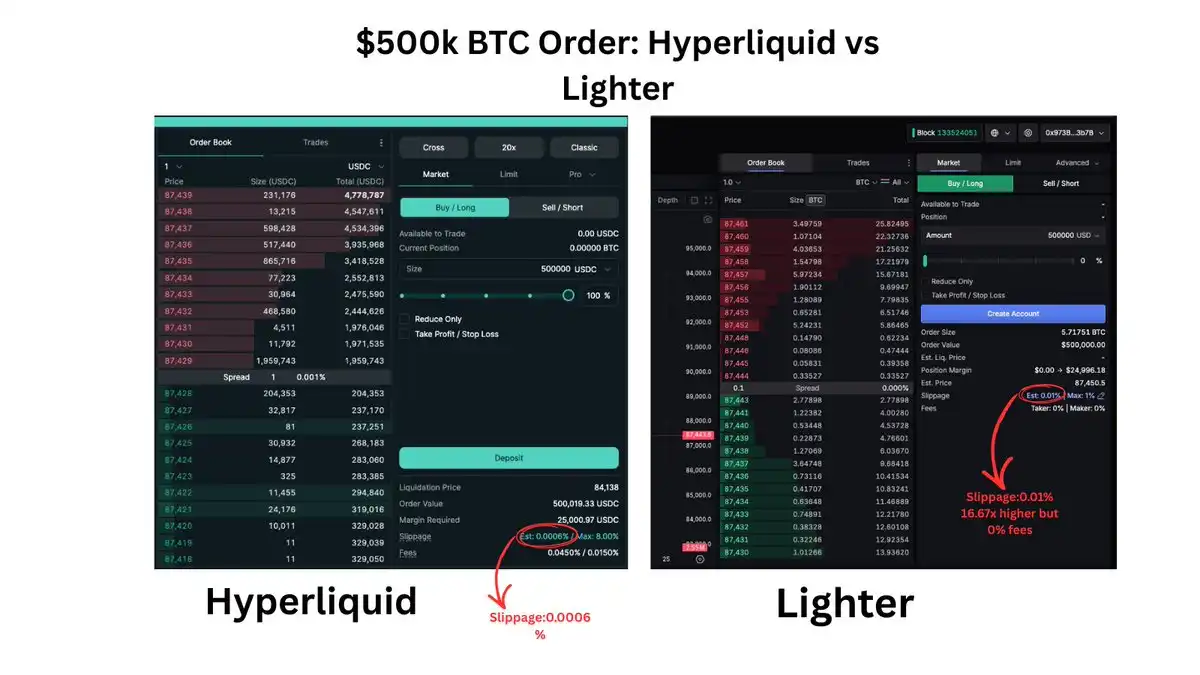

Yet HyperLiquid's true success lies not only in its product quality or even in being the largest airdrop in crypto history. Most importantly, it is rooted in a definitive advantage: establishing the most liquid platform in the market.

For the financial markets, liquidity is the ultimate truth. However, the rise of decentralized finance promised to make finance more open and accessible, but this openness has led to the emergence of numerous blockchains and applications all mercilessly competing to attract and retain the same liquidity.

The history of decentralized finance is an infinitely repeating cycle: a protocol is born, liquidity is attracted through incentives or airdrops, and then once a better opportunity arises, users migrate. In this world, liquidity remains a zero-sum game.

Hyperliquid has built infrastructure capable of retaining such liquidity.

Hyperliquid has established itself through liquidity depth, a unique technical architecture, and market diversity. The platform offers deep order books for major trading pairs and dozens of perpetual markets. This liquidity is highly valuable for traders managing diversified portfolios or large positions.

You can trade on different tokens without having to spread your funds across multiple venues.

Lighter

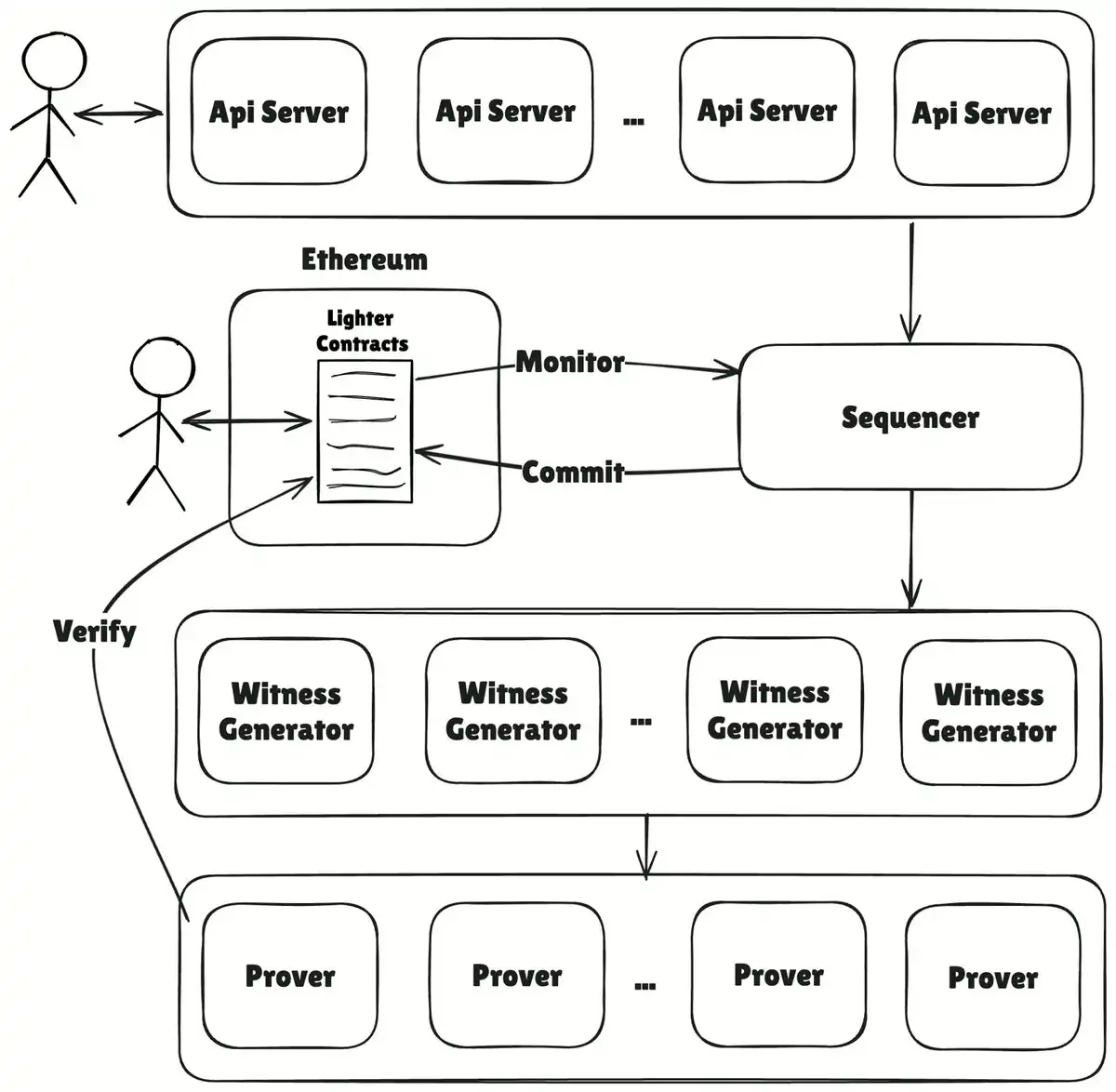

Lighter is a decentralized exchange built on a custom Ethereum-based zkRollup.

Lighter uses a custom ZK circuit to generate cryptographic proofs for all operations, including order matching and settlement, with final settlement on the Ethereum blockchain. This approach allows the platform to process tens of thousands of orders per second with millisecond-level latency, ensuring that each transaction is provably fair and verifiable on-chain.

Hyperliquid and Lighter achieve verifiable transaction execution through different architectures.

Lighter Core is a collection of coordinated components:

User-Submitted Signature Transactions: Orders, cancels, settlements, etc., are all signed by users. This ensures no forged actions and deterministic execution (same input → same output).

These transactions enter the system via API servers (pictured at the top).

Sorter with Soft Finality: At the core of the system is the sorter, responsible for sorting transactions on a "first in, first out" (FIFO) basis. It provides users with real-time "soft finality" through the API, offering a seamless experience similar to a CEX.

Witness Generator with Prover: This is where the magic happens. Data from the sorter is fed into the witness generator, which converts it into a circuit-friendly input. Subsequently, the Lighter prover, purpose-built from scratch for transactional workloads, generates hundreds of thousands of execution proofs in parallel.

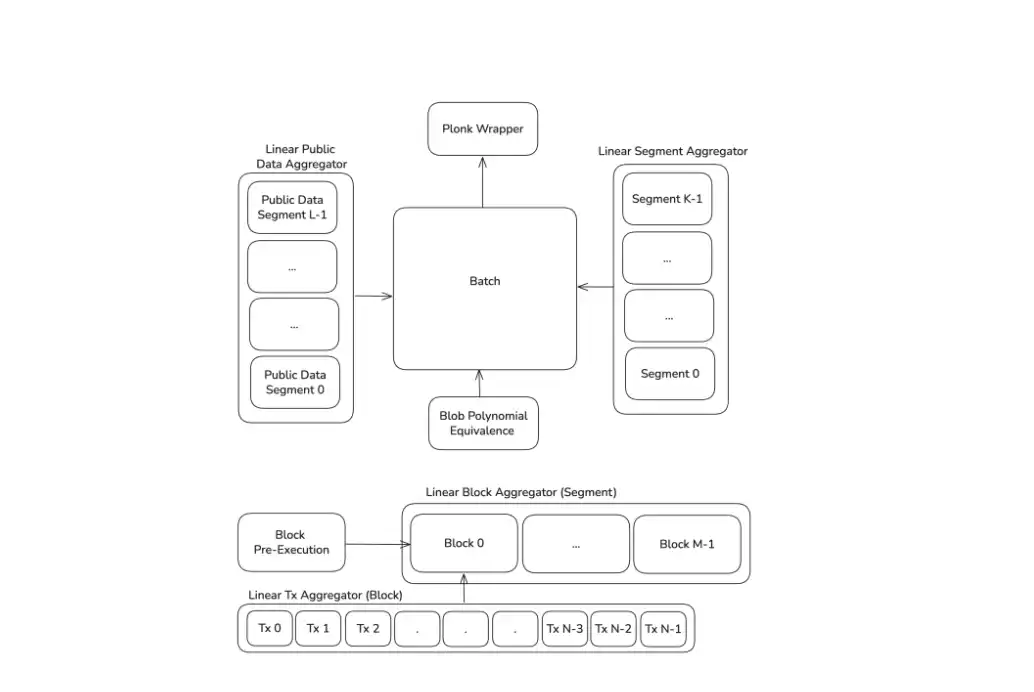

Multi-Layer Aggregation: To minimize gas costs on Ethereum, Lighter employs a multi-layer aggregation engine. This compresses thousands of individual proofs into a single batch proof for final verification on Ethereum.

Escape Hatch

This feature defines true ownership. In the worst-case scenario, such as a sorter attack or an attempt to front-run your withdrawal, the Lighter Core triggers the escape hatch mode.

The protocol allows users to directly submit a priority request on Ethereum. If the sorter fails to process this request within the scheduled time, the smart contract freezes the entire exchange. In this state, users can reconstruct their account state using previously published compressed data on Ethereum and directly withdraw the full asset value on-chain, without relying on the Lighter team or off-chain coordination.

Custom Arithmetic Circuit

A major challenge faced by current Layer 2 scalability solutions is attempting to simulate the entire Ethereum Virtual Machine (EVM) and the "technical debt" it incurs. This often requires redundant opcodes that are unnecessary for specific financial tasks.

Lighter addresses this issue by designing custom arithmetic circuits from scratch.

These circuits are purpose-built for transactional logic: order matching, balance updates, and settlement.

Technical data indicates that by eliminating EVM overhead, Lighter's prover operates significantly faster than its zkEVM counterparts and consumes far fewer resources when processing the same number of transactions. This is a prerequisite for achieving low latency required for high-frequency trading (HFT).

Multi-Layer Aggregation

Lighter is able to offer zero transaction fees to sporadic users not as a result of short-term subsidy strategies, but due to the structural advantage of multi-layer aggregation.

The verification process is akin to a data compression pipeline:

Batching: The prover parallelizes the generation of execution proofs for thousands of small transactions.

Aggregation: The system collects hundreds of thousands of sub-proofs and compresses them into a batch proof.

Final Verification: Smart contracts on Ethereum only need to verify this final singular proof.

The economic consequence is that the marginal cost of validating an additional transaction on the network approaches zero. This creates a sustainable competitive advantage in terms of operational costs.

Fee: Currently, Lighter does not charge maker or taker fees for standard accounts. Everyone can trade for free on all markets. Advanced accounts incur maker and taker fees.

Lighter Treasury: LLP

LLP is the native liquidity pool on Lighter.

The platform features a public liquidity pool where users can provide liquidity and earn rewards based on trading activities. LLP tokens represent shares in these pools, which can be used in the Ethereum DeFi ecosystem for composability with protocols like Aave to access additional yield opportunities.

While its purpose is to ensure order book depth liquidity and tight spreads, it is by no means the sole market maker on the exchange. Other traders/HFT firms can also operate market-making algorithms.

Team: Vladimir Novakovski is the founder and CEO of Lighter, with a background in quantitative trading at Citadel, machine learning at Quora, and engineering leadership at Addepar. He previously co-founded Lunchclub and holds a degree from Harvard University.

Funding: In an undisclosed funding round completed on November 11, 2025, Lighter raised a total of $68 million, reportedly valuing the company at $1.5 billion.

This funding round was led by Ribbit Capital and Founders Fund, with participation from Haun Ventures and the uncommon risk-taking online broker Robinhood.

Additionally, Lighter received broad support from leading venture capital firms and angel investors, including Andreessen Horowitz (a16z), Coatue, Lightspeed, CRV, SVA, 8VC, and Abstract Ventures, among others.

Tokenomics: According to official allocation data, Lighter has a total capped supply of 1,000,000,000 LIT tokens. The allocation structure establishes a precise 50/50 balance between internal and external stakeholders.

26% allocated to the team

25% for airdrops

25% for the ecosystem

24% allocated to investors

Lighter has carved out its position through cost obsession. For high-volume traders, the platform's zero-fee structure could mean the difference between a winning and losing strategy.

Based on a monthly trading volume of $10 million, compared to platforms charging 0.03-0.05% maker fees, savings could amount to thousands of dollars per month or tens of thousands per year. Lighter recognizes that for some traders, fee elimination is more important than access to a hundred different markets.

They have optimized for these types of traders, and these traders have taken notice.

Extended

Extended is a perpetual contract DEX built by the former Revolut team, with a unique product vision centered around Unified Margin.

The goal is to create a full trading experience by combining perpetual contracts, spot, and an integrated borrowing market under one margin system.

The Extended Network, with global Unified Margin at its core, will allow all applications within the network to access users' available margin and share unified liquidity, thereby enhancing overall liquidity depth. From the user's perspective, all activity will be counted towards a single global margin account shared across applications, allowing them to manage one account rather than multiple app-specific accounts and maximize capital efficiency by using the same margin across multiple dApps.

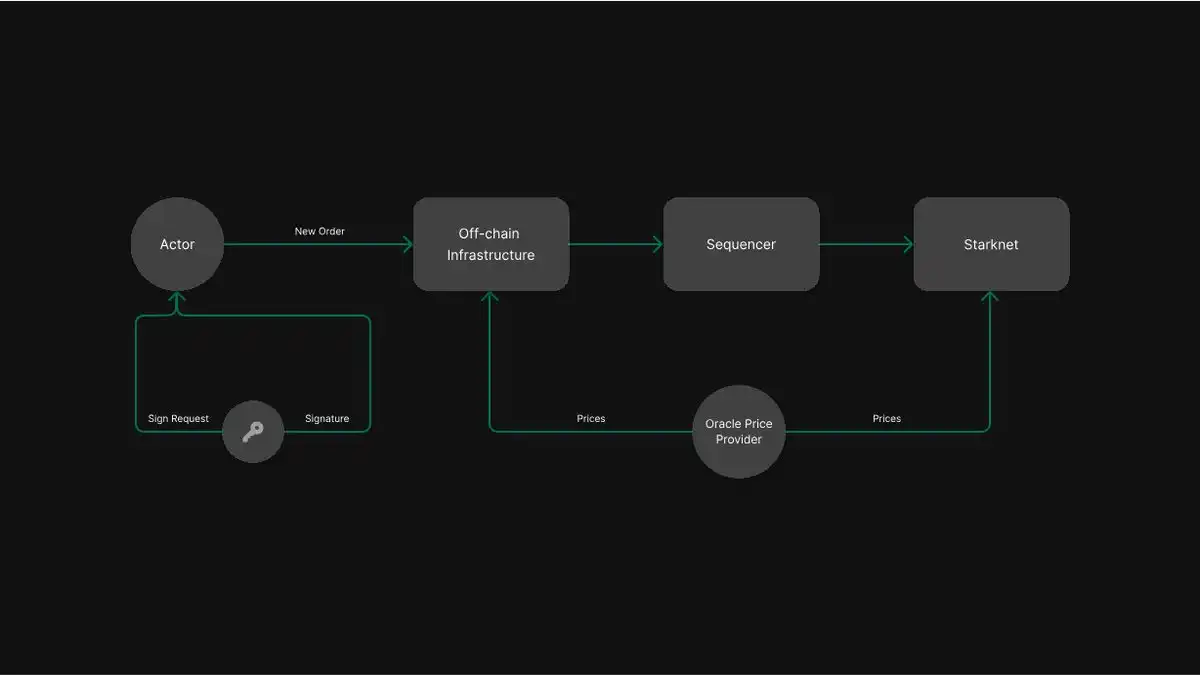

Extended operates as a hybrid Central Limit Order Book (CLOB) exchange. While order processing, matching, position risk assessment, and trade sequencing are handled off-chain, transaction validation and settlement occur on-chain via Starknet.

Extended's hybrid model leverages the advantages of centralized and decentralized components:

On-chain settlement with validation and oracle price feeds: Extended settles each transaction on the blockchain, with on-chain validation of transaction logic ensuring fraud prevention and correct transactions. Furthermore, price feeds from multiple independent oracle providers reduce the risk of price manipulation.

Off-chain trading infrastructure: Off-chain order matching and risk engine, combined with a unique settlement architecture, provide superior performance in throughput, end-to-end latency, and transaction settlement. This performance is comparable to centralized exchanges and superior to other hybrid or decentralized exchanges.

Extended is designed to operate in a fully trustless manner, benefiting from two core principles:

Users retain self-custody of their funds, with all assets held in Starknet smart contracts. This means Extended cannot custody user assets under any circumstances.

On-chain validation of transaction logic ensures that fraud or incorrect transactions (including liquidations that violate on-chain rules) are never allowed.

All transactions occurring on Extended are settled on Starknet. While Starknet does not rely on Ethereum Layer 1 to process each transaction, it inherits Ethereum's security by publishing zero-knowledge proofs every few hours. These proofs verify the state transitions on Starknet, ensuring the integrity and correctness of the entire system.

Team

Extended was created by a former Revolut team, including:

@rf_extended, CEO: Former Head of Crypto at Revolut, former McKinsey.

@dk_extended, CTO: Architect of 4 cryptocurrency exchanges (including the recently launched Revolut Crypto Exchange).

@spooky_x10, CBO: Former Chief Engineer of Revolut Crypto, one of the key contributors to Corda blockchain.

Their journey as a team began at Revolut, where they saw millions of retail users enter the crypto space during the last bull market, but also noticed a lack of high-quality products outside of top exchanges, as well as an overall unsatisfactory DeFi experience.

Fee Structure

Extended uses a simplified fee structure for its perpetual market:

Taker Fee: 0.025% of the executed notional value.

Maker Fee: 0.000% (i.e., no fee for placing limit orders).

From the user's perspective, this means that executing market orders is cost-effective, and limit orders executed as the maker may incur no direct fees.

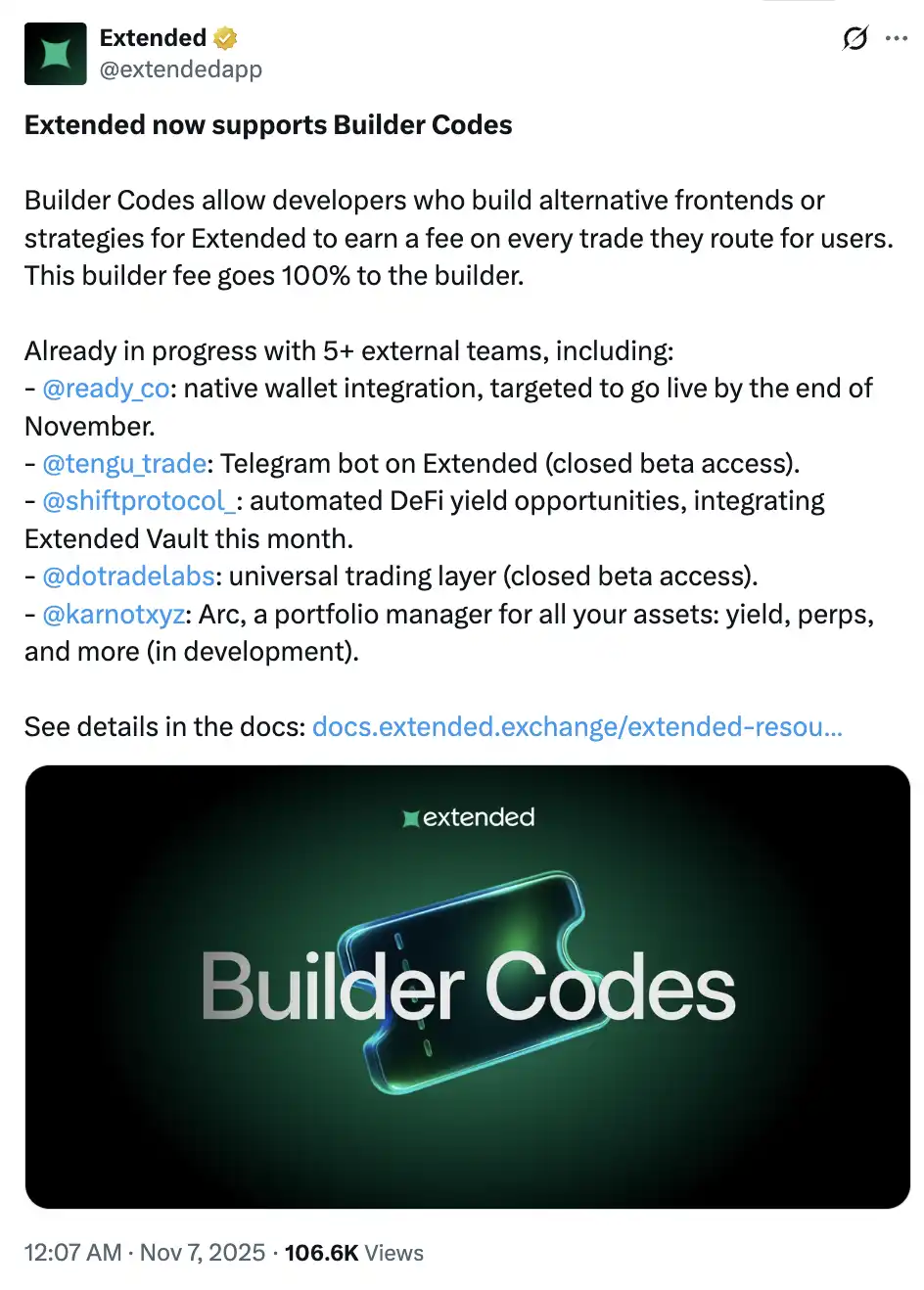

Builder Code

Extended supports builder code, allowing developers building alternative frontends for Extended to earn builder fees on every transaction routed through their frontend for users. This fee is 100% retained by the builder and defined per order.

Builder code has been pushed forward in collaboration with the following teams:

Wallet Trading Integration

In addition to expanding its product offering, Extended has integrated natively with wallets, enabling users to directly engage in perpetual trading within the wallet interface, similar to how accessing token swaps is done today. This integration opens the door to perpetual contracts for a broader retail user base.

Extended Treasury

The vault employs an automated market maker strategy, actively quoting all markets listed on Extended. Its quoting behavior is governed by global and market-specific risk exposure limits, as well as constraints around dynamic capital allocation and spread management logic:

Risk Exposure Management

Global Risk Exposure Cap: If the vault's leverage exceeds 0.2x, it will only quote in markets where it already holds risk exposure and only in the direction that reduces that risk exposure. This acts as a circuit breaker to prevent over-leveraging.

Per-Market Risk Exposure Limit: Each market has a hard cap on the allowable vault risk exposure. Assets with lower liquidity have stricter limits to minimize the risk of illiquidity.

Quoting Behavior

Adaptive Spread Quoting: The spread is dynamically set to tighten in stable conditions and widen in volatility to mitigate adverse selection. Quotes must stay within a predefined width constraint to qualify for rewards.

Risk Exposure-aware Adjustments: The vault adjusts scale and spread directionally asymmetrically to decrease quote size in directions that increase vault risk exposure and widen the spread.

Additionally, the vault earns order book rebates from its market-making activities.

Extended stands out with its vault system, allowing traders to earn yield while trading perpetual contracts. Through Extended Vault Shares (XVS), depositors can earn a base yield of around 15% APY on their collateral and additional rewards based on trading activity.

Additional yield amounts for specific users depend on their trading alliance level. The higher the trading alliance level, the higher the additional yield APY. Extended's trading alliance level is percentile-based and depends on the user's total trading score:

Trading alliance rankings update weekly in sync with score distribution based on the user's total trading score.

Passive vault depositors have no trading alliance level, and their additional yield factor is zero.

Active traders are categorized as: Pawn (bottom 40%), Knight (next 30%), Rook (15%), Queen (10%), and King (top 5%).

The platform allows XVS to be used as collateral, contributing up to 90% of the equity value, enabling traders to earn passive income from their capital while engaging in leveraged trading.

For traders holding a significant amount of funds on a perpetual contract platform, this dual-purpose collateral — serving as both trading margin and interest-generating deposit — creates a level of capital efficiency that traditional platforms cannot provide.

Variational

Variational is a peer-to-peer trading protocol with a fundamentally different operation mode. Unlike order book-based DEXs, Variational uses a Request for Quote (RFQ) model. The protocol offers zero trading fees across 500+ markets while implementing an income redistribution system through loss refunds and trading rebates.

OMNI: Perpetual Contract Trading

The first application launched on the Variational protocol is Omni, a retail-focused perpetual trading platform. Omni allows users to trade hundreds of markets with tight spreads and zero fees, all while receiving loss refunds and other rewards.

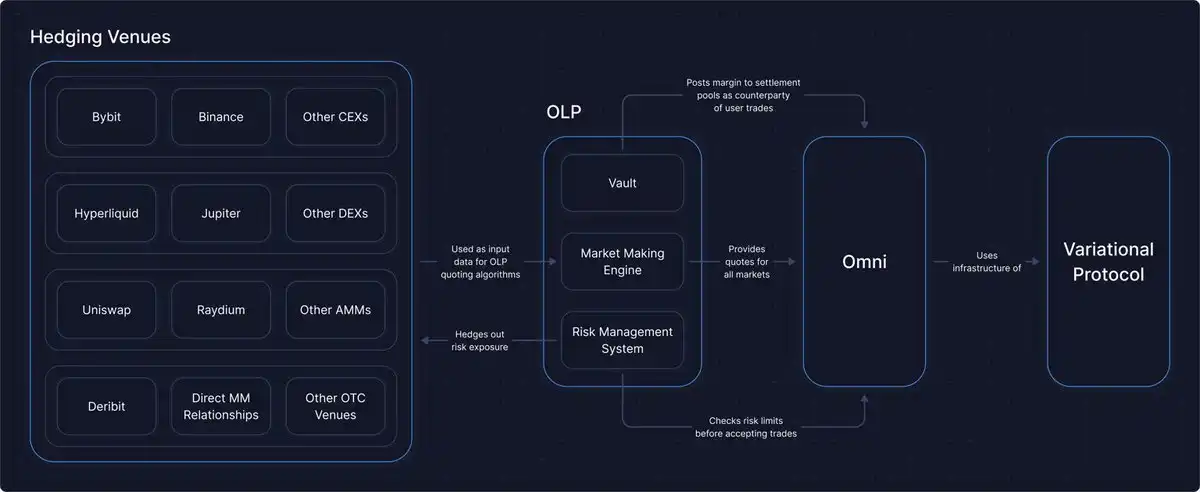

The protocol utilizes an internal market maker called the Omni Liquidity Provider (OLP), which aggregates liquidity from CEXs, DEXs, DeFi protocols, and OTC trading markets. The OLP is the first to run sophisticated market-making strategies concurrently and acts as the users' sole counterparty for trades. When users request a quote, the OLP fetches competitive prices across the entire liquidity landscape. The OLP typically captures a 4-6 basis point spread income while charging users zero fees.

Additionally, due to the RFQ model only requiring the OLP to provide liquidity at trade initiation, the OLP can offer competitive quotes for hundreds of trading pairs simultaneously.

Variational redistributes a significant portion of the revenue to users through two mechanisms:

Loss Refunds: Whenever a trader closes a losing position, they have the chance to receive an immediate refund of the full loss amount, with probabilities ranging from 0% to 5% depending on their reward tier (from zero to master). The protocol has distributed over $2 million in refunds across more than 70,000 trades, with the highest single refund exceeding $100,000. This fund comes from 10% of the OLP's spread income.

Trading Rebates: Active traders earn rebates based on their trading volume and benefit from spread discounts. The higher the volume, the more value flows back to the trader.

With over 500 markets to choose from, Variational has the broadest coverage in the perpetual contract DEX space. Through an automatic listing engine that leverages OLP liquidity aggregated from CEXs, DEXs, DeFi protocols, and off-chain sources, new assets can be listed within hours. Having a customizable internal oracle allows Variational to quickly support new assets and potentially list alternative and novel markets in the future.

On Omni, on-chain transactions handle user deposits and withdrawals, and when necessary, move funds from OLP to a new settlement pool to pay Gas fees. This eliminates the hassle of managing Gas fees for different transaction operations.

For traders looking for downside protection, access to alternative markets, and rewards based on activity, Variational's model meets their unique needs.

PRO: Institutional OTC Derivatives Trading

As Omni addresses the perpetual market, Pro is designed for institutional traders who need more than standard perpetual contracts. Pro extends the RFQ model, allowing multiple market makers to real-time compete on a single quote request, providing higher transparency and better pricing than the current "negotiating in a Telegram group" model.

Pro aims to bring transparency and automation to OTC derivatives trading. It transforms a slow, opaque, and high-risk market into an efficient, fair on-chain infrastructure.

Team

Variational was founded by Lucas Schuermann and Edward Yu. Lucas and Edward met at Columbia University as engineering students and researchers, later founding their own hedge fund (Qu Capital) in 2017. In 2019, Qu Capital was acquired by Digital Currency Group, with Lucas and Edward becoming the VP of Engineering and VP of Quantitative Trading at Genesis Trading, respectively.

In 2021, after processing billions of dollars in trading volume at Genesis (then one of the largest exchanges in the crypto space), Lucas and Edward left to start their proprietary trading firm: Variational. After raising $10 million to run their trading strategies profitably for years and integrating with nearly all CEXs and DEXs in the industry, Lucas and Edward decided to use Variational's trading profits to develop the Variational Protocol.

Lucas and Edward's goal for the Variational protocol is to: redistribute liquidity provider profits to traders through Omni and address the pain points they witnessed firsthand by bringing institutional off-chain trading on-chain through Pro.

The Variational development and quant team is composed of industry veterans who have been active in the crypto algorithmic trading space since 2017, with previous experience at companies such as Google, Meta, Goldman Sachs, and GSR. All members of the core technology team have over a decade of experience in software engineering and/or quantitative research.

Fundraising: In a funding round completed on June 4, 2025, Variational raised a total of $11.8 million.

Variational has received support from industry leaders, including Bain Capital Crypto, Peak XV (formerly Sequoia India/Southeast Asia), Coinbase Ventures, Dragonfly, Hack VC, North Island Ventures, Caladan, Mirana Ventures, Zoku Ventures, and others.

Fee

There are no transaction fees on Omni.

Omni only charges a fixed fee of $0.1 per deposit/withdrawal to prevent spam transactions and cover Gas costs.

OLP

The Omni Liquidity Provider (OLP) is a vertically integrated market maker that serves as the counterparty to all trades on Omni.

The OLP can be broken down into three key components: Treasury, Market Making Engine, and Risk Management System.

Treasury: The Treasury is a smart contract where the capital (USDC) that powers the OLP is securely held. The Treasury serves as the source of the OLP's collateral and the place where the OLP's market making profits accumulate.

Market Making Engine: The OLP runs sophisticated market-making strategies responsible for generating competitive quotes and acting as the counterparty for every trade executed on Omni. The OLP operates proprietary internal algorithms that analyze real-time data from both CEXs and on-chain sources (such as fund flows and volatility) to determine fair prices. The primary goal of the market-making engine is to maintain as tight a spread as possible across all markets.

The OLP is based on the same market-making engine that the Variational founders have been using and improving for over 7 years.

OLP as the Sole Counterparty

For every trade on Omni, both OLP and the user must adhere to margin requirements. This means both parties need to maintain margin in the settlement pool, and if their margin falls below the requirement, they may be liquidated.

A key difference in Omni's design compared to other platforms is that OLP is the counterparty for all trades on Omni. This provides several benefits to traders:

Zero Fees: Since all market-making on Omni is done by OLP instead of external market makers, Omni does not need to rely on fees to generate revenue.

Loss Refunds: A portion of the spread income is immediately returned to traders, including through Omni's loss refund mechanism.

Listing Diversity: All OLP needs for a new listing is a reliable price feed, a quoting strategy, and a hedging mechanism—all of which can be built and maintained in-house. This is reflected in the approximately 500 tradable markets on Omni, with the potential to add RWAs and other alternative markets in the future.

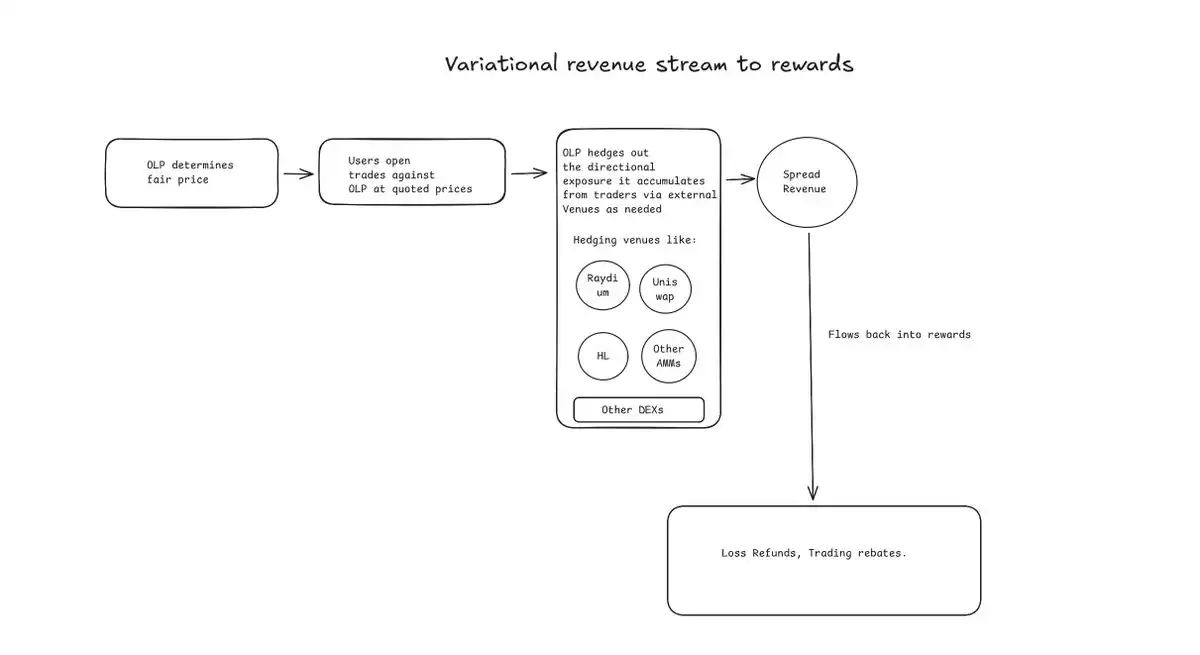

OLP makes money through the following process:

OLP consistently determines a fair spread for each asset.

Users open trades with OLP at the quoted price.

OLP hedges the directional risk accumulated from traders through external venues as needed.

The Variational Protocol makes money by taking a percentage of the spread income on Omni. For example, at a high level, the Variational Protocol may earn 10% of all spread paid on Omni.

OLP's Funding Sources

Initially, the Variational team provided the initial capital for OLP. Once the system has proven stable on the mainnet over time and has a good track record of generating market-neutral returns, the team intends to open deposits to users through a community treasury.

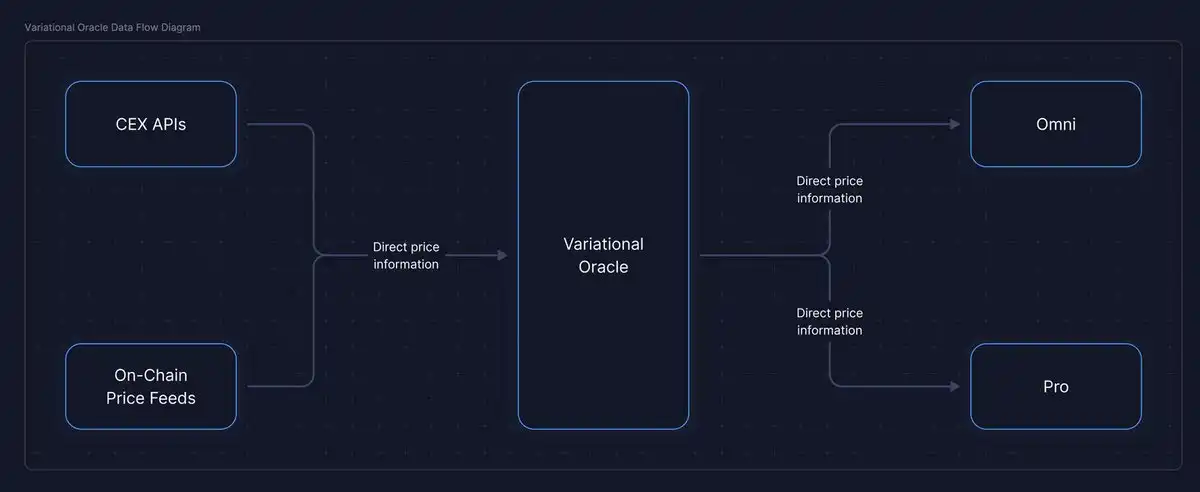

Variational Oracle

The Variational Oracle provides price and market information for all assets supported by the Variational Protocol.

This oracle works by streaming multiple diverse real-time data sources for each supported market, using a weighted combination of prices from different exchanges. Having a customizable internal oracle allows Variational to quickly support new assets and potentially list alternative and novel markets in the future.

Omni's permissionless perpetual contract listing feature is achieved through its custom oracle, which can autonomously assess price reliability, decentralization level, and market activity before activating a new market.

Through RFQ Trading

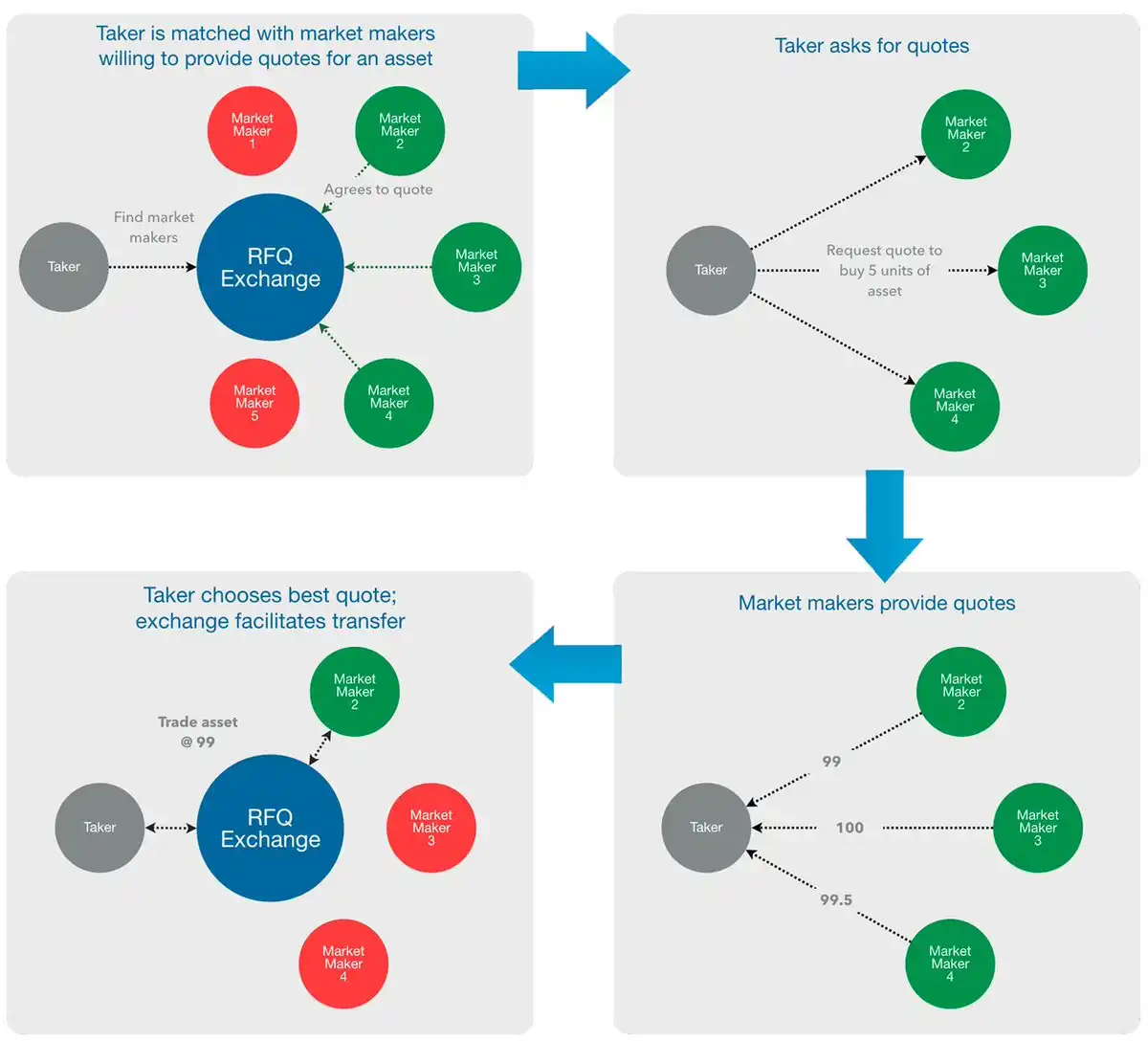

Variational is a Request for Quote (RFQ) protocol that does not use an order book.

Source: https://hummingbot.org/blog/exchange-types-explained-clob-rfq-amm/#request-for-quotation-rfq-exchanges

At a high level, an RFQ system consists of the requester seeking a quote and the liquidity provider responding with buy and/or sell prices. The general RFQ process (at the protocol level) is as follows:

The requester creates an RFQ by specifying the structure they want to trade, for example, an ETH contract with a settlement date of 2026-01-01. The requester can broadcast the RFQ to the entire globe (all liquidity providers) or to specific whitelisted liquidity providers.

Liquidity providers meeting the criteria can respond with a quote. Each quote includes terms:

The price at which the trade will execute. Liquidity providers can quote a two-way price (with both a buy and sell price) or a one-way price (either a buy or sell price).

The settlement pool where the trade will be booked. This can be an existing pool between the parties (if it exists) or a new pool created alongside the trade. Whether the trade will use an existing pool or a new pool, margin requirements, liquidation penalties, and other pool parameters are proposed here before the quote is accepted.

If the terms are acceptable, the requester can choose to accept a quote. At this stage, the requester needs to approve a smart contract call to move collateral into the pool. However, funds will not actually move until the final confirmation stage with the liquidity provider.

The quoting party has a final confirmation stage, which is a final confirmation of the transaction and all terms. If the quoting party gives final "OK" approval through a smart contract call, the pending transaction will proceed to the settlement process. If a new settlement pool needs to be created, it will be done at this stage. At this point, both parties' collateral is moved into the pool, the transaction is recorded, and the new position will be reflected in the pool's ledger.

In summary, Variational represents a fundamentally different derivatives trading approach. By combining a request-for-quote (RFQ)-based execution model with vertically integrated liquidity provision, Variational serves as a properly constructed perpetual contract DEX aggregator; abstracting fragmented liquidity across CEXs, DEXs, DeFi protocols, and OTC markets into a single, zero-fee trading interface.

The result is a system that can provide institutional-grade pricing, broad market coverage, and capital efficiency while directly returning a portion of the market-making profits to traders through loss refunds and rebates. Traditional perpetual contract DEXs rely on external market makers and fee extraction, while Variational internalizes liquidity supply, adjusts incentive mechanisms, and removes unnecessary intermediaries. This design transforms Variational not just into another perpetual contract venue but as an execution layer connecting retail and institutional trading within a unified on-chain framework.

Key Points

The long-term trajectory of DEXs is not a winner-takes-all battle but a progressive improvement cycle driven by self-custody demand and capital efficiency. As traders increasingly value retaining control of their assets, DEXs will continue to gain traction.

However, once the metatrend of perpetual contract DEXs takes off, there will inevitably be dozens of teams eager to launch cheap knockoffs and point-driven clones, more aimed at extracting fees from those farming the "next big DEX" before the opportunity window closes than truly optimizing for traders. This is the same late-cycle behavior we have seen in every successful metatrend, essentially a saturation phase where it is best to just protect your capital.

What we are witnessing now is strikingly similar to the broader crypto cycle:

Paradigm shift and great success: a high-quality trailblazer reshapes expectations; Hyperliquid pioneered deep on-chain liquidity, a unique technical architecture, and set a new standard.

Latter entrants with tangible value propositions: Protocols like Lighter and Variational highlight a specific structural advantage (Lighter's zero fees and Variational's zero fees, RFQ-based aggregator model, and trading rebates).

Saturation and Low-Quality Latecomers: As the narrative becomes crowded, latecomers and derivative knockoffs abound, many of which offer little differentiation beyond speculative returns. This reflects the saturation phase seen in NFTs, yield farming stablecoins, ICO mania, and even early perpetual markets like GMX and its myriad forks.

This pattern is a structural feature of crypto narratives. Early entrants capture outsized opportunities by establishing new paradigms that many traders have yet to price in. Early latecomers can still profit if they meaningfully differentiate. Latecomers, however, face a straightforward reality:

Most will never have true liquidity and cannot offer any meaningfully better option for serious traders.

For users, once a meta-trend is crowded, preserving capital often makes more sense than spreading funds across redundant farming activities.

Differentiation is a key factor in paradigm shifts

Hyperliquid represents a paradigm shift as it combines depth, unified liquidity, a fully on-chain order book, and achieves CEX-level performance on its homegrown L1.

Lighter achieves differentiation through the next very clear, opinionated bet: zero trading fees.

Variational takes a completely different approach by adopting an RFQ-based aggregator model, abstracting fragmented cross-platform liquidity, and returning part of the market maker's profit to traders.

Trends will shift, and in some cases, competitors will still exist; ultimately, what sets them apart is the specific value they bring.

If you are farming a Perp DEX that seems functionally similar to these platforms: the same order book, no front token value prop, the same gamified playbook, then you are likely too late.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia