BofA Analysis: Why is Meta Given the Lowest Valuation in the AI Arms Race?

TL;DR

· BofA raised capital expenditure forecasts for Alphabet, Meta, and AWS, stating that the combined capacity by 2027 could reach 57GW.

· A model breakdown shows that Meta's implied value per GW of AI capacity is around $4 billion, much lower than the two major cloud providers.

· Meta appears to be the cheapest, but enterprise AI sales, power access, and customer payments are still not fully proven.

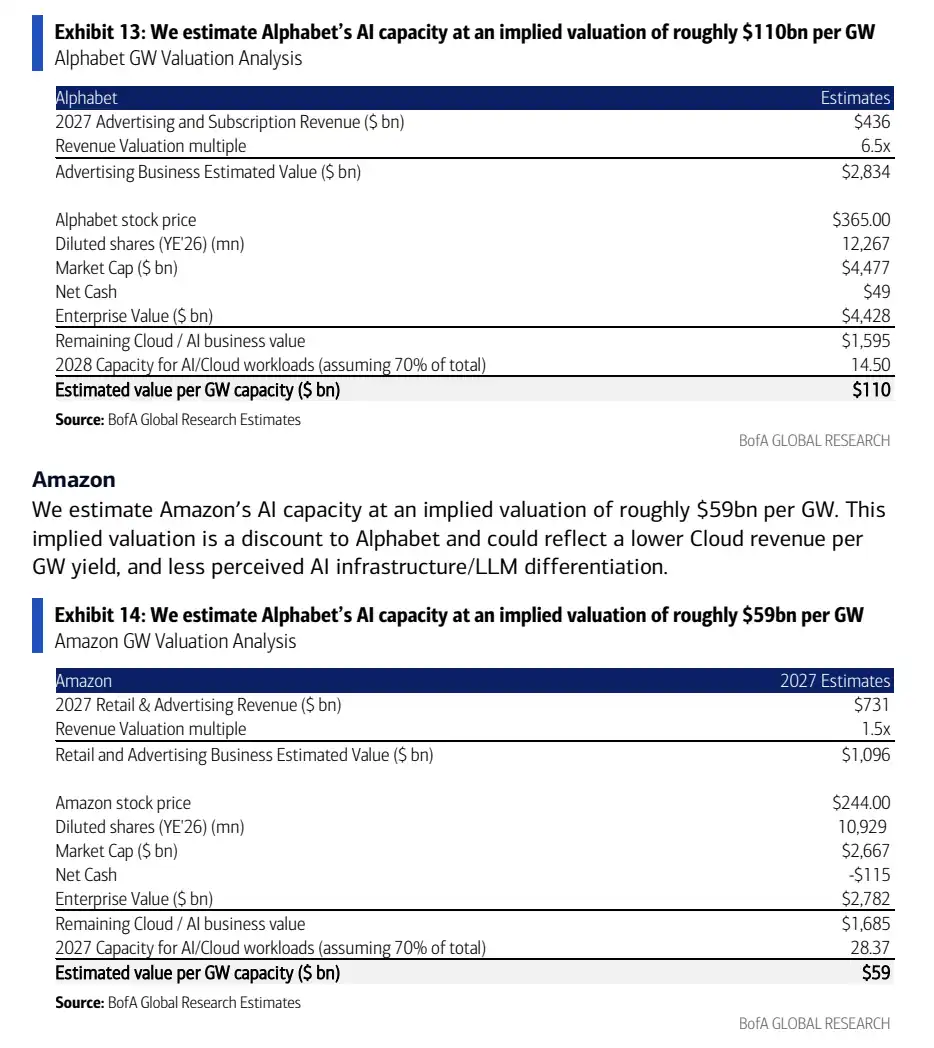

BofA has raised its outlook for future capital expenditures and data center capacity for Alphabet, Meta, and Amazon AWS in its latest report, providing a stark valuation split: according to its model, Meta's implied value per GW of AI capacity is only about $4 billion at the current stock price, far below Alphabet's about $110 billion/GW and Amazon's about $59 billion/GW.

The highlight of this report is not about who is spending the most money, but that for the same AI data center expansion, the market has assigned vastly different prices to the capacity of different companies. AWS and Google Cloud have mature cloud businesses and can sell computing power to enterprise customers. Meta relies more on its advertising business, AI recommendation efficiency, and early-stage enterprise AI products, with the data center value reflected in its stock price also being lower.

For investors, AI capital spending ultimately needs to answer a practical question: can power, GPU, and data center capacity translate into cloud revenue, enterprise AI service revenue, or higher advertising efficiency. The discount on Meta's valuation is precisely because this question has not yet been fully embraced by the market.

Big Three to Reach 57GW Capacity by 2027, Capital Expenditure Continues to Rise

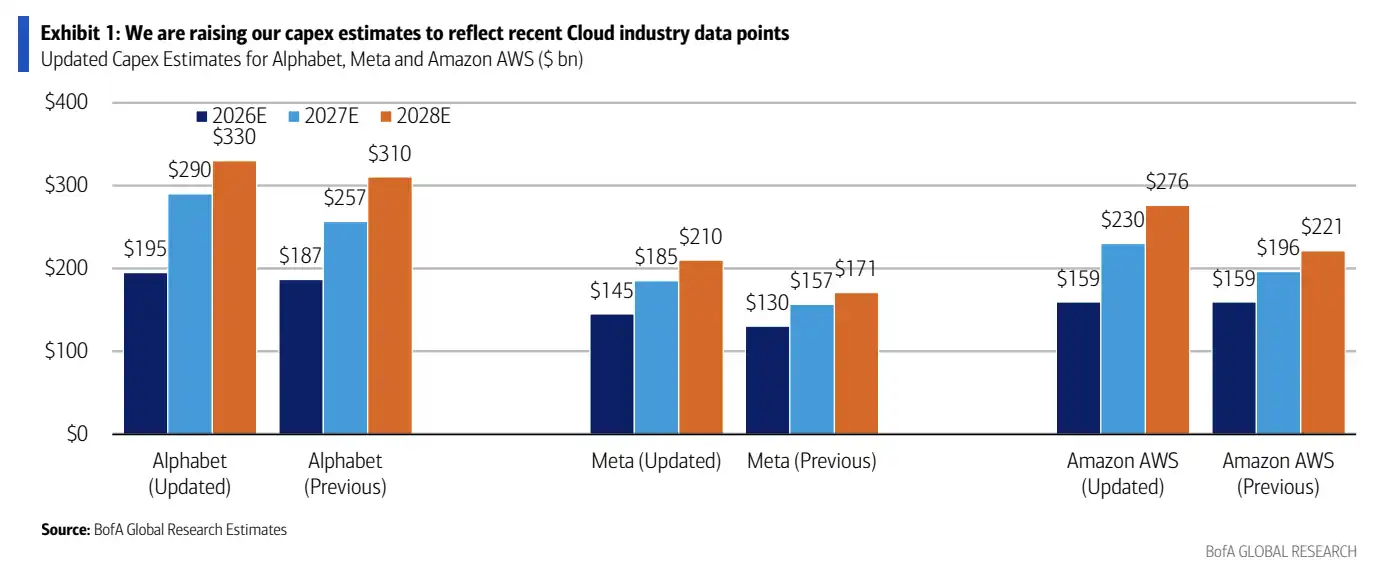

According to BofA's forecast, capital expenditure expectations for Alphabet, Meta, and AWS from 2026 to 2027 have been revised upward overall. Specifically, Alphabet's 2026 capital expenditure forecast has been raised from $187 billion to $195 billion and from $257 billion to $290 billion in 2027. Meta's 2026 expenditure has been increased from $130 billion to $145 billion and from $157 billion to $185 billion in 2027. AWS is maintaining $159 billion for 2026 and increasing it from $196 billion to $230 billion in 2027.

These figures are closer to BofA's model predictions and do not entirely align with the companies' public guidance. Publicly, Meta had previously raised its 2026 capital expenditure guidance to $125 billion to $145 billion, and Alphabet's public guidance is around $180 billion to $190 billion.

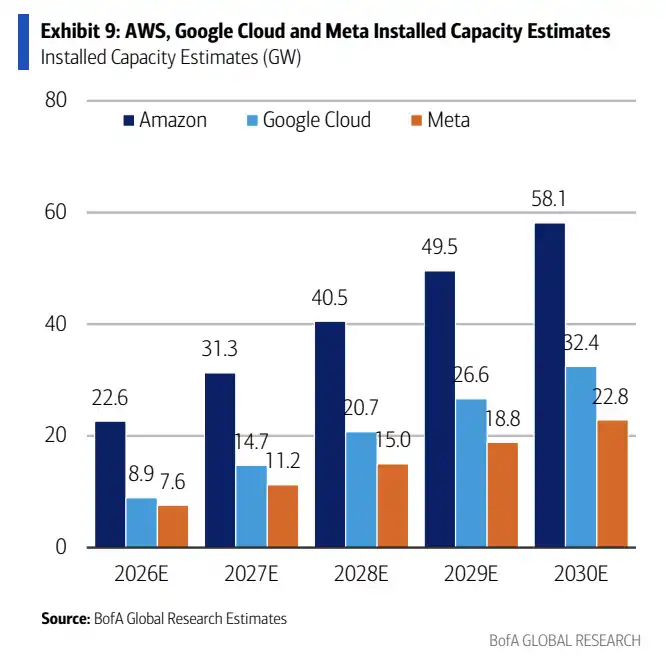

In terms of data center capacity, Bank of America estimates that the three companies will have a total of approximately 27GW by the end of 2025, increasing to 39GW by 2026, and further to 57GW by 2027. In other words, there will be an additional capacity of about 30GW within two years.

The largest increase will be from Amazon. From 2026 to 2027, AWS is expected to add around 15GW, Google around 9GW, and Meta around 6GW. AWS itself has a larger cloud infrastructure base, with customer demand, internal e-commerce, and AI services collectively absorbing capacity, making it the largest in terms of expansion scale.

An analysis comparing Alphabet, Meta, and AWS's capital expenditure forecasts for 2026-2028 shows the most significant upward revision in 2027.

Building the same 1GW capacity incurs different costs. According to Bank of America's estimates, in 2026, the cost per additional GW of capacity is approximately $25 billion for Amazon, $37 billion for Google, and $45 billion for Meta. Amazon has the lowest cost, mainly due to scale advantages and self-developed chips. Meta has the highest cost, more influenced by early-stage construction investment and external GPU dependencies.

This puts Meta in a more awkward position: it does not have the highest additional capacity, but the construction cost per GW is higher. If it cannot smoothly generate corporate income in the future, or cannot be clearly reflected in advertising efficiency, the market will find it even more challenging to assign a higher valuation to this part of its assets.

Widening Valuation Gap: Meta's Value Is Only $4 Billion per GW

Bank of America's valuation breakdown method first strips away the value of the three companies' traditional businesses and then deduces the implicit value the market assigns to AI capacity.

Based on multiples of core advertising, retail, and other revenue in 2027, Meta's AI capacity is implicitly valued at only about $4 billion per GW. Alphabet is around $110 billion per GW, and Amazon is about $59 billion per GW.

This gap directly points to the different commercialization paths of the three companies. The market is more willing to view Alphabet and Amazon's data center capacity as assets that can be monetized, but remains notably cautious about Meta's AI capacity.

Comparison of implicit valuations per GW of capacity: Alphabet around $110 billion, Amazon around $59 billion, Meta around $4 billion.

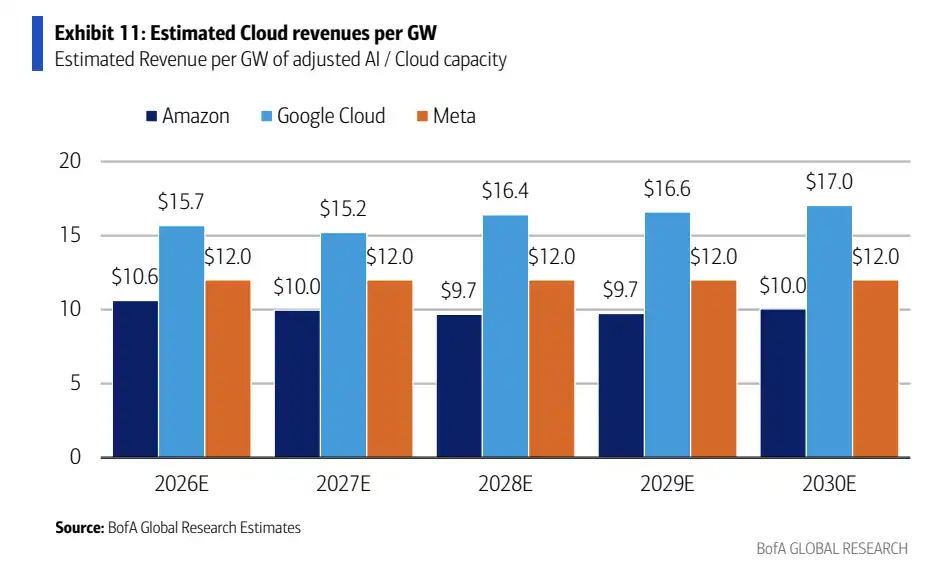

The capacity of AWS and Google Cloud is more easily tied to cloud revenue. According to Bank of America's model, by 2026 AWS is expected to generate around $10.6 billion in cloud revenue per GW, while Google Cloud is expected to generate around $15.7 billion. Enterprise customers purchase cloud computing power, AI training, and inference services, making the revenue path relatively clear.

Meta, on the other hand, is different. It has a massive advertising business and AI recommendation systems, but enterprise AI revenue is still in its early stages. Even as Meta accelerates the construction of AI data centers, the market will still question: Will this capacity mainly enhance its own advertising efficiency, or will it be able to be sold externally like cloud providers?

If primarily used for internal products, the valuation method will be more aligned with advertising efficiency improvements rather than independent cloud infrastructure assets. For Meta to achieve a higher valuation per GW, the market needs to see a clearer path to enterprise AI products, subscription revenue, or Business Agent sales.

Meta's Upside, Stuck on Whether It Can Sell the Capacity

In Bank of America's optimistic calculation, by 2030, Meta's data center capacity could reach around 22.8 to 23GW. If 40% of this is used for enterprise AI sales and calculated based on $12 billion/GW in revenue, the corresponding potential enterprise revenue opportunity is around $110 billion.

These are still model assumptions, not management targets, nor confirmed revenue opportunities. It explains where the "Meta is undervalued" narrative comes from: if in the future Meta can productize some AI capacity, sell AI services to enterprises, offer subscription products, or utilize Business Agent capabilities, then the current implied value of around $4 billion/GW appears very low.

Forecast for 2026-2030 Amazon, Google Cloud, and Meta installed capacity growth, with Meta's capacity reaching approximately 22.8GW by 2030.

The issue is, this assumption has not yet materialized. AWS and Google Cloud already have customers, contracts, and cloud revenue metrics, while Meta needs to prove itself not just as "building compute for itself" but also as a creator of sustainable enterprise AI revenue.

The report outlines potential catalysts, including cloud gross margin improvement, increased visibility into Meta's enterprise AI and subscription products, and more AI revenue breakdown disclosure. Some of the more forward-looking products and partnerships are still at the assumption level and cannot be directly regarded as realized business contributions.

Estimated cloud/AI revenue per GW for 2026-2030: AWS around $100-106 billion, Google Cloud around $152-170 billion, Meta's conservative estimate around $120 billion.

For Meta, what can truly change market perception is not another announcement of a larger data center plan, but showing investors what this capacity can bring in terms of revenue. Especially in terms of enterprise AI sales mix, product form, and revenue disclosure, these are currently not clear enough.

The Cheapest Asset, Yet Most in Need of Proof

Meta appears to have the lowest AI capacity valuation among the three companies, but cheapness itself is not the answer.

The first constraint is power. The U.S. Department of Energy's website previously quoted EPRI estimates that by 2030, data center power consumption could account for as much as about 9% of U.S. electricity, up from about 4% in 2023. Recent EPRI and Lawrence Berkeley National Laboratory research ranges higher, indicating that power pressures could continue to rise. Power access, transmission, local approvals, and energy prices will all affect whether GW capacity in the plan can be deployed on time.

The second constraint is chips and construction delivery. GPU supply, network equipment, power infrastructure, and construction cycles will all affect the pace of deployment. An increase in capital expenditure does not mean immediate capacity online or immediate revenue recognition.

The third constraint is customer payment. Enterprise AI demand is still growing, but more financial data is needed to validate how much customers are willing to pay for the scale of inference, training, and AI agent services. For Meta, if enterprise AI revenue cannot be clearly disclosed for a long time, the market will find it difficult to value its data center capacity according to cloud vendor standards.

Therefore, the Bank of America report does not conclude that "Meta has already realized the value of AI," but rather provides a more direct valuation gap: against the backdrop of the three major Internet giants continuing to expand AI capital expenditures, the market gives Meta's data center capacity the lowest price. It has the most to prove, not only to build out capacity but also to convince investors that this capacity can turn into visible revenue.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia