SemiAnalysis Insights: NVIDIA Secures GPU Financing, AI Compute Enters the Credit Era

TL;DR

· SemiAnalysis estimates that by 2029, AI-related outstanding debt could reach $7.1 trillion, with AI development becoming more reliant on the credit market.

· NVIDIA has introduced a revenue-sharing and credit support model for AI cloud, with Sharon AI and Firmus being the first partners.

· Backstopping can alleviate bank concerns, but rent decline, data center shortages, and contingent liabilities remain key risks.

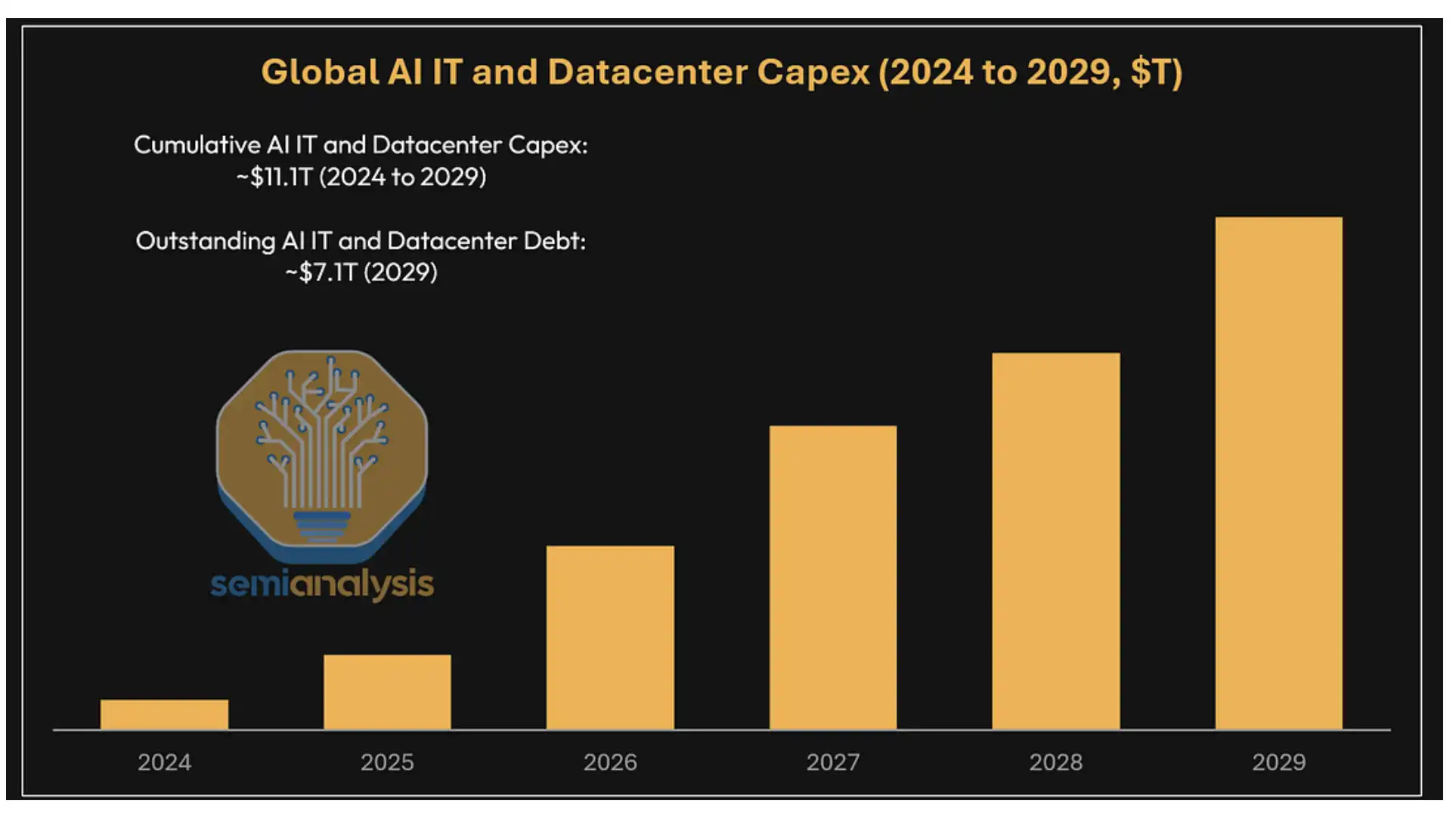

A report released by SemiAnalysis on July 6 brings AI infrastructure financing to the forefront: from 2024 to 2029, global AI capex could total around $11.1 trillion, and by 2029, outstanding AI-related debt could exceed $7 trillion, approximately $7.1 trillion.

This is not just a GPU sales forecast. The core shift discussed in the report is that AI development is transitioning from "tech giants buying GPUs with cash flow" to "banks and the bond market financing GPU clusters." If this estimate materializes, AI-related debt could become a giant asset-backed financing category second only to the U.S. mortgage-backed financing market.

NVIDIA's role is also changing. In an official blog post on July 1, NVIDIA confirmed the launch of a "revenue-sharing and credit support model" for AI clouds, driving AI infrastructure development through a combination of capital partners, cloud service providers, and data center projects. Sharon AI and Firmus are the first partners.

SemiAnalysis further suggests that NVIDIA may help Neocloud package GPUs, customer orders, and data center capacity into financeable assets through GPU revenue backing, revenue sharing, and similar structures. For lenders, the key is not how hot future AI demand is, but whether the project can still generate cash flow for debt repayment under the worst-case scenario.

Global AI IT and Data Center Capex and Debt Forecast: Cumulative capital expenditure from 2024 to 2029 is approximately $11.1 trillion, with outstanding debt in 2029 estimated at around $7.1 trillion.

AI Development Getting More Expensive; Banks Want to See Who Will Pay the Rent First

In recent years, AI infrastructure has been mainly shouldered by mega-scale cloud providers like Google, Amazon, Meta, Microsoft, Oracle, and others. These companies have cash flow, balance sheets, and internal AI demand, making financing relatively easier.

However, as AI training and inference requirements continue to grow, it is difficult for a few giants' capital expenditures alone to cover the entire compute gap. SemiAnalysis estimates that the annual AI capital expenditure will far exceed $20 trillion by 2028. GPUs, networking, storage, auxiliary CPUs, and data center construction will all require substantial funding, with the credit market being one of the sources of funds.

Neocloud's financing difficulty also lies here.

These new cloud service providers typically need to achieve three things at the same time: acquire GPUs, secure data center capacity, and sign up future customers. The most challenging aspect for banks is to assess whether GPU rental income over the next few years can cover debt service. AI compute power leasing prices change rapidly, customer lease terms are not uniform, and GPU residual value and utilization rate are also more difficult to estimate than traditional infrastructure.

NVIDIA's credit support model attempts to provide loan institutions with a clearer cash flow bottom line. While the official statement mentions revenue sharing and credit support, SemiAnalysis describes the typical structure as GPU revenue backing.

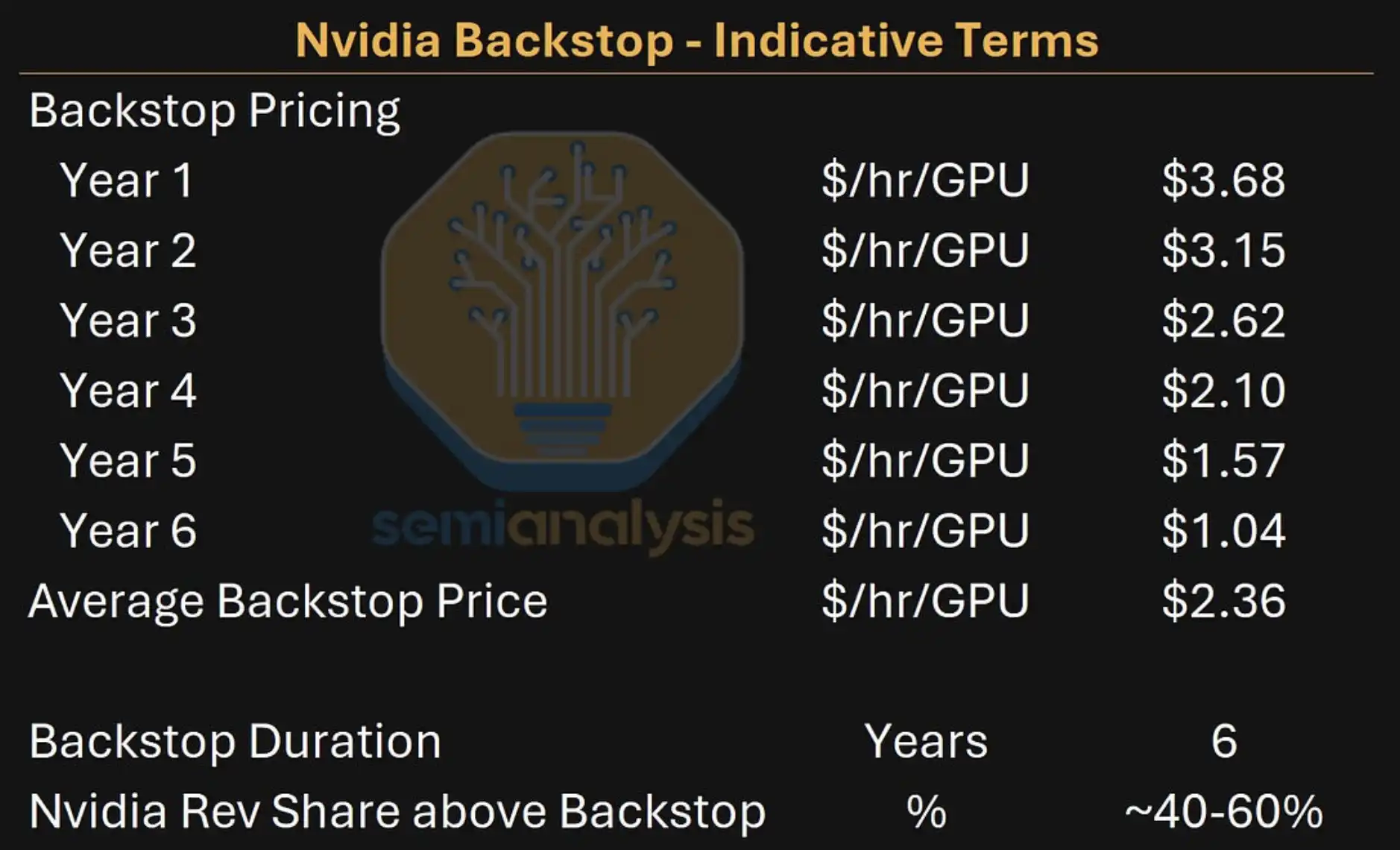

6-Year Average Backing Price of $2.36, Short-Term Lease Scenario IRR Up to 25%

The example structure provided by SemiAnalysis is that NVIDIA provides a 6-year minimum revenue support for a specific GPU cluster, with a price curve decreasing annually, averaging around $2.36/hour/GPU over 6 years. If the actual project rent is higher than the bottoming level, Neocloud and NVIDIA will then share income at a ratio of approximately 40% to 60%.

This is not an officially disclosed accounting term by NVIDIA but an indicative estimate in the SemiAnalysis model. Its appeal to loan institutions is that it can partially transform a highly uncertain GPU leasing project into an asset with a commitment to minimum cash flow.

Banks do not necessarily have to fully believe that future AI leasing prices will remain high. As long as the project can still meet debt service coverage requirements in a bottoming scenario, loans may be obtained. According to SemiAnalysis' calculation, a cluster supported by NVIDIA's AA/Aa2 rating requires a debt service coverage ratio of at least about 1.3 times, corresponding to a loan-to-value ratio of 70% to 80%. The initial financing spread may be higher than transactions supported by hyperscale cloud providers but lower than the 10% yield level of CoreWeave's unsecured bond contract.

NVIDIA Guidance for Backing: An average of around $2.36/hour/GPU over 6 years, with a 40%-60% revenue sharing arrangement.

For Neocloud, the backstop is not just insurance, but a key condition for the project to secure debt financing.

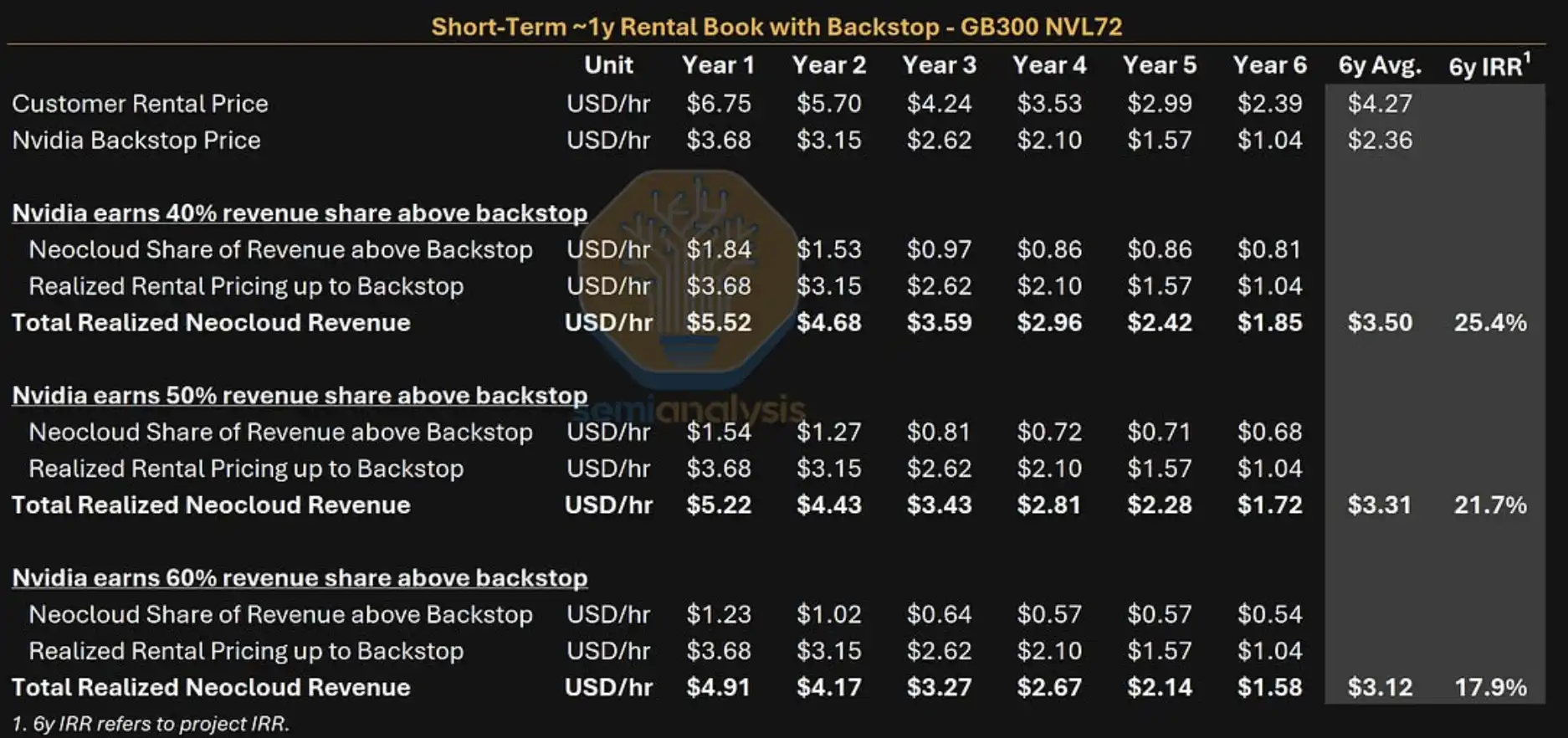

In the GB300 short-term one-year lease example, if the first-year rent is $6.75 per hour, Nvidia's revenue share is 40%, Neocloud's 6-year project IRR is around 25.4%, and Nvidia's average cut is about 18%. If market demand is insufficient and the project falls entirely into the backstop lease, Neocloud's IRR may approach zero or slightly negative.

While this is not friendly to equity returns, it is crucial for financing: project returns may be suppressed, but debt servicing still has a chance to be covered. In other words, the backstop transforms the GPU cluster, which "could potentially earn a lot of money," into a financing asset that "may still repay debt under stress scenarios."

GB300 Neocloud Return Comparison: Under the 40% revenue share, the 6-year IRR is around 25.4%, and when the backstop is fully triggered, the IRR is close to zero or slightly negative.

Sharon AI and Firmus First to Land, Asia-Pacific Projects as Testbed

Nvidia has confirmed that Sharon AI and Firmus are the first partners in this revenue-sharing and credit support model.

On June 12th, Sharon AI announced that the company has reached a 6-year strategic computational power cooperation with Nvidia, with a maximum deployment of 40,000 Grace Blackwell GB300 in a 72MW AI factory in Australia. Sharon AI's overall AI factory capacity plan aims to reach 132MW, with 102MW already contracted, expecting to deploy over 55,000 Nvidia GPUs by mid-2027.

Firmus's project in Batam, Indonesia, is on a larger scale. In an official Nvidia blog post, Firmus Batam project can expand to 360MW, deploying a maximum of 170,000 Nvidia GPUs. SemiAnalysis includes this project in discussions, stating it is mainly aimed at AI-native enterprises and inference service providers, and may offer diversified lease terms.

These cases illustrate that Nvidia's credit support model has moved beyond just a financial model assumption to entering the early project implementation stage. However, current publicly disclosed cases are mainly concentrated in the Asia-Pacific region, while the U.S. market still faces constraints such as data center capacity, power, and grid speed.

The data center remains the hardest bottleneck. GPUs can be purchased, customer demand can be signed, but progress in power, land, cabinets, cooling, and grid connectivity is challenging to replicate quickly. SemiAnalysis's model also suggests that Nvidia may need to directly lease data center capacity to help Neocloud bridge the supply-demand gap. The specific capacity and scale involved in this aspect are still part of estimated reports and cannot be equated with official Nvidia disclosures.

NVIDIA Can Take a Cut and Shoulder Larger Long-Term Commitment

For NVIDIA, supporting GPU financing has a dual benefit.

First, it can expand the sales and deployment of GPUs. With more Neoclouds receiving financing, more entities can purchase and operate large-scale GPU clusters, and the AI computing power market is no longer completely dependent on a few hyperscale cloud providers.

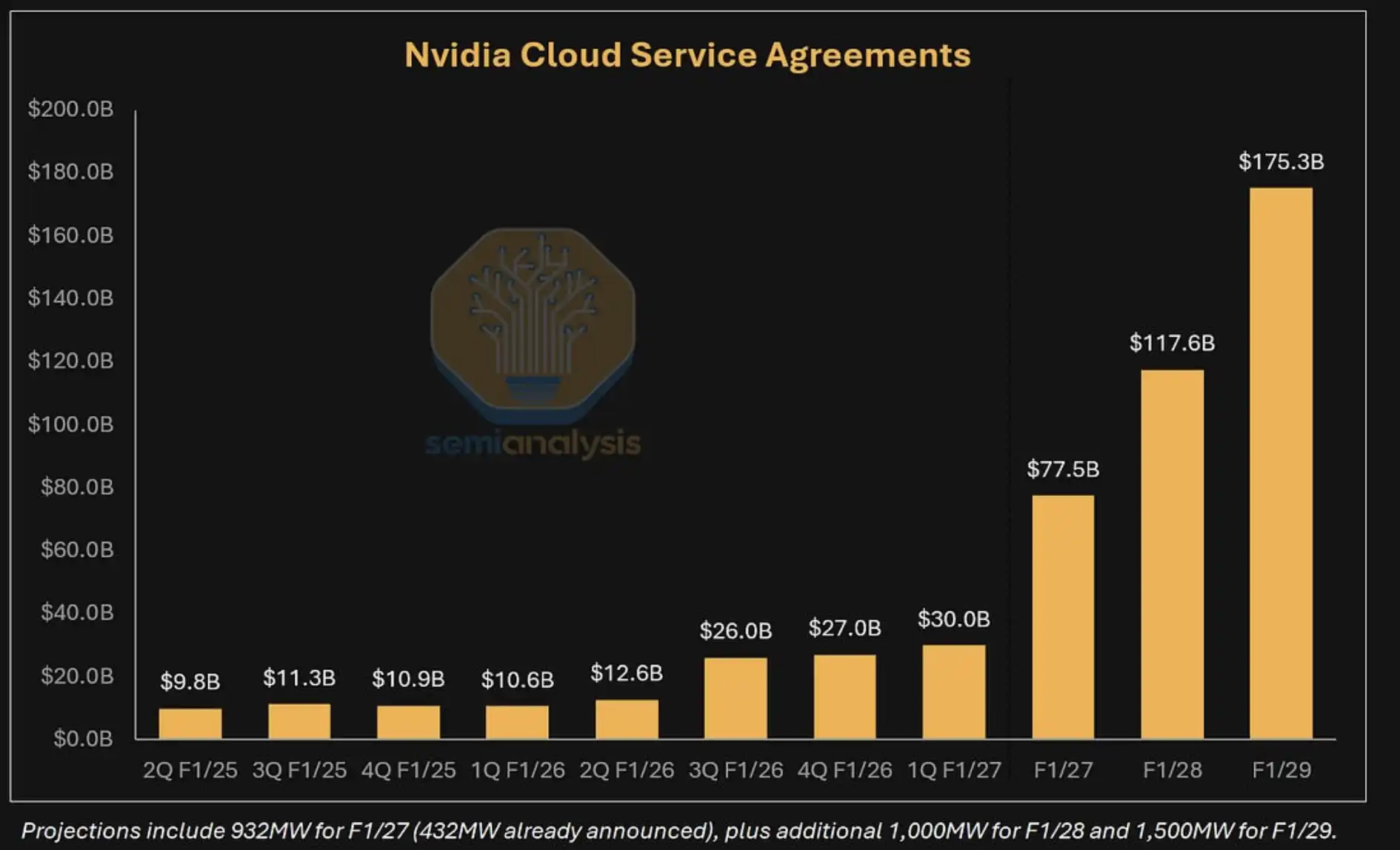

Second, it may receive additional revenue sharing. According to SemiAnalysis' model, if this type of structure continues to expand, NVIDIA's incremental revenue from backing and revenue sharing could become significant and with a higher profit margin.

The cost is also evident. NVIDIA's long-term commitments off-balance sheet or in related disclosures may quickly increase. In a paid report section, SemiAnalysis estimates that NVIDIA's cloud service agreements or guaranteed balance could rise to the tens of billions of dollars in the coming years. Since these figures have not been individually confirmed by NVIDIA, they are more suitable as a model stress test rather than established liabilities.

NVIDIA Cloud Service Agreement Growth Prediction: According to the SemiAnalysis model, related long-term commitments may continue to accumulate with each 100MW computing power support.

This is not debt in the traditional sense. However, if the GPU leasing market weakens and customer demand is insufficient, the likelihood of backing triggers increases, and NVIDIA will need to bear more minimum revenue support. In the end, the market will not only look at how much NVIDIA can earn from the revenue sharing but also whether these commitments will affect its own capital allocation and cash flow priorities.

The Ultimate Test is Whether Rent and Data Center Can Hold Up

The most impactful aspect of this report is placing AI computing construction into the credit market. When capital expenditures swell to the trillion-dollar level, GPU clusters are no longer just a tech product but also a financing asset evaluated by banks, bond investors, and cloud service providers.

However, the $7.1 trillion AI debt is still a forward-looking model prediction, not a fact. It relies on several assumptions: AI demand continues to expand, GPU utilization remains at a high level, leasing prices decrease at a controllable rate, data center construction can keep up, and lending institutions are willing to accept cash flow models supported by NVIDIA's credit.

The most susceptible areas are price and deployment speed. If GPU rents decline faster than expected, Neocloud's returns under high revenue sharing and financing costs will be compressed. If a large number of triggers occur, while the project may continue to repay debt, NVIDIA's commitments will become heavier. If there are delays in data center, power, and grid connection, the deployment time of GPUs in the financing model will also be disrupted.

The story of NVIDIA "GPU Lending" is aimed at the next phase of AI infrastructure funding. It can allow more computing power projects to receive loans and may also move NVIDIA to a more central position in the AI credit market. However, whether this market can grow to $7 trillion in the end will depend on rent, utilization rates, and data center deployment.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia