HODL Strategy, Creating a Permanent Sell-off Pipeline

Saylor spent four years telling everyone that Strategy will never sell Bitcoin. On June 29, his company released a document titled the "Digital Asset Framework," which essentially allows Strategy to sell up to $1.25 billion worth of Bitcoin. Following this news, MSTR surged nearly 7% in pre-market trading.

A company that believed in "never selling" announced a plan to sell its coins, yet the market saw it as a positive development. This is worth dissecting.

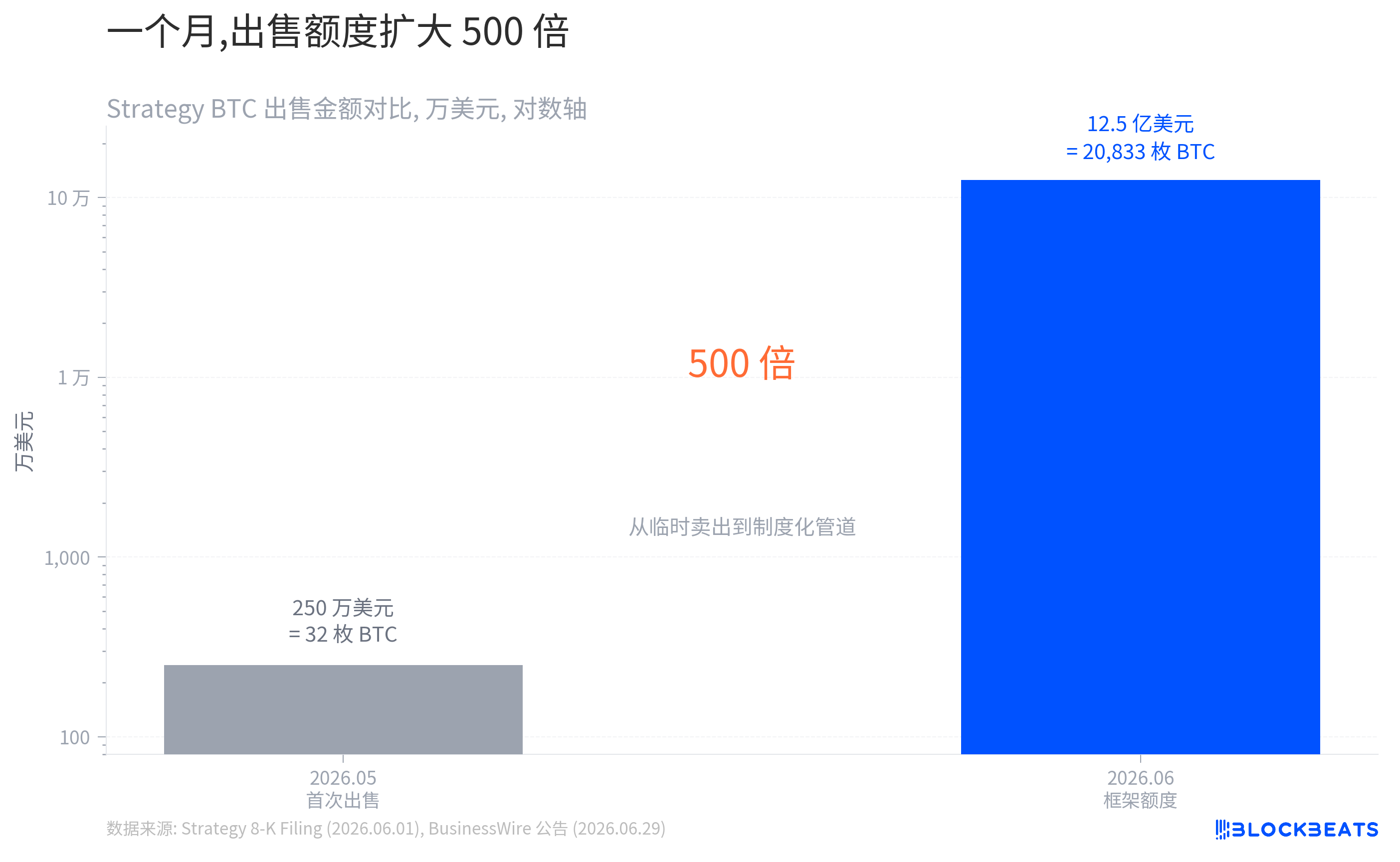

From 32 Coins to $1.25 Billion

By the end of May this year, as reported by CoinDesk, Strategy quietly sold 32 bitcoins, equivalent to about $2.5 million. This marked the first sale since 2022, with the direct purpose of paying off convertible debt. At that time, MSTR fell as investors felt that Saylor's promise of "never selling" had been broken.

One month later, the framework document increased the selling limit by 500 times.

At current prices, this limit is roughly equivalent to 20,000 bitcoins, accounting for 2.5% of Strategy's total holdings.

However, the change in scale is merely superficial. The real transformation lies in the nature of the sales. According to an 8-K filing submitted by Strategy, the May sale was classified as "ad-hoc," meaning it was temporary and incidental. In contrast, the new framework establishes an institutionalized pipeline, outlining four distinct use cases, including bolstering the dollar reserves, paying convertible debt interest, repurchasing its own convertible preferred stock, and buying back MSTR common shares.

Selling coins is no longer a temporary measure but has become an integral part of its operations. Strategy CEO Phong Le's language in the announcement was straightforward, stating that the company is shifting from "one-way capital issuance to active capital management." The transition from an exception to a system took just a month. The question is, what exactly is driving this transformation?

Price Drop, Rate Hike

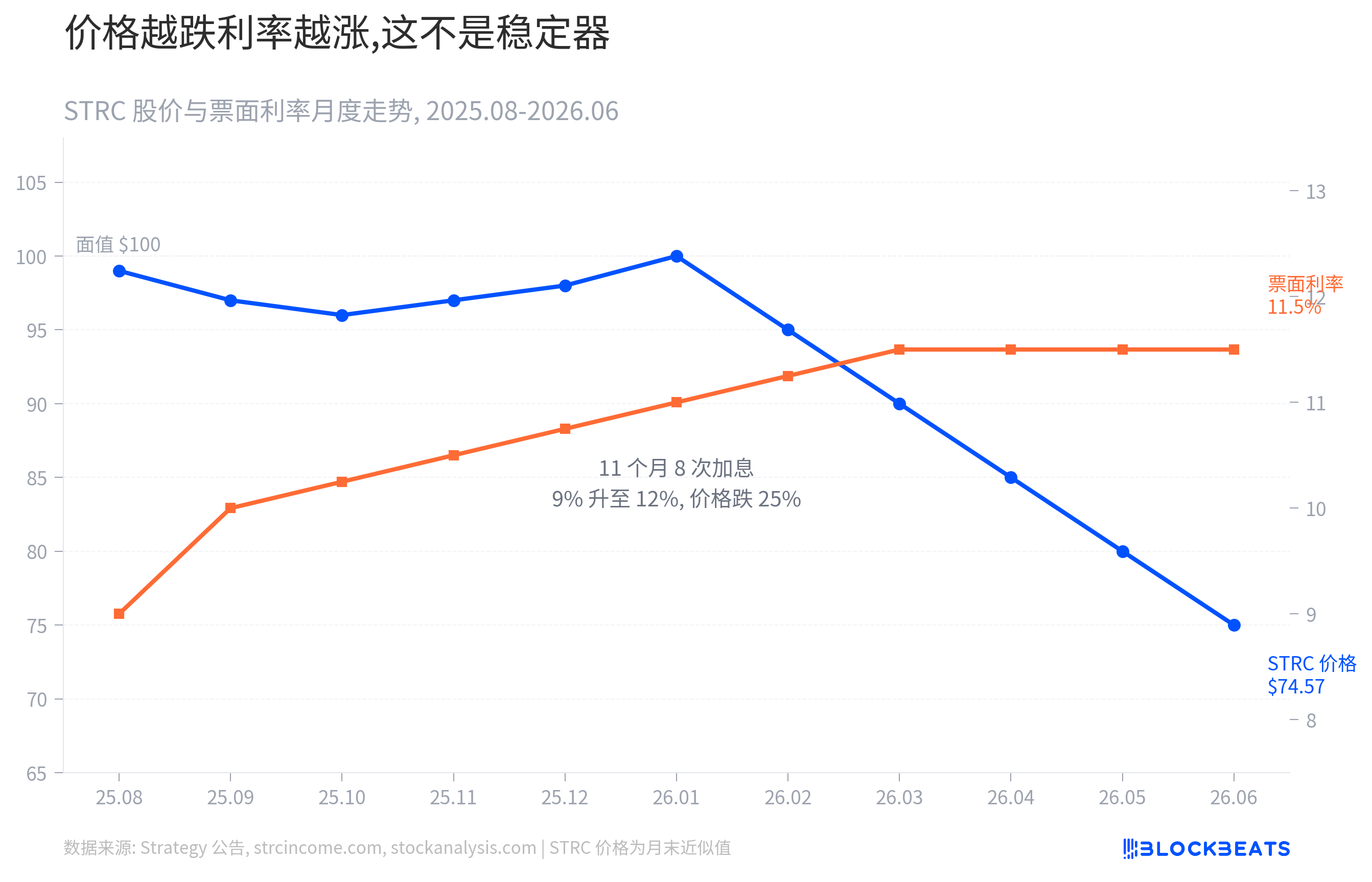

The answer lies within Strategy's largest convertible preferred stock, STRC.

STRC is a perpetual preferred stock issued in July 2025, with a face value of $100. According to a BusinessWire announcement, the issuance size is around $8.5 billion, making it the largest single preferred stock globally. STRC has a unique mechanism where the coupon rate is not fixed but resets monthly. In theory, raising the interest rate can attract buyers and stabilize the price.

In practice, it has indeed been constantly adjusted. According to strcincome.com's dividend records, the annual rate of STRC has increased from 9% to 12%. It has been adjusted 8 times in one year, averaging once every six weeks, each time meaning Strategy has to pay a little more for this world's largest preferred stock.

But the rate hikes did not stabilize the price; instead, the more they adjusted, the more it fell. According to stockanalysis.com data, STRC has dropped from face value to $74.57, a deviation of over 25%.

Related Reading: "STRC Falls Below $80, Can Financialists Still Bottom Fish?"

The scissor spread in the chart began to widen rapidly from early 2026. Each rate hike means Strategy has to pay more money for each share, and each price drop means the market doesn't believe it can afford it. The interest rate hike was supposed to be a stabilizer, but it turned into an accelerator.

How expensive is this scissor? STRC has a principal amount of $8.5 billion with a current interest rate of 12%.

Just from this, the annualized dividend exceeds $1 billion.

In addition to STRC, Strategy also has three preferred stocks, STRK, STRF, STRD, and around $6.7 billion in convertible bonds. According to the company's announcement, the annualized fixed obligation of the entire capital structure has reached $1.76 billion.

What does $1.76 billion mean? It's roughly equivalent to burning $4.8 million every day.

According to the same announcement, Strategy's USD reserves amount to $2.55 billion, at this consumption rate enough to last approximately one and a half years. Adding the Bitcoin liquidation limit of the framework, the coverage period can be extended to over two years.

This is the reason for the framework's existence. It is not selling Bitcoin in the market but providing an increasingly expensive capital structure with an oxygen tube extension.

What If the Price Falls Again?

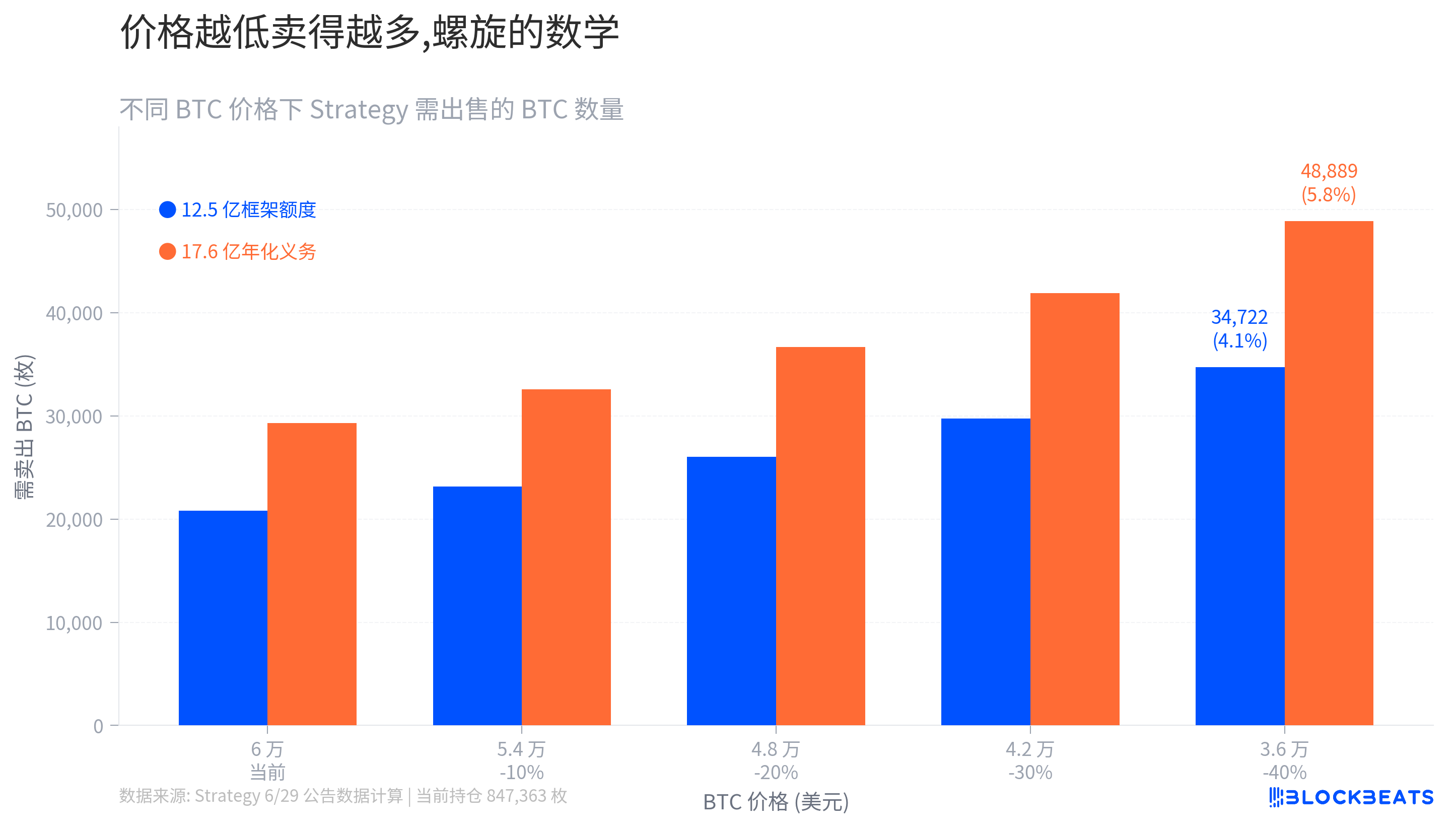

How long the framework can last depends on the price of Bitcoin. This is a simple yet brutal math problem.

At the current price, the framework would need to sell approximately 20,000 Bitcoins, accounting for 2.5% of the total holdings. This proportion seems manageable. However, as seen in the chart below, as the price drops, the required sell-off quantity rapidly increases. If Bitcoin falls by 40%, the same amount would require nearly twice the quantity to exchange.

Of particular interest is the scenario outside the framework. According to VanEck's analysis, if all annualized obligations need to be covered by selling BTC, under the most extreme price assumption, the Strategy would need to sell nearly 50,000 BTC in a year, representing 5.8% of the holdings.

There is a self-reinforcing cycle at play here. A decline in the Bitcoin price would reduce MSTR's NAV multiple. According to Trefis' analysis, MSTR's current mNAV is around 0.64x, meaning the market values each $1 of Bitcoin in the Strategy at only $0.64.

What does a mNAV below 1 signify? At this discount level, executing At-the-Market (ATM) offerings is akin to selling one's Bitcoin at a discount. According to several institutional analyses, this was once the primary funding route for the Strategy and is effectively now frozen.

Options are limited. If the USD reserves continue to deplete, the STRC's depegging worsens, leading to a forced increase in interest rates. Higher interest rates escalate the annualized obligations, compelling the Strategy to sell more Bitcoin, increasing selling pressure that further depresses the Bitcoin price. Selling BTC may not necessarily break this cycle and could even accelerate it.

However, the 5.8% annual depletion is under the most extreme assumption. As per the announcement, the Strategy's reserves combined with the framework capacity total $3.8 billion, enough to cover obligations for over two years. Large-scale coin sales are not needed in the short term.

The rationale behind the 7% market surge may lie here. Prior to the framework's unveiling, investors priced in a bleaker scenario, where the Strategy might be forced into disorderly Bitcoin liquidations, possibly failing to meet preferred stock dividends. The framework replaced panic with an institutionalized solution. According to Bohan Jiang, Senior Derivatives Trader at FalconX, the framework is "positive for both common and preferred stockholders."

However, easing liquidity concerns does not equate to resolving structural issues. The $17.6 billion in annualized obligations will not decrease due to the framework's presence, and the STRC's interest rate remains at 12%. If the Bitcoin price does not recover, the length of this oxygen tube can be calculated.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia