Behind the Trend of "Stock Tokenization": Buying the Dip or Catching a Falling Knife?

Original Article Title: Tokenized Stock Boom: Time to Get Rich

Original Article Author: Ignas, DeFi Analyst

Original Article Translation: Saoirse, Foresight News

I believe there is only one way to get rich through tokenized stocks.

Of course, you can buy into these tokens hoping for a tenfold increase, but apart from very few exceptions like Micron Technology (MU), the likelihood of getting rich quick is extremely low.

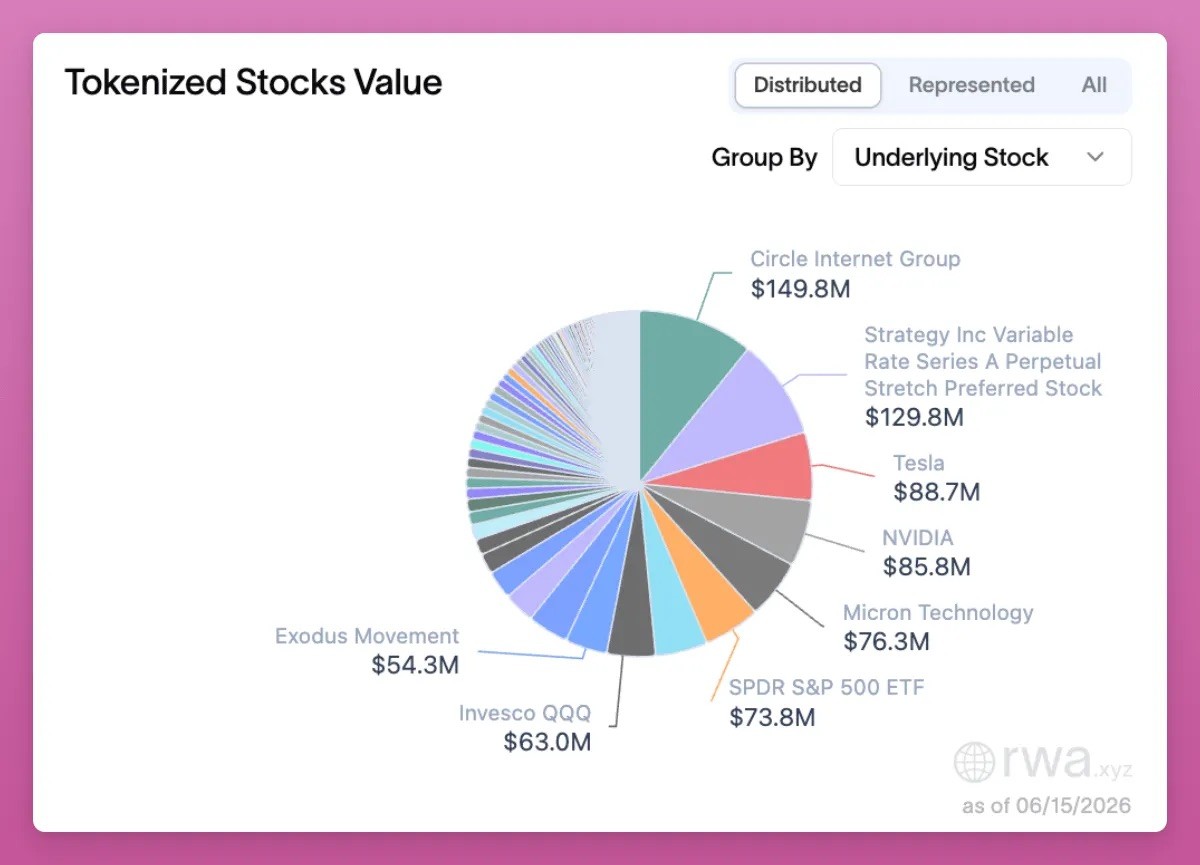

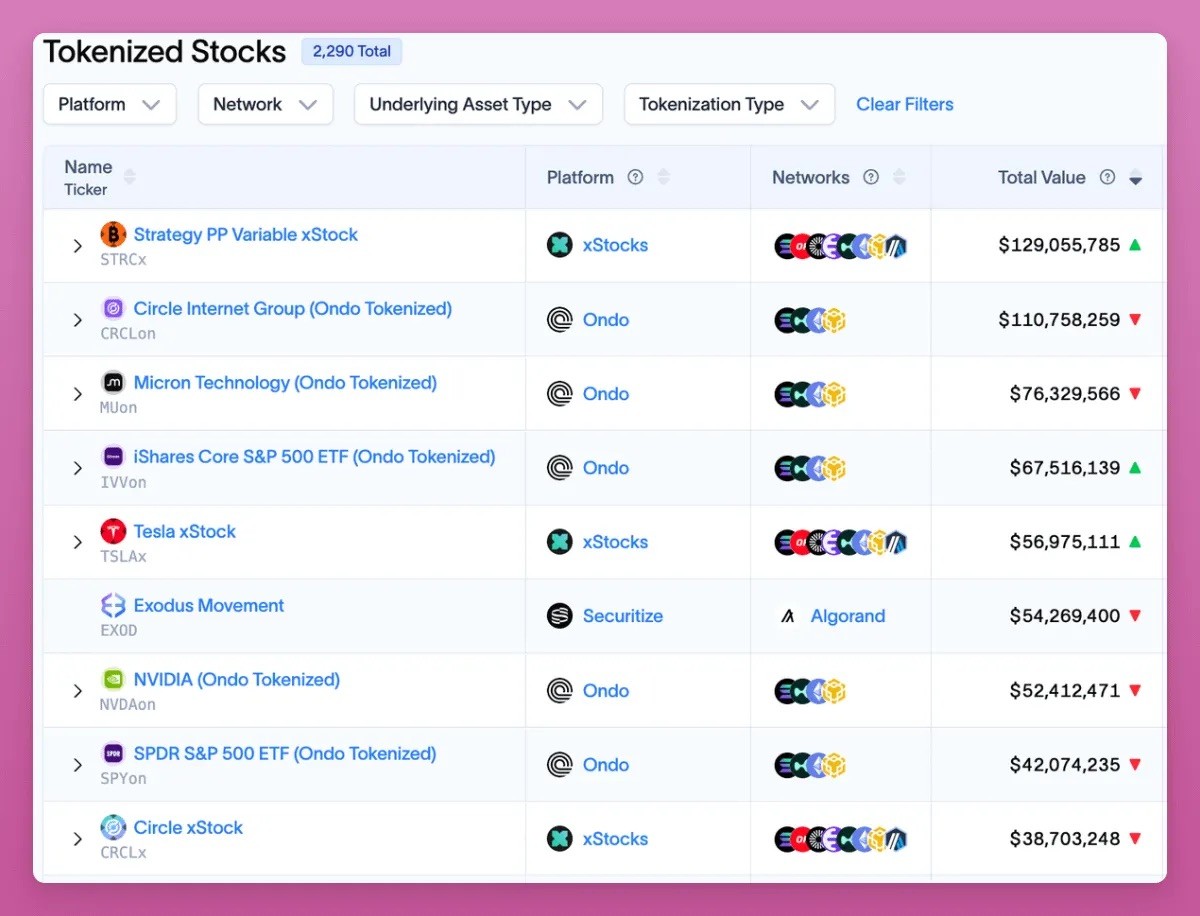

Firstly, only 2290 stocks have been tokenized so far, with only about 130 targets having a total market cap exceeding $1 million. The majority of tokenized stocks have little to no on-chain liquidity.

According to the RWA data website rwa.xyz, Strategy is one of the largest targets, with a total value of $129 million.

Currently, the tokenized stocks that have been completed are mostly shares of mature listed companies. If you want to explore undervalued and less recognized stocks, you may find more opportunities through traditional brokers like Interactive Brokers.

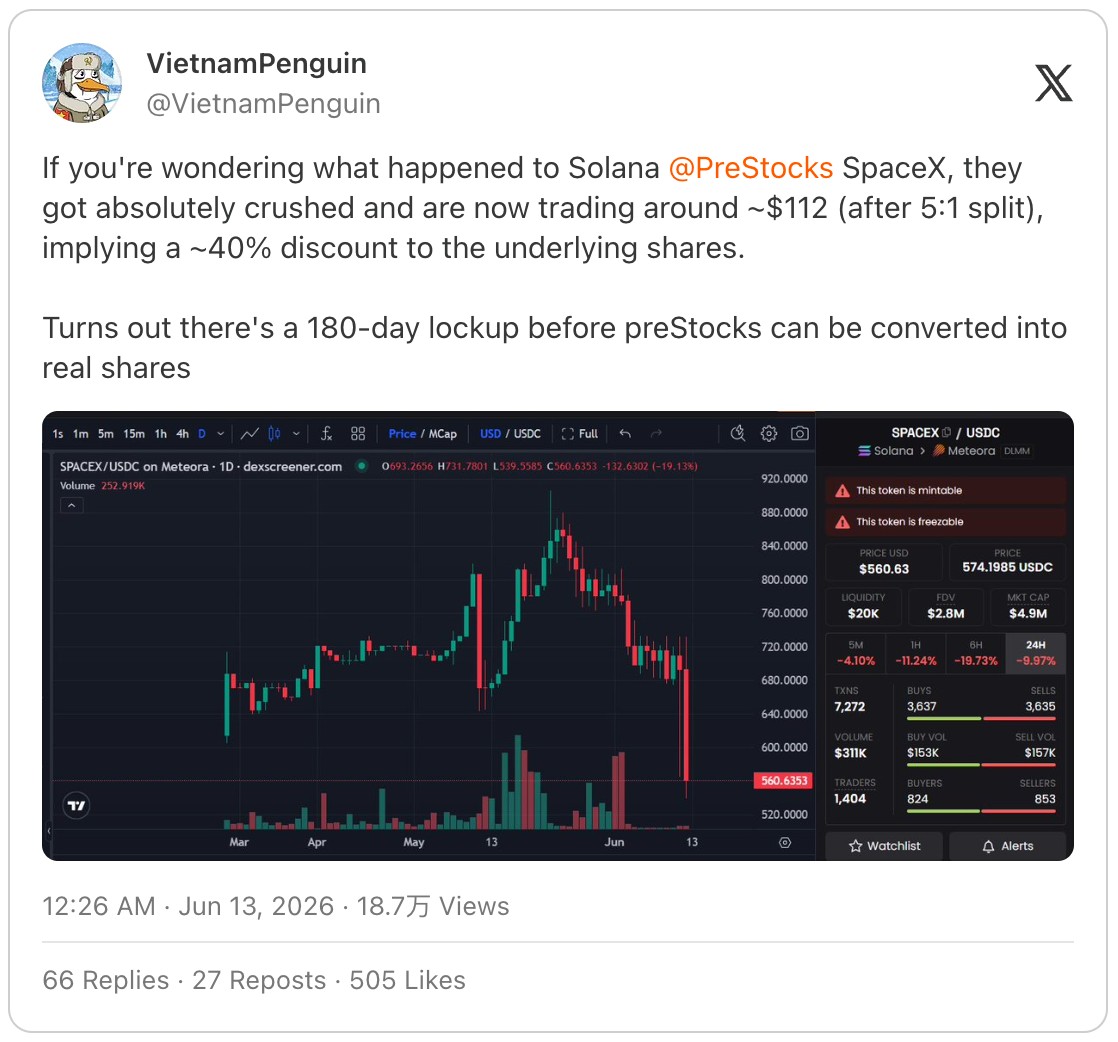

Secondly, holding tokenized stocks introduces many risks that are not present in traditional broker holdings. For example, investors who bought SpaceX tokenized stock (SPCX) on the PreStocks platform found that these tokens require a 180-day lockup period before they can be converted into real stocks, leading to a 40% price drop.

Source: https://x.com/VietnamPenguin/status/2065470925252759680

Therefore, investors not only need to bear the inherent smart contract risk of the crypto industry, the risk of self-custody assets (without the convenience of self-custody), and liquidity risk, but also the additional risks brought by the issuer and asset custodian.

However, I am not completely opposed to the tokenized stock track. It is one of the most potentially lucrative sectors in the crypto industry: it can attract new users and retain existing users who were planning to cash out their crypto assets to invest in the traditional financial market. Tokenized stocks bring on-chain transactions and fee income to the blockchain, attract venture capital and developers to the industry, and gain market attention.

Tokenized stocks themselves present numerous opportunities: you can provide liquidity to a decentralized exchange (DEX) pool to earn yields, use them as collateral for lending, hold the SPCX spot on-chain while shorting the corresponding perpetual contract to earn delta-neutral returns, and receive perpetual contract DEX platform tokens as a bonus.

Speaking of hedging strategies, you can buy tokenized stocks spot while shorting on the Variational platform. The platform's native token VAR currently offers a highly attractive airdrop opportunity:

· 50% of the total token supply will be distributed to the community;

· The mining activity will end on September 30, with only about a 3.5-month mining window left;

· After the token is listed, the team plans to allocate 30% of the platform's revenue for buyback and burn;

· The platform is currently in a closed testing phase.

Tokenized Stocks Are Not Part of the Early Investment Track

However, my biggest concern about tokenized stocks is this: fundamentally, this track has turned crypto investors into the bag holders of traditional financial assets.

The reason the crypto industry has created many millionaires in the past is that we were early in exploring new tracks: Bitcoin, smart contract platforms, various project airdrops, NFTs, and Hyperliquid airdrops, among countless others. SpaceX's tokenization listing process has made me realize this issue.

Its issuance model and the hype around secondary layer token issuance in crypto are identical: low circulating supply, extremely high fully diluted valuation, price movements completely detached from the company's fundamentals. In the short term, the traditional financial market is now in a phase similar to the "high fully diluted valuation is just a gimmick" phase the crypto industry experienced two years ago.

There is no denying that the space industry, artificial intelligence, and Starlink business sound promising, but aspects such as company valuation, equity unlocking schedule, revenue data, and governance mechanisms are far from optimistic.

The core value of tokenization lies in expanding asset distribution channels: any user with a Phantom, Metamask, Rabby wallet can hold these tokens. Their price volatility is lower than Bitcoin and altcoins, and unlike stablecoins pegged to the dollar, the risk-return profile falls between the two. For investors outside developed markets or users who do not want or cannot convert their crypto assets into the traditional financial system, tokenized stocks offer an attractive solution.

However, this does not mean we are seizing early investment opportunities. Crypto's past allure was to enable ordinary retail investors to invest in revolutionary early-stage companies. IPO projects with valuations in the trillions of dollars are far from being considered early-stage investments.

The future of the cryptocurrency industry with true long-term growth potential lies in enterprises achieving tokenization on the equity chain from the very beginning. ICOs and fair launches were once good attempts, but in the last bull market cycle, the industry increasingly preyed on retail investors: early-stage private sale valuations were inflated, Token Generation Events (TGE) were further hyped, and the token allocation for the general public was pitifully small. Cobie dissected this point very insightfully in his blog post.

Up until now, I am still participating in investments through Cobie's launched Echo platform because the platform truly provides early-stage project investment opportunities: my participation in the MegaETH round has already seen a 3.85x return on investment, even as the token's market performance has remained lackluster post-listing.

Apptronic is a humanoid robot company, and despite its high valuation, I also took part in its Series B strategic financing. Such investment opportunities are not open to ordinary retail investors on traditional financial platforms.

On a side note, apart from Echo, I am also very bullish on the Legion platform, but the platform still needs to discover high-quality investment targets with reasonable valuations, which is not an easy task.

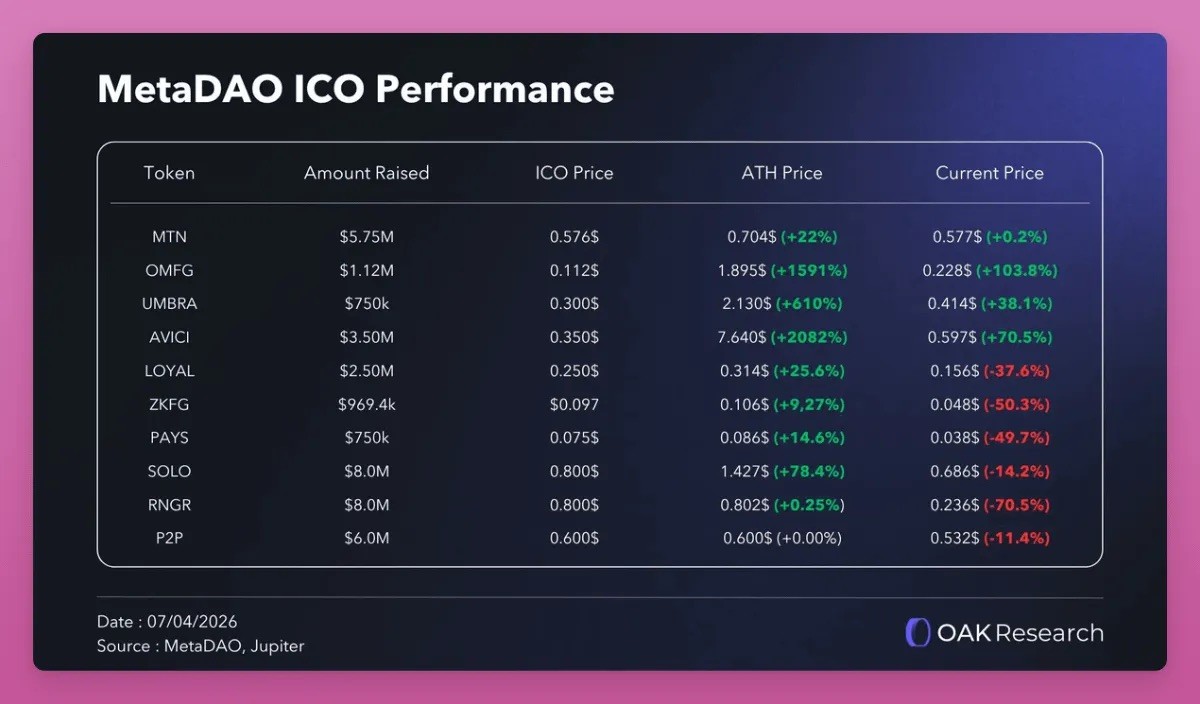

The model of MetaDAO is excellent: all ownership tokens issued by the platform grant holders legitimate equity, supervise treasury fund expenditures through quota control, and unlock tokens based on corporate performance, perfectly addressing the core flaws exposed in the initial token issuance years ago. It is for this reason that considering the current market environment, ICO projects launched on MetaDAO have generally performed better.

Source: X Platform OAK Research

In addition to this, there is also the on-chain native issuance model, such as the Opening Bell product line introduced by Superstate, with the first target being Galaxy stocks, where corporate equity is directly issued on-chain in a compliant manner.

Imagine if large enterprises did not go through the traditional IPO process offline but instead directly issued equity on Ethereum, Solana, and other public chains, rather than just using the blockchain to encapsulate offline legal equity certificates. At that time, the tamper-resistant and secure properties of the blockchain would become the industry's core competitive advantage, and the value of the tokens we hold would soar.

MetaLeX is precisely adopting this approach: building a fully programmable on-chain enterprise, where corporate capital, equity, and equity ownership periods are all managed on-chain.

Returning to the point, today, top centralized exchanges like Binance, Coinbase, and Kraken are heavily expanding into traditional financial services, launching tokenized stock, bond, and ETF products. However, the xStocks platform cannot deliver underlying physical stocks, leading Binance, Bybit, and Bitget to all delist SpaceX tokenized stock products, with over $1 billion in user orders unable to be fulfilled. In comparison, traditional brokers' trading orders are more reliable.

Stablecoins were originally only used for short-term asset holding while waiting to enter the crypto native asset market; today, stablecoins have become a liquidity exit point for the funds of elderly investors from traditional finance.

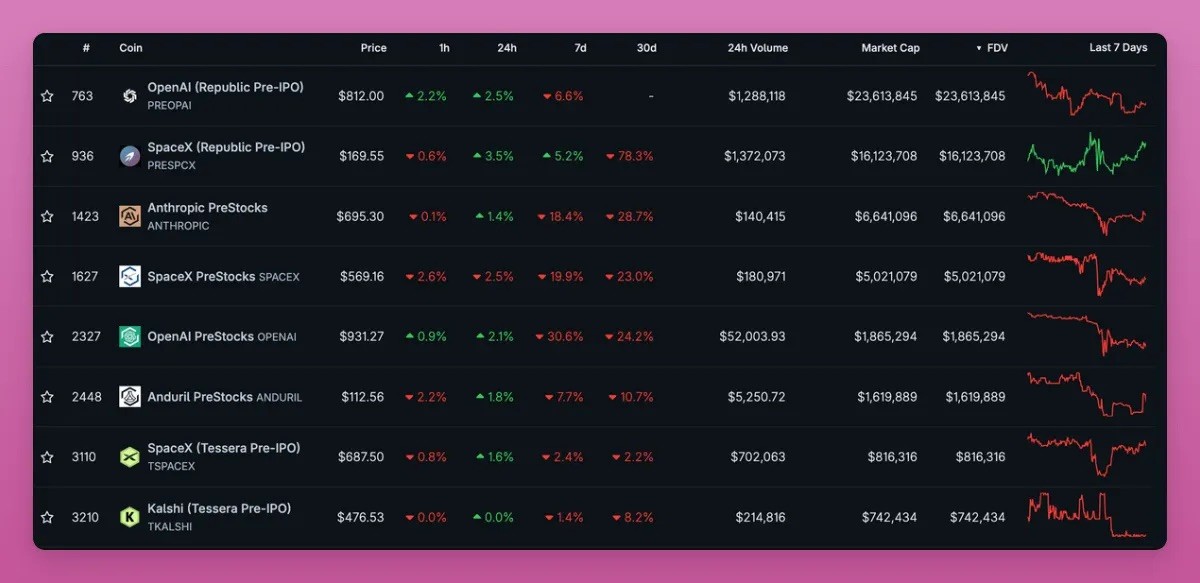

Some might say that pre-IPO tokenized stocks allow the common person to position themselves early in top-tier star companies like OpenAI and Anthropic. Indeed, by market capitalization, these two are the hottest primary market tokenization targets at the moment, but both companies are valued close to a trillion dollars.

This can hardly be considered early-stage investment: Anthropic's latest Series H strategic financing valuation has reached $965 billion. Financing rounds: Series A, Series B, Series C, Series D, Series E, Series F, Series G, Series H (latest round)

The Tokenization of Equity Race is Still in Its Early Stages

Standard Chartered Bank has set a target price of $100 for Uniswap's UNI token, with a potential upside of 40 times! The underlying logic is as follows: the bank predicts that by 2030, the size of tokenized assets circulating within decentralized finance will grow by 37 times (currently accounting for only 3.5% of total assets, rising to 30% by 2030); by 2028, the total on-chain tokenized asset size will exceed $40 trillion.

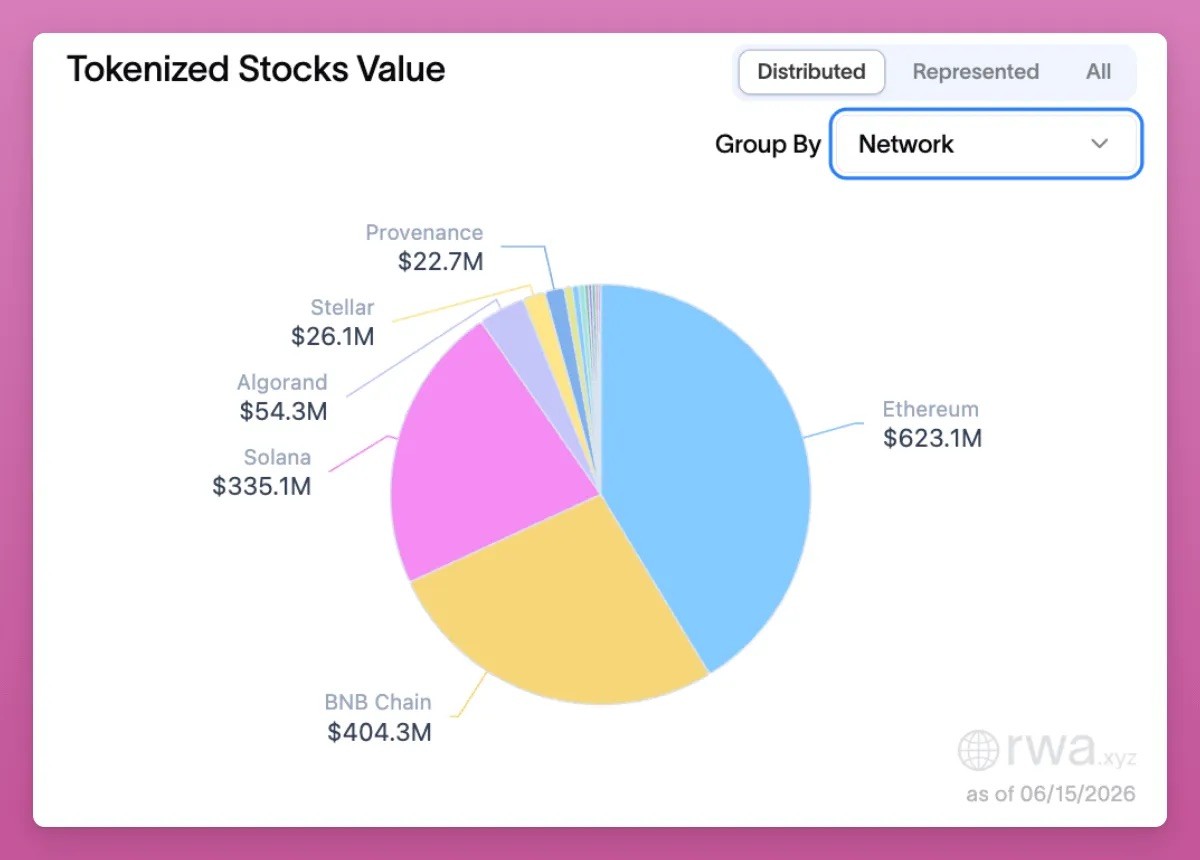

As of now, the total value of tokenized equity freely tradable across platforms is $1.5 billion (these assets can be transferred peer-to-peer between different wallets independent of the issuing platform), mainly deployed on Ethereum, BNB Smart Chain, and Solana. However, the overall size of the race is still small: $1.5 billion is even lower than Uniswap's UNI token market cap of $1.9 billion.

Standard Chartered Bank has always provided extremely optimistic price predictions (previously forecasting $40,000 for Ethereum and $500,000 for Bitcoin by 2030), but its bullish view on UNI is very coherent: the total value of locked tokenized equity continues to rise, driving on-chain transaction volume higher, platform fees increasing simultaneously, and now fees are used to buy back and burn UNI tokens.

It's not just Uniswap that benefits. Once the tokenized equity race sees an explosion, the entire crypto industry chain will profit: lending protocols like Aave, Fluid, Kamino, as well as decentralized exchange platforms on various public chains like Pancakeswap, Jupiter, all stand to gain.

The development of tokenized equity will give the crypto industry countercyclical properties: when Bitcoin and Ethereum prices are falling, decentralized lending will experience significant deleveraging, various protocol incomes will shrink, and platform tokens will be under pressure. Perpetual contract decentralized trading platforms are the first to benefit from the tokenized stock dividend, spot trading platforms will be the next wave of beneficiaries.

Following the Standard Chartered report, the UNI token saw a 13% daily increase, but there are still more investment opportunities in the race. Over the past two weeks, Backpack's platform token BP has surged by as much as 200%.

As a centralized exchange platform, Backpack has struggled to find a core business that truly meets market demand. It has had to compete with established top-tier exchanges like Binance while also vying with Hyperliquid, a decentralized perpetual contract platform, for users. The tokenization of assets seems to have finally helped it find a core growth path.

Most of the tokenized stocks on the market (such as xStocks and Ondo) follow a custody-wrapped model: the issuing institution holds the physical stocks, mints tokens that track the stock price, and users can only gain price appreciation without actual ownership rights.

However, Backpack achieves native on-chain issuance through Superstate's Opening Bell product line: these tokens are regular securities registered with the U.S. Securities and Exchange Commission, with rights identical to Nasdaq-listed stocks. Holders enjoy dividends and voting rights, and the platform holds a full set of regulatory licenses (Backpack's founding team comes from the original FTX European division).

This logic also extends to the platform's native token BP: by staking BP for a full year, holders can convert BP into corporate equity during an IPO or acquisition (with a 7-day unlocking redemption window each year).

There are still many direct trading opportunities in the tokenized equity race: by total float-adjusted market value, Ondo ranks second in the industry and has issued its native token ONDO.

However, ONDO only has governance functions and almost no value capture capability. All platform revenues go to the company and are not distributed to token holders.

Although the market is discussing the implementation of a fee-sharing mechanism, the actual execution remains uncertain. Additionally, there is significant token dilution pressure, with nearly 50% of the tokens still waiting to unlock by 2029.

If the sentiment in the tokenized equity market heats up, there may be a short-term trading opportunity for ONDO, but I would not hold it long term.

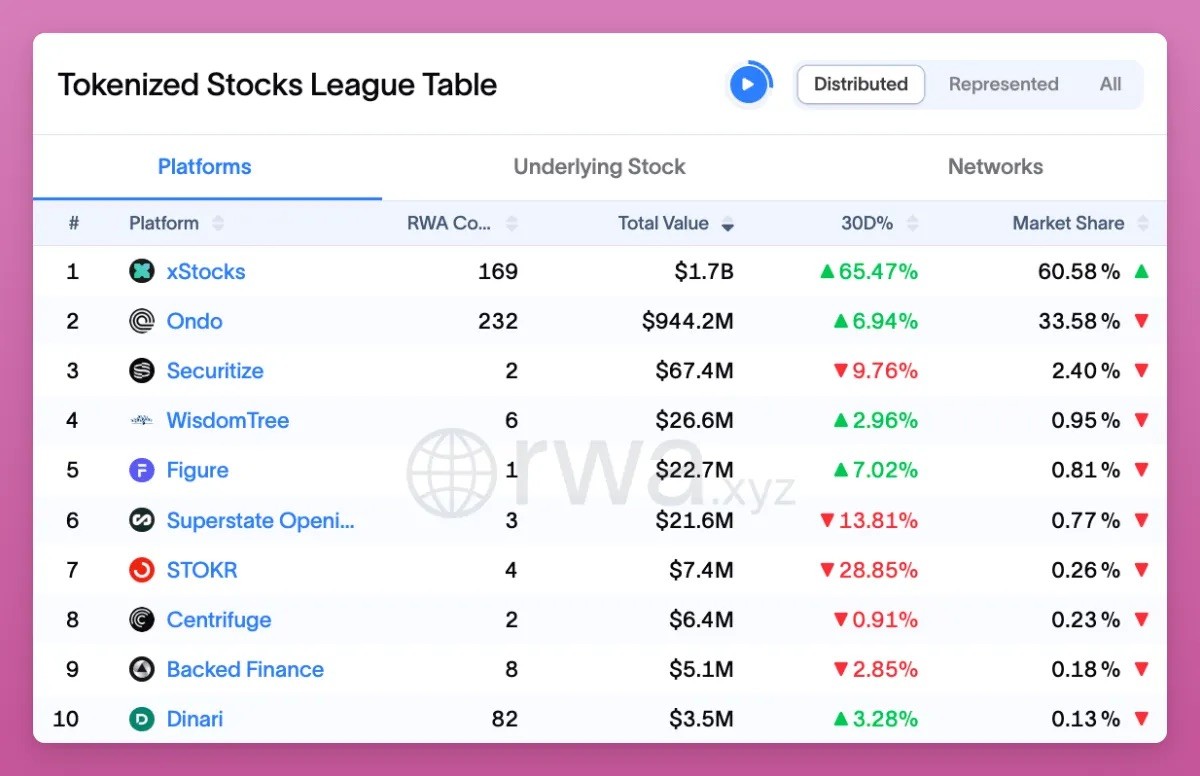

The industry leader xStocks holds a 60% market share, with a total size of approximately $1.7 billion. Backed Finance buys real stocks and ETFs, entrusts them to custodians in a 1:1 reserve ratio, and then mints tokens that track the assets' prices. The products are deployed on Solana, Ethereum (with a small amount on the Arbitrum layer two), allowing users to trade five days a week on the Kraken exchange platform or trade on-chain 24/7, covering about 60 underlying assets. The number of assets is fewer than Ondo, but the liquidity is better.

Owning xStock tokens does not equate to owning underlying equities, as it merely represents a claim on the issuing entity. In the event of platform risk, investors are merely unsecured creditors of a cross-jurisdictional custodial service provider, which is a stark contrast to Backpack's model of holding actual equity.

Ironically, Kraken, which acquired Backed Finance last year and recently filed for its own IPO with a valuation of $20 billion, has left the market questioning whether the platform will issue its own token.

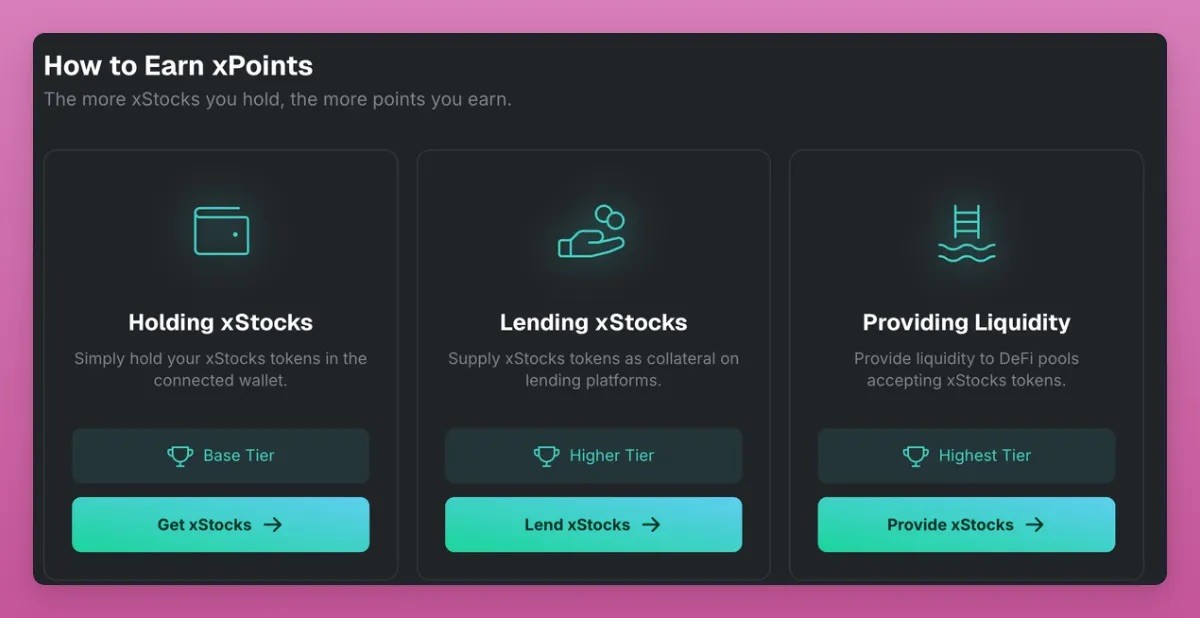

Following the acquisition, xStocks introduced the xPoints rewards program in March, typically a precursor to a token issuance, although the platform has yet to confirm the token launch.

xPoints Rewards Program Website

This situation is quite peculiar: If Kraken could sell its equity through traditional channels, why would it opt for a separate issuance of xStocks platform tokens?

A more plausible explanation for the rewards program launch is that Kraken has entered into a tokenized stock partnership with Nasdaq, where the platform requires trading volume and liquidity to support its operations and boost Kraken's overall performance metrics.

I do not wish to fall into the trap of blindly accepting hand-me-downs, but if you are willing to participate in points mining, here are the rules:

· Provide Liquidity: 7x Points (top tier, supporting Raydium, Orca, Byreal)

· Asset Borrowing: 5x Points (Kamino platform)

· Simply Holding Tokens: 1x Base Points

· Trading on Kraken's centralized exchange does not earn points; only on-chain operations accumulate points

The third-largest player in the industry is Securitize, and I do not intend to participate in its points mining activities. The company will go public via a SPAC merger with Cantor Equity Partners, with an estimated valuation of around $1.25 billion and BlackRock leading a $47 million funding round. The platform has no native token, and mining activities offer no returns.

As mentioned, there are various arbitrage opportunities within the industry: for instance, when the perpetual contract funding rate is negative, you can short on Hyperliquid (which also offers trade.xyz mining rewards), go long on Variational, and simultaneously buy spot tokens; or you can compare funding rates across major exchanges on the Ostium platform (which currently has no token).

If manually managing positions is too cumbersome, you can learn about the Nado platform: the platform is an order-book-based decentralized exchange that supports spot, margin, and perpetual contract trading with a unified margin account. The development team previously built Kraken and launched the INK product. The platform will support tokenized stock spot trading and perpetual contracts, enabling a delta-neutral strategy. It is an opportunity with relatively low visibility but worth participating in for mining rewards.

However, it is essential to remain cautious: the primary market token platform Ventuals has just announced its shutdown, informing users that all platform token values are reset to zero. Nowadays, participating in token airdrop mining requires more effort, significantly increasing the uncertainty of returns.

The Story is Far From Over

The term "crypto" now covers a wide range, including perpetual contracts, NFTs, prediction markets, meme coins, and other tracks. The RWA sector's volume is also continuously expanding, and each sub-track is worth a detailed analysis.

Stablecoins, money market funds, credit, private equity, and tokenized stocks belong to different sub-sectors, each with vastly different risk and return logics.

Tokenized stocks have a unique advantage in asset turnover efficiency: stocks inherently have price volatility, creating arbitrage and trading opportunities that do not exist in passive real-world assets.

I believe this will lead to a resurgence in trading-focused public chains, especially benefiting Solana (I see Ethereum as a storage public chain for high-value assets, more suitable for passive investments).

Previously, the Solana ecosystem was highly reliant on meme coins, and the new narrative of "everything can be traded on-chain" through tokenized stocks may drive a strong market for public chains. For example, the future trading volume of tokenized stocks may dominate Solana's on-chain total trading volume: low transaction fees, fast confirmation speeds, and a user experience superior to Ethereum-based public chains.

In the future, millions of ordinary retail investors may hold and trade tokenized stocks on their mobile phones, rather than just holding stablecoins. This will increase the revenue of the mainstream layer-one public chain ecosystem and subsequently raise the valuation of public chain tokens.

Overall, to truly achieve wealth growth through the tokenized stock track, the core idea is to bet on the widespread adoption of on-chain asset tokenization: in the next 1 year, 3 years, 5 years, which issuers and platforms will dominate the track? Which platforms will issue tokens and start airdrops? In fact, the investment opportunities are right in front of you: you can invest in UNI, BP, ONDO, or wait for Kraken's listing.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia