The Fed and BOJ Rate Hikes Looming: Will the Stock Market Decline This Week?

The key theme in the global markets this week was the Bank of Japan's rate hike and the Fed meeting. For risk assets, this week was destined to be anything but mild.

Just three months ago, Wall Street was still debating when to cut rates. When Powell took office, the market was willing to give the new chairman some leeway. With inflation trending down and the labor market loosening, a rate cut was only a matter of time. However, the financial world is fickle, and the originally envisioned script never played out.

In May, the CPI rose by 4.2% year-on-year and 0.5% month-on-month, with energy prices up 3.9% month-on-month. The core CPI is still around 2.9% year-on-year. Employment did not give the Fed an immediate reason to turn dovish, with 172,000 non-farm payrolls added in May and the unemployment rate holding at 4.3%. This means that the Fed is now facing a very awkward scenario: resurging inflation, stable employment, AI-related investments supporting economic resilience, weakening reasons for rate cuts, and accumulating conditions for rate hikes.

Meanwhile, the Bank of Japan held its policy meeting on June 15-16, with the market almost taking a 25 basis point rate hike as the baseline scenario. The Polymarket's "Bank of Japan Decision in June" market indicates a probability of around 98.3% for a 25bp rate hike, about 1.45% for no change, and around 0.55% for a rate hike of over 50bp.

Many may still remember that Japan's previous rate hikes have had a significant impact on the overall financial markets. This week, facing Japan's rate hike on Tuesday and the Fed's FOMC meeting on Thursday, will the market decline?

Powell's "Debut," Fed Rate Hike Probability Rises

Let's first look at the Fed's situation.

The possibility of a rate cut seems to have been nearly ruled out. On Polymarket, the probability of "No rate cut in 2026" is around 70.35%, "Rate cut before July" is about 2.35%, and "Rate cut before December" is only about 23%. Seventy percent of people bet that there will be no rate cut this year. Regarding the year-end rate range, around 37% expect the upper limit to stay at 3.75%, about 32.5% at 4.00%, around 11.25% at 4.25%, and 3.35% or above at 4.50%.

The market's assessment of Powell is generally consensually focused on his debut, meaning at this week's FOMC meeting, he is unlikely to raise rates. The risk of a rate hike is mainly concentrated after the third quarter. Several Polymarket markets can illustrate this consensus:

"Fed rate hike in 2026?" shows a probability of around 34.5% for any time rate hike in 2026; "Fed rate hike by...?" shows around 0.65% before June, about 6.15% before July, around 24.5% before September, and about 32% before October; in "Fed Decision in July," approximately 3.15% expect a 25bp rate hike in July, about 0.3% expect a rate hike of 50bp or more, and around 93.5% expect no change; in "What will the Fed rate be at the end of 2026?" the probability of the year-end rate hitting the upper limit of 3.75% is about 37%, around 32.5% at 4.00%, about 11.25% at 4.25%, and 3.35% or higher at 4.50%.

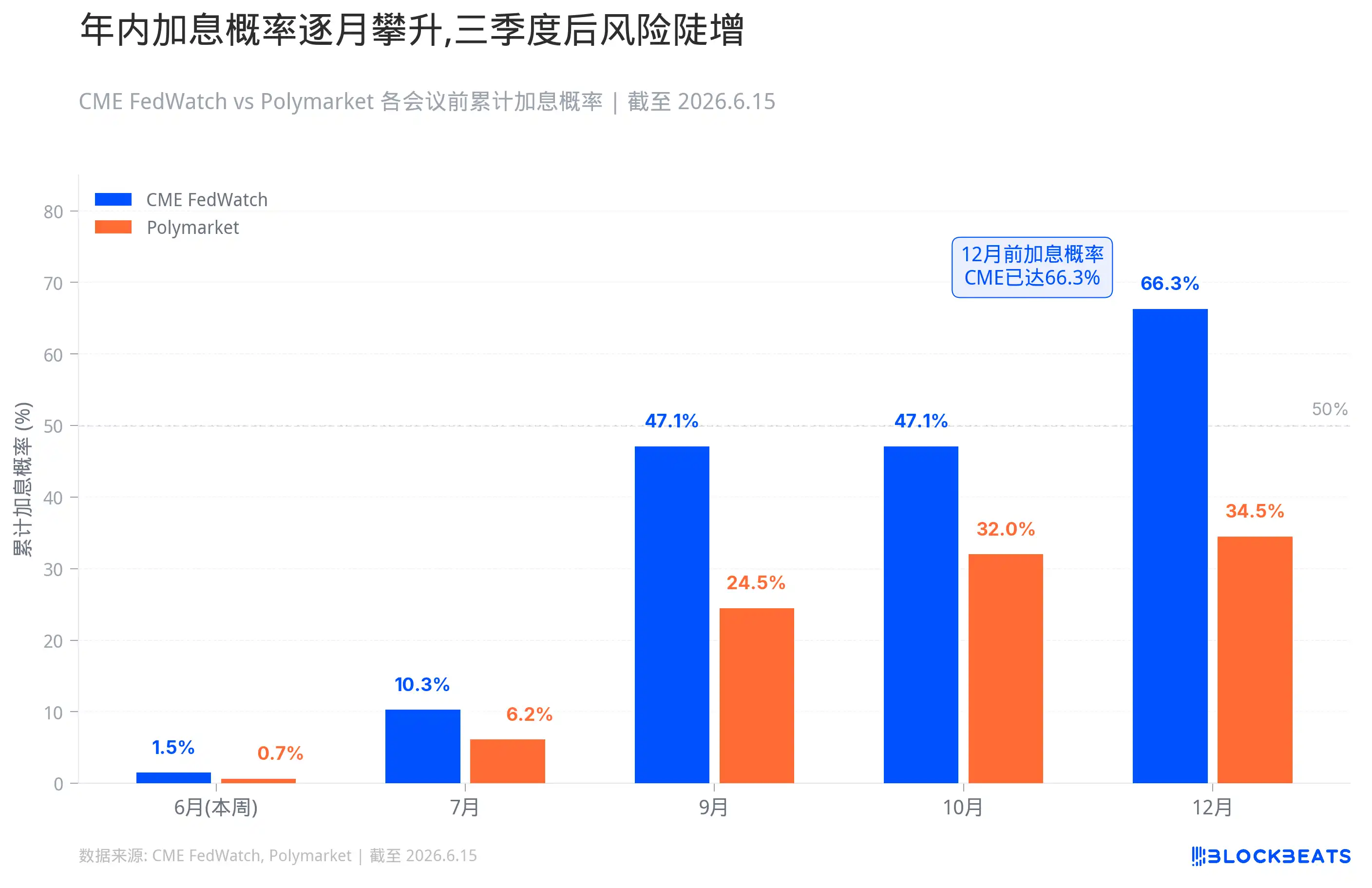

But for more specific probabilities and data. The probability of a rate hike before July 29 is about 10.3%, before October 28 about 47.1%, and before December 9 about 66.3%. Polymarket is more conservative, with "Fed rate hike in 2026?" at 34.5%, before September about 24.5%, and before October about 32%. As for this month's probabilities, CME FedWatch indicates a 98.5% chance of no change, while Polymarket indicates 99.55%.

This week in the U.S., it is highly probable to remain unchanged, but "remaining unchanged" and "not tightening" are two different things.

If Powell acknowledges at the press conference that inflation risks have overtaken growth concerns again, if the dot plot shifts the 2026 rate central tendency from a rate cut direction to staying flat or even raising, if the wording of a "rate cut bias" is removed from the statement, then the market will tighten on behalf of the Fed.

The first reaction will be in the U.S. bond short end. The 2-year and 1-year yields will directly follow the Fed's path. Once the market switches from "rate cuts later on" to "rate hikes later on," short-term yields will rise. The dollar will also be supported, as a strong dollar itself is a form of global tightening.

Within the U.S. stock market, high-valuation growth stocks and AI long-duration assets are the most sensitive. The higher the interest rates, the less valuable future cash flows, the more expensive the financing, and the market will be less willing to pay a premium for unrealized stories. The logic of small-cap stocks, micro-cap stocks, and unprofitable tech stocks is even more fragile as these companies thrive on cheap money, and once money is no longer cheap, valuations will be the first to collapse.

If a true tail scenario occurs, where 98.5% price in "no change" and the Fed directly hikes rates, the impact will be very severe. Short-term rates will spike, the dollar will surge, leveraged positions will be forced to de-risk. It is not certain to happen, but the implication of this probability is that if it does happen, no one will have time to react.

After all, Powell's "debut" is perceived as crucial by the market, and another very important factor is that he may change the Fed's communication. Reporters who have long tracked the Fed have made it clear: for Powell, symbolic adjustments such as the dot plot, statement wording, and news conference rhythm can be done quickly, but truly changing the Fed's communication system requires long-term persuasion and internal coordination. This week's meeting may be the first step.

Across the Pacific, Japan's "Curse" of a Rate Hike

Turning to Japan, the Bank of Japan will hold its policy meeting on June 15-16, with Polymarket indicating a 98.3% probability of a 25-basis-point rate hike. If implemented, the policy rate would rise from 0.75% to 1%, the highest since 1995.

The logic that has forced Japan to this point is very straightforward. The Middle East conflict has driven up oil prices, and Japan, as a typical energy-importing country, has seen its import costs amplified by a weak yen. Wages are rising, service prices are rising, and inflation expectations are beginning to loosen. If interest rates remain low, the market will question whether the Bank of Japan is really concerned about inflation.

The interest rate hike itself is not suspenseful, but a very important concern is this: over the past few years, a large amount of global funds have borrowed low-interest yen to exchange for dollars or other high-yield assets, buying US Treasuries, stocks, and credit, indirectly entering high-volatility risky assets. This structure is built on one premise: Japanese interest rates are low enough, yen financing is cheap enough, and the central bank is slow enough. In other words, if the market believes that the normalization of Japanese interest rates will be continuous, carry trades will become fragile, yen shorts will be squeezed, and global leveraged funds will begin to shrink.

The market's fear of a Japanese interest rate hike is not groundless. Over the past twenty-plus years, every time the Bank of Japan has tried to raise rates from near zero, the global market has almost always encountered issues.

The first time was in August 2000. The Bank of Japan raised rates from zero to 0.25%, which coincided with the peak of the US dot-com bubble. Within three months of the rate hike, the Nasdaq plummeted by 35%. Japan's economy itself could not withstand the pressure, quickly slipping back into recession, and the Bank of Japan had to lower rates back to zero in 2001.

The second time was from 2006 to 2007. The Bank of Japan raised rates to 0.5% in two steps, first in July 2006 and secondly in February 2007. The timeline almost perfectly matched the brewing period of the US subprime mortgage crisis. As the US subprime crisis began to unfold in the summer of 2007, leading to Lehman Brothers' collapse in 2008 and the global financial crisis, the Bank of Japan was once again forced to lower rates back to zero.

The third time was on July 31, 2024. The Bank of Japan raised rates from 0% to 0.25%, a small magnitude hike, but the market's reaction was extreme. On August 5, the Nikkei 225 plummeted by 12.4% in a single day, marking the largest drop since Black Monday in 1987. South Korea's KOSPI triggered a circuit breaker, while the Nasdaq and S&P 500 fell by 3.4% and 3%, respectively. The VIX panic index surged above 65. The transmission mechanism of that crash was clear: the rate hike by the Bank of Japan triggered a sharp rise in the yen, forced unwinding of carry trades borrowing yen to buy overseas assets, selling stocks to buy yen, and the collective sell-off led to a stampede. To cover margin calls, fund managers even sold off "safe-haven assets" like gold and BTC. Amid a liquidity crisis, the correlation of all assets approached 1. The editor still vividly remembers the market turmoil of that day.

Therefore, what is even more crucial is what kind of hint the Japanese government will give at tomorrow's press conference: how high will the interest rate ultimately rise to?

US Stocks, Treasuries, Bitcoin: Who Is the Riskiest This Week?

As mentioned earlier, during the past three tightening cycles by the Bank of Japan, the performance of the global market has mostly declined.

However, in fact, BOJ rate hikes themselves don't necessarily trigger a sell-off. Sell-offs usually occur when other vulnerabilities and leverage exist. For example, in 2000 and 2007, it collided with bigger bubbles in other countries. In August 2024, it caught the market off guard, as the market positioning was too heavy to react in time. But in the subsequent hikes, the market was prepared, and no accidents occurred.

This time, the 25 basis points have already been priced in at 98.3%, with little room for surprises. Based on the experiences in December 2024 and January 2025, the rate hike itself is likely to be smoothly digested. However, there are two additional variables this time.

Firstly, Governor Kuroda and BOJ Policy Board member Funo have been hospitalized for infectious hepatitis, and they are expected to be absent from this meeting and the post-meeting press conference. According to public reports, Deputy Governor Amamiya will act as the meeting's chair in the absence and Deputy Governor Nukaga will lead the post-meeting press conference. This arrangement is unlikely to change the direction of the rate hike. However, the market is not as familiar with Nukaga’s communication style as with Kuroda’s, amplifying the volatility of interpretation. A single phrase like "decisions will be data-dependent" versus "there is still room for rate normalization" may seem minor, but to traders, they are completely different signals.

Secondly, the Fed is also meeting the same week. The BOJ rate decision and the FOMC meeting are only one day apart. If the market reacts mildly after the BOJ rate hike, but Powell takes a hawkish tone the next day during the press conference, the dual pressure will intensify. Conversely, if the market is already nervous after the BOJ rate hike, and then Powell adds fuel to the fire, short-term sentiment may overreact. Having two central banks announce results back-to-back amplifies the volatility.

Let's analyze asset by asset:

US Treasuries are likely to be the first to react this week. The short end of the yield curve directly follows the Fed's path, with the 2-year and 1-year yields being the most sensitive. If Powell's press conference is hawkish and the dot plot shows upward revisions, short-term yields will rise, reflecting the market's repricing towards "delayed rate cuts" or even "rate hikes within the year." The long end is more complex; the 10-year yield may not surge in sync. If the market starts to worry that high rates will damage the economy, the yield curve may flatten further or even invert more. On the Japanese side, if Nukaga hints at further rate hikes, Japanese government bond yields will also be pushed higher. If Japan's $1.13 trillion US Treasury holdings show marginal loosening, it will in turn affect the supply and demand in the US Treasury market.

The US Dollar is likely to find support. A hawkish turn by the Fed will raise expectations for US asset yields, strengthening the DXY. While a BOJ rate hike theoretically favors the Japanese Yen and weakens the US Dollar, the actual direction depends on the tone: if the BOJ signals dovishness right after the hike, the Yen may fall instead of rise, and the Dollar Index may strengthen further. With both central banks meeting in the same week, the relative movements of the USD and JPY will be highly sensitive, and foreign exchange market volatility is likely to increase. Asian currencies and emerging market currencies will be under pressure, as a strong dollar itself is a form of global tightening that will drain offshore dollar liquidity.

The U.S. stock market will see significant differentiation. High-valuation growth stocks, AI long-duration assets, small-cap stocks, micro-cap stocks, and loss-making tech stocks will be the most vulnerable. As interest rates increase, future cash flows are less valuable when discounted, financing becomes more expensive, and the market is less willing to pay a premium for unrealized stories. The Russell 2000 and companies surviving on cheap money will be the hardest hit. Bank stocks' reaction will be more complex, with short-term interest spreads benefiting, but if the yield curve continues to invert and credit risk rises, it may not be a good thing. Defensive stocks will relatively resist the fall, but bond-like assets such as utilities and REITs will also face valuation pressure from higher interest rates. The S&P 500 closed near 7382 points last Friday, while the Nikkei 225 was at 66078 points. If the two central banks lean hawkish this week, both the U.S. and Japanese stock markets will be under pressure, especially indices with a high weighting in technology.

The situation in the Japanese stock market is somewhat unique. A rate hike by the Bank of Japan itself is bad news for Japanese export companies because a stronger yen will erode overseas profits. However, if the rate hike magnitude and pace are within expectations, Japanese stocks may not plummet, as seen in December 2024 and January 2025. The real risk lies in the post-meeting communication. If Governor Kuroda hints at further normalization, the Nikkei may see an initial drop followed by stabilization.

Gold will be pulled in two directions. Rising real interest rates and a stronger dollar usually weigh on gold prices. However, if the reasons behind the rate hike are energy shocks, geopolitical risks, and uncontrollable inflation, safe-haven demand will support the price of gold. Gold is likely to fluctuate near a high this week, with the direction depending on what the market fears more: rising interest rates or uncontrollable inflation. Oil's performance will be more dependent on supply and demand dynamics and geopolitical factors, with the ongoing Iran conflict. If the rate hike is due to oil price-driven inflation, oil may not immediately decline. However, if the market begins to trade on expectations of slowing demand, industrial metals and oil will come under pressure.

Corporate bonds and real estate are slow-moving variables, but the direction is clear. High-yield bond spreads will widen, financing costs will rise, and commercial real estate, REITs, and mortgage-sensitive assets will come under pressure. Emerging markets with a high percentage of dollar-denominated debt will also face more difficulties, as capital outflow pressures increase.

The cryptocurrency market will also face pressure in this macroeconomic backdrop. BTC is currently near $65,000, down from around $72,000 in early June. After the CPI announcement, it dropped all the way to around $61,500, only rebounding in the past few days. This price level is inherently unstable. On June 5, when it fell below $62,000, over $1.5 billion in long liquidations occurred on-chain, with Bitcoin spot ETFs seeing net outflows of $2.7 billion in a single week. Although the price has recovered somewhat, the market structure is not healthy. BTC has some macro-asset properties, so it may not necessarily collapse with rising interest rates, but it is also unlikely to strengthen independently. ETH, SOL, altcoins, meme coins, and low-cap coins are more fragile. These assets rely on liquidity overflow and risk appetite. Once the market starts to reevaluate the yield attractiveness of cash, short-term debt, and money market funds, high-beta assets will be the first to be cut. Contract market funding rates have fallen, on-chain risk appetite has cooled, as was seen in early June.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia