Profit Barely Grows, MLCC Leader Murata's Stock Price Doubles in a Year: Market Pricing in the "Next Year"

On May 28, Murata Manufacturing, the world's largest passive component manufacturer, saw a 12.36% single-day surge on the Tokyo Stock Exchange, hitting the daily limit up at one point and closing at 8,787 yen, setting a new all-time high after adjustment for stock splits. Two months ago, we dissected an article on Murata's 15-35% price hike for AI server MLCCs (multi-layer ceramic capacitors), discussing how this sub-millimeter capacitor disrupted the AI computing power supply chain. This time, what's worth dissecting is not the capacitor but Murata's stock itself.

Because if you look at Murata's recently released financial report, you'll find a contrast: the performance is actually quite flat, yet the stock price has doubled in a year.

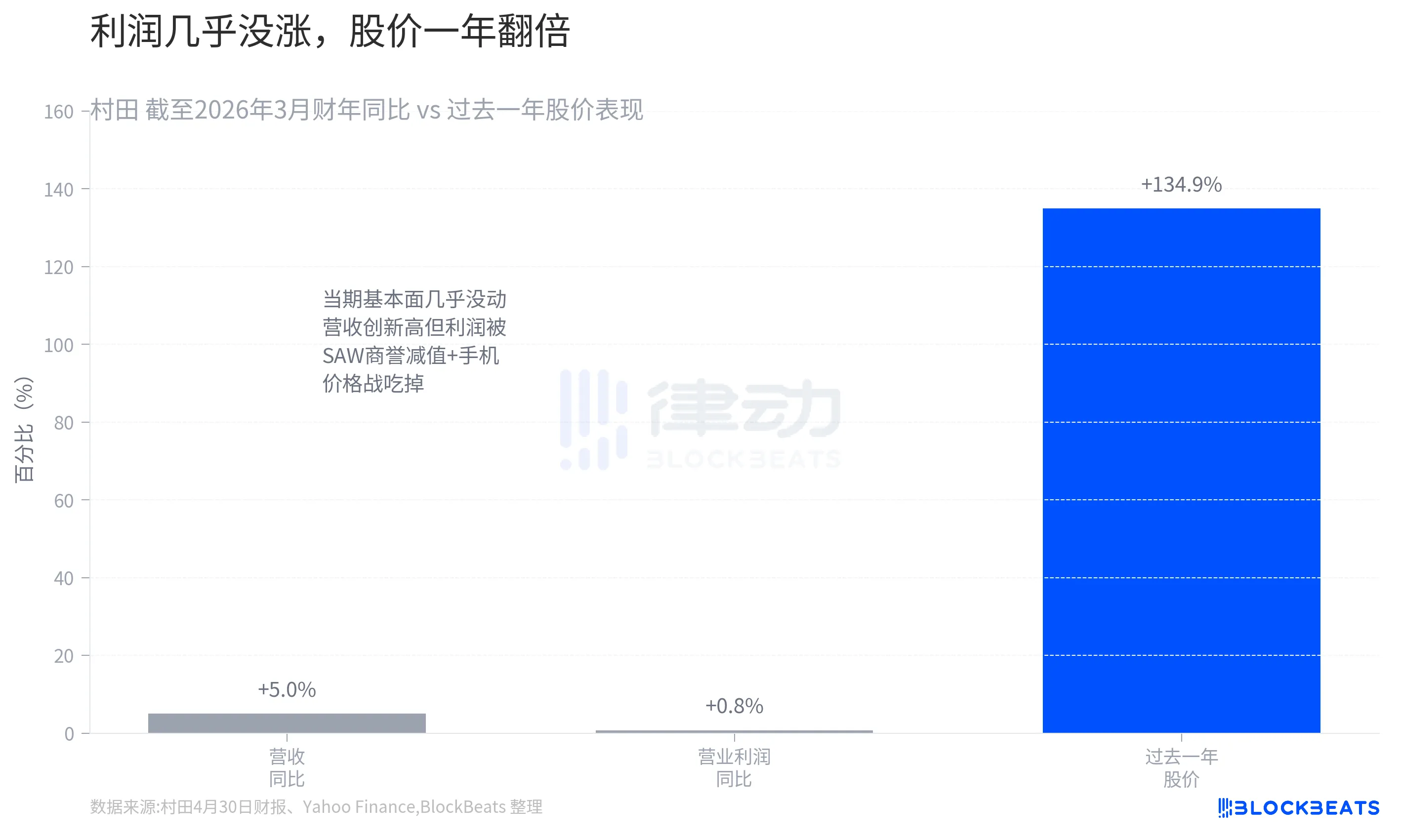

According to Murata's financial report as of April 30, in the fiscal year ending March 2026, the company achieved a record high revenue of 1.83 trillion yen, representing only a 5.0% year-on-year increase. Operating profit was 281.8 billion yen, up by a mere 0.8% year-on-year, almost stagnant. Two factors dragged down the profit: impairment of goodwill related to the Surface Acoustic Wave (SAW) filter business, and mature applications like smartphones engaging in price wars. In other words, the bright spot of AI only offset the bleeding of mature businesses.

However, during the same time frame, Murata's stock price has surged by approximately 134.9% over the past year (according to Yahoo Finance data), with the latest stock price surpassing 9,000 yen and the market capitalization reaching around 17 trillion yen, pushing the P/E ratio to about 75 times. For a company in passive components with zero profit growth, being priced by the market at a P/E ratio of 75 can only mean one thing: the buyers simply do not care about this year's profit; they are betting on the story ahead.

The Real Trigger Was an Analyst Meeting

The catalyst for this surge was not the price hike or the financial report but a small meeting Murata held with securities analysts on May 27.

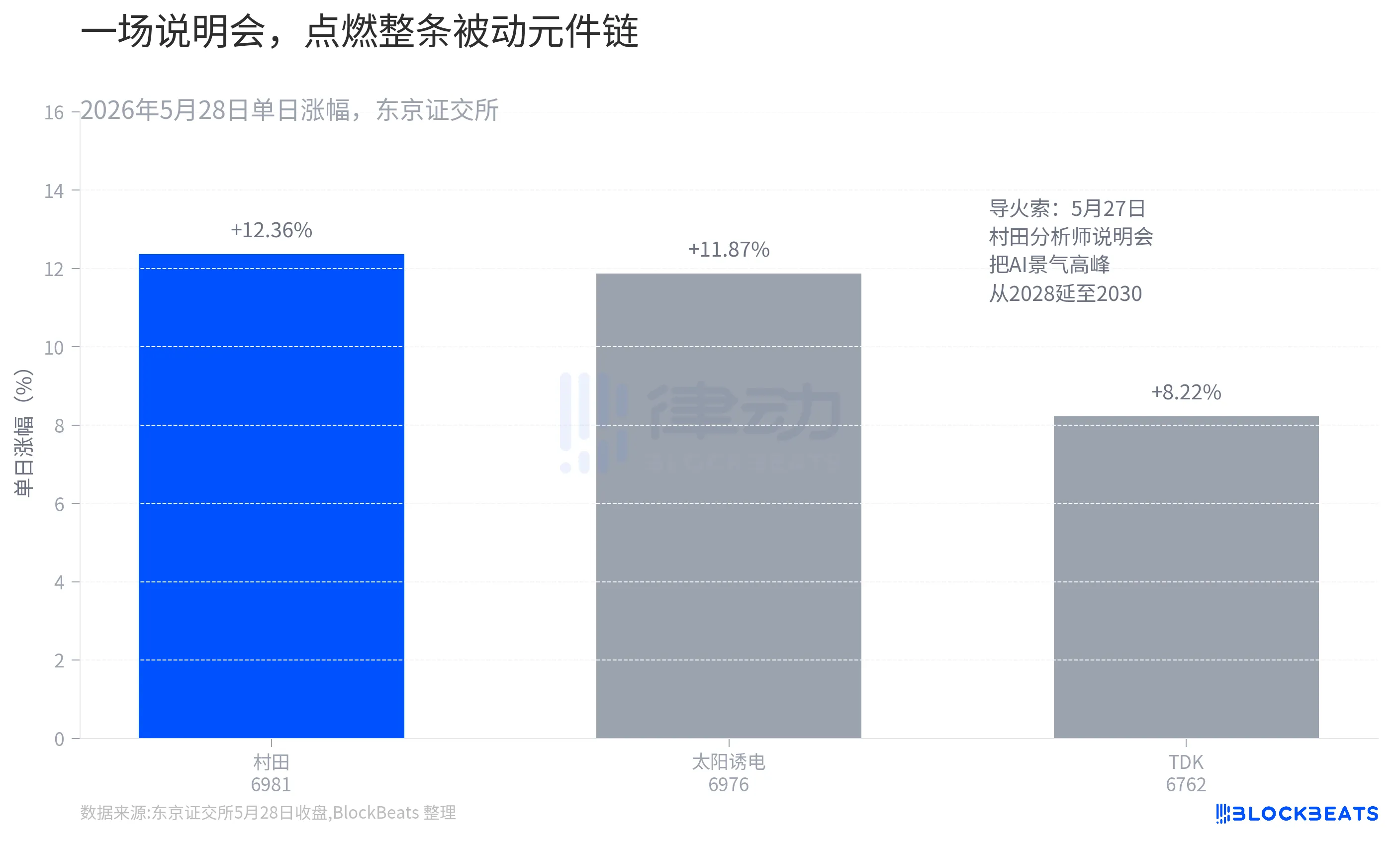

According to investment blogger kabuya66 citing the meeting content, Murata's management threw out two key sentences. The first sentence revised the expected peak of AI investments from "around 2028" to "expected to continue until around 2030." For a heavy asset, order-based component factory, extending the business cycle by two years means that order backlogs will continue to accumulate, making the return on expanded production investment more certain. The second sentence was more direct: customers now "guarantee volume, not price," with demand being about twice the capacity, implying that downstream customers are willing to buy regardless of price as long as they can secure the volume.

The impact of these two sentences could be seen in the market the next day. Murata surged by +12.36%, while its peers Sunwoda and TDK rose by 11.87% and 8.22%, respectively (according to the Tokyo Stock Exchange closing data). A flagship presentation reshaped not just a single stock but the entire passive component supply chain. The Nikkei 225 index also surpassed the 66,000 mark for the first time that day, with the MLCC sector being one of the main drivers.

What the market is buying is the "pillar" for next year

The reason why the presentation ignited the market is that it provided clarity on Murata's profit outlook for the next year.

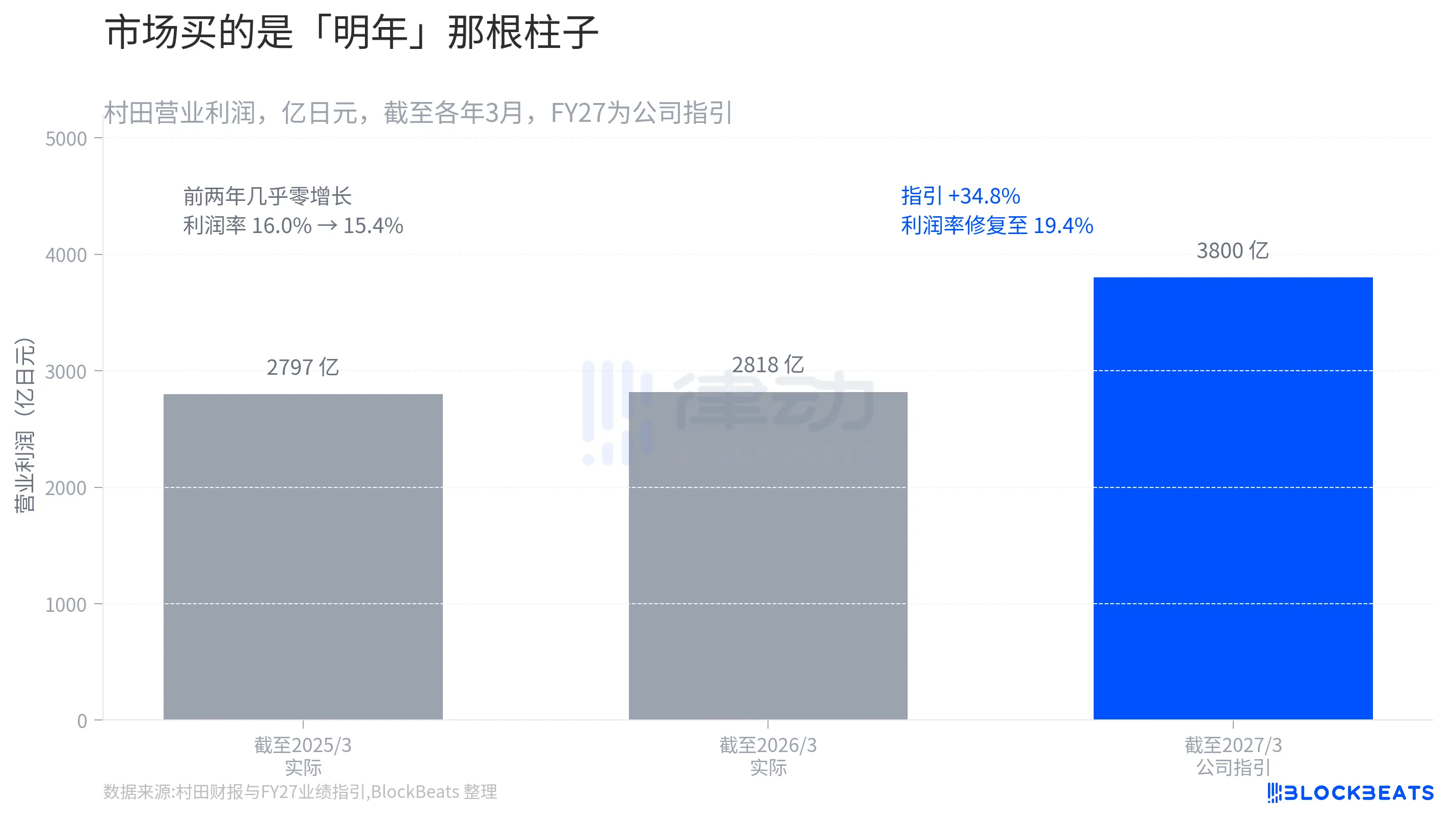

By visualizing Murata's operating profit as three pillars, the story became clear. For the fiscal year ending in March 2025, it was 279.7 billion yen, and for the year ending in March 2026, it was 281.8 billion yen, showing almost zero growth for two consecutive years, with the profit margin sliding from 16.0% to 15.4%. However, the guidance given by Murata for the current fiscal year (ending in March 2027) is an operating profit of 380.0 billion yen, a significant 34.8% year-on-year increase, bringing the profit margin back up to 19.4%.

All the growth is locked in that right-most pillar. What the market is currently buying is not the past two years of flat performance but this yet-to-be-realized guided pillar. A supporting factor is the order book, as per the Nikkei Veritas, among listed companies with a market value of over 50 billion yen and expected profitability for the current fiscal year, Murata ranked first in the growth rate of the previous fiscal year's order backlog. The order backlog directly translates to future revenue, providing the foundation for that guided pillar. Murata also announced a buyback plan with a cap of 150.0 billion yen, planning to repurchase 75.0 million shares, accounting for 4.12% of the issued shares. The management's commitment with real money is akin to acknowledging that the current price is not overly expensive.

What's supporting this pillar is AI revenue set to double again

Where does that 34.8% profit growth come from? The answer lies in one key area.

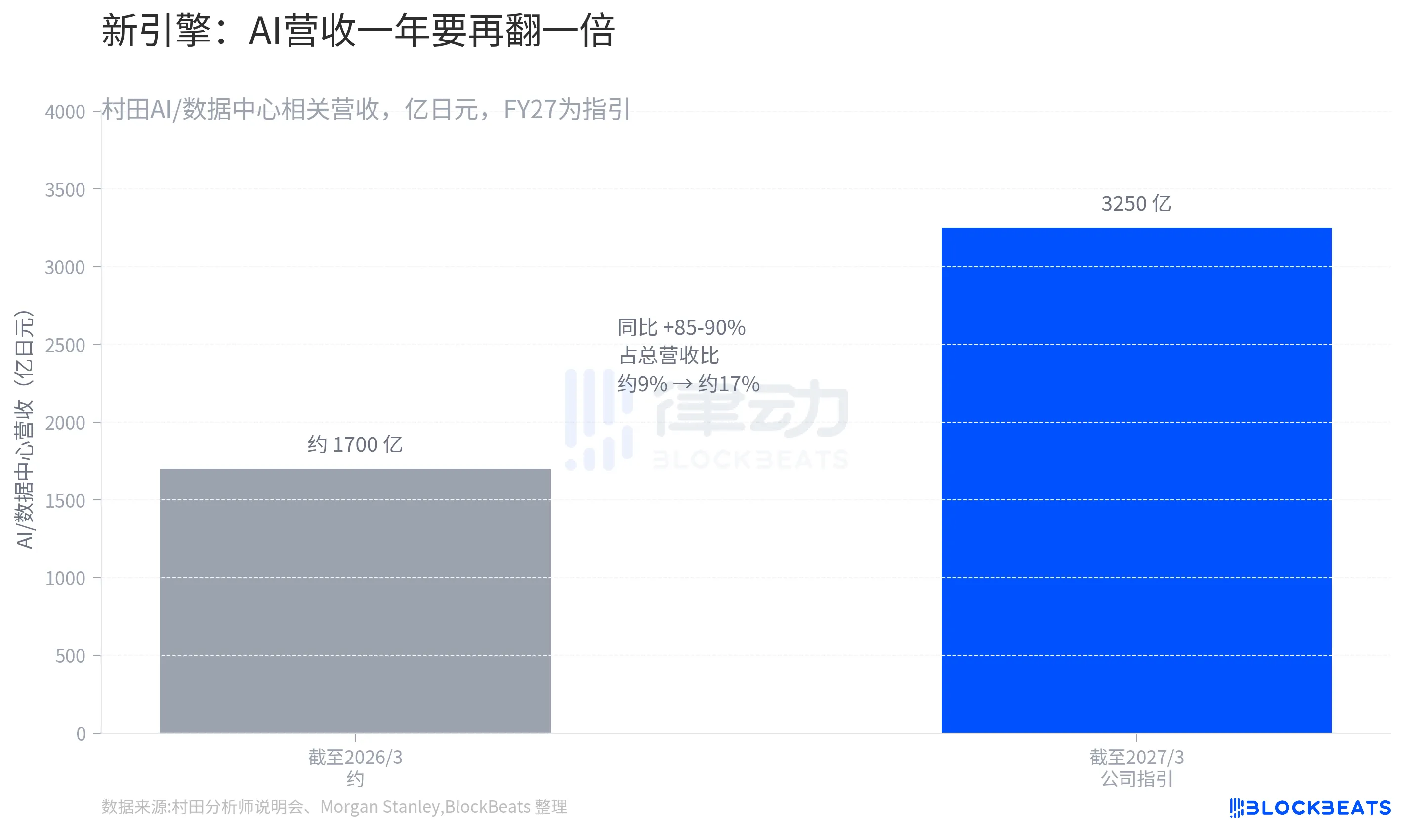

According to Murata's presentation data, the company's AI/data center-related revenue is set to jump from around 170.0 billion yen in the previous fiscal year to the guided 325.0 billion yen for the current fiscal year, an 85-90% year-on-year increase. The revenue contribution from this area will increase from approximately 9% to around 17% of the total revenue. In other words, within a year, AI's share of Murata's revenue, which was a fraction, will become close to one-fifth.

More importantly is the "quality" of this growth. According to analysis by Morgan Stanley MUFG Securities, Murata's recent AI revenue growth did not come from raising prices on existing MLCC products, but rather from product structure upgrades. The proportion of cutting-edge products with smaller sizes and higher capacitance has increased, pushing up the average selling price (ASP). Murata holds over 70% market share in the cutting-edge MLCCs required for AI servers, with hardly any competitors able to keep up. This means that its price increase is not due to cyclical "supply shortfall driving up prices," but rather to structural "I'm the only one who can do this so it's expensive." The market is willing to give it a P/E ratio of 75, pricing in this sustainable pricing power.

Of course, the flip side of expecting to reach a new historical high is that the expectations may have already run ahead. Murata's President, Norio Nakajima, has also acknowledged that there is a possibility that some customers' demand forecasts were "overly optimistic." If the pace of AI investments slows down or future quarterly guidance falls short of expectations, this high valuation also carries the risk of a rapid pullback. For high-valuation stocks, "not good enough" is the best reason to sell.

Murata is still the Murata that makes capacitors. What has changed is the yardstick the market is using to measure it: from a "cyclic component manufacturer doomed to price declines" to an AI shovel seller who is "supply-constrained and holds pricing power."

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia