Bankless Founder's Story: Why I Sold My ETH?

Original Article Title: ETH Is Money Was Always a Longshot

Original Article Author: David Hoffman, Co-founder of Bankless

Original Article Translation: DeepTech TechFlow

If you missed the news last week, "I sold all my Ethereum."

For someone who has built a career, community, identity, and business around Ethereum, making such a choice is no easy task.

The decision to sell requires a more thorough explanation than a few scattered tweets on Twitter.

It's best to read the full article on Bankless.com.

However, if you prefer the somewhat less aesthetically pleasing reading experience of a native X article, the article content is as follows.

tl;dr

The argument for "ETH Is Money" has not failed... it has merely been validated. Ethereum has reached its rightful price, and I do not believe that the value of ETH as an asset will be reevaluated, whether it goes up or down.

PS: I am very bullish on Ethereum. I expect the Ethereum network to thrive in the future. However, I believe that only a small part of Ethereum's success will be reflected in the Ethereum price (ETH).

Here is the content of the article:

ETH Being Money Has Always Been a Far-Fetched Dream

Money is a coordination game, and coordination is difficult.

The Ethereum project itself is a series of coordination challenges across multiple layers, and the idea that "ETH is money" requires all these layers to succeed and succeed confidently.

ETH can only become money when each layer of the Ethereum technological social stack outcompetes the competition.

Given the ambitious nature of the Ethereum project, achieving the most successful version of Ethereum has always been a monumental challenge. Despite its shortcomings, the Ethereum project has still achieved remarkable feats, and its current market value is well-deserved.

However, the window of opportunity... the hope of Ethereum being "revalued" by the market seems to be fading.

Ethereum is to some extent money. But it is not the kind of perfect money we all aspire to.

Ethereum is a Coordination Game

A Turing-complete blockchain is such a powerful concept that Ethereum's greatest potential lies in the entire cryptocurrency space, encompassing everything.

For Ethereum to achieve 100% dominance in all areas, the only barrier is coordination.

Ethereum's leadership needs to be decentralized enough, governance needs "rough consensus" to create trusted neutrality, thereby maximizing Ethereum's adoption.

Ethereum's leadership needs to be responsive to market dynamics and operate like a startup, constantly facing the existential threat of obsolescence.

Ethereum L2s need to be able to run independently of the base layer and make their own market choices, but they also need to be economically tied to and constrained by the broader Ethereum economy and brand.

The Ethereum roadmap needs to be executed in a specific order to maximize Ethereum's development momentum and market leadership, effectively suppressing competition and maximizing people's confidence in Ethereum and ETH.

To prove Ethereum's practicality to the world and maintain its leading position in the competition, key technologies need to be researched and developed at a fast enough pace.

The concept of "ETH is money" is to create a revolutionary and powerful financial asset, attracting previously indifferent people with its unique attributes as a superior global store of value. The strength of Ethereum's brand and ETH must be strong enough to make the baby boomer generation not only feel secure but also, due to Ethereum's project leadership, compel them to see ETH as a significant part of their retirement portfolio.

To achieve the goal of "ETH is money," all upstream components of Ethereum need to function at a high level.

Ethereum is not Bitcoin—it has chosen a difficult path. Bitcoin, on the other hand, has chosen to strip away all information on its blockchain to elevate its own status.

Ethereum has chosen to add all content to its blockchain to maximize its block space. Only by doing this in the best possible way before its competitors can Ethereum achieve global monetary status.

We have made some progress, and Ethereum has reached its rightful maximum potential market share.

Unfortunately, the prime time to play this game may have passed.

The Environment May Never Allow This

Looking back over these years, I see that Ethereum has had to overcome a significant number of environmental challenges.

The Inseparability of Layer-One Assets and Revenue

While it is challenging to assess a smart contract chain based on fees and revenue, fees and revenue are clearly a way for a smart contract L1 asset to increase its pricing power.

By 2026, we will have a wealth of data proving that all of these things are closely related: L1 activity, L1 fees, and the rise in L1 native asset prices.

· In 2021, ETH dominated, with its L1 revenue market share being the highest at that time.

· In 2024, SOL's L1 revenue market share saw unique growth compared to other parts of the industry, establishing its dominance.

· By 2026, NEAR will undergo a price reappraisal, and both L1 revenue and NEAR consumption will see fundamental growth.

You can also look at assets like BNB and TRX — perhaps the highest-earning projects in history. Their price charts resemble my expectations for ETH, assuming ETH can maintain its dominance in the L1 fee market for a longer period, not just in 2022.

The Imposition of a Strong Crypto Version Has Not Been Effective

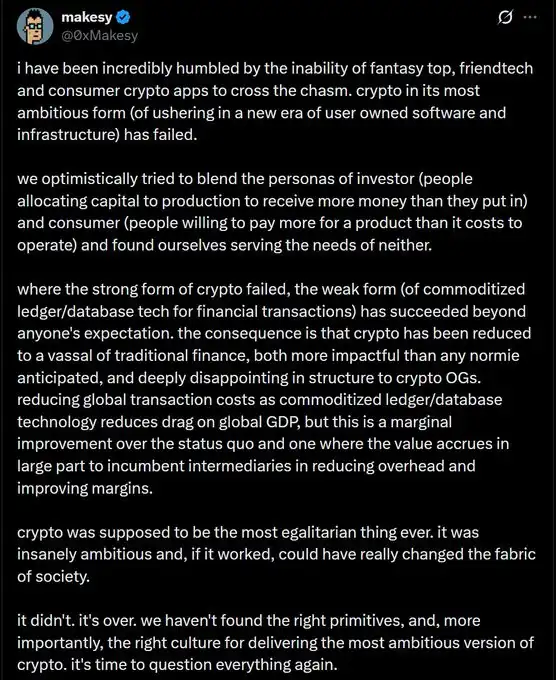

@0xMakesy said it best:

Ethereum represents a potent version of cryptocurrency — cryptocurrency itself is the goal, capable of self-sustenance and self-perpetuation. DeFi, NFTs, DAOs — we are rebels, committed to building an alternative financial system created by the people, for the people, turning imagination into currency.

There is also a weaker version: providing efficient ledger infrastructure for financial institution backends. This weaker version will empower the stronger version, channeling demand for internet ledgers inward — toward cryptocurrency, toward Ethereum, and ultimately toward ETH.

Perhaps, if Ethereum were more efficient, faster, and had stronger execution, if cryptocurrency hadn't attracted so many scammers and exploiters, this industry might have gained the influence and respect I have long believed it deserves. However, the period when cryptocurrency truly had a positive image in the public eye was limited to late 2020 through early 2022.

Furthermore, the reputation of cryptocurrency has always been associated with scams, fraud, get-rich-quick schemes, and its perceived uselessness to the average person.

ETH Relies on Being a "Strong Cryptocurrency"

Ethereum's moment as a global currency coincided perfectly with the moment when everyone was forced onto the internet. The world discovered cryptocurrency for the first time, and in that brief window, it had its moment.

Currency is a coordination game, where the value of a currency is upheld by people's belief. In 2021, there was a widespread belief in Ethereum (ETH): that it was cool, disruptive, and widely embraced. Bitcoin shared these qualities too, and post-2021, it has better maintained these qualities compared to Ethereum.

This leads to a troubling possibility: strong cryptocurrencies may never have reached a stable equilibrium. During the COVID-19 pandemic, the monetary system was unusually distorted, and Ethereum's position as a currency may have benefited from this distortion. If true, Ethereum's status as a currency has always relied on a strong cryptocurrency system performing better in theory than in practice.

Ethereum's utility has also contributed to the development of other currencies.

Is Bitcoin a currency? Is the US Dollar a currency? Is gold a currency? It doesn't matter—any currency will be tokenized on Ethereum.

In 2020, Nick Carter argued a case for "unbankedness."

Stablecoins are likely pegged to Ethereum rather than being native tokens of Ethereum. At that time, Ethereum's stablecoin supply was $3 billion. Today, the stablecoin supply has reached $163.0 billion, a 54x increase.

Ethereum's provided utility has helped expand the currency network to encompass all forms of currency, which is why the US is so bullish on cryptocurrency and applying it to stablecoins. Ethereum is helping the US maintain dollar hegemony, and leveraging this fact is a clear policy of the US government.

Positive spillover effects Ethereum's value as a currency is clearly dwarfed by what the US government sees in the Ethereum stablecoin ecosystem.

Ethereum is a Giver, Not a Taker

Ethereum's core is about giving, not taking.

It provides the world's most secure block space on Layer 2 at cost.

It tokenizes global assets at cost.

It secures billions of dollars in DeFi at cost.

All transactions on Ethereum do not incur any fees.

This is the nature of open-source software and the strength of Ethereum. Ethereum provides all its immensely important value to the world at cost.

Ethereum is noble. Ethereum is good.

Ethereum is the world's most successful nonprofit organization.

Ethereum will naturally achieve widespread adoption. It is currently, and potentially in the future, the most impactful open-source project in the history of mankind, with "nonprofit protocol" being one of its core features.

This is why Ethereum's path to becoming a currency depends on its continued high market dominance.

Ultimately, as block space becomes commoditized, fees will drop to zero. As long as it is Ethereum that drives block space commoditization and not a competitor, Ethereum can maintain its margin and dominance.

Ultimately, the fat protocol theory will be replaced by the fat application theory, with applications taking up the remaining profit space. As long as these applications are Ethereum applications and not competitors, this is fine for Ethereum.

The "ETH is money" argument and the "Ethereum is for givers, not takers" argument are difficult to reconcile. Ethereum's architectural design intention was to give back all resources to the ecosystem, taking only the minimal resources necessary to keep the network running.

Architecturally, Ethereum did not prioritize Ether (ETH), which is not a flaw but a feature. Ether will only become money when Ethereum wins the game it was not originally designed to play.

If Ethereum can maintain its astounding market dominance, this approach might work.

The argument that Ethereum is money has raised many questions about Ethereum.

The realization of "ETH is money" requires all of Ethereum's progress to go smoothly. The margin of error is much smaller than I initially anticipated. Ethereum's strong momentum in 2021 and 2022 makes "ETH is money" seem like an inevitable choice.

In hindsight, Solana's rise in 2021 and the increasing anti-Ethereum sentiment were the first significant signs that the coordination game between Ethereum and ETH was not going as planned.

The European Financial Group needs to decentralize and allow for the emergence of other power structures. But it also needs to respond to market forces with a sense of urgency and drive, as if facing the survival threat posed by disruptive startups.

The L2 team needs to have autonomy, but also operate within the larger Ethereum and ETH brand framework. Faster execution is needed for technical sync integration between Ethereum and its L2 teams.

The value proposition of a smart contract chain depends on transaction fees, and to break free from this model, Ethereum needs to rewrite the rules with a strong show of force.

The Ethereum Is Money Thesis Hasn't Failed

It just hasn't fully realized its potential.

Ethereum has made noble choices, opting for the most challenging, ambitious, and purest path for its future.

It has achieved some incredible victories but also faced challenges and setbacks.

Ethereum's market cap has reached its rightful level.

I am extremely bullish on the Ethereum network and its ecosystem—Ethereum's architecture is designed to maximize the success of its applications, L2 services, and ecosystem. The "fat app" thesis means Ethereum's applications will capture all fees, and the Rollup-centric roadmap means L2 services will capture 97% of the profits.

As for an asset like Ethereum, I find it hard to imagine a structural revaluation of Ethereum in any direction—be it upward or downward.

So, the reason I sold my ETH is not because I am bearish on ETH, but because I believe the "ETH is money" thesis is outdated, and I want to allocate my funds to other opportunities I see in the market.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia