FOMO into SpaceX Secondary Surges, Stunned in Greatest-Ever Wealth Creation Wave

A couple of days ago, The Wall Street Journal published a report featuring a little-known hedge fund named Darsana Capital.

This fund was established in 2014 and was relatively small. In 2019, it made a decision: to bet on a pre-IPO rocket company. That year, SpaceX was valued at around $300 billion.

Seven years later, as SpaceX prepares to go public, with a valuation of $1.75 trillion, Darsana's initial investment of about $600 million is now worth approximately $150 billion. This investment represents one of the most profitable hedge fund trades in Wall Street history. The SpaceX stake accounts for nearly 60% of Darsana's total assets.

SpaceX, in what is the largest IPO ever, also marks the beginning of this year's tech company IPO frenzy. Stories like Darsana's have been frequently reported recently. Google invested $900 million in 2015, and that sum is now worth over a trillion. The $200 million lifeline that Founders Fund extended in 2008 has now ballooned to $19.5 billion.

However, turning to some other reports, the tone changes completely.

At the end of March, both Bloomberg and Reuters reported a strange occurrence: a group of investors bought into SpaceX but could not confirm if they actually owned it. One of these investors, an entrepreneur named Tejpaul Bhatia, believed he held SpaceX stock but could not verify the authenticity of the shares supposedly belonging to him.

On one side, there is the myth of precise wealth creation in the billions, while on the other side are individuals who can't even determine if they made a purchase. The same company, the same IPO – why such a stark divide?

Private Secondary Markets Under "AI Anxiety"

In the past two to three years, AI has driven primary market valuations to absurd heights.

Companies like OpenAI, Anthropic, xAI, and SpaceX have valuations in the hundreds of billions or even trillions of dollars, and these numbers are rapidly increasing. Regular investors look at these figures and have one thought: I want in too.

The trouble is, there are more people trying to get in on the action now than ever before. The issue is that these companies are not yet public. For the average person looking to buy in before the IPO, there are hardly any avenues.

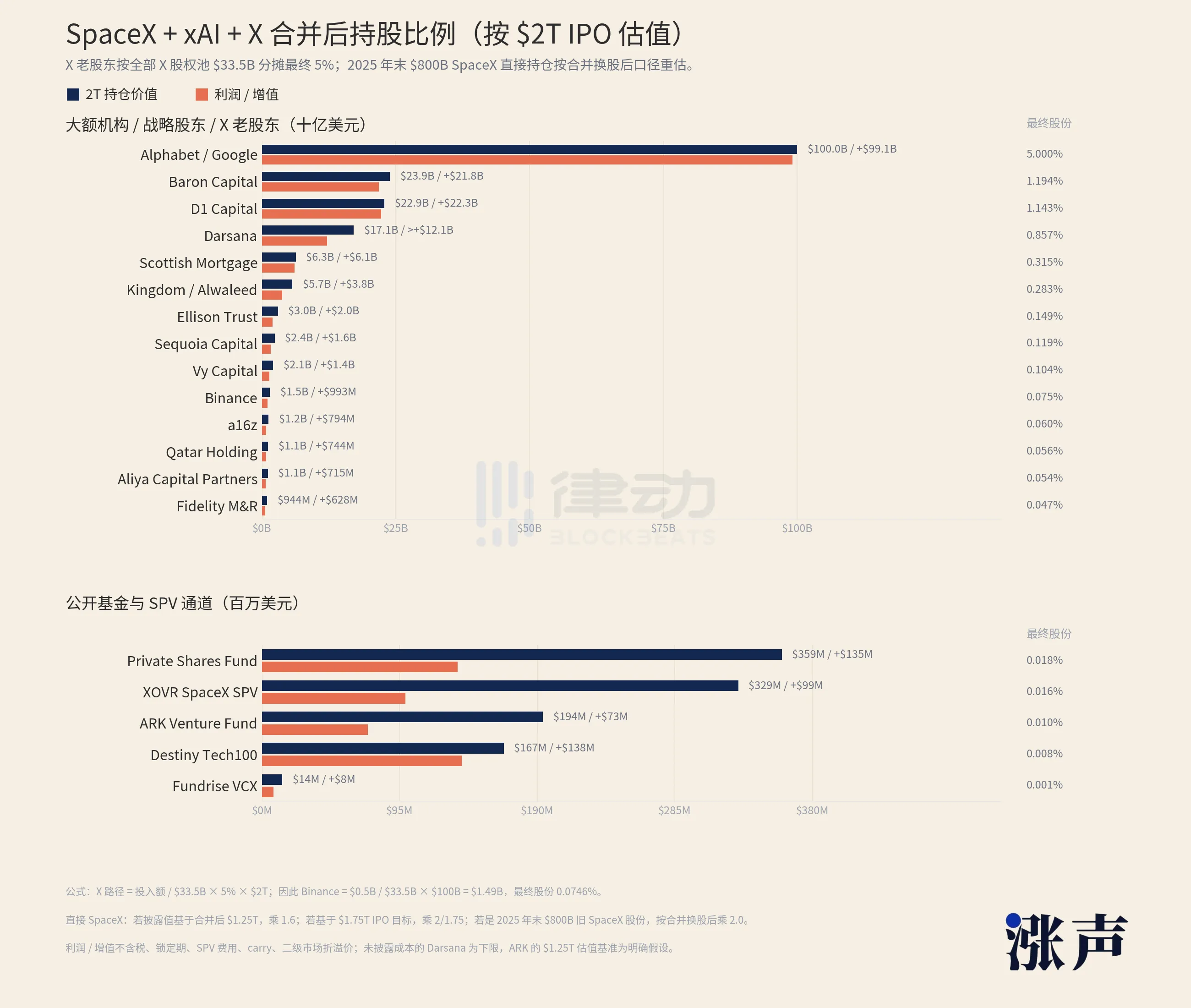

One only needs to look at the list of SpaceX shareholders. Large institutions and strategic investors hold positions worth tens of billions or even hundreds of billions of dollars, with Alphabet, Google's parent company, alone holding over a trillion. Whereas all the currently available public channels, combining several ETFs and funds holding SpaceX, have an exposure of approximately $10 billion.

With an estimated $2 trillion valuation, how much money can SpaceX's investment vehicles make?

Not to mention, most avenues still block out regular folks. The majority of private market channels are only open to accredited investors. In the U.S., this means an annual income exceeding $200,000 or assets of over $1 million excluding primary residence. Those who don't meet this threshold may not even fit into that $1 billion small opening.

For something else, this kind of disparity is enough to make people give up. But the logic of FOMO works in reverse. The scarcer it is, the more one sees others making money, the more they want to get in.

The money hasn't left. It has surged into a place called the private secondary market.

This market specifically trades shares of private companies. Early investors and employees want to cash out, those who missed out on early tickets want to get in, and the platforms, funds, and various vehicles that facilitate it all, make it up.

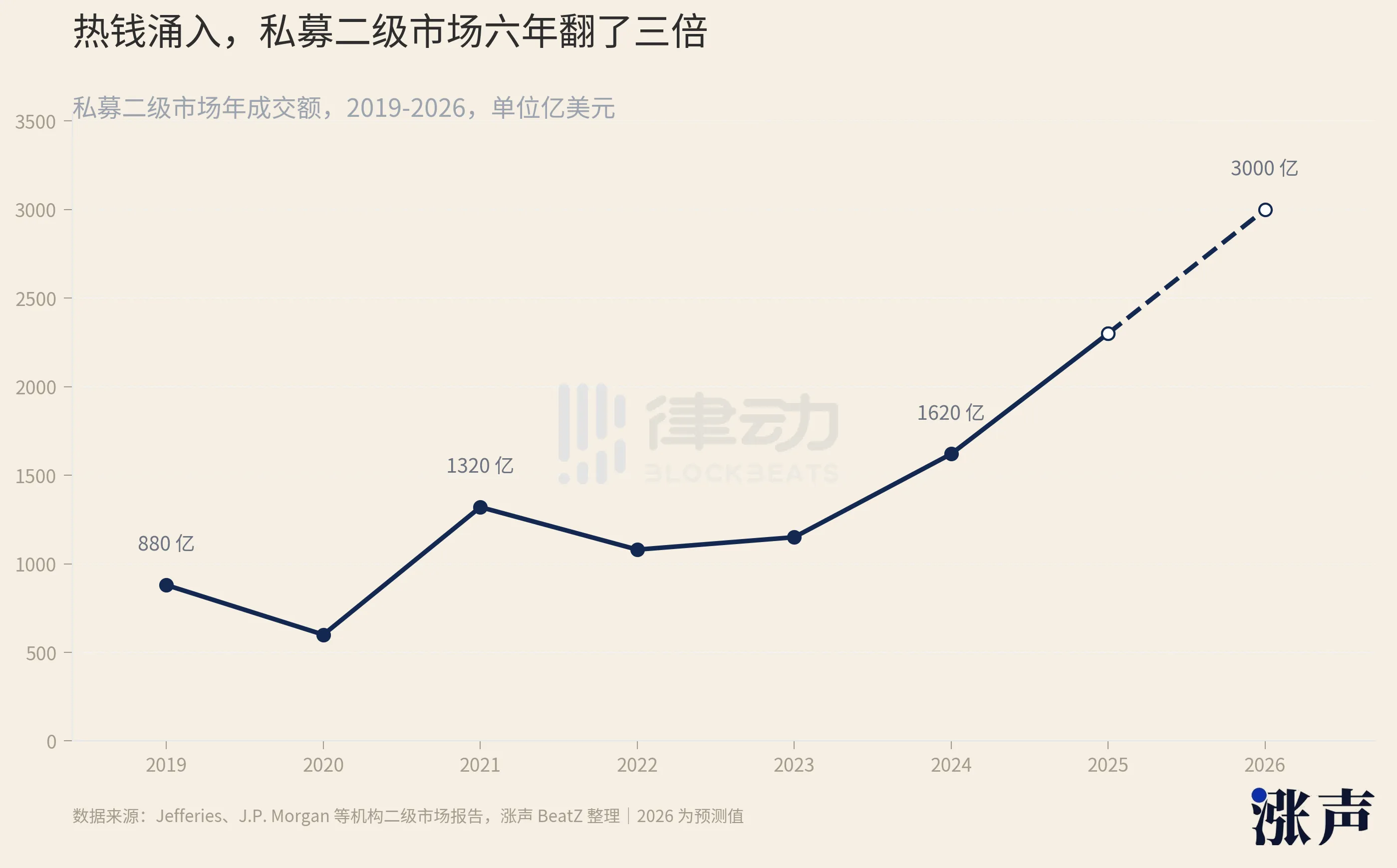

In recent years, it has expanded unbelievably. From 2019 to now, the scale has tripled. The full-year transaction volume is expected to reach about $162 billion in 2024, rising to around $230 billion in 2025, and is projected to touch $250 billion in 2026. The number of companies willing to offer shares for secondary transfers has increased from 12 to 31 within a year.

As money pours in, the sellers of SpaceX come out.

How many exactly are coming out? According to The New York Times, there are at least 170 special purpose vehicles (SPVs) that have bought into SpaceX. An SPV is a shell; whoever can get hold of some SpaceX shares, puts them in the shell, and then sells the shell's stake to subsequent investors. 170 shells revolving around the same company.

All these shells have some background.

In October 2025, an institution named Witz Ventures launched an SPV on the fundraising platform Republic called The Cashmere Fund, which packaged the three hottest targets, xAI, SpaceX, and Perplexity, together to be sold to retail investors. About 150 listeners of a financial podcast called Rich Habits, through a collective group purchase, also managed to get into SpaceX. Rapper 2 Chainz and SkyBridge founder Anthony Scaramucci have publicly stated that they hold SpaceX in their hands.

Retired NBA Player Tristan Thompson Claims to Have Invested in SpaceX When It Was Valued at $300 Billion on a TV Show

The problem is, among these opportunistic middlemen, not all are reliable.

One institution called Vika Ventures raised $5.9 million from investors, promising to buy SpaceX shares. It was later revealed that the founder of this institution used the money to buy luxury watches and a private jet. In 2023, another financial intermediary was sentenced to eight years for defrauding over 50 investors of nearly $6 million, also selling pre-IPO shares including SpaceX.

There was also a once-popular platform called Linqto, which focused on star-studded assets like SpaceX. It went bankrupt in 2025, and the U.S. Securities and Exchange Commission is investigating whether it diligently verified users' accredited investor status. Over 13,000 investors were affected.

Even if they didn't encounter scammers, things are still not necessarily clear.

DataPower Capital is an institution that deals in SpaceX shares. Its founder, David Yakobovitch, told The New York Times that he personally holds shares but only engages in transactions one level away from SpaceX. "As you go down several layers," he said, "things start to get murky."

Down to the Fifth Layer

Back to the 150 podcast listeners from Rich Habits. What they bought wasn't SpaceX.

They bought Witz Ventures, and Witz Ventures bought shares of DataPower Capital. DataPower is the one who directly receives stocks from SpaceX shareholders. This means that an ordinary person placing an order after listening to a podcast is separated by at least two to three layers of shells from actual SpaceX shares.

With each additional layer, two things happen simultaneously.

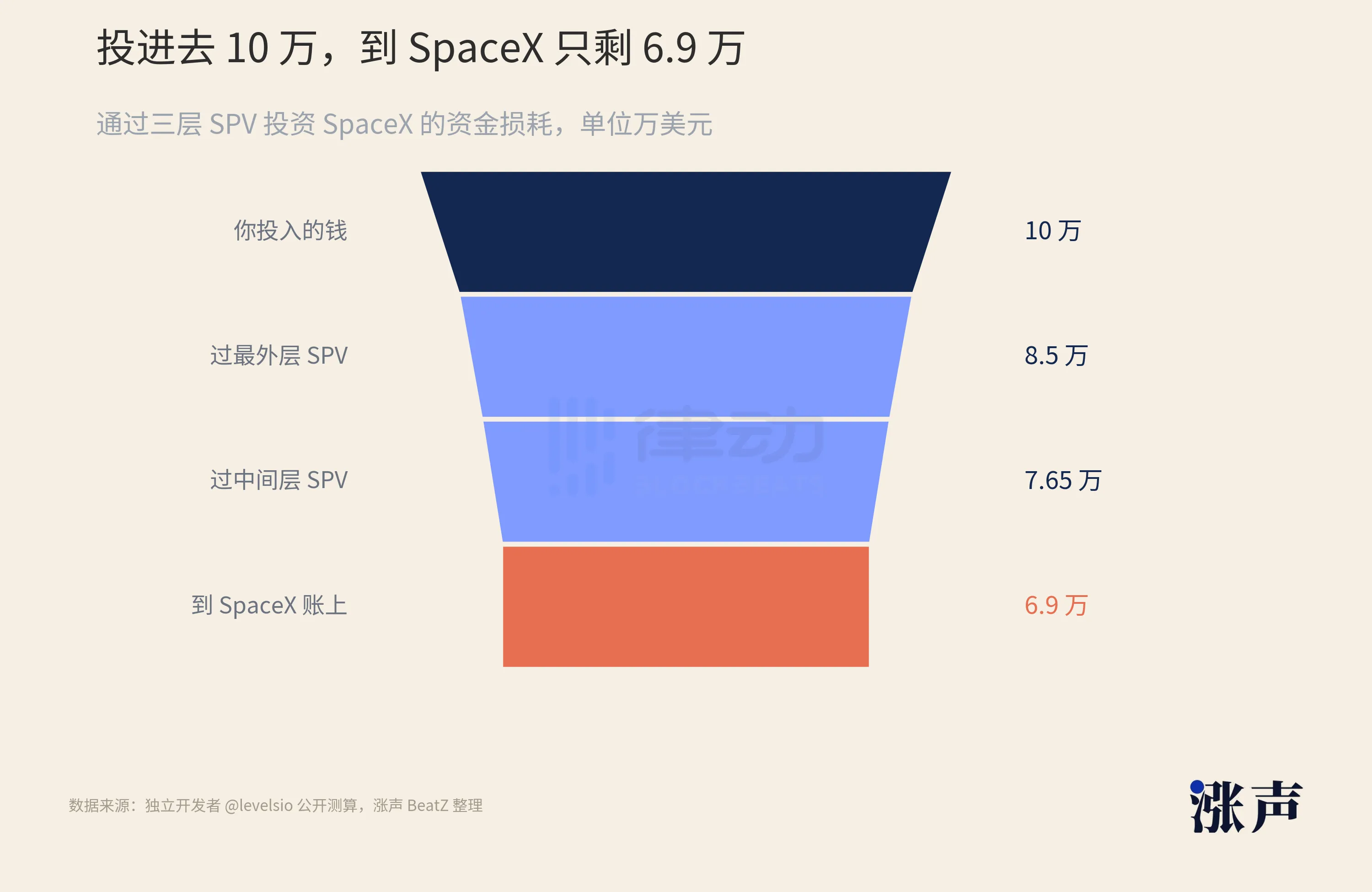

First, the money decreases. Independent developer levelsio did the math on social media: assuming you invest $100,000 in SpaceX through a three-layer SPV, the outermost layer takes a 6% setup fee, the inner two layers each take management fees and profit shares, and by the time the money reaches the core SpaceX layer, only about $69,000 is left. Before any earnings, thirty percent is already gone.

The second issue is the increasing distance from the truth. This kind of SPV structure has a fatal feature: at each layer, investors can only see the layer above them. When you buy the outermost shell, the shell's manager tells you it holds the shell of the next layer. Is the next layer real or fake? And does it actually hold SpaceX stock at the bottom? You can't see it, and you have no right to check.

There are 170 shells, nested to such a depth that there are even five layers. This is why the Bhatias cannot confirm their holdings. It's not that they are not careful enough, it's that this structure, by design, never intended to let outsiders see inside.

Why is SpaceX's nesting doll structure so deep?

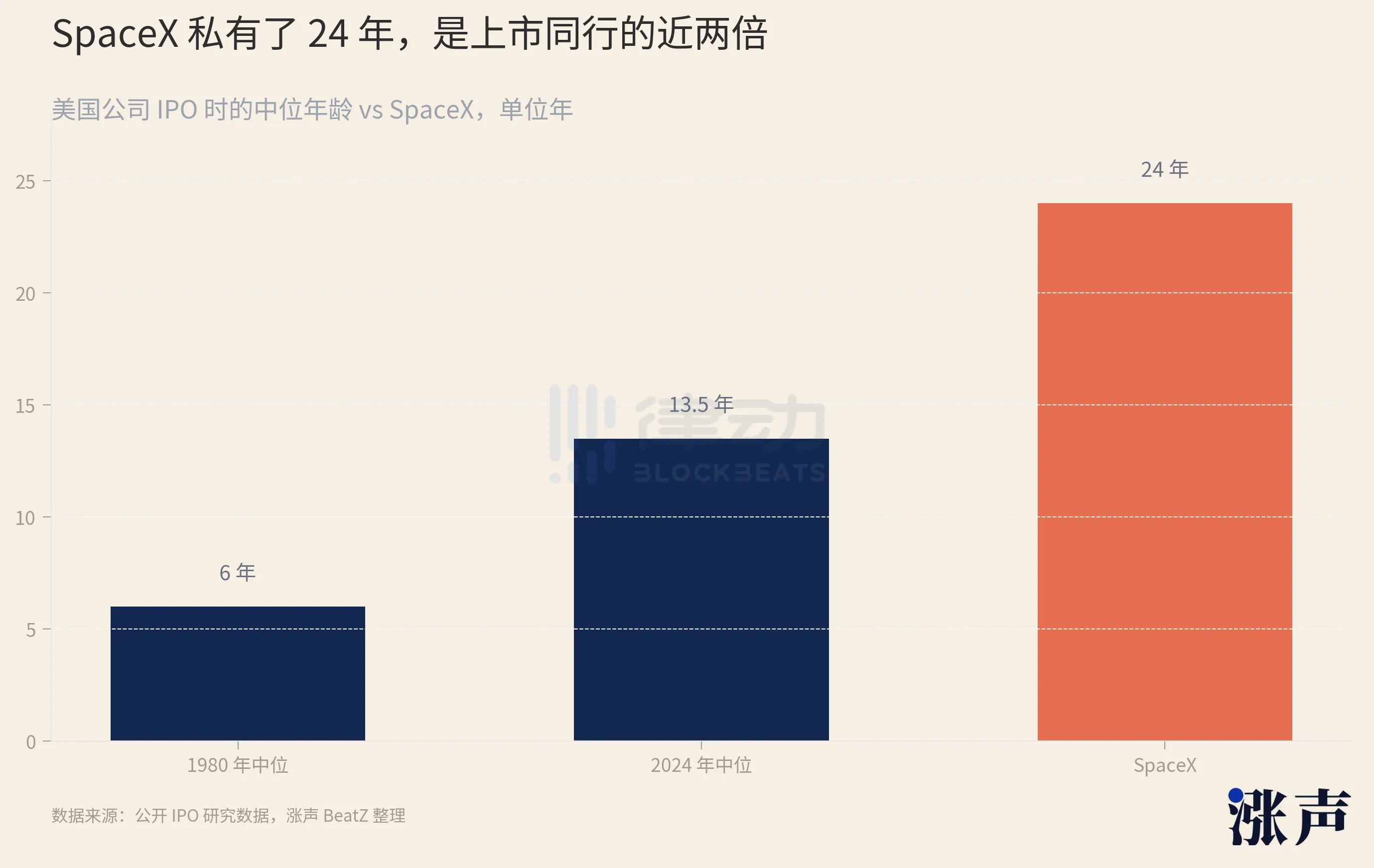

This depends on how long it stayed in the private placement market. It was founded in 2002 and didn't go public until 2026, remaining private for a full 24 years.

What does 24 years mean? The batch of tech companies that went public in 1999 had an average age of only 4 years. The 2014 batch averaged 11 years. In recent years, the median age of U.S. companies going public has been stretched to 14 years. SpaceX's 24 years, on this continuously lengthening curve, is extreme.

The longer a company stays in the private market, the longer its stock has been bought, sold, and nested in shells. SpaceX's shares have been circulating off-exchange for over twenty years, layered with one shell after another.

The lengthening of the private ownership period is not unique to SpaceX.

In recent years, the median age of U.S. companies at the time of their IPO has risen from 6 years in 1980 to 13.5 years by 2024. The reason is not complicated: there is just too much money in the private market.

By 2023, there was over $650 billion in uninvested global venture capital. With no shortage of funding, companies are naturally not in a rush to go public to face the pressure of public market financials and regulations. Therefore, the number of unicorns with valuations over a billion dollars continues to grow, with over 1500 such companies globally valued at $6 trillion, most of which have not raised money at a public valuation for over three years.

The longer companies stay in the private market, the longer the stocks held by employees and early investors remain locked up. For these people to cash out, the secondary market is the only exit. The demand accumulates there, and Special Purpose Vehicles (SPVs) specifically designed to accommodate this demand emerge in batches.

During the peak of venture capital enthusiasm in 2021, the United States saw a 235% year-on-year increase in the number of new SPVs established. By the third quarter of 2024, there were over 2,400 active SPVs. When a tool has been massively and repeatedly utilized for over two decades, stacking up to the fifth layer like a Matryoshka doll, the current situation becomes almost inevitable.

However, SpaceX happens to be the most restrictive company in the entire private placement market when it comes to managing its stocks. Externally, almost every share transfer triggers SpaceX's right of first refusal, allowing them to intercept the transaction. Every six months, SpaceX conducts a share buyback, absorbing any stocks that employees wish to sell into its controlled inventory.

The tighter the door is welded shut, the higher the price of admission outside.

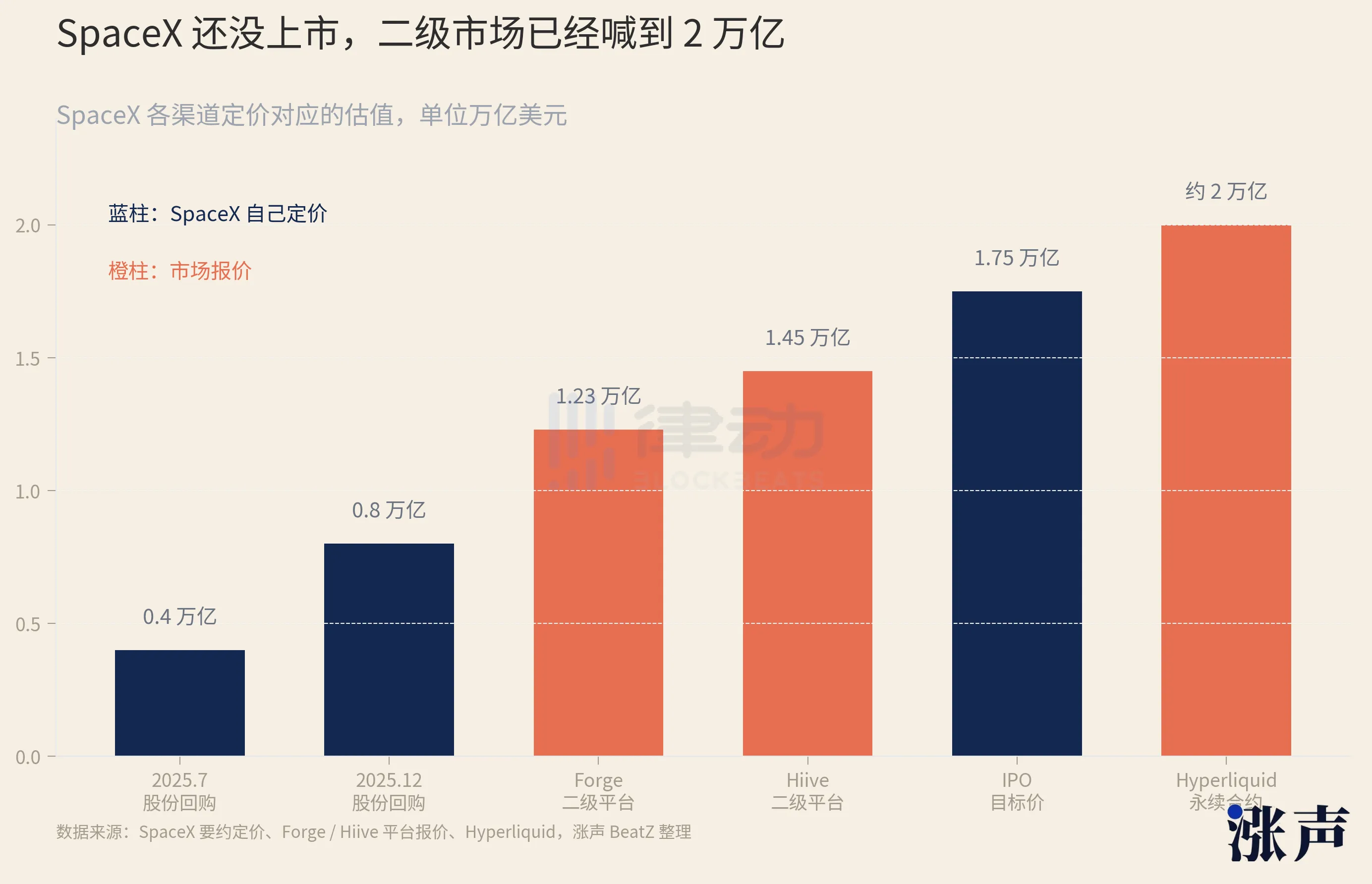

SpaceX has set its own prices: a share buyback in July 2025 was priced to correspond to a $400 billion valuation; by December of the same year, this valuation had doubled to $800 billion. However, the secondary market prices had already surged ahead. The Forge platform indicated around $1.23 trillion, Hiive at $1.45 trillion, and the contract listed on the crypto trading platform Hyperliquid even surpassed $2 trillion, exceeding the targeted IPO valuation set by SpaceX.

There is yet another tangled web formed through mergers. In March 2025, Musk merged X, the original Twitter, into his AI company xAI. In February 2026, SpaceX absorbed xAI entirely. Those who had previously purchased Twitter and xAI, along with the entire shell behind them, went through two rounds of stock swaps and all ended up on SpaceX's roster.

Open Mystery Box

With things reaching this level of complexity, even the companies themselves couldn't sit still.

In May 2026, both Anthropic and OpenAI publicly declared that any stock transfers conducted without board approval would be deemed invalid and not recorded in the company's books. They specifically named eight platforms, including Forge and Hiive, as unauthorized. Once this news broke, tokens associated with these unauthorized transfers in the on-chain secondary market, especially those focused on Pre-IPO trading, plummeted by thirty to forty percent in a single day.

Such announcements regarding secondary market trading were not made on a whim by one or two companies.

Recently, when robotics company Figure AI was reported to have a valuation of $39.5 billion, it also intervened in its own secondary share trading. The hottest targets in the private market, including Anthropic, SpaceX, Anduril, Stripe, and Databricks, are almost all doing the same thing: reducing the tolerance for secondary transactions to zero.

Why did they all turn against this practice?

This brings us to a usually overlooked threshold for going public. According to U.S. regulations, once a company's number of shareholders exceeds 2,000, even if it's not publicly traded, it must disclose financial information regularly like a public company. However, nested SPVs make it hard for companies to know exactly how many shareholders they have. An SPV may count as only one on the roster but could actually represent hundreds of individuals. Once a company unknowingly crosses this 2,000 shareholder threshold, it is compelled to open its books.

Another reason is the pricing of employee stock options. If a company's stock is freely traded in the secondary market at a high price, when the company sets the exercise price for employee options, it cannot ignore that number. The crazier the secondary market gets, the less valuable the options become for employees.

Even more critical is information. Shareholders have a legal right to access a company's operational details. For AI companies, details such as model architecture, training data, and computing resources are the most sensitive secrets that cannot leak out. When a company cannot even accurately count its shareholders, it cannot explain where this information might be flowing.

Purging the ambiguous shareholders, safeguarding the pricing of options, and sealing off the information leaks are not novel tasks on their own. However, as the secondary market swelled to $230 billion, with nested SPVs reaching five layers deep, companies found that they could no longer manage everything privately. Consequently, they stepped into the spotlight and, for the first time, publicly announced that "your shares are invalid." SpaceX did not follow up with a similar statement. Nevertheless, its preemptive purchase rights were essentially achieving the same goal.

With this statement from the company, those multi-layered shells were left hanging in midair. You bought into an SPV, paid the money. However, until the company publicly reconciles its accounts, no one can tell you whether the underlying batch of SpaceX shares has been approved, counted, or even exists.

Therefore, buying into a SpaceX SPV is becoming more like opening a mystery box.

When the box will be opened is predetermined. On June 12th, when SpaceX rings the bell at NASDAQ and submits its IPO filing, for the first time, there will be a public, verifiable shareholder roster. Every shell that has been wrapped around its stock for the past couple of decades will have to be brought out for reconciliation at that moment. If it matches, there are real stocks in the box; if it doesn't, it's just a worthless piece of paper. On that day, Bhatia will finally find out which one he has drawn.

But after SpaceX, there is OpenAI, there is Anthropic, and there is a long list of names waiting in line. Just scroll through your Moments and you will see the "promotional posts" of these hottest AI companies.

The hot money generated by AI in recent years is so abundant that it has nowhere to go. There are only a few assets worth buying, and they are all locked up tightly. With too much money and a narrow entrance, numerous shells have emerged in between.

As long as this imbalance persists, the private placement secondary market will remain in its current state: a blind box that everyone wants to play with, but no one can clearly explain what they have actually received.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia