A Decade of Regulation Clarity Finally Culminates in Victory for Crypto-Native Principles

BTC, ETH, SOL, XRP, DOGE, SHIB.

These names were written together in an SEC regulatory filing for the first time, with a few words added after them: not securities.

On the evening of March 17, 2026, the SEC and CFTC jointly released a 68-page interpretive document, formally providing a systematic qualitative assessment of the security attributes of crypto assets. This marked the first time at the U.S. federal level that specific tokens were officially named and classified in a regulatory interpretation. The document also replaced the SEC's previous 2019 "Investment Contract Analysis Framework," which had been a key reference point for industry compliance assessments.

There is a clear timeline for the issuance of this document.

In January 2025, SEC Acting Chair Mark T. Uyeda established the Crypto Task Force to specifically clarify the application boundaries of securities law to crypto assets. In July of the same year, the President's Working Group on Digital Assets released a report recommending that the SEC and CFTC use existing powers to provide regulatory clarity to the industry.

SEC Chair Paul S. Atkins subsequently launched Project Crypto, which was upgraded to a joint SEC-CFTC project in January 2026. During this period, the Crypto Task Force received over 300 public comments from issuers, investors, law firms, auditing firms, and various other stakeholders.

In other words, this document represents a "unified answer" from the two federal regulatory agencies after over a year of industry maneuvering and policy coordination.

Five Lines Draw the Entire Map

In this document, the SEC categorizes crypto assets into five classes. The core criterion for judgment is based on the four elements of the Howey Test.

The first class is "Digital Commodities." This is the most notable part of the entire document as the SEC provides a specific list of names. BTC, ETH, SOL, XRP, ADA, AVAX, DOGE, SHIB, LINK, DOT, LTC, BCH, HBAR, XLM, XTZ, APT, a total of 16 tokens are explicitly included in the text. The footnote also mentions that Algorand (ALGO) and LBRY Credits (LBC) fall under this category.

The logic provided by the SEC is: the value of these tokens is inherently tied to the programmable operation of the functional cryptographic system they reside in, primarily driven by supply and demand, rather than by the expectation of profit from the managerial efforts of others.

The second category is "Digital Collectibles." CryptoPunks, Chromie Squiggles, WIF (dogwifhat), and VCOIN are specifically mentioned. Meme coins find their place here, as the SEC views their value as being primarily driven by "artistic, entertainment, social, or cultural significance," similar to physical collectibles, and therefore not deemed securities.

The third category is "Digital Tools." Examples include ENS domains and CoinDesk's Microcosms NFT tickets. The defining feature of these assets is their ability to perform specific functions, such as membership credentials, identity markers, or ownership certificates, many of which are non-transferable by soul-binding.

The fourth category is "Stablecoins." According to the passed GENIUS Act, "payment-type stablecoins" issued by compliant issuers are expressly excluded from the definition of securities. However, the SEC retains jurisdiction over stablecoins that do not meet the standards set by this Act.

The fifth category is "Digital Securities." This is the only category definitively classified as securities. However, the SEC does not mention any specific tokens as belonging to this category in the document.

The boundaries between these five categories are not absolute. The SEC itself acknowledges the existence of hybrid assets that blend categories and crypto assets that do not fall into any category. However, the significance of this classification framework lies in its shift of the "what is a security, what is not" debate from the courtroom to the regulatory enforcement level.

Four On-Chain Behaviors, Unified Qualification

Beyond token classification, another significant contribution of this document is the unified qualification of four core on-chain behaviors: mining, staking, wrapping, and airdrops.

Protocol Mining does not constitute a securities offering. Whether solo mining or joining a mining pool, mining is considered a network maintenance activity, where the newly minted tokens represent a protocol-level programmed reward, free from any investment contract relationships.

Protocol Staking does not constitute a securities offering. This determination covers four scenarios: solo staking, self-custody with key delegation, third-party staking with custody, and liquidity staking. The SEC makes it clear in the document that staking rewards stem from the protocol's pre-set programmatic allocation, rather than the managerial efforts of a specific team. Regarding liquidity staking tokens (LSTs such as stETH), the SEC deems them merely as "receipts" for the underlying staked assets, not categorized as derivatives and not considered securities.

Asset Wrapping does not constitute a securities offering. Wrapping BTC as WBTC for use on Ethereum is merely a technical interoperability operation that does not change the underlying asset's nature.

Airdrops do not constitute a securities offering. As long as recipients do not provide funds, goods, or services in exchange, the free distribution of tokens does not meet the "investment of money" element in the Howey Test.

These rulings have a direct impact on the industry, where the core mechanisms of DeFi protocols, such as staking, wrapping, and airdrops, have all been removed from the scope of securities law. Over the past three years, every project offering staking services or conducting airdrops has been concerned about this issue, and now there is a unified answer from federal regulators.

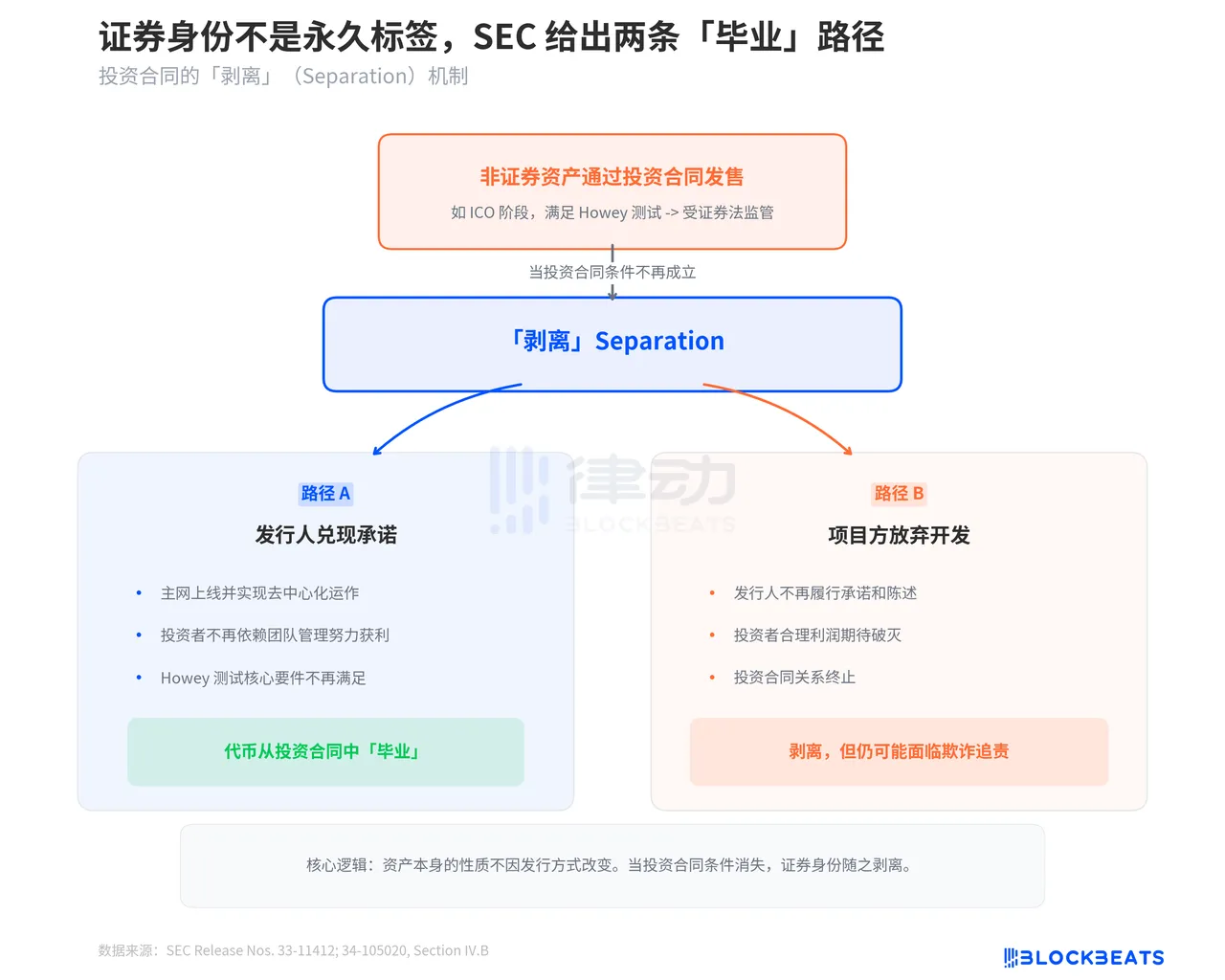

Security Status Is Not a Permanent Label

Perhaps the most important part of this document is the SEC's explanation of the "Separation" mechanism. The document clearly states that a crypto asset that is not itself a security can be brought under securities regulation due to its method of issuance (e.g., through an investment contract). However, when the conditions of the investment contract are no longer met, this asset can be "separated" from its security status.

The SEC provides two scenarios for separation. The first is when the issuer fulfills their promises. For example, if a project promised to develop a decentralized network during an ICO and the network actually goes live and operates in a decentralized manner, investors no longer need to rely on the efforts of the issuing team to profit. The core element of the Howey Test is no longer met, and the token "graduates" from the investment contract.

The second scenario is more interesting, where the project team "abandons" the project. If the issuer fails to fulfill the promises and representations made in the investment contract, and investors' reasonable expectations of profit through the efforts of others are dashed, the investment contract is likewise terminated. However, the SEC emphasizes that this does not mean the issuer can escape liability, as they may still face fraud charges.

The true significance of this "separation" mechanism is that it provides a compliant path for crypto projects. From ICO to mainnet launch to full decentralization, it is no longer an adventure in legal gray areas but a regulatory tunnel with a clear endpoint. Once you go through it, you're out.

Page 68. Nine chapters. 18 tokens mentioned by name, 6 categorized on-chain behaviors, 2 "graduation" paths. The SEC spent over a year collecting 300+ comment letters, ultimately collaborating with the CFTC to produce this report. It's not perfect; the boundaries of stablecoins still have gray areas, no specific examples were given under the "digital security" category, and there is room for interpretation in judging hybrid assets.

But for an agency that has been criticized in the past for regulating by enforcement

, this document at least did one thing: It put the rules down on paper instead of in a complaint.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia