Glassnode: The $100K Defense Battle resumes - Will Bitcoin Rebound or Continue to Dip?

Original Article Title: Defending $100k

Original Article Authors: Chris Beamish, CryptoVizArt, Antoine Colpaert, Glassnode

Original Article Translation: Luffy, Foresight News

Abstract

· Bitcoin broke below the short-term holder cost basis (approximately $112.5k), confirming weakened demand and officially marking the end of the previous bull market phase. The current price is consolidating around $100k, down approximately 21% from its all-time high (ATH).

· About 71% of the Bitcoin supply is still in a profitable state, aligning with characteristics of a mid-term correction. The 3.1% relative unrealized loss rate indicates a mild bear market phase at present, rather than a deep capitulation.

· Since July, the supply of Bitcoin held by long-term holders has decreased by 300k coins, indicating that despite the price drop, selling pressure continues — a pattern different from the early stages of this cycle's "sell the rallies" approach.

· The U.S. Bitcoin spot ETF has seen persistent outflows (daily outflows ranging from $150M to $700M), and the Cumulative Volume Delta (CVD) of major exchanges reveals sustained selling pressure, indicating reduced organic trading demand.

· The directional open interest premium in the perpetual contract market has decreased from a monthly average of $338M in April to $118M, suggesting traders are unwinding leveraged long positions.

· Demand for put options with a $100k strike price remains strong, with increasing premiums, showing traders are still hedging risk rather than buying the dip. Short-term implied volatility remains sensitive to price swings, but has stabilized since the spike in October.

· Overall, the market is in a fragile equilibrium state: weak demand, manageable losses, and a strong sense of caution. To achieve a sustained rebound, there is a need to reattract inflows and reclaim the $112k - $113k range.

On-Chain Insights

Following the release of last week's report, Bitcoin, after several failed attempts to reclaim the short-term holder cost basis, broke below the psychological level of $100k. This breakdown confirmed weakening demand momentum, persistent selling pressure from long-term investors, and marked the market's clear departure from the bull phase.

This article will assess market structural weakness through on-chain pricing models and expenditure-based indicators, and then combine spot, perpetual contract, and options market data to gauge market sentiment and risk positioning for the upcoming week.

Test the Support Below

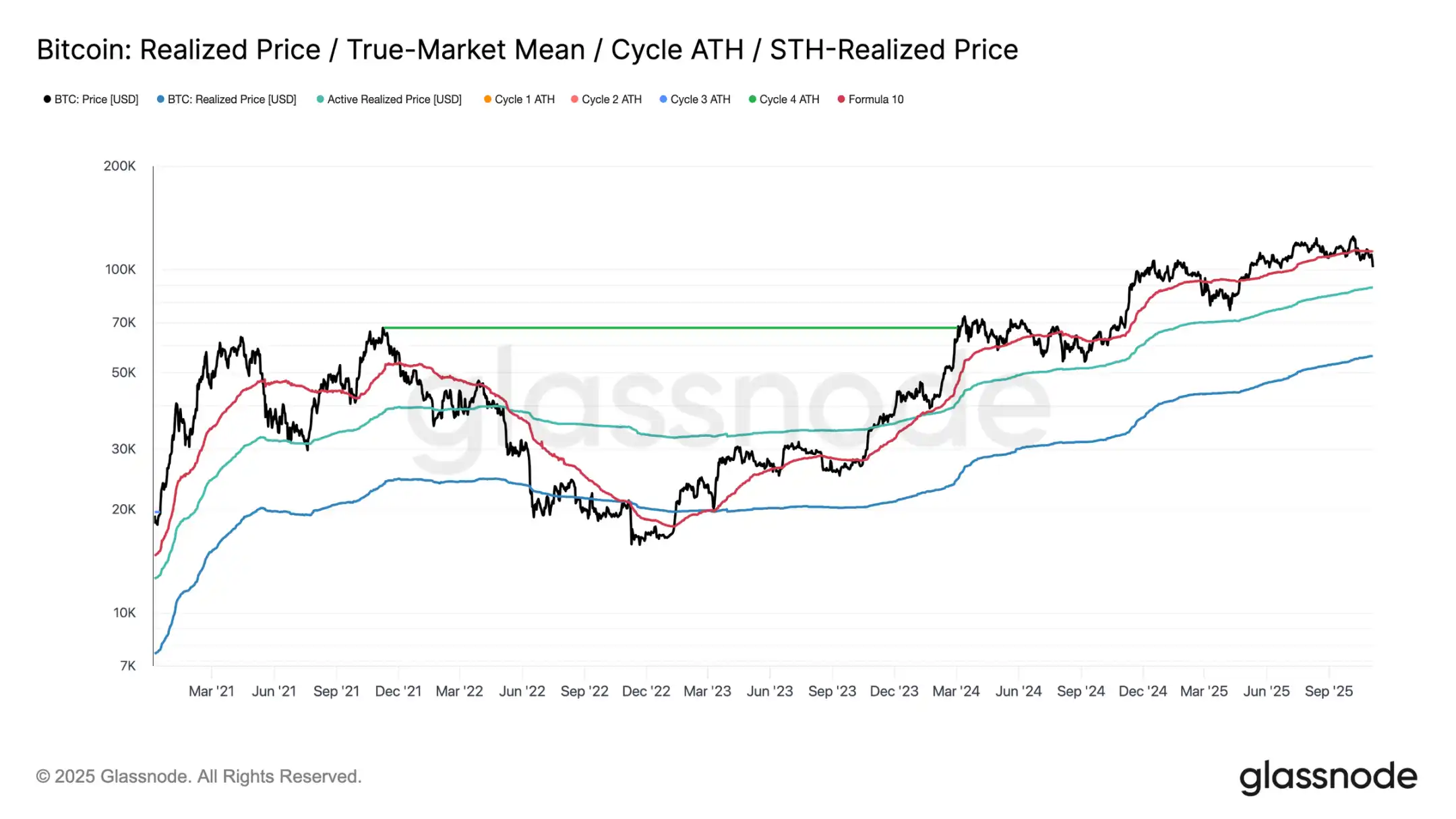

Since the market crash on October 10th, Bitcoin has struggled to hold above the short-term holder cost benchmark, eventually plummeting to around $100,000, roughly 11% below the key threshold of $112,500.

Looking at historical data, when the price experiences such a significant discount to this level, the possibility of further retracement to lower structural support levels increases — for example, the current active investor realized price of around $88,500. This indicator dynamically tracks the cost basis of active circulating supply (excluding dormant tokens) and has often played a crucial reference role during extended consolidation phases in past cycles.

Standing at a Crossroads

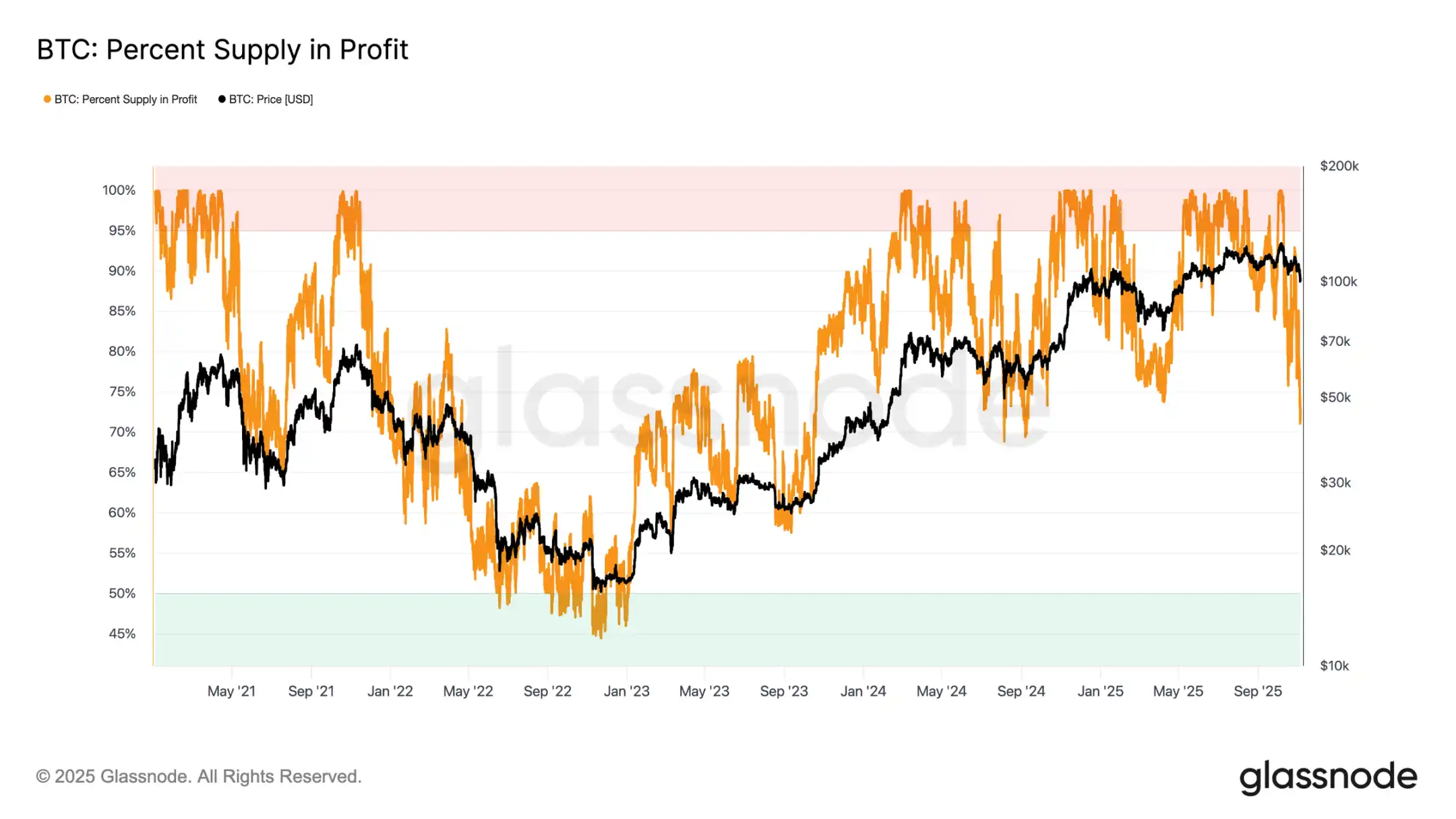

Further analysis reveals that the structure formed by this correction is similar to that of June 2024 and February 2025 — during these two periods, Bitcoin was at a key crossroads of "rebound" and "deep retraction." With the price at $100,000 currently, around 71% of the supply is still profitable, placing the market in a typical 70%-90% profit supply equilibrium range, signaling a mid-term slowdown.

This phase often sees a brief corrective bounce towards the short-term holder cost benchmark, but sustained recovery typically requires prolonged consolidation and new demand influx. Conversely, if further weakening leads to more holders facing losses, the market may transition from the current mild decline to a deep bear market phase. Historically, this phase is characterized by capitulative selling and long-term re-accumulation.

Tolerable Losses

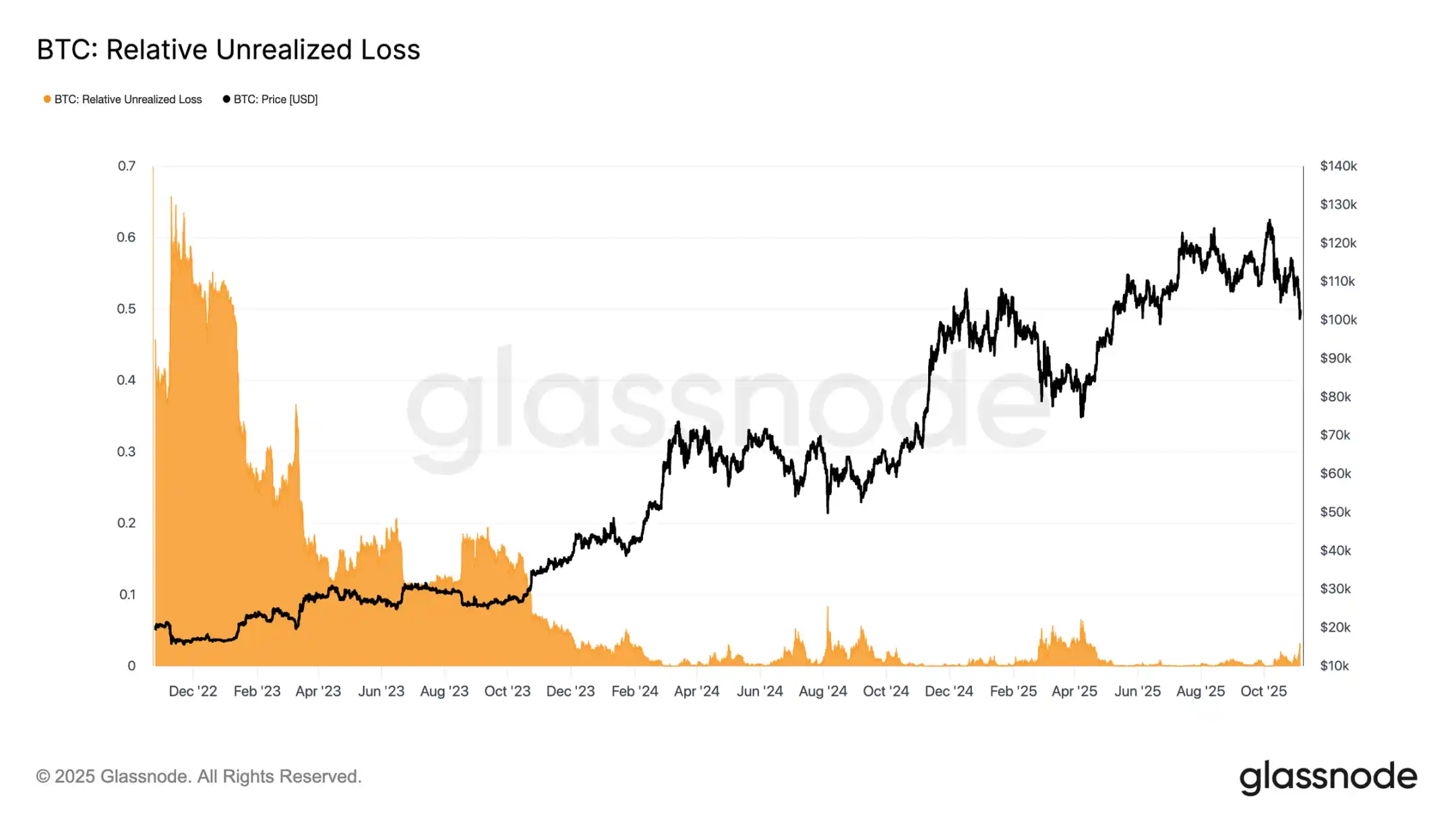

To further differentiate the nature of the current pullback, one can look at the relative unrealized loss ratio — this metric measures the proportion of total unrealized losses in USD terms to market capitalization. In contrast to the extreme loss levels during the 2022-2023 bear market, the current 3.1% unrealized loss ratio indicates mild market pressure, akin to the mid-term corrections in the third and fourth quarters of 2024 and the second quarter of 2025, all remaining below the 5% threshold.

As long as the unrealized loss ratio stays within this range, the market can be classified as a "mild bear market," characterized by orderly reassessment rather than panic selling. However, if the pullback intensifies and this ratio surpasses 10%, it could trigger widespread capitulative selling, signaling a more severe bear market environment.

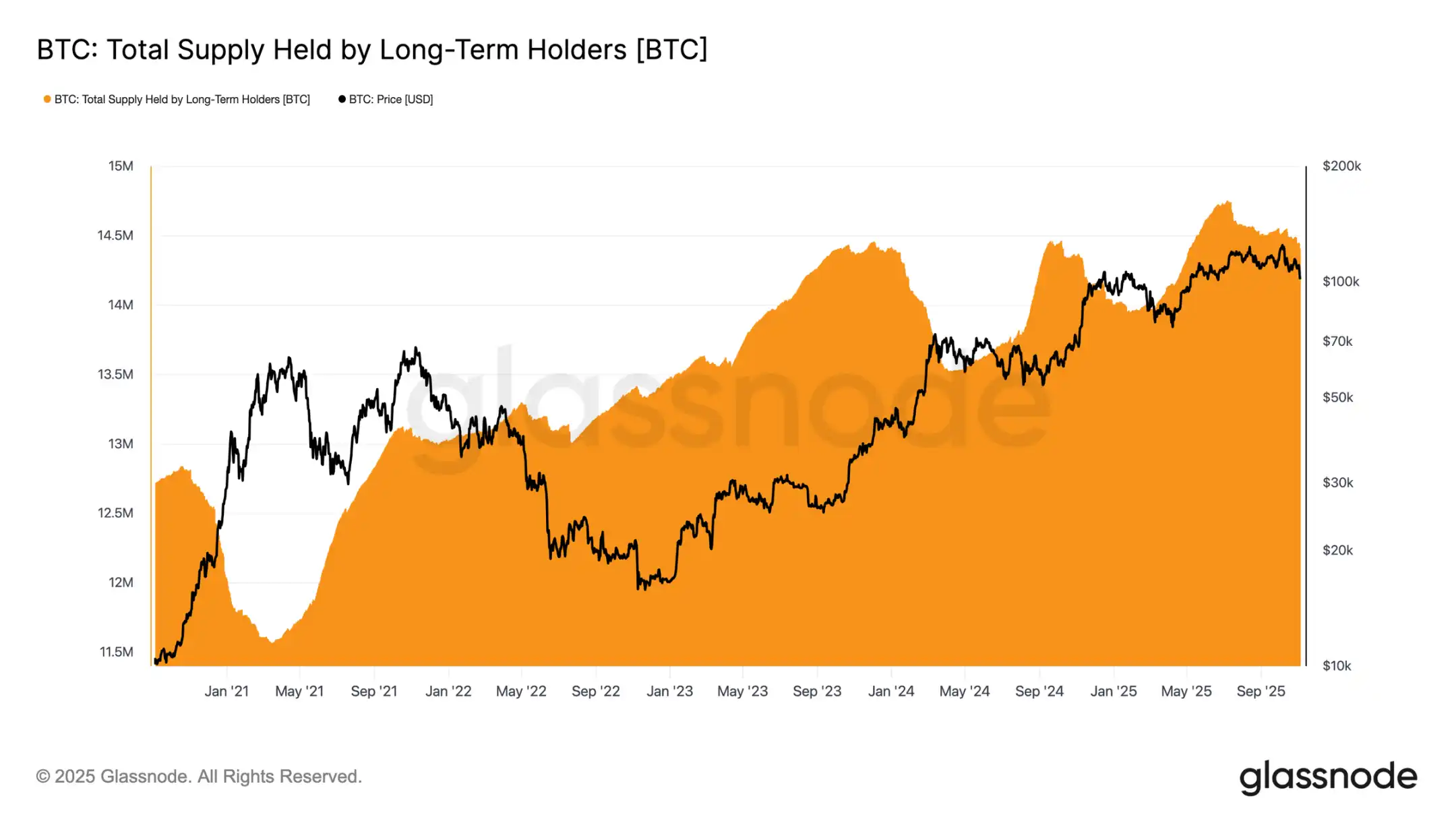

Long-Term Holders Continuously Selling

Despite the relatively manageable level of losses and a modest 21% retreat from the historical high of $126,000, the market is still facing mild but sustained selling pressure from long-term holders (LTH). This trend has been gradually emerging since July 2025, and even the new all-time high reached in early October has not changed this pattern, catching many investors by surprise.

During this period, the amount of Bitcoin held by long-term holders has decreased by approximately 300,000 coins (from 14.7 million coins to 14.4 million coins). Unlike the sell-off wave in the early stages of this cycle when long-term holders "sold the top," this time they are choosing to "sell the dips," meaning they are reducing their holdings during price consolidation and a sustained downtrend. This shift in behavior indicates that experienced investors are showing signs of deeper fatigue and a decrease in confidence.

On-Chain Insights

Ammo Depletion: Cooling Institutional Demand

Turning our attention to institutional demand: over the past two weeks, inflows into the U.S. Bitcoin spot ETF have significantly slowed, with daily net outflows ranging from $150 million to $700 million. This is a stark contrast to the strong inflows from September to early October, which provided price support.

The recent trend indicates that institutional fund allocations are becoming more cautious, with profit-taking and reduced willingness to open new positions dragging down overall ETF buying pressure. This cooling activity is closely related to the overall price weakness, highlighting a decrease in buyer confidence after months of accumulation.

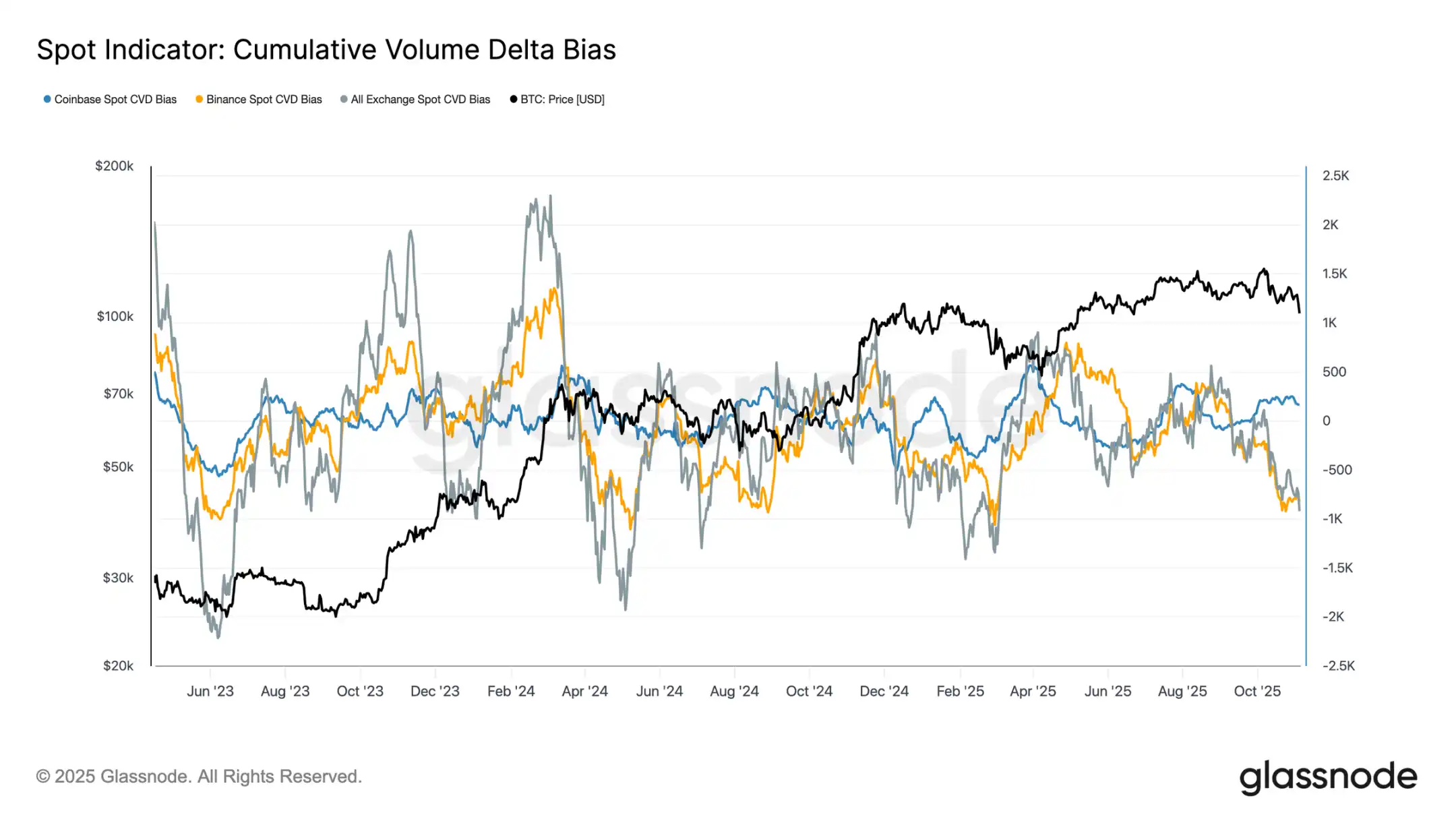

Biases Evident: Weak Spot Demand

Over the past month, spot market activity has continued to decline, with the cumulative volume delta (CVD) on major exchanges showing a downward trend. Both Binance and the overall spot CVD have turned negative, at -822 BTC and -917 BTC, respectively, indicating sustained selling pressure and limited active buying interest. Coinbase remains relatively neutral, with a CVD of +170 BTC, showing no clear signs of buyer absorption.

The deterioration in spot demand aligns with the slowdown in ETF inflows, indicating a decrease in retail investor confidence. These signals collectively reinforce the cooling of the market: waning buying interest, and a swift profit-taking encountered in the rebounding market.

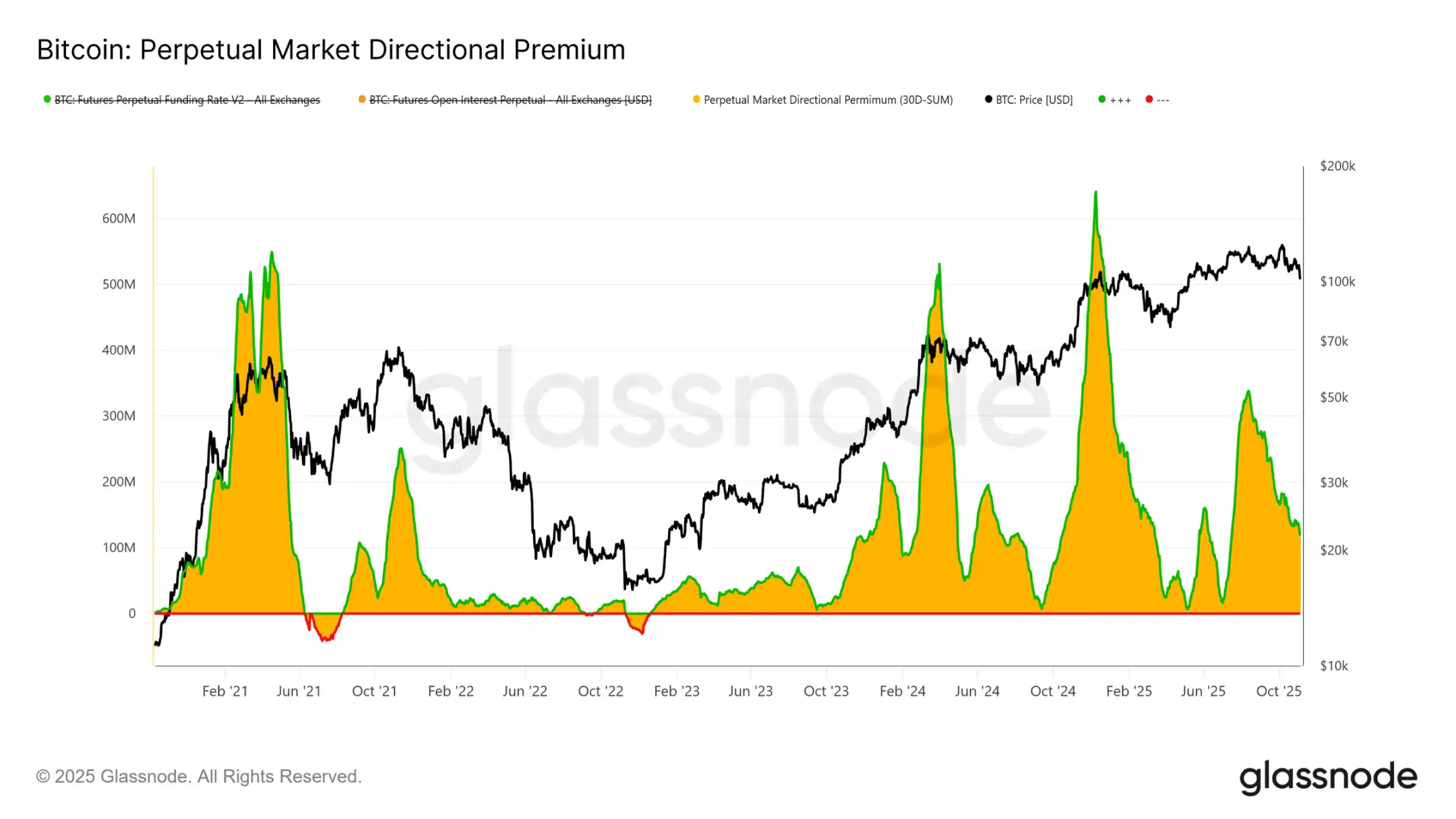

Interest Waning: Deleveraging in the Derivatives Market

In the derivatives market, the directional premium in the perpetual futures market (i.e., the cost paid by long traders to maintain their positions) has dropped significantly from a monthly peak of $338 million in April to approximately $118 million. This notable decline indicates widespread unwinding of speculative positions, with risk appetite clearly cooling off.

After a sustained period of elevated positive funding rates in the first half of the year, the steady slide of this metric suggests that traders are reducing directional leverage, favoring a more neutral stance rather than an aggressive long exposure. This shift aligns with overall tepid spot demand and ETF inflows, highlighting that the perpetual futures market has transitioned from an optimistic bias to a more cautious risk-averse posture.

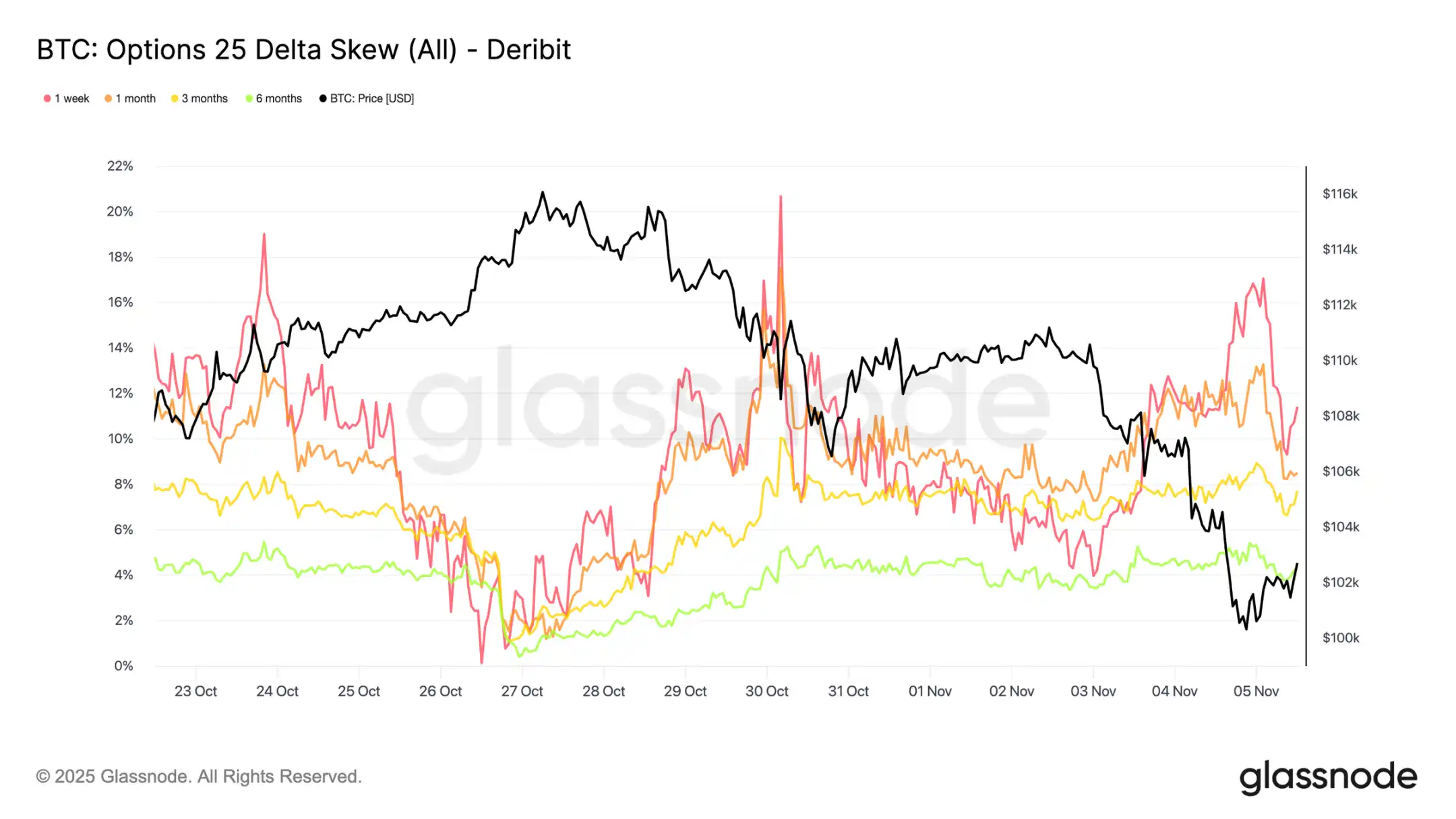

Seeking Protection: Defensive Tone in the Options Market

As Bitcoin hovers around the $100,000 psychological level, the option skew indicator unsurprisingly shows a strong demand for put options. Data indicates that the options market is not betting on a reversal or "buying the dip" but rather paying a high premium to hedge against further downside risk. Put option prices at key support levels are elevated, indicating that traders are still focused on risk protection rather than accumulating positions. In short, the market is hedging, not bottom-fishing.

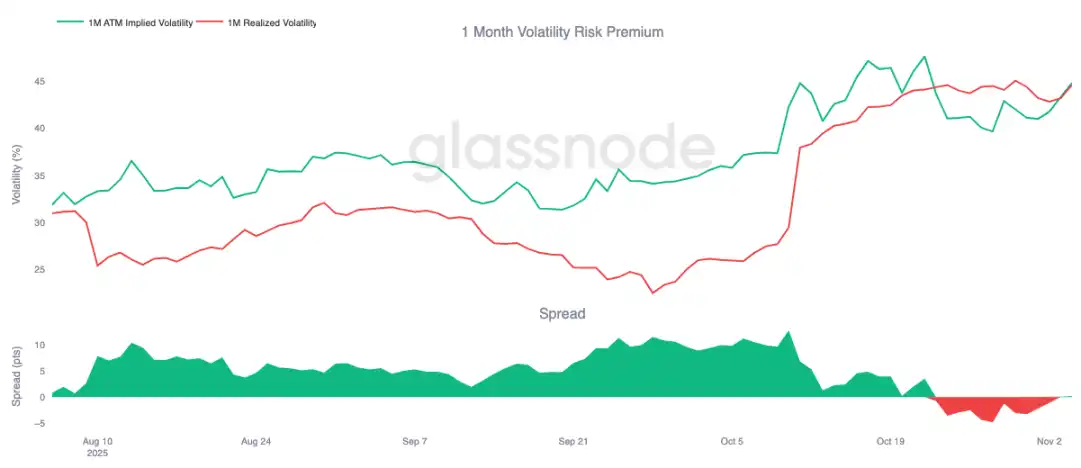

Risk Premium Resurgence

After ten consecutive days of negative values, the one-month implied volatility risk premium has slightly turned positive. As anticipated, this premium exhibits mean reversion—after a tough period for gamma sellers, implied volatility reprices higher.

This shift reflects a market still dominated by cautious sentiment. Traders are willing to pay a premium for protection, enabling market makers to take on offsetting positions. It's worth noting that as Bitcoin dropped to $100,000, implied volatility rose in sync with the re-establishment of defensive positions.

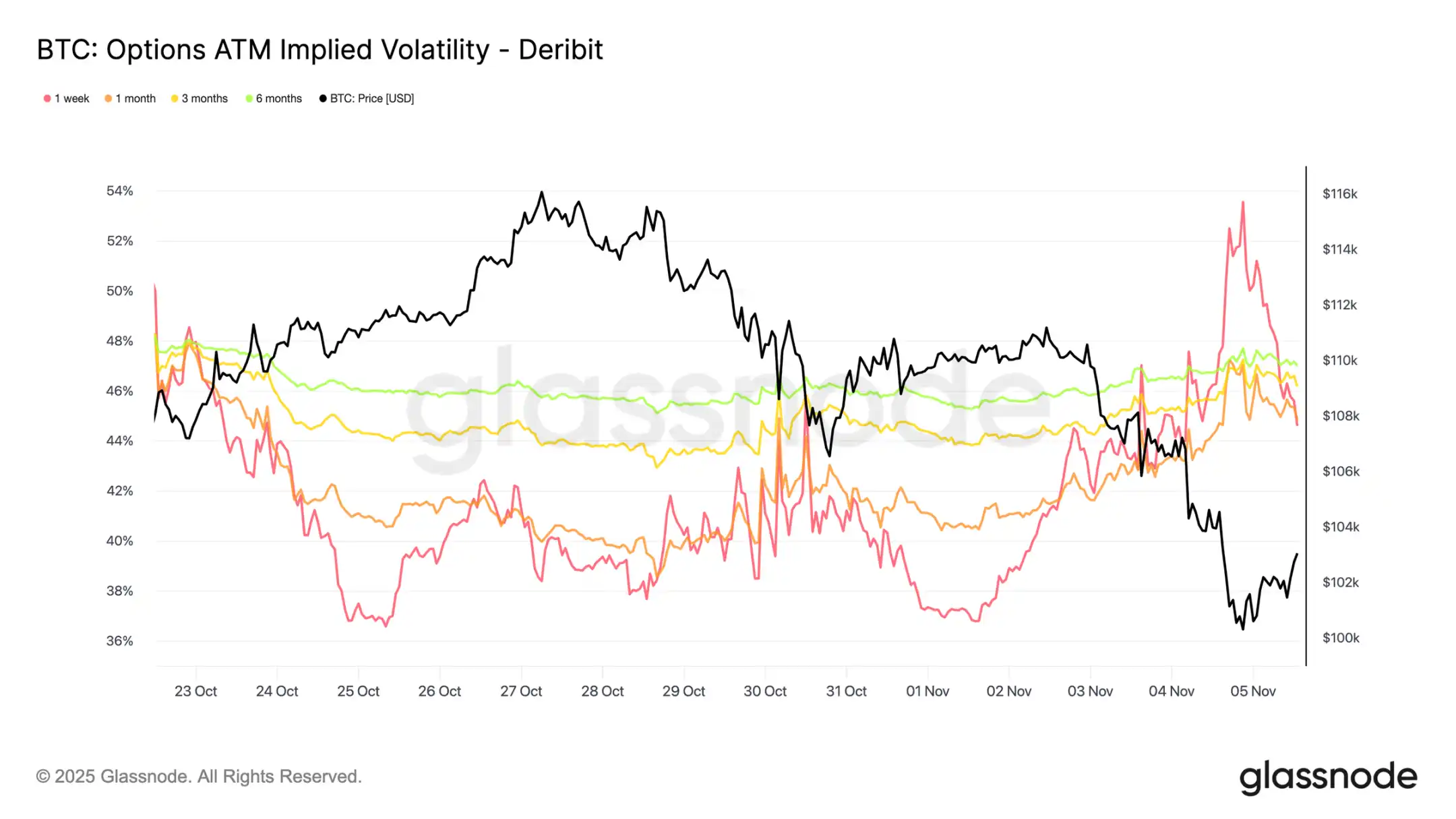

Volatility Spike Followed by Retreat

Short-term implied volatility remains closely inversely correlated with price action. During Bitcoin sell-offs, volatility surged significantly, with one-period implied volatility spiking to 54% at one point, before retracing approximately 10 volatility points near $100,000.

Longer-term maturity volatilities also rose: one-month implied volatility increased by around 4 volatility points from near $110,000 pre-adjustment levels, while the six-month implied volatility rose by about 1.5 volatility points. This pattern highlights the classic "panic-volatility" relationship, where rapid price declines still drive short-term volatility spikes.

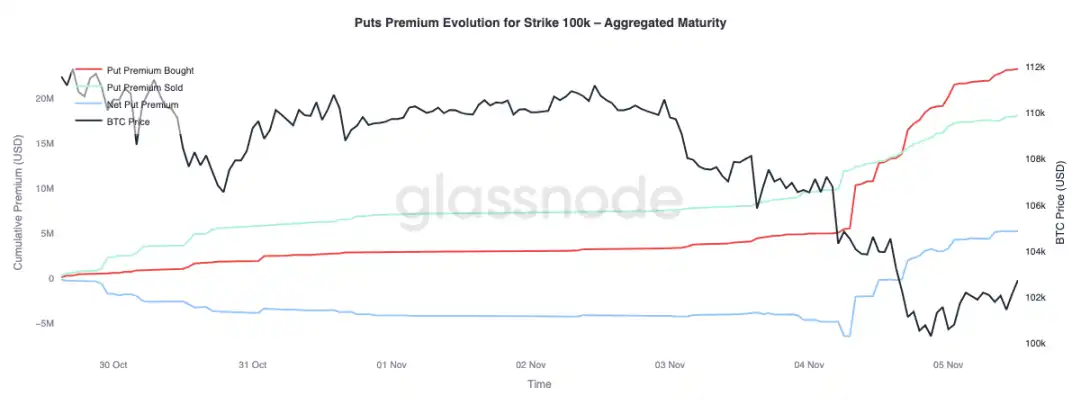

The Battle to Defend the $100,000 Mark

Observing the put options premium at a $100,000 strike price can provide further insights into the current sentiment. Over the past two weeks, the net premium of put options has gradually risen. Yesterday, as worries about the possible end of the bull market intensified, the premium surged significantly. During the sell-off period, the put options premium spiked, and even as Bitcoin stabilized near support levels, the premium remained high. This trend confirms that hedging activities persist, with traders choosing to protect rather than take on risk once again.

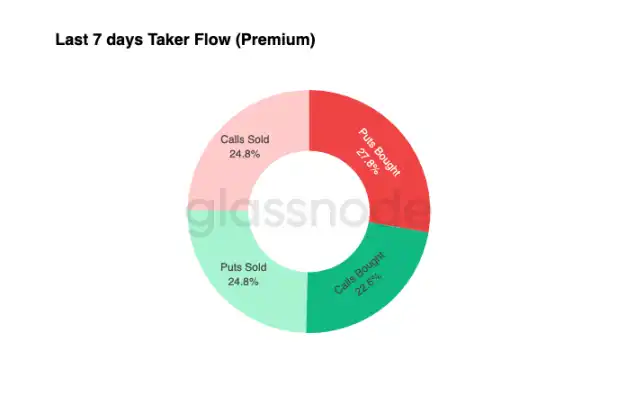

Defensive Fund Flows

Fund flow data from the past seven days shows that buy-side trades are dominated by negative delta positions—mainly achieved through buying put options and selling call options. In the past 24 hours, there is still no clear bottom signal. Market makers continue to hold long gamma, absorbing significant risk from profit-seeking traders and potentially capitalizing on bidirectional price swings.

This pattern has kept volatility high but manageable, with the market maintaining a cautious tone. Overall, the current environment is more conducive to defense rather than aggressive risk-taking, lacking a clear upward catalyst. However, due to the persistently high cost of downside protection, some traders may soon start selling risk premium to seek value investment opportunities.

Conclusion

Bitcoin breaking below the short-term holder cost basis (around $112,500) and stabilizing near $100,000 signals a decisive shift in market structure. As of now, this correction resembles past mid-cycle slowdown stages: 71% (in the 70%-90% range) of the supply is still in profit, and the relative unrealized loss stands at 3.1% (below 5%), indicating a mild bear market rather than a deep capitulation. However, ongoing selling by long-term holders since July and outflows from ETF products highlight weakening confidence among both retail and institutional investors.

If selling pressure continues, the active investor realized price (around $88,500) will be a key downside reference; while reclaiming the short-term holder cost basis would signal renewed demand strength. Meanwhile, directional basis swaps in the perpetual futures market and CVD skew both indicate a retreat of speculative leverage, reduced spot participation, and reinforce a risk-averse environment.

In the options market, strong demand for put options, a rise in the $100,000 strike price premium, and a slight rebound in implied volatility all confirm a defensive tone. Traders continue to prioritize protection over accumulation, reflecting a hesitancy toward the "bottom."

Overall, the market is in a fragile equilibrium: oversold but not in panic, cautious but structurally sound. The next directional move will depend on whether new demand can absorb sustained selling from long-term holders and reclaim the $112,000 - $113,000 range as strong support; or if sellers continue to dominate, extending the current downtrend.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia