Morgan Stanley Analysis: TSMC's Price Target Raised to 2988 New Taiwan Dollars, Can AI Capacity Expansion Support Profit Margins?

TL;DR

· TSMC raised its 2026 USD revenue growth outlook to slightly above 40%, and Morgan Stanley increased the target price to 2988 TWD.

· 2026 capital expenditure guidance raised to $60-64 billion, with 70-80% allocated to advanced processes.

· Challenges such as early production of 2nm chips, overseas factory costs, and weaker non-AI demand will still weigh on profit margin expectations.

After TSMC announced its second-quarter performance on July 16 and raised its full-year outlook, Morgan Stanley raised its target price from 2888 TWD to 2988 TWD, maintaining an "Overweight" rating.

The core numbers of this revision are straightforward. TSMC revised its 2026 USD revenue growth forecast from "over 30%" in April to "slightly above 40%," and the capital expenditure guidance increased from $52-56 billion to $60-64 billion. The company also stated that 70-80% of the full-year capital expenditure will be directed towards advanced processes.

Morgan Stanley's assessment is that AI demand is larger and more urgent than previously expected, prompting a change in TSMC's 2026 growth trajectory and expansion pace. However, this is not an unconstrained optimistic report. Challenges such as early production of 2nm chips, overseas factory costs, and weaker non-AI demand will still impact the speed of margin realization.

Strong Performance Leads, Growth Guidance Steps Up

TSMC's second-quarter performance provided support for the raised expectations.

According to the company's financial report, second-quarter 2026 revenue was 1.27038 trillion TWD, a year-on-year increase of 36.0%. Gross margin was 67.7%, operating margin was 60.3%, and earnings per share were 27.25 TWD. For the third quarter, the company provided revenue guidance of $44.6-45.8 billion, gross margin of 65-67%, and operating margin of 56-58%.

The more significant changes appeared in the full-year outlook. TSMC raised its 2026 USD revenue growth forecast to slightly above 40% during the analyst conference call, exceeding the previous "over 30%" guidance provided in April. Management described AI demand as "extremely strong," with cloud service providers being the key customers and signaling robust demand.

The growth assumption for AI revenue was also further increased by Morgan Stanley. TSMC had previously mentioned that AI semiconductor revenue growth is stronger than the "50% mid-to-high range" long-term statement, but the company did not provide a new CAGR number. Morgan Stanley incorporated a higher growth rate into the model, believing that a 70-80% annual compound growth rate assumption is now more reasonable.

This main trend does not equate to a synchronous recovery in all semiconductor demand. Non-AI demand remains weak, and inventory corrections in consumer electronics and traditional semiconductors are still ongoing. TSMC's current advantage lies in the fact that advanced processes are more easily filled with AI orders, and this part of the business has a greater impact on the company's revenue and profit.

Capital Expenditure Midpoint Raised to $62 Billion, Continued Focus on Advanced Processes

Capital expenditure is the most striking figure in this upward revision.

TSMC has raised its 2026 capital expenditure guidance to $60 billion to $64 billion, with a midpoint of around $62 billion. The company stated that 70%-80% of this amount will be allocated to advanced processes. Morgan Stanley has also raised its assumptions for future years' capital expenditures and expects the capacity for 2nm and 1.6nm to continue expanding.

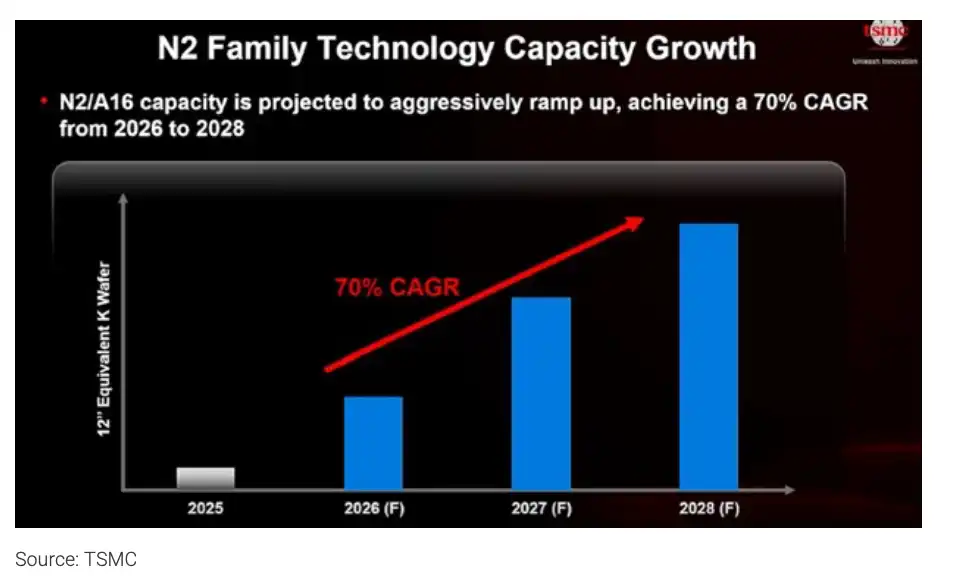

Capacity for the 2nm family of technologies is rapidly expanding from 2026 to 2028, with monthly capacity exceeding 200,000 wafers in 2028.

The expansion focus is not only on 2nm. TSMC mentioned at a recent investor conference that the scale of A14 and derivative technologies will be larger than N2, and their lifecycle will also be longer. Investment in U.S. fabs is also part of the long-term capacity plan. The company has previously proposed additional large-scale investments in the U.S., and the global layout of advanced nodes will raise the intensity of capital expenditures.

However, a capital expenditure increase does not simply equate to immediately adding an equivalent amount of available capacity. Morgan Stanley expects that the increment includes factors such as rising equipment prices and prepayments. In other words, the increase in investment intensity reflects urgent demand and changes in cost and payment pacing.

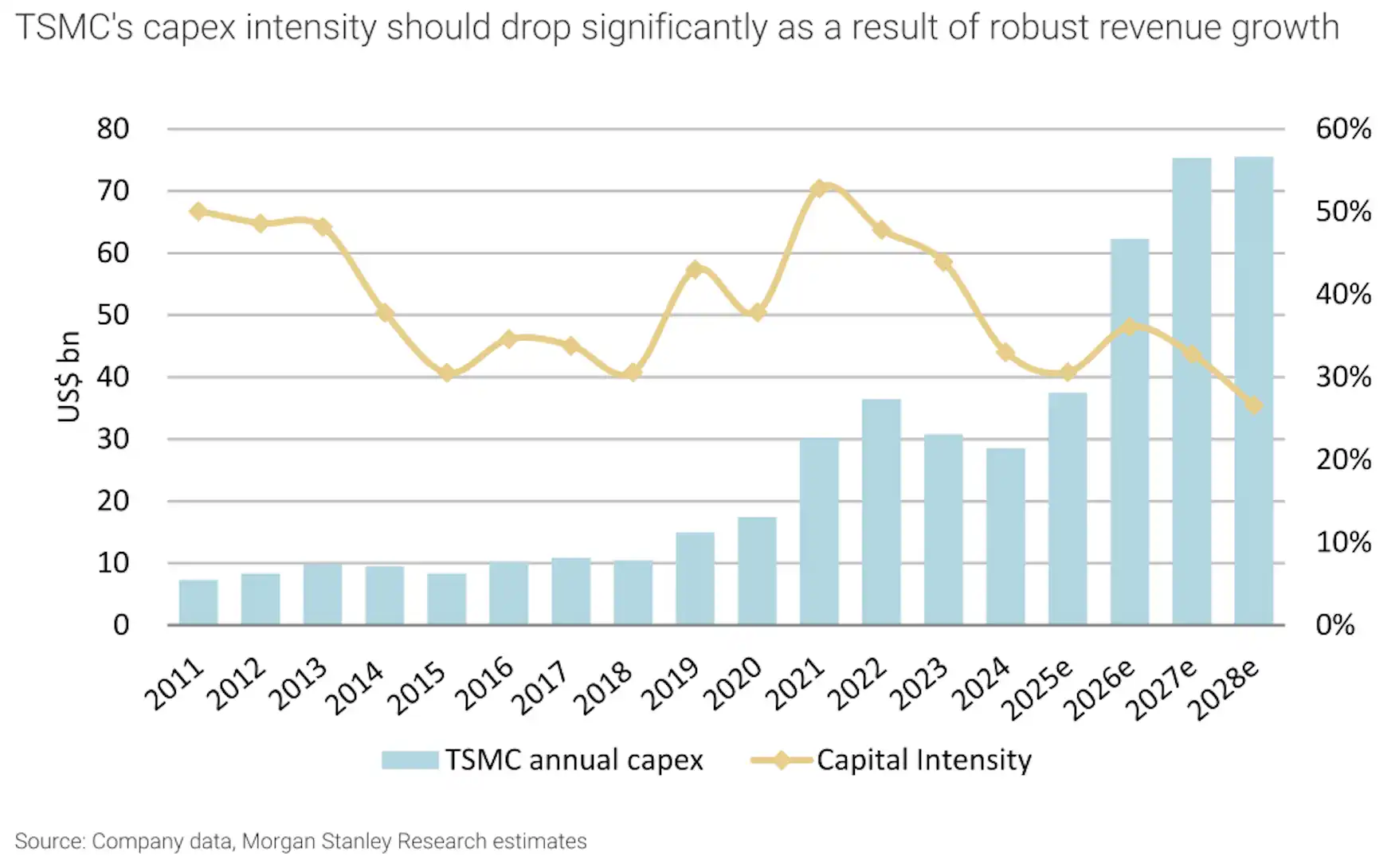

Capital intensity is expected to decline from a peak to about 30% between 2021 and 2028, as revenue growth improves capital expenditure efficiency.

For TSMC, the key is whether higher capital expenditure can lead to a higher revenue base. Morgan Stanley's long-term assumption remains somewhat optimistic, believing that as AI-related revenue continues to grow, capital intensity is expected to drop to around 30% by 2028.

NT$2988 Price Target, Betting on Continued Profitability

The price target has been raised from NT$2888 to NT$2988, reflecting not a quarterly earnings surprise but an upward revision in earnings assumptions for the next few years.

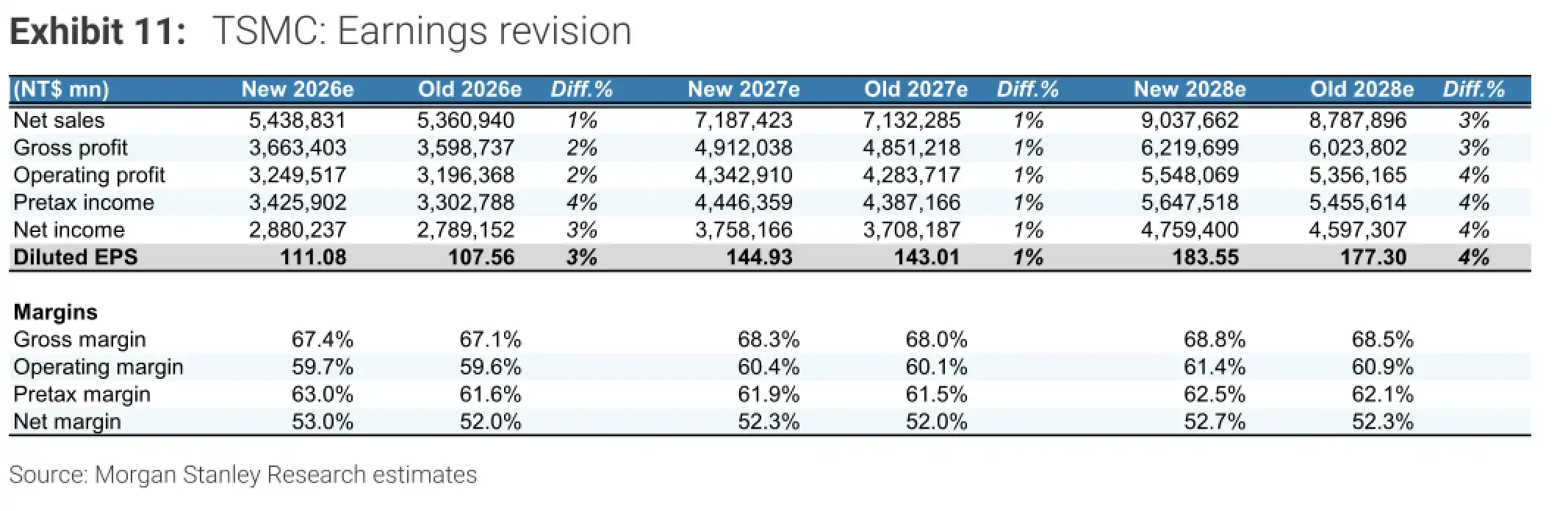

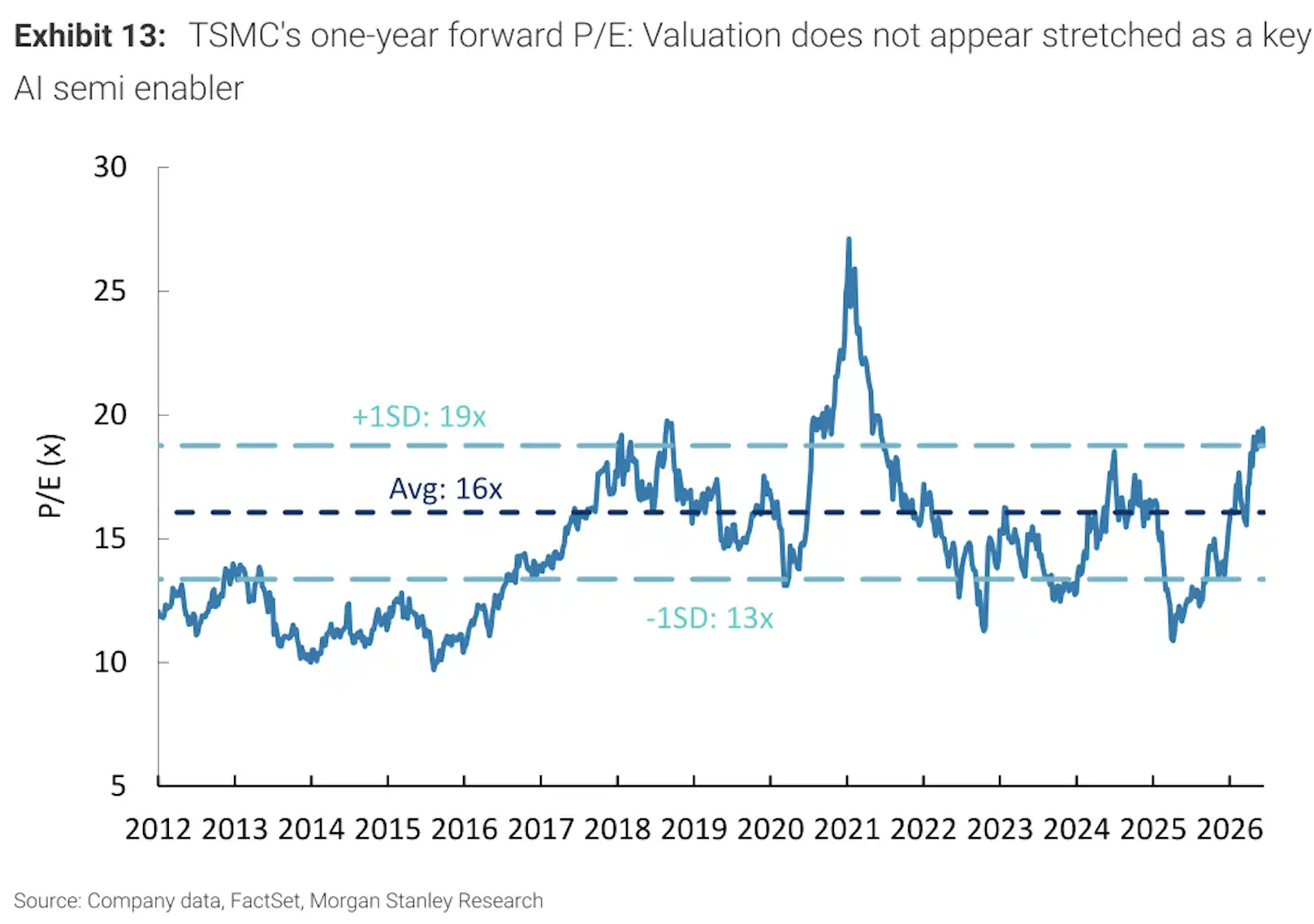

Morgan Stanley expects that TSMC's revenue, gross margin, and net profit forecasts for 2026-2028 have all been slightly revised upwards, with a simultaneous increase in earnings per share assumptions. The target price corresponds to a price-to-earnings ratio of about 20 times for 2027, while TSMC's current stock price corresponds to about 17 times for 2027, close to the historical average of around 16.5 times since 2018.

Revenue, Gross Margin, and Net Profit Forecasts for 2026-2028 Revised Upwards, with EPS Assumption Increased Accordingly.

The valuation upside comes from two conditions. First, AI revenue continues to be revised upwards. Second, TSMC's pricing and capacity utilization in advanced processes are expected to remain stable. Morgan Stanley expects that leading-edge wafer prices could still rise by 5%-10% in 2027, as customer reliance on advanced nodes will continue to support TSMC's bargaining power.

TSMC's One-Year Forward P/E Ratio is close to the 2018 average, with the target price implying approximately 20 times P/E for 2027.

This is also the reason why the market is willing to give TSMC a higher target price. The demand for AI chips not only brings order volume but also pushes the most advanced processes, advanced packaging, and next-generation node capacity scheduling to full capacity. As long as high-end AI chips continue to rely on TSMC, capacity constraints have the opportunity to translate into higher revenue and gross margin.

Gross Margin Yet to Meet the Most Optimistic Expectations

The current biggest constraint is still whether the profit margin can be smoothly realized.

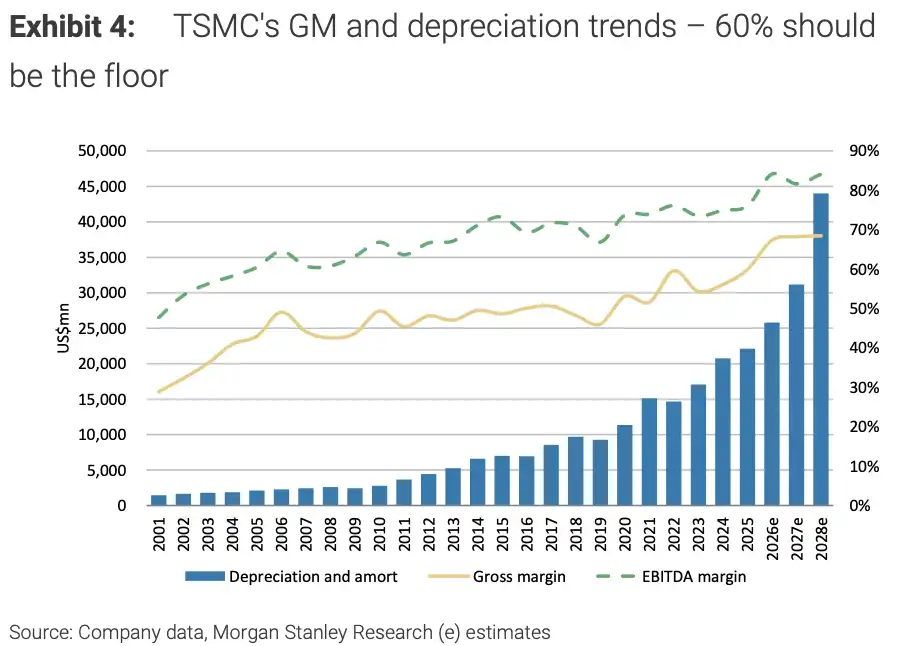

TSMC's third-quarter gross margin guidance is 65%-67%, still at a historical high, but lower than some market expectations close to 70% previously. As 2nm enters the early stage of mass production, depreciation, yield ramp-up, and early investments will bring cost pressures; production costs in overseas factories are generally higher than those in Taiwan. The faster the expansion of advanced nodes, the easier the short-term gross margin will be dragged down.

TSMC's depreciation and amortization are expected to increase significantly from 2026 to 2028, but Morgan Stanley believes the gross margin has the potential to remain above 60% in the long term.

Morgan Stanley remains relatively optimistic about the medium- to long-term profit margin. Although depreciation and amortization over the next three years will increase significantly with the expansion of advanced processes, the higher revenue scale, more favorable product mix, and pricing power of advanced nodes are expected to offset some cost pressures. The core judgment is that even as expansion enters a high-intensity phase, 60% could still be a long-term support line for TSMC's gross margin.

Non-AI demand poses another significant constraint. Consumer electronics demand remains weak, and the traditional semiconductor inventory adjustment has not yet been completed. If demand for end-applications such as smartphones and PCs remains soft, AI orders will need to take on more capacity filling and growth support. Morgan Stanley mentioned in the report that the tracking of Chinese smartphone shipments is weaker than previously expected, implying that TSMC's guidance revision should be more understood as being driven by AI demand rather than a comprehensive recovery of the semiconductor industry.

The competitive pressure is not significant in the short term, but it will still impact long-term valuation assumptions. TSMC currently maintains a clear lead in advanced processes, and its key high-end customers still heavily rely on its capacity and technology roadmap. However, if Samsung or Intel catch up in subsequent nodes, TSMC's long-term market share, pricing power, and profitability could face reassessment.

The key takeaway from this report is that AI demand has become strong enough to drive TSMC to raise both its 2026 growth expectations and capital expenditure plans. Whether a higher target price can continue to be absorbed by the market ultimately depends on whether these orders can consistently translate into high capacity utilization at 2 nanometers and subsequent nodes, stronger pricing power, and stable gross margins.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia