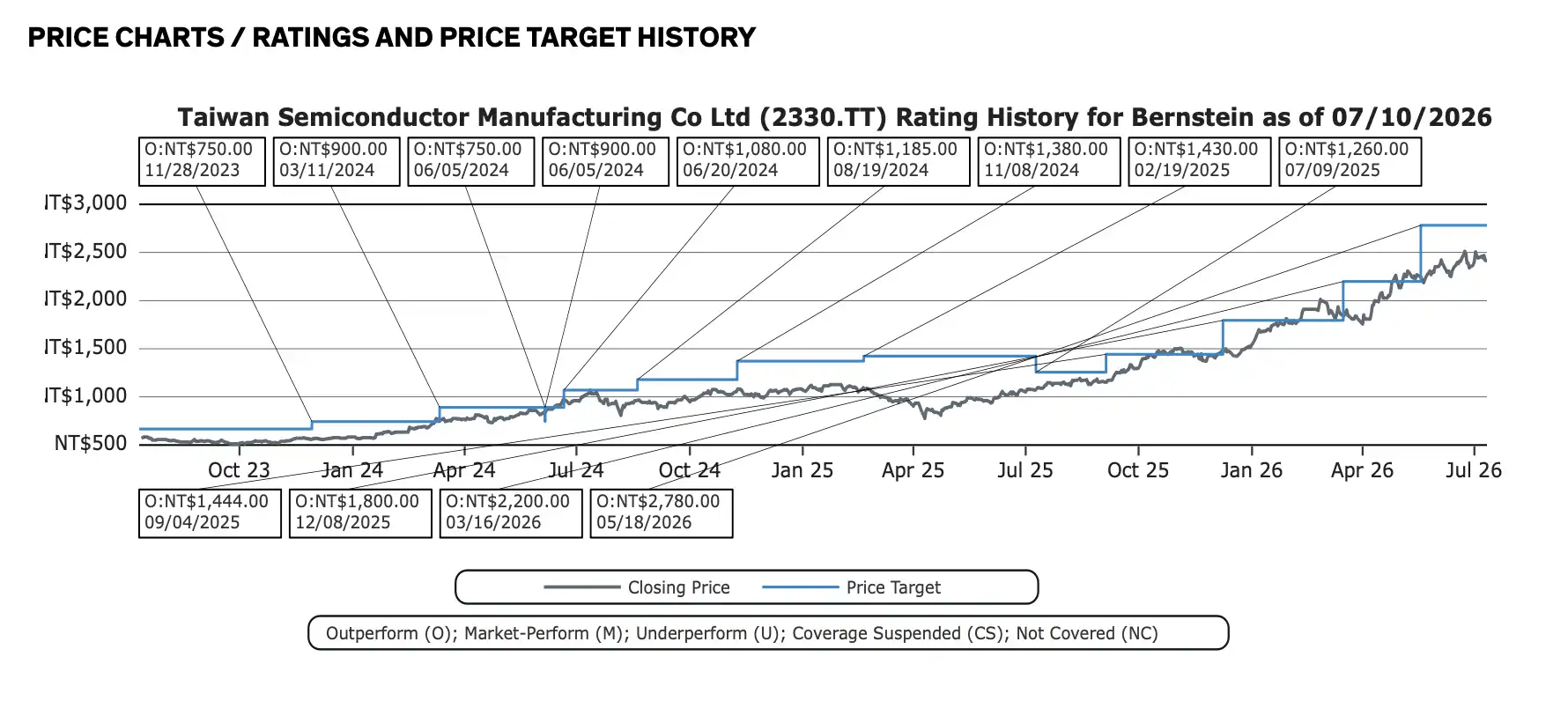

Bernstein Analysis: TSMC's Price Target Raised to 2780 NTD, Can CoWoS and N2 Keep Up?

TL;DR

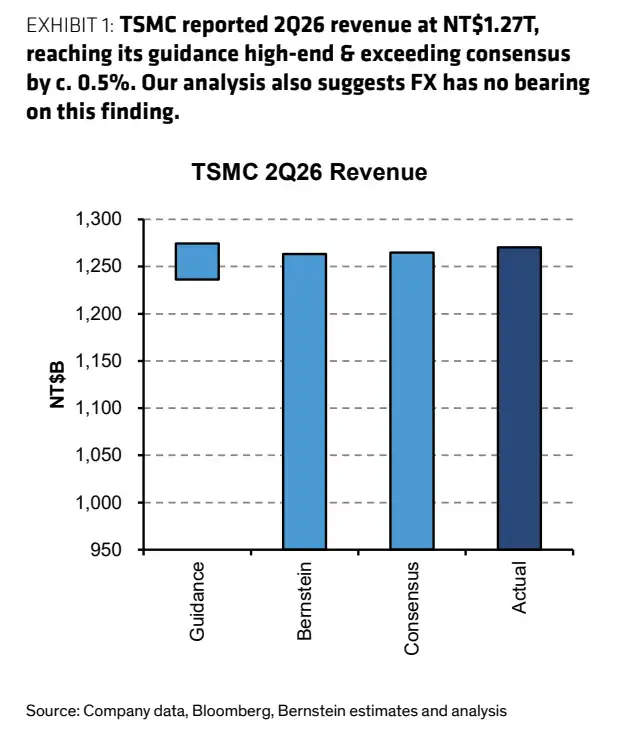

· TSMC's 2Q26 revenue is approximately NT$1.27 trillion, with a 67.9% YoY increase in June, demonstrating continued AI demand.

· Bernstein maintains a NT$2780 target price, with the model betting on high capex to bring more AI capacity.

· The high valuation requires the gross margin to keep up, while customer diversification and geopolitical risks will still constrain upside potential.

TSMC's second-quarter revenue is approximately NT$1.27 trillion, with a sequential growth of about 12% and a year-on-year growth of about 36%, falling within the company's earlier USD revenue guidance range and nearing the upper middle range. TSMC's official website monthly revenue data shows that the single-month revenue in June is NT$442.68 billion, with a 6.2% sequential growth and a 67.9% year-on-year growth.

This set of data continues to support a market consensus: AI chips, advanced processes, and advanced packaging demand continue to outpace supply. Bernstein recently maintained an Outperform rating on TSMC and raised the target price to NT$2780. Compared to the closing price of NT$2440 on the Taiwan Stock Exchange on July 13, this target price still leaves room for upside potential. However, what investors are more concerned about next is not just quarterly revenue but capacity, gross margin, and N2 process ramp-up.

Bernstein Continuously Raises TSMC's Target Price

TSMC will hold its second-quarter earnings conference on July 16. With the second-quarter revenue already disclosed, the focus has shifted to how management will update full-year demand, expand advanced packaging, 2026 to 2027 capital expenditure, and whether the intensive investment will start impacting the gross margin.

Second-Quarter Revenue Nearing Upper Middle Range of Guidance, June YoY Increase Nearly 68%

The second-quarter NT$1.27 trillion revenue is the most direct number in this report. The company's previous USD revenue guidance for the second quarter was between $39 billion and $40.2 billion, assuming an exchange rate of 31.7. By this measure, second-quarter revenue is approximately $39.6 billion, within the guidance range and close to the upper middle range.

June's single-month revenue of NT$442.68 billion continues to rise from May's NT$416.97 billion. The first half of the year totaled NT$2.404 trillion in revenue, a 35.6% year-on-year increase. This indicates that orders for advanced processes and AI-related demand are still translating into actual revenue, rather than just staying in the capital market expectations.

2Q26 Revenue Comparison Bar Chart, actual around 1.27 trillion New Taiwan dollars, higher than some market estimates and within the company's guidance range.

The profit margin is another story. The source report projected a second-quarter gross margin of around 65%, but TSMC's previous official guidance was 65.5% to 67.5%. As the official financial report release date on July 16 approaches, a more cautious statement is that the market still expects TSMC's gross margin to remain high, but the final number should be based on the July 16 earnings report.

For wafer foundries, whether the gross margin can stay high depends on the proportion of advanced processes, capacity utilization, depreciation pressure, and customer bargaining power. TSMC's current advantage lies in the fact that AI and high-performance computing demand continue to help it absorb higher capital expenditures.

$56 billion Capex for AI Capacity

Whether TSMC's valuation can hold steady depends not only on how much second-quarter revenue exceeds expectations but also on whether it can turn AI demand into deliverable capacity.

According to the Bernstein model, TSMC's 2026 capital expenditure is estimated to be $56 billion, further increasing to $68 billion in 2027. This scale reflects dual pressures: the continued increase in demand for advanced processes and the fact that advanced packaging capacity remains a bottleneck for AI chip delivery.

Based on the source report, CoWoS capacity is expected to reach 135,000 wafers per month by the end of 2026 and 195,000 wafers per month by the end of 2027. For NVIDIA, AMD, and major cloud providers developing their AI chips, advanced packaging capacity directly affects whether chips can be delivered on time. If the packaging stage lags behind after wafer manufacturing, final shipments will still be constrained.

This is also why the market pays close attention to TSMC's capex guidance. High capital expenditure not only indicates strong demand but also brings about increased depreciation and cash flow pressure. As long as customers are willing to lock in capacity and advanced process prices can be maintained, high investment is a growth driver. If AI demand slows, high investment will in turn squeeze profit margins.

The N2 process will also be a focus of the financial report. TSMC's leadership in advanced processes remains a key moat that sets it apart from other foundries. What the market wants to confirm is whether the N2 ramp-up is progressing as planned, whether customer adoption is smooth, and whether cost pressures from new processes can be offset by price and scale.

Price Target of NT$2780 is Not Low, Stock Price Already Betting on AI

As of July 13, 2026, TSMC's Taiwan Stock Exchange closing price was NT$2440. Bernstein's NT$2780 price target, based on approximately 20 times one-year forward P/E ratio, still implies some upside.

But this is no longer a story of undervaluation reversal. Based on the source report, the current stock price corresponds to a forward P/E ratio of about 21 times. The market has already priced in a premium for AI demand, leading-edge process technology, and high gross margins.

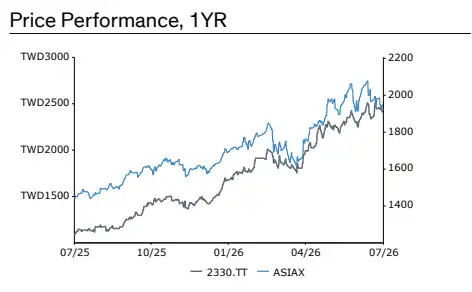

TSMC's stock price has been on a continuous uptrend over the past year, currently around 2440 New Taiwan dollars, with a TTM relative performance of 86.5%.

The future stock price will depend more on earnings realization. As long as revenue, gross margin, and capacity expansion continue to outperform expectations, the high valuation can be absorbed by earnings growth. If capital expenditures continue to rise but profit margins start to slip, investor tolerance for the current valuation will decrease.

Over the past 12 months, TSMC's relative performance has reached 86.5%. The market has deemed it as one of the most core beneficiaries of AI infrastructure expansion. The more core the asset, the easier it is to withstand valuation pressure when expectations cool slightly.

The Rise of Secondary Sources, But TSMC's Dominance is Hard to Replace Temporarily

The competitive risk currently does not lie in TSMC's leading position being shaken but rather in customers seeking more options amid capacity constraints.

Samsung has recently been reported by the media to have raised prices by about 15% for some new customers at the 4/5nm and 8nm nodes, and has discussed a 2nm AI chip project with Anthropic and Meta. Intel has also garnered market attention regarding its possible participation in Google's TPU-related supply, but current discussions lean more towards advanced packaging or technologies like EMIB, which cannot be simply equated to wafer foundry orders.

These pieces of news are unlikely to substantially impact TSMC's revenue in the short term. TSMC still holds significant advantages in leading process yields, scale, and customer base. The real signal is that when advanced process and advanced packaging supplies remain tight in the long term, large customers will actively seek a second source of supply.

Even if alternative solutions have limited short-term capacity and a long technology validation cycle, they may weaken TSMC's bargaining power in the medium to long term. Geopolitical uncertainties and customer concerns about overreliance on a single supplier will also sustain diversified demand.

For TSMC at the current valuation level, these risks do not need to immediately impact revenue. They merely need to affect the valuation multiples that investors are willing to give, which is enough to cause stock price volatility. The questions to be addressed at the July 16 earnings call are very specific: how fast will advanced packaging expand, will N2 ramp-up drag down gross margins, and can high capital expenditures continue to be absorbed by AI orders. TSMC remains one of the most dominant companies in the AI manufacturing chain, but to achieve the target price of 2780 New Taiwan dollars, more capacity and margin data need to keep up.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia