Federal Reserve's new chair Jerome Powell made his debut. With interest rates unchanged, what should the market focus on?

TL;DR

· Kevin Warsh has assumed the role of Federal Reserve Chair, and the June 16-17 FOMC meeting is his first to chair with quarterly projections.

· The market is hardly pricing in a rate cut this time, with the focus on whether he will downplay the dot plot and forward guidance in his remarks.

· Related assets: US Treasuries, US Dollar, Gold, Bitcoin, Nasdaq growth stocks, VIX, MOVE.

Kevin Warsh will chair the June 16-17 FOMC meeting for the first time as Federal Reserve Chair. The market does not anticipate a rate change, instead, all eyes are on whether he will alter the Fed's communication approach.

According to the Fed's announcement on May 22, Kevin Warsh has been sworn in as Federal Reserve Chair and Governor, and was unanimously selected as Chair of the FOMC. This June meeting is a two-day gathering with a press conference and quarterly economic projections. For traders, this is not just any policy meeting, but the new Chair's first decision on how to use the Fed's "roadmap tools."

For a considerable period, macro trading has revolved not just around trading inflation and employment but also around trading the path the Fed provides. The dot plot, press conference wording, and hints from the Chair about future policy have all been translated into movements in US Treasuries' yields, the US Dollar, Gold, growth stocks, and Bitcoin.

What sets Warsh apart is his public skepticism of these tools. Publicly reported and confirmed hearing testimonies indicate his reservations about forward guidance and the dot plot, suggesting they may shackle policymakers to outdated forecasts. If in his debut he keeps rates unchanged but starts to diminish the weight of these tools, the market loses not just a chart but an anchor to pre-trade future rate paths.

This is not to be misconstrued as the "death of the dot plot." New Chairs typically avoid unnecessary market turmoil in their initial meeting. What is more likely to change is that the tools will remain, but the tone will shift. The chart will still be published, but the Chair will caution the market against interpreting it as a commitment. Investors need to assess that if the Fed provides less of a roadmap, what will be the primary driver for prices going forward.

Rates Not in Question, Language Becomes the Trade

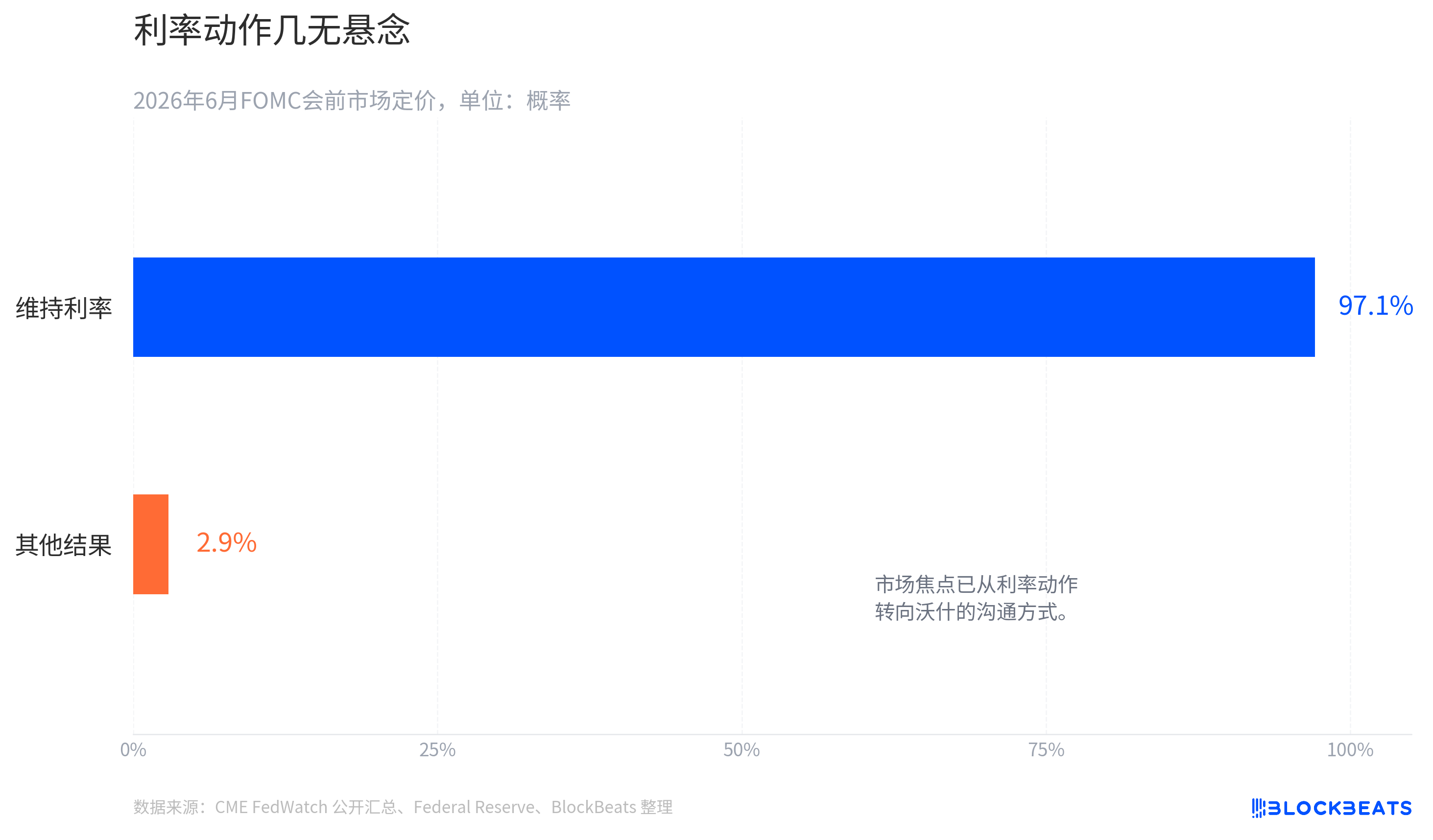

This meeting is most easily misinterpreted as a standard FOMC preview: will they cut rates, hike rates, how will the dot plot median change. However, from pre-meeting pricing, the rate decision itself is no longer the main variable.

According to CME FedWatch and public summaries of related pricing, the market's expectation before the meeting for June is around a 97%-99% probability of maintaining the Federal Funds Rate in the 3.50%-3.75% range, which fluctuates over time. Unless an extreme surprise occurs, investors are not awaiting a rate action but Warsh's interpretation of future policy.

The sensitivity of the quarterly projection meeting lies in the Federal Reserve's release of the Economic Projections Summary, with the most anticipated being the dot plot. The dot plot can be understood as an anonymous vote by Federal Reserve officials on the future level of interest rates, with each dot representing a committee member's view on where the rate should be around a certain year. It is not a formal commitment but has long been treated by the market as a rough policy roadmap.

Forward guidance is more direct. It is when a central bank informs the market in advance about the likely future path of policy, aiming to stabilize expectations and reduce price volatility. In the past, investors often traded not based on actual Federal Reserve actions but on clues released beforehand in speeches and statements by the chair. Hawkish wording led to rising yields, while dovish wording resulted in a rebound in risk assets. Hinting at a rate cut benefited long-duration assets.

The focus of Powell's debut lies here. If he keeps rates unchanged and emphasizes that all projections are merely conditional assessments and that the future entirely depends on real-time data, the market will interpret this as the Federal Reserve being unwilling to continue providing a clear roadmap. Even though the dot plot still exists, its trading weight may decrease.

This is directly related to retail investors. When looking at U.S. Treasuries, gold, Bitcoin, and the Nasdaq in the past, one often wondered, "What will the Fed say next?" If Powell's framework becomes "wait for the next inflation and jobs report," asset prices will be more easily swayed by individual data points and oil price fluctuations, making it harder to keep volatility suppressed in the long term.

Powell's Communication Philosophy is Being Priced In by the Market

The biggest difference between Powell and Powell's era may not lie in a single rate decision but in his fundamental philosophy on central bank communication.

According to several media outlets and think tanks' analysis of his congressional testimonies, Powell has repeatedly questioned forward guidance and the dot plot. His core concern is that once the Federal Reserve maps out a path for the market in advance, it will be constrained by its own forecasts. When real data changes, policymakers might delay acknowledging that the forecasts are outdated to maintain communication consistency.

This logic may not sit well with the market, but it is appealing for internal central bank decision-making. The economy does not operate on a quarterly projection schedule. Inflation could suddenly be affected by an energy shock, employment could be stronger than the models anticipated, and financial conditions could loosen due to asset price rebounds. By prematurely committing to a certain path, the central bank would relinquish flexibility to past judgments.

What Powell prefers is a framework that involves reassessing based on the latest data at each meeting, rather than letting the market deduce the next meeting based on the previous dot plot. This would partly take back policy initiative from market expectations and make it harder for traders to lock in rate paths in advance.

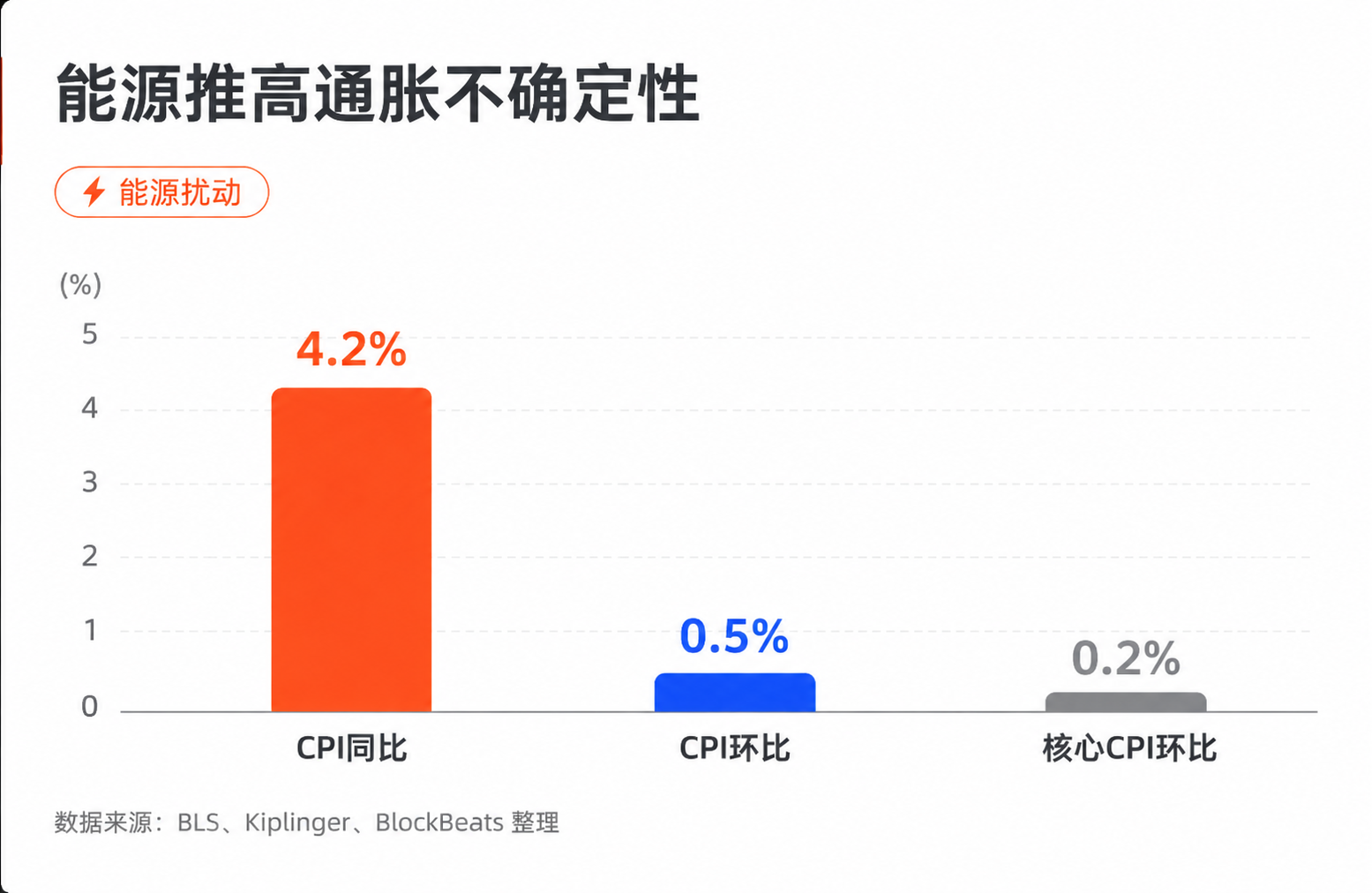

The current macro environment has strengthened this trend. According to BLS data, the US May CPI year-over-year rose to 4.2%, up 0.5% month-over-month, with core CPI up 0.2% month-over-month, where energy was a significant contributing factor. It is not a simple equation to say that energy prices determine inflation, as services, housing, wages, base effects, and supply chain issues also impact the price trajectory. However, the energy shock has indeed increased inflation uncertainty, making it more challenging for the Fed to signal early easing.

If inflation picks up again and employment remains robust, the Fed will be less willing to be tied to a future rate-cutting path. For Powell, downplaying the dot plot is not a mere formality but a way to reduce the market's reliance on a single path.

The market's issue is that it has long been accustomed to transparent communication. While the dot plot often deviates from reality, it provides traders with a common reference point. It allows different assets to be priced around the same interest rate path and keeps volatility suppressed most of the time. Powell wants more flexibility, but what the market loses is predictability.

If the Fed Talks Less, Volatility Will Be Repriced First

The market may not necessarily demand the Fed always be accurate in its communication, but it heavily relies on the Fed being clear in its communication.

This is the conflict between Powell and many Fed watchers. Many observers acknowledge that the dot plot forecasts often deviate from reality and understand that forward guidance can fail in extreme circumstances. However, financial markets trade not only the real world but also others' expectations of the real world. An imperfect but public anchor often makes pricing easier than having no anchor at all.

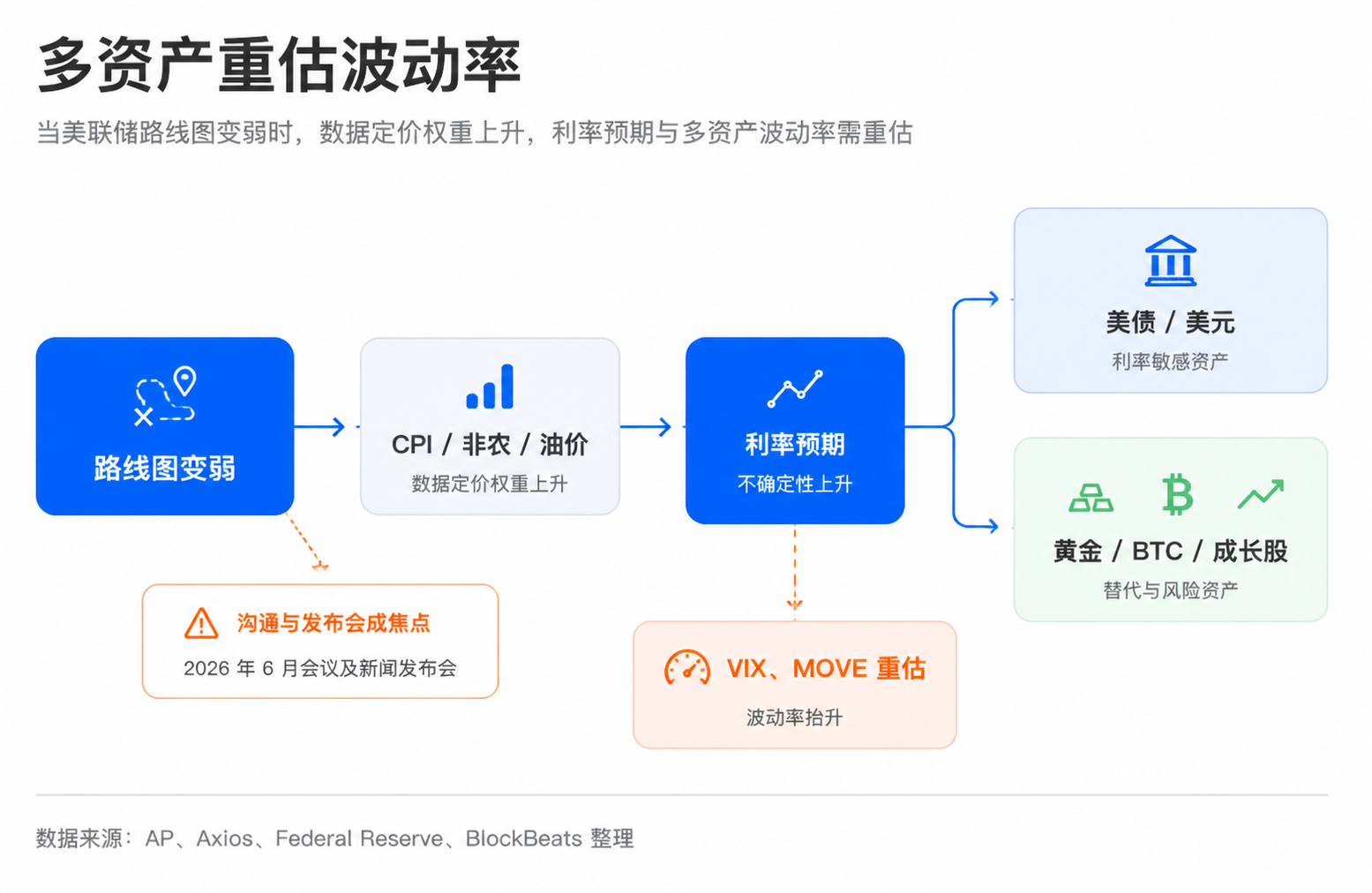

If this anchor weakens, the impact would first fall on US Treasuries. Treasury yields do not simply reflect the current rate but discount future inflation, growth, policy paths, and risk premia. In the past, when the Fed hinted at future paths, the market could adjust the entire yield curve in advance. If future chairs provide less direction, the 10-year yield could become more sensitive to every CPI, nonfarm payroll, and oil price change.

The dollar would face a similar issue. The dollar's short-term strength often depends on the US rate expectations relative to other economies. When the Fed's path is more uncertain, the forex market would need to directly compare US inflation, employment, fiscal policy, and global risk sentiment, and dollar volatility may no longer revolve solely around a press conference remark.

Gold's logic is more complex. Inflation uncertainty and geopolitical risks usually support gold, but if US Treasury real rates rise due to hawkish data, gold would also come under pressure. Powell talking less is not automatically bullish for gold; what truly favors gold is a combination of an unclear policy path and persistent inflation risks.

Bitcoin and growth stocks are more sensitive to uncertainty in the discount rate. Such assets are more sensitive to long-term liquidity and the future interest rate path. In the past, if the market was convinced of a clear rate-cutting path, risk assets could trade at a valuation expansion in advance. If the Fed is unwilling to provide a clear path, investors must pay a risk premium for a wider range of interest rate outcomes. Even if there is ultimately no rate hike, as long as uncertainty rises, valuations may be temporarily suppressed.

Low-volatility trades will also face challenges. Over a period of time, many strategies have been built on the assumption that central banks would communicate in advance and the market would not suddenly lose its anchor. If the new chair's communication framework allows data itself to take on more pricing function, the low levels of stability in volatility indicators such as VIX and MOVE will need to be revalidated.

The Emphasis is Not on the Institutional Announcement

Investors should not only focus on whether the dot plot has been released; it is highly probable that it will still appear as usual. More crucial is how Powell characterizes it: if he emphasizes that the dot plot is only a collection of individual forecasts, does not represent a committee commitment, and redirects attention to inflation, employment, and energy prices, the market will begin to reduce the weight of the dot plot in its trading models.

The divergence within the dot plot itself is also worth watching. If the committee's judgments on the future interest rate path become more dispersed, even if the median does not change much, it will increase the market's pricing range for different policy outcomes. For U.S. Treasuries, the U.S. dollar, gold, growth stocks, and Bitcoin, this means that volatility may be reassessed beforehand.

What this meeting truly validates is not whether Powell will immediately abandon a certain tool, but whether he is starting to change the market's interpretation of the Fed. If he transitions cautiously, asset prices may breathe a sigh of relief in the short term; if he explicitly reduces the weight on the dot plot and forward guidance, the next CPI release, the next nonfarm payroll report, and a sudden jump in oil prices will be more like a mini FOMC press conference than in the past.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia