Binance is using its main platform to facilitate stock token liquidity, CME is set to launch 24-hour trading for oil, and will Hyperliquid's valuation anchor be changed?

TL;DR

· CME plans to introduce mini WTI crude oil and 1 oz gold for 24/7 trading, as the traditional market addresses the risk management gap during off-market hours.

· Binance, NYSE/ICE are also advancing towards round-the-clock tokenized assets, with Hyperliquid's "instant trading of traditional assets" advantage being reevaluated.

· Related tickers: HYPE, CME, ICE, BNB, as well as oil, gold, and US stock tokenization-related products.

The recent pullback of HYPE can easily be attributed to unlocks, whale selling, or questions around TradeXYZ's SpaceX preIPO. However, looking at a longer time frame, another issue is becoming more significant: the ability of Hyperliquid, historically rewarded by the market for "instant trading of traditional assets," is now being replicated by traditional finance and centralized exchanges.

On June 11, CME announced plans to launch 24/7 mini WTI crude oil futures pending regulatory review and to extend the existing 1 oz gold futures to round-the-clock trading. Almost simultaneously, as publicly disclosed, Binance introduced bStocks, allowing users to trade tokenized US stocks like NVDA, TSLA with the liquidity of the Binance main platform; NYSE/ICE is also developing their own 24/7 tokenized securities and on-chain settlement platform.

These products are not the same. What CME is doing is regulated futures, Binance bStocks is closer to the gateway of tokenized stocks, and what Hyperliquid is doing is on-chain perpetual contracts. However, they are competing for the same demand: when crude oil, gold, or US stocks are off the traditional market, traders still want immediate exposure or instant risk hedging.

So this is not a story of "CME has already taken away Hyperliquid's trading volume." The CME crude oil new product has not yet launched, and gold 24/7 trading is also awaiting until July, real diversion still needs transaction data validation. It is more like an anticipated reevaluation: if 24/7 is no longer a unique scarce ability of Hyperliquid, how should the market understand HYPE's valuation anchor?

24/7 Trading is Transitioning from a Cryptocurrency Advantage to a Platform Standard

Regular investors can understand the issue more simply: news does not wait for the opening bell.

A geopolitical conflict could occur over the weekend, causing immediate changes in oil and gold prices. Earnings reports, regulatory investigations, or unexpected events involving a US stock could also take place outside of traditional trading hours. In the past, traders either had to wait for the market to open and face the risk of price gaps or seek alternative instruments to hedge in advance. The cryptocurrency market has always had an advantage in this regard due to its natural 24/7 trading.

Hyperliquid aims to address this gap. It is not just a cryptocurrency perpetual trading platform but also brings exposure to traditional assets such as stocks, crude oil, and gold onto the blockchain. Some third-party HIP-3 markets and ecosystem products even extend to earlier assets. For some traders, Hyperliquid is like a "never-closing convenience store of risk": when the US stock market is closed or commodity futures liquidity is insufficient, on-chain contracts still allow them to express their views, hedge, and even engage in leveraged trading.

This is precisely the pain point that CME is tapping into. According to CME's announcement on June 11, the new 10-Barrel WTI Crude Oil futures contract will be approximately the size of 10 barrels, one-tenth the size of the existing Micro WTI contract, and is scheduled to launch on August 30, 2026, with cash settlement. The existing 1 oz Gold futures contract is set to transition to 24/7 trading starting from July 26, 2026, also settled in cash.

The so-called small-scale futures, in plain terms, refer to breaking down large commodity contracts into smaller units so that traders do not have to commit a large amount of capital and can manage risks more finely. Derek Sammann, Global Head of Commodities at CME, stated in the announcement that in the face of geopolitical uncertainty, traders need regulated products of suitable size available 24/7 to manage risk exposure when news breaks.

The key emphasis in this statement lies not only on "24/7" but also on being "regulated" and "of suitable size." The former targets institutions and compliant funds, while the latter reduces the entry barriers. CME does not necessarily aim to replicate Hyperliquid's high leverage and on-chain experience; it aims to provide another form of round-the-clock exposure: something more traditional, compliant, and easier to be accepted by the existing financial system.

CME, Binance, NYSE Eyeing the Same Layer of Demand

CME, Binance, and NYSE/ICE have introduced products in different forms, but what they collectively replicate is a layer of advantage that Hyperliquid has most easily explained to the market: the ability to trade traditional assets even during market closures.

CME's approach focuses on commodities. Crude oil and gold are already core assets in global macro trading, and the more intense the geopolitical tensions, the stronger the risk management need during non-trading hours. For traditional institutions, if CME can provide sufficient liquidity during nighttime and weekends, they may not necessarily need to turn to on-chain perpetual platforms to take on additional compliance, custody, and operational risks.

Binance's niche is the tokenization of US stocks. According to public reports, the initial batch of bStocks includes NVDAB, TSLAB, CRCLB, MUB, SNDKB, among others, emphasizing 24/7 trading, 1:1 conversion, and self-custody support. a differentiation needs to be made here compared to Binance's other stock-related products; bStocks are closer to a tokenized stock gateway and should not be confused with stock perpetual contracts.

Tokenized stocks can be understood as "on-chain versions of stock certificates," unlike Hyperliquid's synthetic perpetuals. Synthetic perpetuals are more like contracts based on price movements, where traders do not hold real stocks. Tokenized stocks, on the other hand, aim to peg the price closer to the underlying asset and enhance trust through a conversion mechanism.

The direction of NYSE/ICE is more like foundational infrastructure. ICE/NYSE announced in January this year that they are developing a tokenized securities trading and on-chain settlement platform, intending to support 24/7 trading, instant settlement, USD amount orders, stablecoin fund transfers, and requiring regulatory approval. If this direction materializes, traditional trading platforms will not only extend trading hours but will also transition some of the securities market's settlement and trading logic to a more on-chain-like experience.

These three cannot be directly equated. CME futures involve margin, delivery, and a regulatory framework; Binance bStocks are more like a tokenized stock gateway within a centralized exchange; Hyperliquid perpetuals lean towards high leverage, on-chain collateral, and rapid speculation or hedging. Their users, risk management, leverage, and KYC requirements are all different.

However, market revaluation does not require them to be entirely the same. As long as they address some overlapping needs, Hyperliquid's narrative will change. The previous narrative was that if you wanted to trade oil, gold, or US stocks at any time, on-chain perpetuals were one of the most direct gateways. The current narrative has evolved into: you can still go to Hyperliquid, but you can also choose CME, Binance, and in the future, possibly NYSE's tokenized platform.

Hyperliquid Needs to Prove Traders Will Stick Around

For supporters of Hyperliquid, the moves by CME and Binance certainly do not equate to full replacement. The appeal of on-chain perpetuals has never solely been about round-the-clock trading.

Hyperliquid's strengths include high leverage, self-custody, on-chain speed, trading culture, and an established liquidity network. For crypto-native traders and certain high-frequency speculative capital, less KYC, faster listing, more flexible margin use — these are experiences that traditional trading platforms find challenging to replicate. Even if CME offers 24/7 trading for crude oil and gold, it will not immediately attract all traders willing to take on on-chain risks and seek higher leverage.

Liquidity itself also exhibits inertia. Traders consider not only product specifications but also depth, slippage, fees, available leverage, and counterparties. If Hyperliquid already has sufficient liquidity on certain contracts, new compliant products may not immediately capture trading volume. Especially in the early stages, whether CME's overnight and weekend trading is truly active still needs to be confirmed with actual trade data, rather than just relying on product announcements.

Pressure is also coming from here: Hyperliquid can no longer rely solely on the phrase "we are 24/7" to prove the scarcity of exposure to traditional assets. What it needs to demonstrate is that even though other platforms also trade around the clock, traders are still willing to keep their positions, margins, and trading volume here.

This will translate into the pricing logic of HYPE. Some investors usually perceive HYPE as a platform-traded asset related to trading volume and fees: the more trading, the higher the fees, the stronger the protocol's funds for HYPE buybacks, making the token more likely to receive narrative support from cash flow. This fee and buyback cycle has been a key reason why HYPE has differentiated itself from many purely narrative tokens in the past.

The actions of CME, Binance, and NYSE/ICE may not immediately change Hyperliquid's actual revenue in the short term, but they will alter the market's perception of future revenue growth. The HYPE pullback can be explained by various factors, including unlocks, whale behavior, overall risk appetite, and competitive expectations, rather than simply attributing it to CME's new products. However, as competitors begin to fill the gap in 24/7 capability, the market will naturally question whether the smooth conversion of future traditional asset perpetual trading volume into fees and buybacks can continue as before.

This is why this round of discussion is more a reassessment of expectations than a performance validation. CME's new crude oil contract has not yet launched, and there is no clear data on user migration between Binance bStocks and Hyperliquid's stock perpetual. What can be confirmed now is that the "uniqueness" of Hyperliquid in traditional asset exposure is declining; what cannot be confirmed is to what extent this will translate into actual trading volume loss.

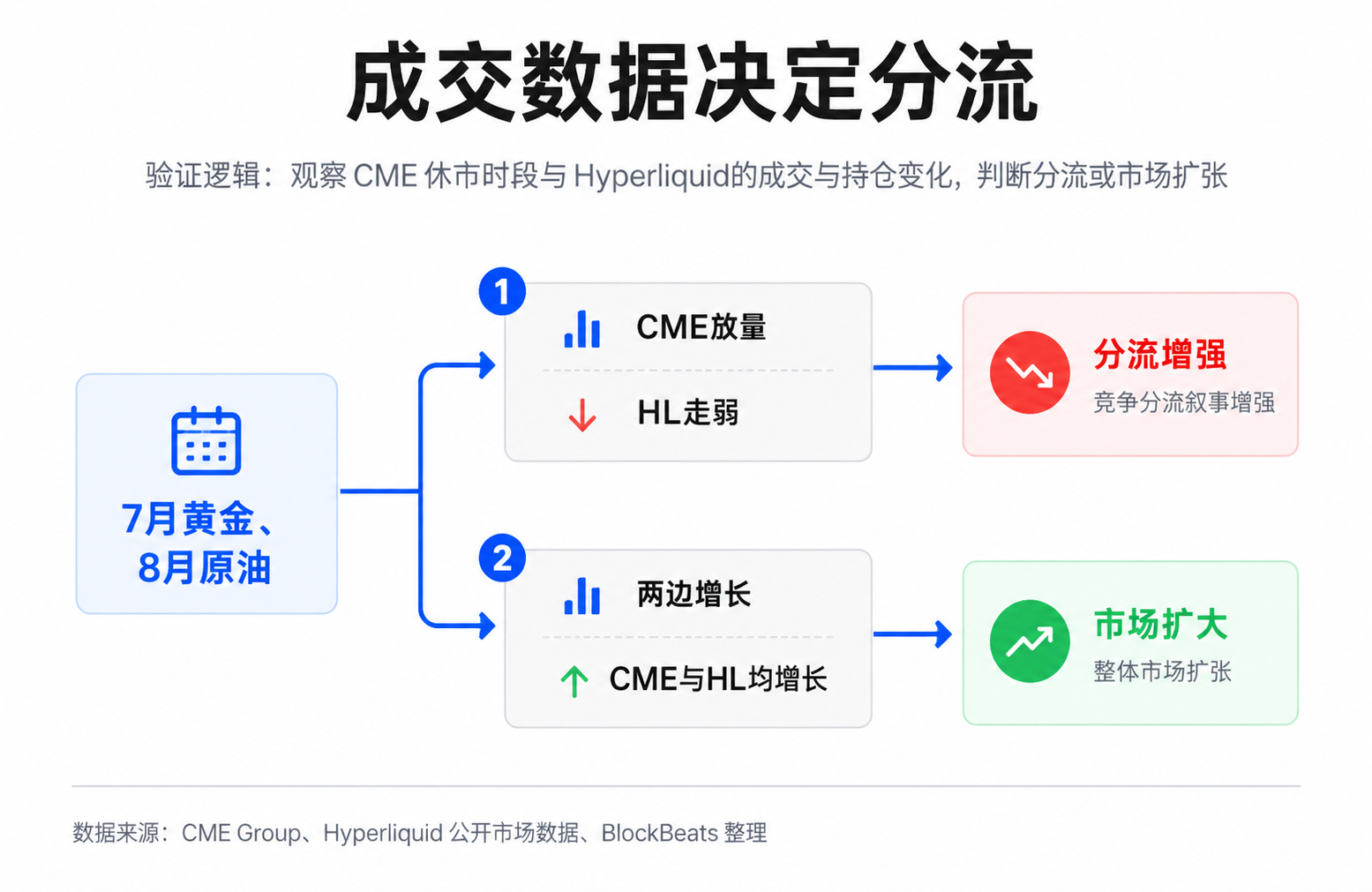

July and August Will Provide the First Round of Validation

What is truly worth watching next is not which platform states 24/7 in its announcement, but whether there is actual trading and depth during off-hours.

CME's 1-ounce gold futures plan to commence 24/7 trading on July 26, 2026, and the new 10-contract WTI crude oil futures plan is set to go live on August 30, 2026. These two milestones will provide the market with the first batch of validation samples: whether overnight and weekend trading is active enough, whether spreads are tight enough, and whether institutions and professional traders are indeed relocating risk management back to the regulated futures system.

For Hyperliquid, a more direct observation metric is the trading volume, open interest, and fee contribution of the corresponding perpetuals for commodities and stocks. If the CME Gold and Crude Oil futures volumes surge, while Hyperliquid's market sees a simultaneous decline in trading volume and open interest, the narrative of competitive diversion will strengthen. If both sides experience growth, it indicates that 24/7 trading may be expanding the overall market, rather than simply moving on-chain trading off-chain.

The key to HYPE is also here. Unlockings and whale trades may impact short-term prices, but the longer-term valuation anchor still needs to return to whether the platform can sustainably generate fees and convert those fees into buybacks. As long as the trading volume and buyback intensity can cover the additional supply and sentiment pressure, the competitive expectations may not necessarily turn into a trend damage. Conversely, if the perpetual growth of traditional assets slows down and external platforms' round-the-clock liquidity begins to take shape, the market's pricing of HYPE will shift from a "high-growth trading platform token" to a more cautious cash flow expectation.

It is not yet time to draw conclusions about Hyperliquid. More accurately, the demand it pioneered and validated is being recognized and replicated by larger financial platforms. The next round of data will determine whether this reassessment remains at the narrative level or continues to transmit to revenue and token prices.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia