Illustration of SpaceX Trillion-Dollar IPO Pricing: Bypassing Wall Street's Mandatory "Reference Price," What's the Significance of the $135 Price Point?

On June 2, SpaceX submitted an amended S-1 to the SEC, disclosing IPO pricing details: $135 per share, issuing 5.556 billion shares of Class A common stock, implying a valuation of approximately $1.77 trillion, and raising $750 billion. On June 12, it debuted on the Nasdaq under the ticker symbol SPCX. This marks the largest tech IPO in history, exceeding Saudi Aramco's 2019 IPO fundraising record by over 2.5 times.

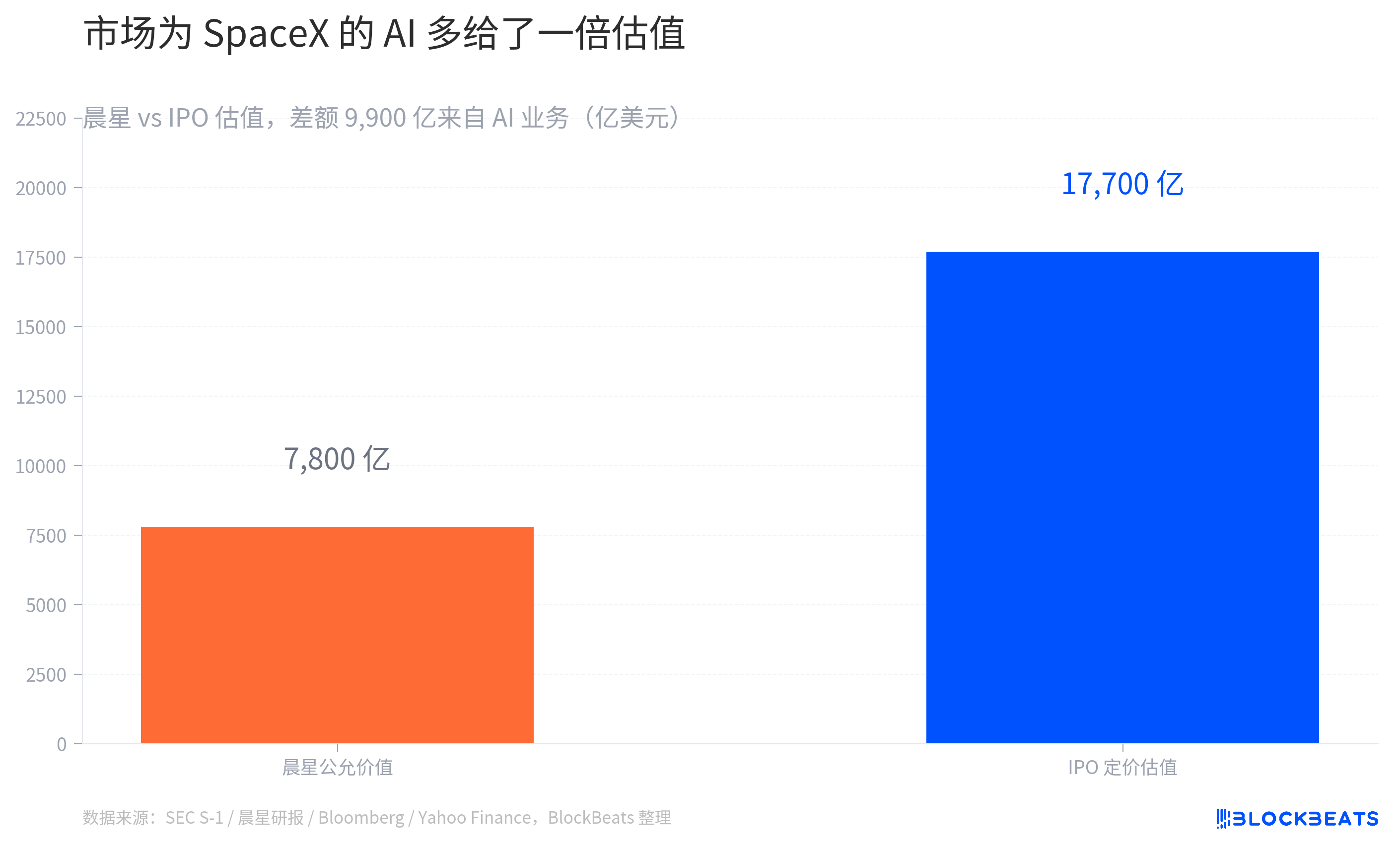

However, on the same day as the pricing announcement, Morningstar's initial research coverage took a completely different stance. According to analyst Nicolas Owens' DCF model calculation, SpaceX's actual fair value is around $780 billion, less than half of the IPO valuation.

There is a $990 billion gap between the two approaches. The calculation of this difference will determine whether this IPO becomes the largest tech company listing in history or a result of overheated pricing.

According to the Morningstar research report, the $780 billion figure is not a flat discount but is divided into two parts. The core business (rocket launches plus Starlink satellite internet) has a DCF valuation of $611 billion. The AI business (xAI computing power plus SpaceX's own orbital data center plan) is valued at $170 billion based on scenario-weighted probabilities. The sum of these two parts amounts to $780 billion.

The entire gap lies in the valuation multiples of the AI business. The IPO pricing valued the entire company at $1.77 trillion. After deducting the core business's $611 billion, the market assigned $1.16 trillion to the AI business, at a multiple of 6.8 times given by Morningstar. The $990 billion difference essentially represents the premium the market is willing to pay for SpaceX's AI narrative.

Morningstar provides two specific reasons for the discount. Firstly, the future feasibility and profitability of the AI business have not been validated. xAI was valued at $965 billion just in May, but the prospectus disclosed an estimated $6.4 billion operating loss and $3.2 billion in revenue by 2025, with the orbital data center not planned to be deployed until 2028. Valuing a cash-flow-negative business in the trillion-dollar range is the biggest discrepancy between the IPO valuation and the DCF valuation. Secondly, governance risks, with Elon Musk holding 85.1% of the voting rights and xAI acquisition terms, were singled out by Morningstar as significant uncertainties.

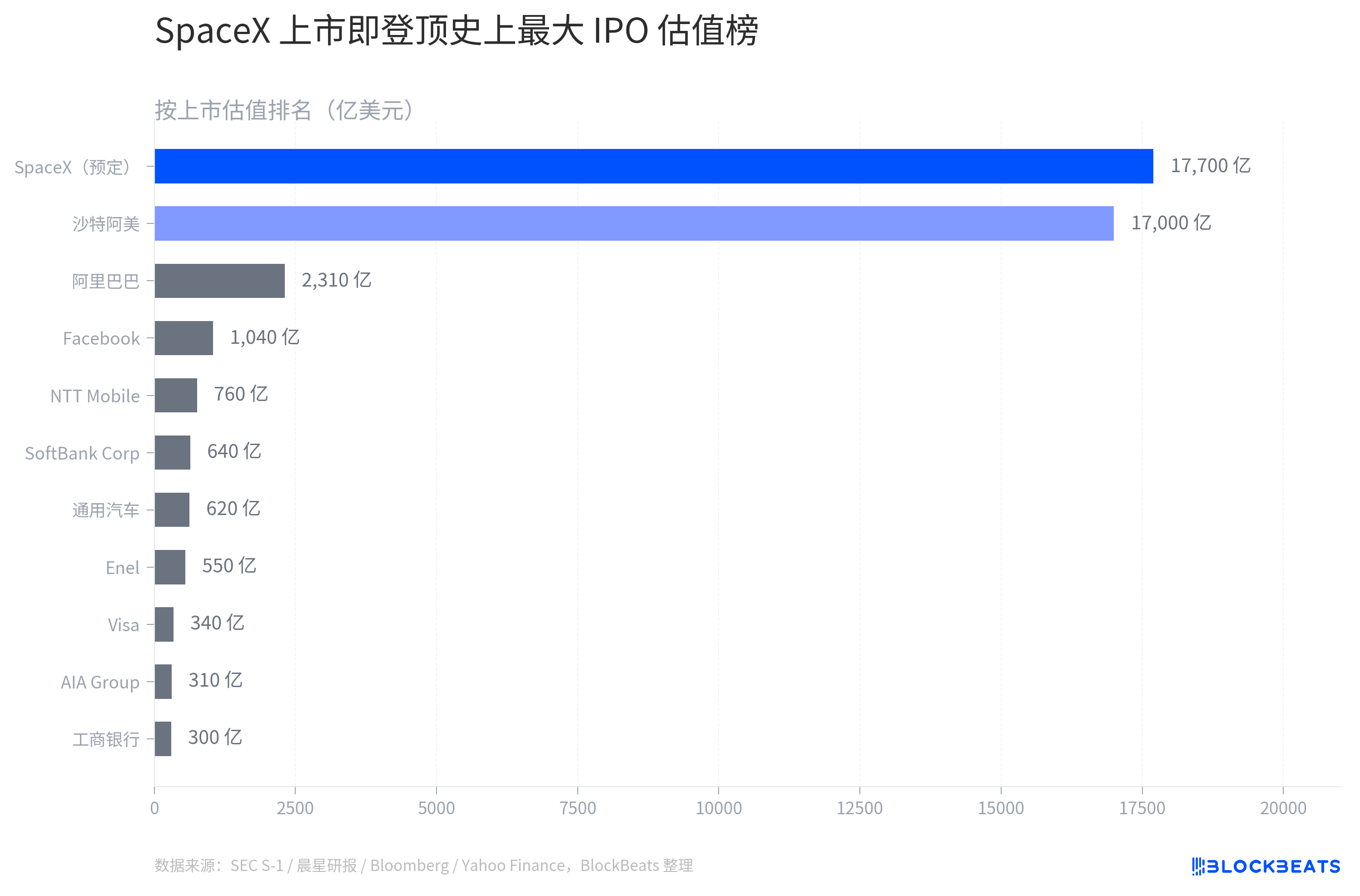

Placing SpaceX on the all-time largest IPO list provides a clearer picture. Prior to SpaceX, the world's largest IPO by valuation was Saudi Aramco, which debuted in 2019 with a valuation of $1.7 trillion, holding the top spot on this list to date.

SpaceX is valued at $1.77 trillion, $700 billion higher than Saudi Aramco. However, these two companies are not highly comparable. Saudi Aramco holds the world's largest crude oil reserves and was already a stable, profitable resource giant at the time of its 2019 IPO. SpaceX is still burning cash, with a $2.6 billion operating loss projected for 2025 on a consolidated basis.

Even more noteworthy is Alibaba, ranked second on the list. Alibaba, with a $231 billion valuation at its 2014 IPO, accounts for 13% of SpaceX's $1.77 trillion valuation. In the past 20 years, aside from Saudi Aramco, no IPO has come close to SpaceX in terms of scale. SpaceX's listing immediately placed it in the market cap range of trillion-dollar club companies like Apple, Nvidia, and Microsoft, all of which took decades of public market operations to reach this level.

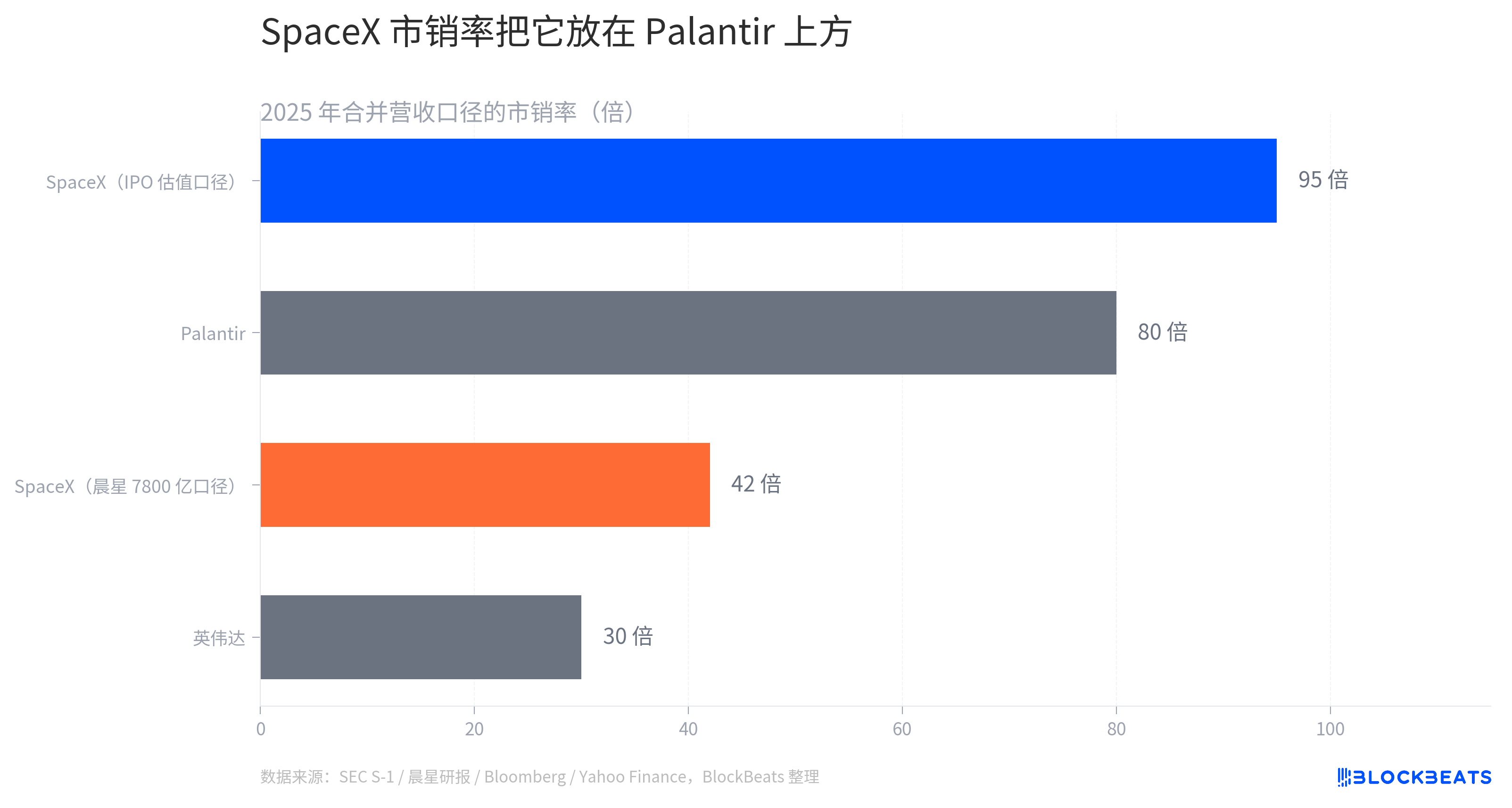

A more telling measure of the valuation controversy is the price-to-sales ratio (the ratio of market cap to revenue). SpaceX's $1.77 trillion valuation divided by projected 2025 consolidated revenue of $18.7 billion results in a price-to-sales ratio of approximately 95x.

During the peak of the AI boom, Nvidia had a price-to-sales ratio of around 30x. Palantir, as an "extreme example of an AI concept stock," had a ratio of about 80x. SpaceX's IPO pricing directly tripled Nvidia's price-to-sales ratio at its peak, surpassing Palantir by a significant margin.

Based on Morningstar's $780 billion estimate, SpaceX's price-to-sales ratio is also 42x, still higher than Nvidia's. Even with the most conservative valuation, SpaceX's pricing remains steep. Between the $1.77 trillion and $780 billion figures, there is no "reasonable" range, only a distinction between "expensive" and "very expensive."

Finally, it is worth dissecting SpaceX's issuance method itself. In a conventional large IPO, the offering price is announced in a price range, such as "$110 to $150 per share," and then adjusted during the roadshow based on feedback from institutional investors. This mechanism, called bookbuilding, is a price discovery tool that Wall Street investment banks have used for decades.

SpaceX skipped this step. By amending its S-1 to directly disclose a single fixed price of $135, without a range, SpaceX indicated that it did not need the market to indicate demand strength; it already knew. In other words, it chose not to let the investment bank adjust this number.

Fixed-price IPOs have been extremely rare in the past 20 years. The Saudi Aramco IPO used a similar method for part of the offering, and a few Chinese state-owned enterprises have also done so. This approach sends two signals: absolute confidence in demand, believing that even at a fixed price, it will be oversubscribed, and a deliberate squeeze on Wall Street's pricing power. In the regular bookbuilding process, banks reserve bargaining space for institutional clients through price adjustments, ultimately lowering the offering price to create a price jump on the first day. SpaceX's fixed price prevented this mechanism from operating.

A small incident in San Francisco served as a footnote to this IPO. In the same week, a 1907-built old house in San Francisco's Duboce Triangle was listed for $2.995 million, with the homeowner stating that they would accept stock options from OpenAI or Anthropic employees as a form of payment. The listing received a significant amount of responses within 24 hours.

This is not an isolated case. In April, an investment banker listed an estate in Marin County, also specifying that they would accept Anthropic shares. Thousands of AI company employees in the Bay Area hold paper stock worth millions of dollars, but selling is restricted and they are cash-poor. As SpaceX pushed the valuation of private tech companies to $1.77 trillion, with OpenAI and Anthropic valued at $852 billion and $965 billion respectively, private tech equity is becoming a true alternative currency.

The high pricing is not the only thing that can be dissected in this IPO. It is simultaneously redefining what counts as currency, what counts as an asset, and how much say Wall Street still has in pricing tech companies.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia