NVIDIA early investor Gavin Baker's investment philosophy: Long AI Infrastructure Bottlenecks, Short Overall Market Risk

Original Video Title: What The Best AI Investors Are Buying Right Now

Original Video Source: Limitless Podcast

Original Text Translation: Deep Tide TechFlow

Editor's Note

This podcast mainly discusses the investment philosophy of Gavin Baker, the founder of Atreides Management and a long-term supporter of Nvidia and Cerebras.

His core thesis is that AI is not a bubble but rather part of a infrastructure supercycle being driven by power, chips, and computing power; true alpha lies not in big models or chatbots, but in GPU connections, memory, inference chips, advanced processes, and power supply — the "sell shovels" segments.

Gavin Baker hedges against overall market pullback through QQQ puts while concentrating his bets on AI physical bottleneck assets such as Astera Labs, Unity, Micron, Nvidia, Cerebras, and Positron.

He shifts the "AI bubble" debate from an emotional level to supply-demand constraints, believing that as long as TSMC, ASML, high-bandwidth memory, and the power grid cannot quickly create oversupply, AI capital spending may not necessarily lead to a rerun of the 2000 Internet bubble.

Key Quotes

AI Bubble or Supercycle

· "AI is not in a bubble; on the contrary, it is in a supercycle."

· "The greatest returns are not in SaaS, not in chatbots like OpenAI or Anthropic, but in power, computing power, and chip manufacturing."

· "This is not like the Internet bubble, as the buyers are primarily the world's smartest and strongest cash-flow companies, not leveraging debt to buy computing power."

· "If the entire market cannot be oversupplied, then it is unlikely to suddenly collapse like a traditional bubble."

The Real Bottleneck: Power, Chips, Token

· "Gavin's theory is simple; focusing only on the bottleneck at the AI infrastructure layer, whoever can increase performance per watt and reduce token costs has value."

· 「AI labs are increasingly concerned with one thing: how many tokens can be generated per watt of electricity.」

· 「Electricity and wafers are two brick walls and also key constraints that prevent AI from accelerating too rapidly.」

Shifting from Pre-Training to Inference and Post-Training

· 「Completing model pre-training does not mean it's a genius forever; it still needs to absorb new information during the post-training phase.」

· 「Inference fundamentally requires significant computation, which is why inference chips and infrastructure will be a focus in the next phase.」

· 「The cost or revenue opportunity from inference alone may be 5 to 10 times the AI training power input.」

Vertical Tiny Models, Edge Models, and Sovereign Infrastructure

· 「In the future, you may not need to interact with Claude every day; what you might really need is a personalized AI agent trained on your own data.」

· 「Infrastructure deployment speed itself is a moat; the iterative speed of the digital world is much faster than the speed of physical infrastructure construction.」

「Whoever can compress what takes months or years to deploy physically into weeks can command a high price in AI infrastructure.」

Gavin's Investment Strategy: Long Bottlenecks, Short Overall Market Risk

· 「He strongly believes that AI winners will emerge, but that doesn't mean he's optimistic about the entire market; QQQ puts are his hedge against overall downside risk.」

· 「TSMC actually limits the speed of foam acceleration; as long as chip capacity cannot expand instantaneously, capital expenditure is not easily out of control.」

· 「Gavin is like a more mature, stable, and record-carrying Leopold: the former's success is measured in decades, while the latter's is currently more quarterly.」

Assets Worth Betting on in the AI Supercycle

EJ: Gavin Baker is an extremely prolific AI investor whom the general public has rarely heard of. Over the past 20 years, he has been investing in some AI companies that later became well-known before they took off. He made early bets on companies like Nvidia (a provider of AI GPUs and acceleration computing cores) and Cerebras (an AI chip company). He has a very clear view that AI is not a bubble; on the contrary, it is a supercycle.

He believes that by focusing on watts (power), wafers, and tokens (units of compute), the underlying infrastructure of AI, one can identify key bottlenecks and constraints. His conclusion is straightforward: the greatest returns in AI come from power, energy, and silicon manufacturing, not so much from SaaS (Software as a Service) or chatbots like Anthropic and OpenAI.

The entire industry will ultimately cascade downstream to semiconductors, the picks and shovels supporting the entire AI sector.

While many have called the AI industry a bubble, he sees it as a once-in-a-generation buying opportunity, especially in AI infrastructure. He expresses this thesis in his fund with a scale of around $41.4 billion.

If you hear him talk about these constraints, particularly in AI infrastructure, you will find this theory very familiar. We have previously discussed an investor, Leopold Aschenbrenner, on the show who has made many similar allocations. The difference is that Leopold has only been at it for about 3 years, while Gavin has been in the game for over 20 years.

Leopold manages assets roughly three times the size of Gavin's, but the show's producer Luke once offered a great reminder: you might be able to outperform Warren Buffett in a year, but can you outperform him consistently for decades? Gavin Baker's track record suggests that he may have a different view on this investment theory.

For those unfamiliar with Gavin Baker, it is worth noting that he is the founder of Atreides Management, an investment fund that has been invested in Nvidia for the past 20 years. Being able to hold Nvidia for 20 years and still be functioning is remarkable in itself because it should have produced outstanding returns.

Some of his recent victories include Cerebras and Astera Labs (an AI data center connectivity chip company). Cerebras is an AI chip company mentioned on the show that saw a staggering valuation post IPO. There are a few companies you may not have heard of that we will explore in this episode based on his portfolio and analysis to see where he believes the AI investment opportunities lie.

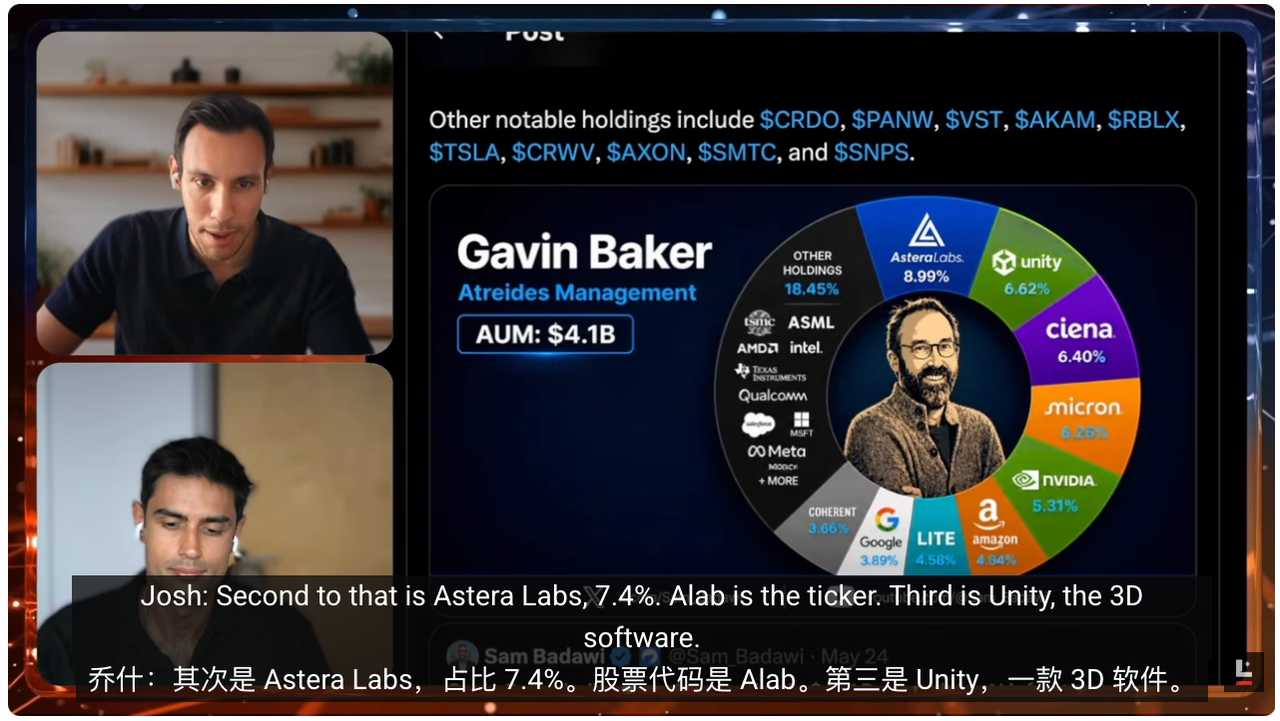

So the question becomes, what has he actually invested in and why? Looking at Atreides Management's recent 13F (a quarterly filing required to be submitted by institutional investment managers in the U.S.), this fund has approximately $4 billion AUM (Assets Under Management). Examining some of its largest holdings reveals that these companies all point to the AI development bottlenecks that Gavin has repeatedly mentioned.

He has a significant position in some not-so-sexy, many unheard-of companies. For example, Astera Labs, which almost accounts for 9% to 10% of the fund. You can think of Astera Labs as the interconnect layer between GPUs.

If you imagine the data center as a system, GPUs are the engines responsible for pre-training, post-training, and inference of models. However, for GPUs to work, they need to transfer a large amount of data between each other and access memory chips where the data is stored.

To achieve this, a "pipeline system" is required. I'm speaking at a high level here because I'm not pretending to understand all the underlying details. Astera Labs addresses precisely this issue. When AI clusters expand to hundreds of thousands of chips, the bottleneck is no longer just the GPU itself but the data transfer window—how to send the right data at the right time and access the correct data. Astera Labs has built such a pipeline system.

I hadn't heard of Astera Labs before researching for this episode. But I remember a similar situation with Cerebras. Gavin talked about Cerebras about six months ago, and considering the timescale of AI, six months is a long time. Then Cerebras went public, with the show mentioning an estimated valuation of around $60 billion, which increased by 40% after the IPO. This indicates that Astera Labs could also be a significant name in a similar trend.

Josh: Cerebras was one of his very early investments. He entered Cerebras in the very early stages of the company's lifecycle, which means he has been betting on this theory for many years. Several other companies are also long-term bets for him, with the most flagship, of course, being Nvidia.

Being involved with Nvidia for over 20 years and maintaining conviction all the way is quite impressive. I recently listened to two podcasts where Gavin clearly expressed a judgment when talking about the Nvidia position. He believes that Nvidia can continue to maintain its current profit margin and demand. This means he thinks Nvidia has the opportunity to approach a nearly $10 trillion market cap, as it is currently only about halfway there.

Another noteworthy mention is Micron, one of the world's major memory makers. In the previous episode, we discussed the AI investment stack and the positions of these companies in it, and I highly recommend everyone to go back and watch. Micron is one of the largest memory makers.

The show mentioned a staggering number: a year ago, its market cap was less than $100 billion, but at the time of recording, it had surpassed a $1 trillion market cap, a 10x increase in a year. This illustrates how crucial the memory problem is.

There are also some less prominent but very interesting companies. EJ, I particularly want to highlight one for you: Unity Software. Those familiar with games know Unity; it's a game engine, and many popular games are created using this 3D rendering software.

So why would an AI investor invest in Unity, this "thing for making video games"? The answer lies in the 3D game engine. Unity is a world model builder; it has a deep understanding of physics, world dynamics, materials, and lighting.

When AI companies are looking to build AGI (Artificial General Intelligence) and humanoid robots, a crucial step is to simulate a virtual environment and a virtual dataset for the robots to train within. Unity happens to be one of the most powerful tools for this.

So as a firm believer in world models, you should appreciate this example: a company known for its game engine has a clear path to becoming a key player in the AI world.

Gavin's Investment Theory and Strategy

EJ: The theory of world models is quite simple: current AI models or LLMs (Large Language Models) mainly understand the world through text and books, like a student sitting in a library, but they lack real-world experience.

What the world model aims to unlock is this: putting a game character in a simulated environment to help it understand how the physical world operates.

For example, if I drop a phone or kick a ball, what will happen? What are the subsequent steps? How should you react? The world model addresses this question.

Currently, there are not many players who can scale this kind of capability. The current frontrunner might be Google, with models like Genie 3 (Google's Generative Interactive Environment model project). The show also mentioned Google's recent release of Gemini Omni, but these models have not yet had their own ChatGPT moment.

What I like about Gavin is that his portfolio is very much like a barbell strategy. On one end, it's very traditional, where everyone needs GPUs and storage, so he invested in major players like Micron and Nvidia. On the other end, it's very forward-thinking. He believes that the puck will go there, so he invested in Cerebras because he thinks inference will be very important. He also invested in Unity because he believes the world model will be the future way to train robots and the next generation of LLM.

In his portfolio, he also has Positron, which focuses on inference chips. If this sounds similar to Cerebras, yes, they both revolve around inference. In a recent interview, Gavin repeatedly talked about a trend, the AI model's infrastructure stack, especially the training stack, is shifting from pre-training to a greater focus on post-training.

If you're in the AI circle, you would know that this shift has already happened. Gavin is very focused on this. A model still needs to understand new information, new data, and update itself. Just because it completed pre-training on a dataset doesn't mean it's a genius for life. It still needs to learn new information, which happens in the post-training layer, and this requires a lot of computation.

Secondly, if you need an AI model to truly think about a problem, just like how we think after receiving new information, does this perspective hold? Is there another theory that can explain it? This is reasoning. Reasoning also requires a lot of computation. The current estimate is that the cost or revenue opportunity from reasoning alone may be 5 to 10 times the compute investment in pre-training.

So AI labs and chip makers are undergoing a significant shift. You've already seen Nvidia rolling out many GPUs aimed at inference to support agentic applications. Gavin has also expressed his bet on inference through a series of investments.

One last point that I find very interesting is Gavin's discussion on China. In the AI competition, the narrative has always been China versus the US. China has a unique setup where it has relatively abundant energy and the ability to expand chip manufacturing. The US is currently struggling in this area, which is why many aspects are outsourced to TSMC in China's Taiwan.

His explanation is that China has a unique opportunity to create a very different AI infrastructure or chip from the US because they will be heavily focused on inference. You could say that Gavin is leading the way in betting on the establishment of US inference infrastructure through his investments in the US. I think this could be a huge opportunity in the future.

Josh: It is worth noting that this bet is not all about the upside. He also holds a significant amount of QQQ puts (puts on the Nasdaq 100 ETF). QQQ is an ETF tracking the Nasdaq 100, a basket of stocks and the second largest ETF by trading volume in the U.S. It has performed very well: up 55% in 2023, 25% in 2024, 20% in 2025, and 17% YTD in 2026.

In other words, QQQ, as an index fund, has performed exceptionally well. Buying it is easy as it represents a basket of the top 100 stocks. However, Gavin is using it for a reverse hedge. He is not saying AI won't win but rather that he is investing in the key creators addressing bottlenecks, while not being overly optimistic about the overall market sentiment.

QQQ put serves as downside protection: if the overall market crashes in an unfavorable way, even if AI continues to succeed long-term, he has this hedge.

Four Categories of Investment-Worthy Directions

Josh: We can break down what he considers the most critical investment bottlenecks into several categories. The first category is verticalized small language models.

Standard LLMs, like chatbots such as Claude and ChatGPT, are generalized LLMs with a broad understanding of the world and can answer specific questions. However, training models around a specific vertical domain or specific issue is another thing.

These specific issues usually exist within enterprises, especially those deeply focused on a particular problem or companies that have carved out a niche in a certain segment. Verticalized SLMs address precisely this issue: they are frontier models but highly optimized to run efficiently on specific enterprise data or run locally on devices.

We have discussed on-device or locally run models before. The reason is that there is a lot of highly personalized data on your phone or other devices that you may not want to share, and companies may not be able to access. For example, medical records, financial details.

I saw that OpenAI released a financial AI agent that can access your bank account but cannot actually carry out transactions on your behalf due to the presence of a lot of personally identifiable information, such as social security numbers and bank details.

Local models or SLMs can address such issues. Gavin largely bets that they will become very important in the future. There is a company he is very bullish on: Apple. Although he may not have expressed explicit investment interest, he believes Apple will be one of the key device makers to run local models on their devices.

If the future unfolds this way, we may no longer think that Claude must be the model you interact with every day. What you might need is a personalized AI agent trained on your own data, which is what SLMs might ultimately evolve into.

The general version can run on your phone, and many companies will also run highly optimized, specialized models trained on their proprietary data to better sell or market products.

EJ: Apple is in a great position for this. I'm looking forward to WWDC (Apple Worldwide Developers Conference); it's coming up soon.

Josh: Yes.

EJ: We're just a few weeks away from the Apple Developer Conference, where they will release new AI software and how this software integrates with hardware. This will be very important, and we will continue to cover it. I am excited to discuss this.

Josh: The second pillar is sovereign infrastructure. We often talk about how the speed of bits is far faster than the speed of atoms. Looking at AI infrastructure makes it very clear: model quality has almost exponentially improved, the intelligence generated per watt, the intelligence per token, will only continue to rise.

But the physical deployment speed has not increased at a similar pace, and this in itself is a moat. Hardware is extremely complex, transistor accuracy is approaching the atomic level; to deploy at scale in a world already under pressure from existing infrastructure is not easy. With the popularization of electric vehicles, the power grid is already under greater strain, approaching full capacity in many places. Now AI is bringing about energy and chip problems.

Gavin made a strong bet on one fact: infrastructure is hard, it takes many days, many months, or even many years to build. His bet is on those who can compress this cycle into weeks. Therefore, the speed of physical deployment is a moat in itself. He is narrowing the target and looking for companies that can deploy quickly.

The first example that comes to my mind is SpaceX, Elon Musk's aerospace company, and their speed in building Colossus (a large AI supercomputing cluster) and leasing it to Anthropic, with potential future leases to other companies. This infrastructure backbone is one of Gavin's key focuses.

Looking at Leopold's portfolio, this is also a core part. The reality is: building things is very hard, and those who can build things can sell them at a very high price. The show mentioned that SpaceX's largest source of revenue now comes from leasing data centers, not rockets. This highlights how important this pillar is.

EJ: He cares about speed, but he also cares about cost. He repeatedly mentions a metric: performance per watt, which is how much performance you get per watt. What he really means is that AI labs are increasingly concerned with how many tokens can be generated per watt.

If you think about it, this year only about five companies spent billions or even trillions of dollars on GPUs, compute, and the power to drive these systems. You definitely want a high bang for your buck, especially when hyperscalers reach this scale, cost is a critical issue.

For instance: if I ask Claude a question and it costs me 2 cents for an answer, and I ask ChatGPT a question and it costs me $1 for an answer. Even if Claude is only 95% as smart as ChatGPT, I would most likely go with Claude. Because I can ask more times and ultimately get the answer at a lower cost.

So, the cost of accessing this kind of intelligence is crucial. Just this week, Microsoft and Uber announced that they are actually reducing the use of Claude Code (Anthropic's AI coding tool for programming scenarios) because the annual budget ran out in about 4 months.

You can see this in Gavin's investment portfolio: Cerebras, Positron, Astera Labs. He identifies very niche infrastructure bottlenecks and then makes a simple bet: if this company solves this bottleneck, achieves a certain level of performance per watt, and lowers token costs to a certain level, AI labs will buy more GPUs, more products, or more of these types of things.

So, his theory is actually quite simple, despite the specific technology being very complex: I am only focusing on the AI infrastructure bottleneck. If we can find a company that improves performance per watt and makes tokens cheaper, I will bet that its future value will be very high, either through an IPO or a high-priced acquisition.

Josh: In this part, if someone wants to replicate Gavin's transaction, they need to know a few names: Astera Labs, Cerebras, SiFive (a RISC-V chip design company), and Positron. These four companies are very key in this sector.

The fourth and also the last direction is the combination of energy and space. As we mentioned earlier, the terrestrial grid largely restricts energy supply, and establishing new energy sources is very difficult. The program mentioned a statistic that about 40% of new data centers will face strong opposition, with people lobbying, protesting, not wanting these data centers to be established.

There are two types of solutions. One is to create out-of-the-box energy, which is portable energy. You can take the data center with you and power it with a small energy device. Blue Marble, which Leopold is very optimistic about, belongs to this category.

The other type is orbital compute, which is a direction Gavin is currently very focused on. The largest and most core company in this field is, of course, SpaceX. It is the only company capable of being the high-speed highway to space, sending payloads into orbit, sending racks and data centers into low orbit, and generating enough intelligence and power to transmit back.

I think the significance of SpaceX is greater than SpaceX itself. I am somewhat surprised that Gavin's portfolio does not have more space stocks allocation, considering he thinks this is a huge industry. Perhaps the reality is that it is still too early, and SpaceX is the linchpin unlocking this industry.

Next, you have to closely watch the Starship V3 launch. We just saw a Starship launch last week, and it performed well. If the Starship cannot operate properly, there will be no space energy, and there will be no racks to orbit. It is a necessary condition because the payload to be launched is very large. So, SpaceX is definitely a company that must be watched, although there will be many second-order companies affected.

Why Is This Not Just Another Internet Bubble?

Josh: Next, everyone will surely ask, why is this not just another dot-com bubble? Gavin has been asked this question many times, and he has given a very strong answer, which I mostly believe in. His argument is very persuasive.

His logic is roughly this: the 2000 internet bubble was debt-fueled. Many people borrowed a large amount of money to invest in unverified theories and products that nobody really used or cared about.

If we compare it to the AI supercycle that Gavin mentioned, just OpenAI and Anthropic alone are expected to reach $200 billion in ARR (Annual Recurring Revenue) this year. And this is not imaginary money; it has already been contracted, with a significant portion, as mentioned in the show, 40% to 60%, pre-paid by enterprise and retail customers.

In other words, real money is flowing.

Now, looking at GPU compute power, if we ignore the model labs and look at who is buying from Nvidia – Google, Microsoft, Amazon, and Meta – they are all using their own cash reserves to pay, without borrowing. Amazon has just tapped into its free cash flow, and if they start borrowing, then we can worry. But for now, the key point is that they are not leveraging.

Moreover, these are among the top five companies globally, in a sense, also some of the smartest companies because of their market cap, scale, and position. In contrast to the internet bubble, back then, many unknown companies raised a lot of money and then burned it in very unreasonable ways. In this cycle, it is the smartest companies globally that are spending without leverage.

In recent weeks, the quarterly reports we discussed on the show also indicate that profits are being optimized around these actions, the models are advancing and becoming smarter. So Gavin's core argument is: this is not an internet bubble because it is not leverage-driven; at the same time, the bottlenecks we are talking about are constrained by physical atoms.

Buying a bunch of memory chips and GPUs is one thing, but Nvidia cannot oversell GPUs, and Micron cannot oversell AI storage chips because they do not have enough chip manufacturing facilities. So his simple argument is: if you cannot oversupply the entire market, then it is not a bubble. We are limited by not having enough picks and shovels to get the job done, and he is investing in precisely those things.

There is also another good point: Gavin believes that if TSMC could supply, Nvidia could have sold $2 to $3 trillion worth of GPUs this year and next year. In other words, TSMC is a key link in the bubble.

The reason is, if TSMC could meet the demand of these companies and provide them with so many chips, it would consume a huge amount of funds. Looking at the chart now, there has not been a significant disconnect between CapEx (Capital Expenditure) and operating cash, as the cash generated by enterprises is still sufficient to support construction.

However, if TSMC were to tell Nvidia tomorrow that they could triple capacity overnight, Nvidia would not refuse; it would start spending massive amounts of money to buy chips. Other companies would also be forced to borrow money to buy these chips, at which point the CapEx bubble would begin to expand, creating a gap with enterprise operating cash flow.

But because there are constraints in every link—storage constraints, chip manufacturing constraints, energy constraints, especially TSMC's constraints on advanced chips—we actually cannot ramp up construction speed that quickly. Therefore, TSMC is hindering the acceleration of the bubble.

As long as TSMC's chip capacity remains limited, as long as Samsung and other chip manufacturers do not surpass their market share, the growth rate is relatively sustainable. It may seem fast, but there is still a lot of demand that cannot be met because we are simply not building fast enough. As long as this dynamic exists, I don't think there is a major issue for now.

EJ: Another point is, you cannot assume that demand remains static because it doesn't. AI-related demand is growing exponentially, and the growth rate exceeds the production supply of these chips.

The only two ways I can think of to falsify this theory are: First, someone miraculously replicates ASML (the global leader in extreme ultraviolet lithography machines), and suddenly a bunch of ASML competitors emerge. For those unfamiliar with ASML, they can understand it this way: ASML produces machines worth about $400 million, and TSMC and all major chip fabs need these machines.

The program mentioned that ASML has only one team manufacturing these things in Norway, and the lead time is very long, with the order backlog stretching to about 5 years.

Second, we create a completely different type of LLM that does not require as many GPUs or as much storage. But currently, we have not seen any signs of this happening.

Today I saw a piece of news about SK Hynix, a major global high-bandwidth memory supplier. It is the leading storage manufacturer and supplier for Nvidia GPUs, almost a top dog in the AI storage field.

It is currently receiving bids of around $50 to $100 billion from Google and Microsoft. Both companies are looking to secure future production supply for the next three years to fund the equipment needed for its expansion.

This shows how hungry these tech giants are for storage, and this is just a sub-track within the AI sector. SK Hynix, on the other hand, said, "I don't want to provide you with a supply guarantee; I'll just raise prices directly." Its operating margin is about 70%, which is almost unimaginable in the semiconductor industry.

So Gavin's all-in move makes sense. It doesn't look like a bubble, perhaps the market will react in the short term. We opened the stock portfolio before recording today, and almost everything was down, but that was more of a reactionary move.

The strategic goal of this matter is: we will only need more GPUs, more semiconductor chips, and the supply is insufficient, and so are the manufacturers.

Gavin's Investment Portfolio

Josh: The conclusion is: power and wafer. Just these two. They are two brick walls and two limiting factors that prevent us from accelerating too quickly. As long as power and wafer remain valuable, with strong demand and limited supply, there are good days ahead.

If you want the TLDR of Gavin's portfolio, I can go over his largest holdings. Once again, this is not investment advice. This is what Gavin holds, not what we hold. I don't know if these stocks will go up, down, or spin in place.

His largest position, a bit counterintuitive, is a QQQ put position (Nasdaq 100 ETF put option). Overall, he is somewhat bearish on the market, which is significant to note. The second largest is Astera Labs, with a position of about 7.4%, ticker ALAB. The third is Unity, the 3D software company.

Behind these, there are many more holdings: Ciena (optical networking equipment company), Micron, Nvidia, Amazon, Lumentum (optical communication and laser device company), Alphabet (Google's parent company), Coherent (photonics and materials company), Roblox (gaming platform), EchoStar (satellite communication company), Twilio (cloud communications platform), Wayfair (online furniture retailer). This person invests in everything.

If you are interested, you can go check out his 13F. This is Gavin's view, the bottleneck is in power and wafer. As long as these constraints exist, it's basically a one-way upward trend. EJ, how do you digest this information? How would you handle it?

EJ: Ever since Leopold's 13F came out, the market has been very volatile. As we record this episode, I am increasingly aware that Gavin is somewhat like a older, wiser Leopold. He has been in this industry for a long time. Maybe he doesn't have $13 billion AUM, but I feel he will still be around in 10 years.

If you hear this and think, I don't want to chase AI progress every minute, every hour, every day, I just want to put my money there and see how it grows over the next few months or years, then Gavin's portfolio might be very informative. Of course, this is not investment advice.

He is taking a more cautious, long-term, and future-oriented approach. If his trend judgment eventually materializes, just like his early bets on Nvidia and Cerebras, there may be exponential returns in the next few years. But all of this is built on one core belief of his: we are not in a bubble.

I am curious if the audience agrees. Obviously, most people will not be as technical or as deep down the stack as Gavin. But after listening to this episode, do you think we are in a bubble or not? What are the reasons for or against? Is there anything we missed? Josh, do you think it's a bubble now before we wrap up?

Josh: I think we are definitely in a bubble. The question is, at which stage of the bubble are we, and that can still be debated. Right now, it looks more like an early stage, so hopefully it will continue to maintain this state. According to Gavin, as long as TSMC continues to limit chip capacity, we should be fine.

That's the overall outlook. We've talked about Leopold, whose success is currently measured quarterly; now we talk about Gavin, whose success is measured over decades. Many people's own answers may fall somewhere in between.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia