Illustration of the Financial Report Secret Behind Dell's 38% Surge

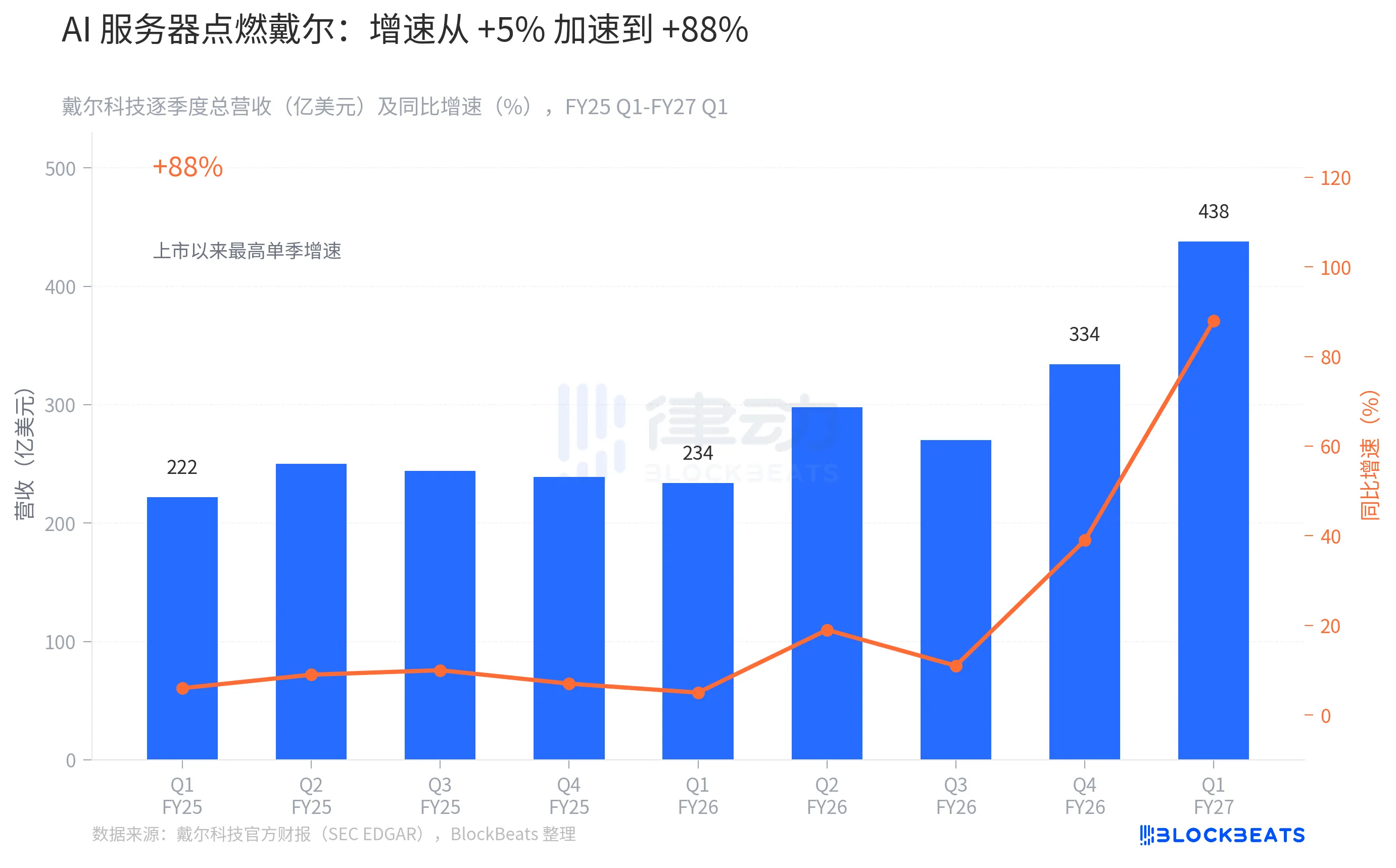

After-hours on May 28th, Dell Technologies announced its FY2027 Q1 performance. According to Dell's official financial report, the total revenue was $438.4 billion, an 88% year-over-year growth rate. This is the highest single-quarter growth rate for the company since going public, with the stock price surging more than 38% after hours.

In the previous quarter, Dell's revenue was $33.4 billion. This quarter, it reached $43.8 billion. The difference of $10.4 billion exceeds the annual revenue of Dell's entire AI server business two years ago. We break down this financial report with three charts to reveal the details that the spotlight missed.

88% Is Not an Accident, It's an Accelerating Curve

If we rewind to FY2025, Dell's growth rate was roughly between 6% and 10% at that time. For four quarters, the direction was consistent, and the magnitude was restrained. By FY2026 Q1, the growth rate even dropped to 5%.

Then the inflection point arrived. According to Dell's official report (SEC EDGAR), the growth rate in FY2026 Q2 jumped to 19%, fell to 11% in Q3, and accelerated again to 39% in Q4. In this year's Q1, it was 88%.

This growth curve was not a sudden spike in a quarter; it was a climb. The 39% in FY2026 Q4 was already a high number, but when compared to 88%, 39% seems like a plateau. Looking at the numbers from eight quarters together, the arrival of 88% was not accidental; it was a curve with a continuously steepening slope reaching its latest position.

It is worth noting the decline in FY2026 Q3. At that time, revenue dropped from $29.8 billion in Q2 to $27 billion, and the growth rate retreated from 19% to 11%. The market was once worried that this was a sign of growth peaking. In hindsight, it seemed more like a brief misalignment in the supply chain, with large orders of AI servers accumulating in Q3 and being confirmed en masse in Q4 and FY2027 Q1. FY2026 ended with a total of $113.5 billion, a 19% year-on-year increase.

The momentum for the four quarters of acceleration came from one place: AI servers.

Only AI Servers Are Truly Soaring

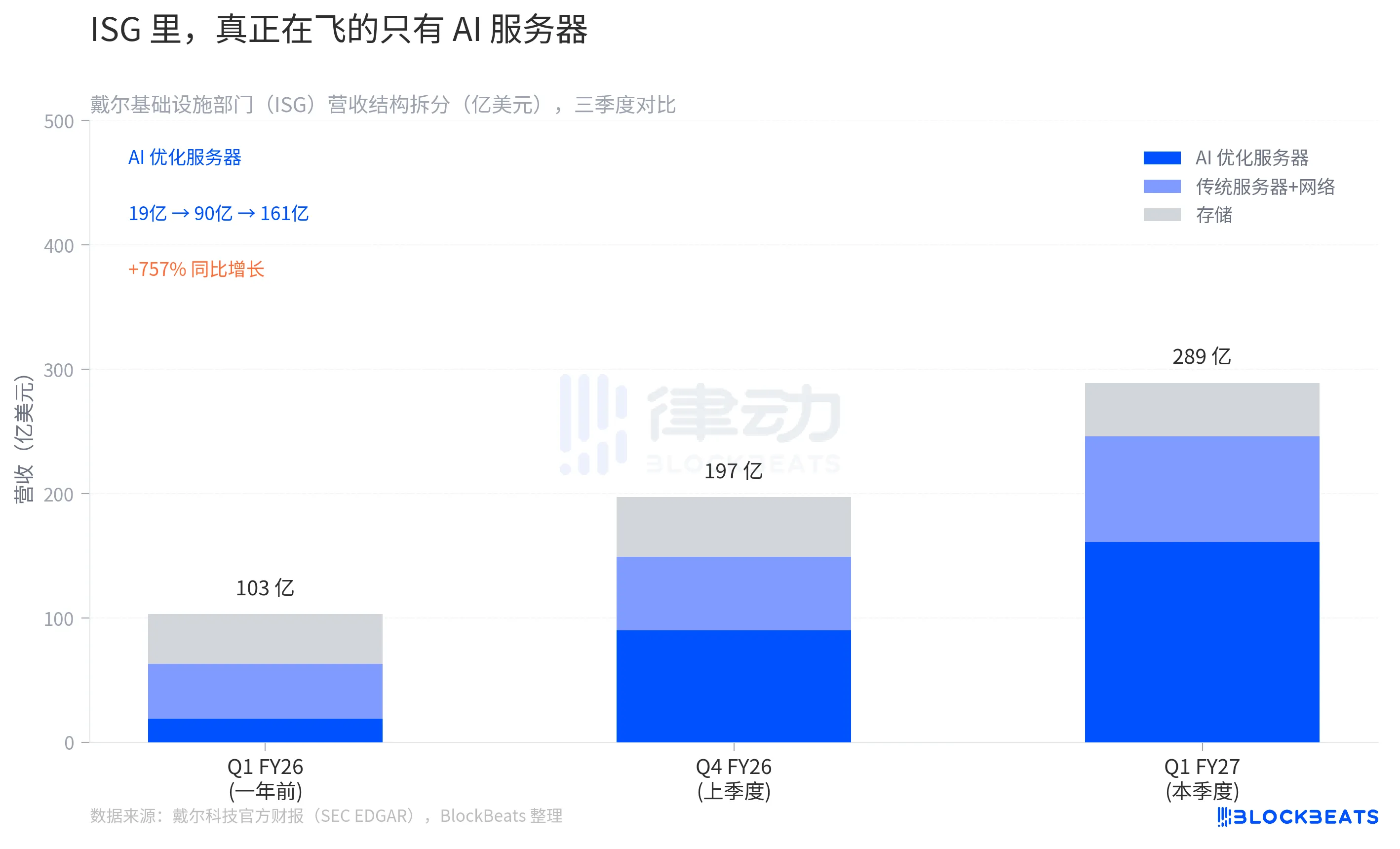

Dell's revenue is divided into two segments: ISG (Infrastructure Solutions Group) and CSG (Client Solutions Group, including PCs and peripherals). According to Dell's official report, ISG's quarterly revenue this quarter was $29 billion, accounting for 66% of total revenue, with a 181% year-over-year growth rate. CSG revenue was $14.6 billion, with a stable 17% year-on-year growth.

The $29 billion from ISG is a total number. What is truly worth dissecting is its internal structure.

According to Dell's segment data filed with the SEC EDGAR, in the FY2026 Q1 from a year ago, ISG's three sub-segments were: AI-Optimized Servers at $1.9 billion, Traditional Servers and Networking at $4.4 billion, and Storage at $4 billion, totaling $10.3 billion. By FY2026 Q4 (the previous quarter), AI server revenue surged to $9 billion, traditional servers to $5.9 billion, and storage to $4.8 billion, totaling $19.7 billion.

In Q1 of this year, according to Dell's financial report, AI-Optimized Servers were at $16.1 billion, showing a 757% year-on-year growth rate. Traditional Servers and Networking reached $8.5 billion, and Storage $4.3 billion.

Three lines, each with a completely different trend. Storage essentially stood still, inching up from $4 billion to $4.3 billion over three quarters, a change within the margin of error. Traditional servers are growing, but the magnitude is not as striking in comparison to the whole. The AI servers resemble a nearly vertical pillar, climbing from $1.9 billion to $9 billion, and then from $9 billion to $16.1 billion, with each step being almost twice the previous.

Looking at it from another angle: a year ago in FY2026 Q1, AI servers accounted for only 18.4% of ISG, while traditional servers and storage together made up 81.6%. In this year's Q1, AI servers represent 55.6% of ISG's total revenue. In other words, Dell's Infrastructure Solutions Group underwent a structural transformation in revenue over the year, with AI servers shifting from a supporting role to the absolute key player.

During the earnings call, Dell COO Jeff Clarke mentioned that the composition of AI customers includes new cloud players (neocloud), sovereign AI buyers, and enterprise clients. This distribution indicates that the demand for AI servers comes from multiple directions, not relying solely on a single type of buyer's cycle.

The $29.1 billion ISG expansion, the main drive came from this one sub-segment.

Dell CFO David Kennedy revealed another figure during the earnings call: $24.4 billion in new orders for AI servers this quarter, with a current backlog of $51.3 billion. Dell has also raised its full-year AI server revenue guidance from around $24.6 billion to about $60 billion, a 144% increase.

Analysts Never Expected This Magnitude

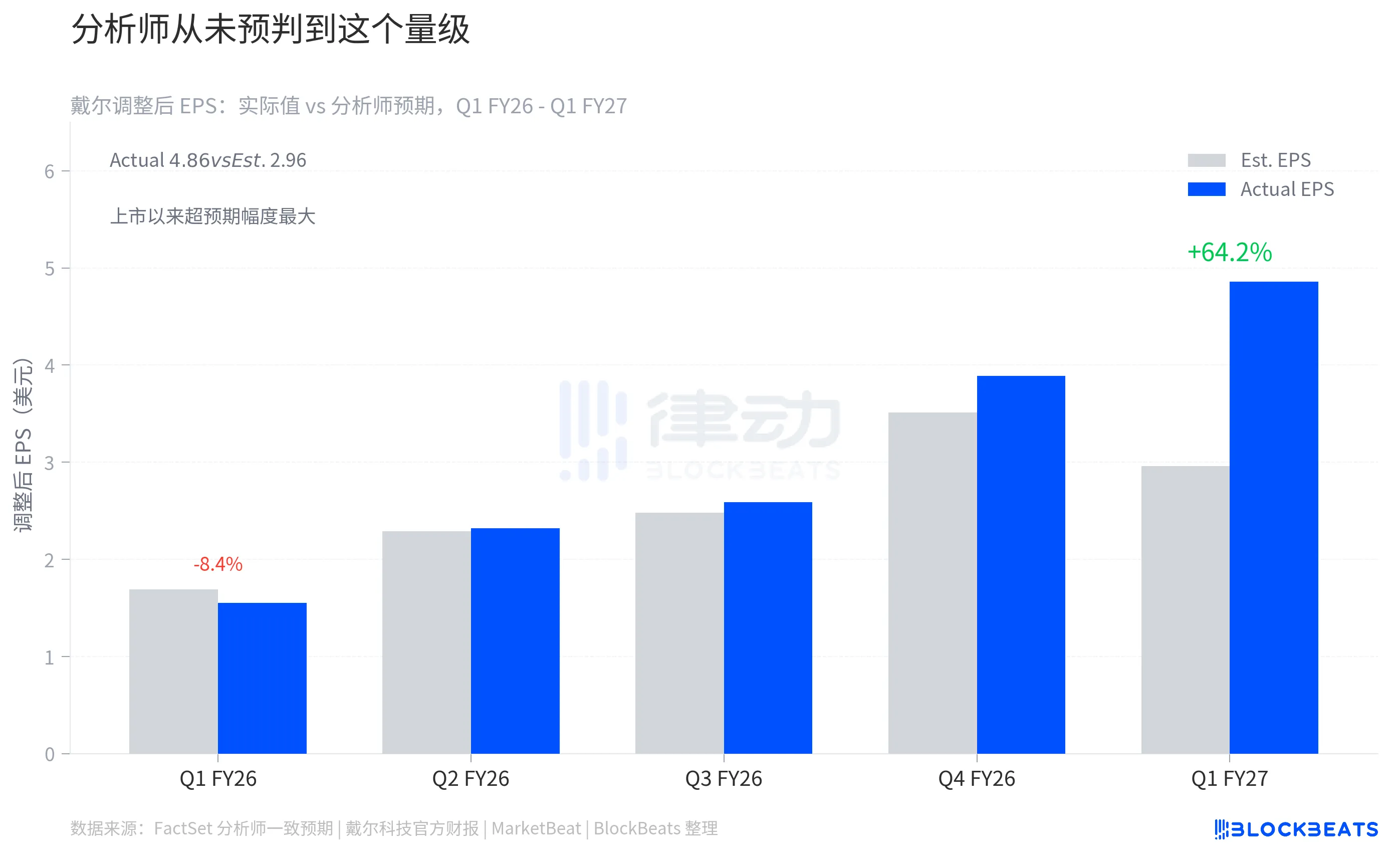

Adjusted Earnings Per Share (adj. EPS) is the key metric analysts use to measure a company's profitability. This chart shows Dell's deviation from analysts' consensus expectations for adj. EPS over the past five quarters.

According to analyst expectation data compiled by MarketBeat, the FY2026 Q1 actual value was $1.55, with analysts expecting around $1.69, a slight miss at -8.4%. This was one of the few misses for Dell in the past few years. The following three quarters showed a gradual recovery: Q2 beat 1.1%, Q3 beat 4.5%, Q4 beat 10.8%.

In FY2027 Q1, according to Dell's official financial report, the actual adj. EPS was $4.86. According to FactSet's compiled analyst consensus, the expected value was $2.96. The actual value exceeded expectations by $1.90, a deviation of +64.2%.

64.2% is a significant number. The highest beat in the past four quarters was 10.8%, making this quarter almost 6 times that. According to the analysis firm Benzinga, this is the largest single-quarter EPS beat for Dell since its IPO.

The source of the beat is not hard to understand: the demand for AI servers surged in this quarter, but analysts' models were still based on relatively smooth growth assumptions. A backlog of $51.3 billion in AI orders at quarter-end was not factored into any previous analyst forecasts.

A notable point of comparison is the change in profit margins. According to Dell's financial statement, this quarter's ISG operating margin was 10.5%, up from 9.7% a year ago, indicating that the large-scale shipment of AI servers did not significantly drag down the gross margin. AI servers are usually considered to have thin profit margins because most costs come from NVIDIA GPUs, with Dell mainly focusing on system integration and delivery.

However, the 10.5% ISG margin is still reasonable compared to historical levels. Dell's CFO attributed this on the earnings call to "strong sales, supply chain, and pricing execution." This quarter's adjusted operating profit totaled $4.235 billion, nearly 70% higher than the approximately $2.5 billion expected by FactSet.

At the same time, Dell raised its FY2027 full-year GAAP diluted EPS midpoint from $17.31 per share in February to $17.90 per share for non-GAAP diluted EPS, while analysts had previously expected around $13.16. The full-year revenue guidance range was adjusted to $165 billion to $169 billion, up from the initial range of $138 billion to $142 billion in February, with the midpoint raised by around $27 billion, close to a 20% increase.

Full-Year AI Server Backlog at $51.3 Billion. This is the floor, not the ceiling, for revenue in the next quarter and beyond.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia