A 39-Fold Surge in One Year, Can the U.S. Stock Storage Sector Still Be Bought?

The S&P 500 has risen by 28% in the past 12 months, while Nvidia has surged by 73%. However, compared to the storage sector, these gains pale in comparison. A year ago, SanDisk was at $34.61, and today it is at $1,406.32, a staggering 39x increase.

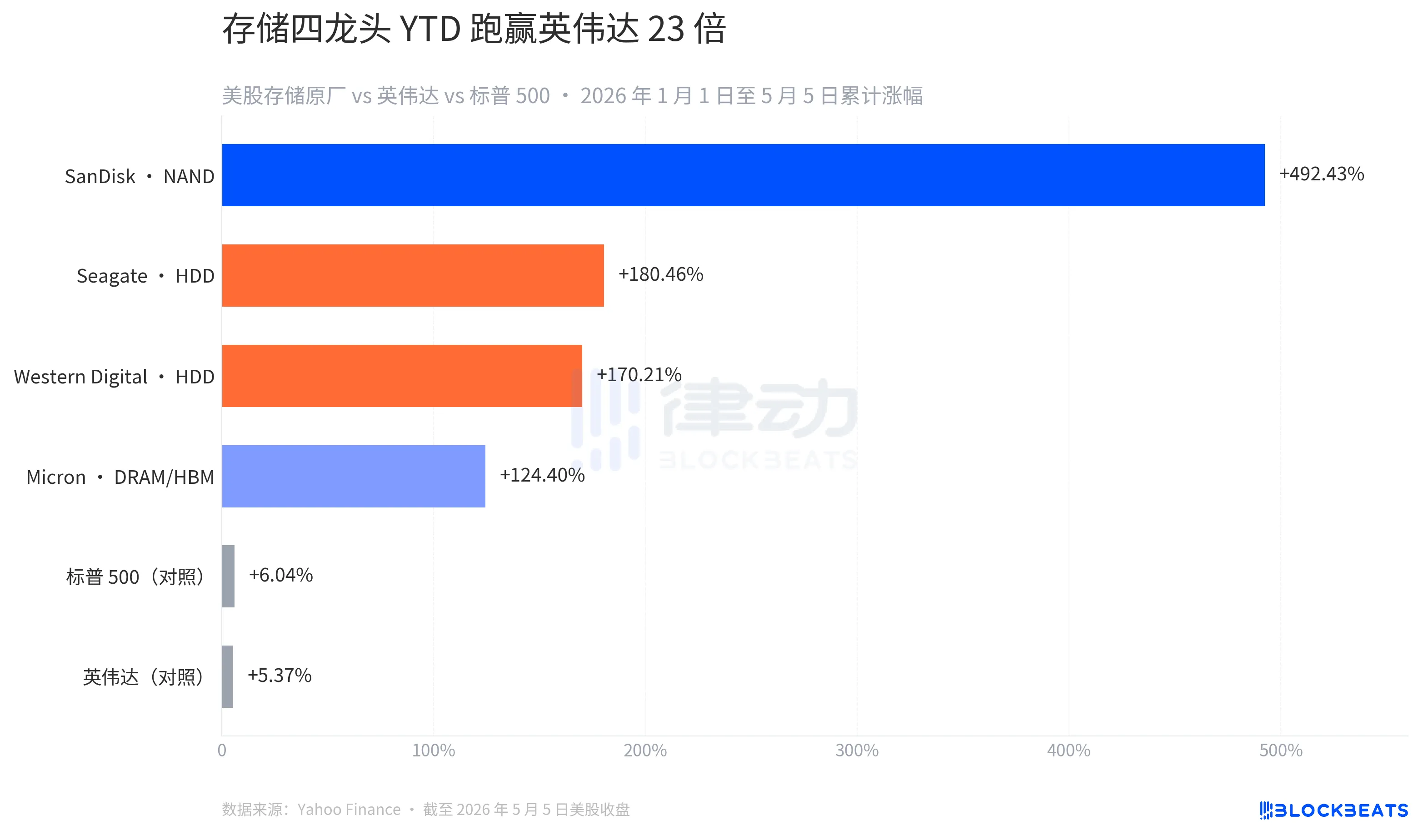

This NAND flash memory factory, spun off from Western Digital just 14.5 months ago, is the best-performing stock in the U.S. stock market year-to-date in 2026, skyrocketing by 492% within the year. Behind it, Micron, Seagate, and Western Digital, the four U.S. storage OEMs, have seen their YTD gains range from 124% to 492%, with the lowest performer outperforming Nvidia by 23x. The "shovel seller" label of the AI revolution is now shifting from the GPU end to the memory end.

The most notable day was May 5. SanDisk surged by 11.98%, Micron by 11.06%, Western Digital by 5.18%, and Seagate by 4.38%. Three of the four U.S. storage OEMs hit 52-week highs.

The catalyst was two earnings reports and a supply narrative. On April 28, Seagate reported Q3 FY26 revenue up 44% year-over-year, with a record-high gross margin of 47%. CEO Dave Mosley stated during the earnings call, "AI is ushering Seagate into a new era of structural growth," with nearline exabyte capacity already allocated through 2027.

Two days later, SanDisk announced Q3 FY26 revenue of $5.95 billion, a 252% increase year-over-year, surpassing the upper end of guidance by $1.15 billion. Data center revenue soared by 645% year-over-year and nearly doubled sequentially, with Q4 guidance projecting a further 308% to 334% year-over-year increase. Coupled with Micron receiving a credit rating upgrade from Moody's, the entire sector took off in unison on Monday.

However, this is just scratching the surface. When the four stocks are analyzed individually, the "storage sector rally" is actually a misleading summary. They are driven by three entirely different supply narratives, resulting in vastly differing growth rates.

Looking at year-to-date performance, SanDisk is up by 492.43%, Seagate by 180.46%, Western Digital by 170.21%, and Micron by 124.40%, spread across four entirely different tiers. Meanwhile, the S&P 500 has risen by 6.04% and Nvidia by 5.37% during the same period. The latter has even dropped by 7.82% in the past five days. The label of being the "primary beneficiary of AI" is shifting: the GPU story driven by large-scale model training has completed its valuation expansion cycle over the past year, and money is now shifting downstream, towards the memory and storage needed to support AI workloads.

This type of segmentation is not uniform. It is layered along the medium's properties.

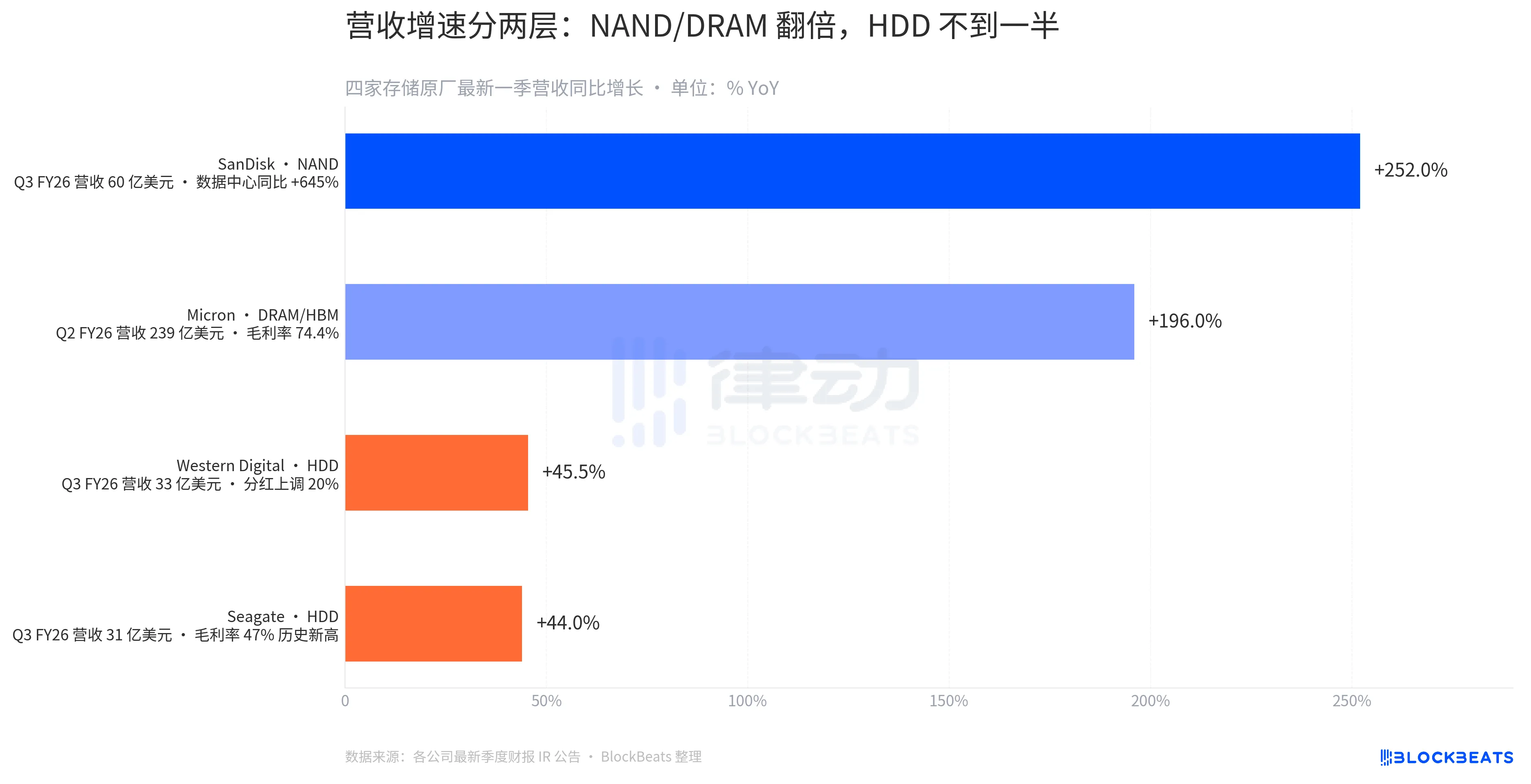

The latest quarterly financial report numbers make the segmentation very clear. SanDisk's revenue on the NAND side grew by +252% year-on-year, Micron's revenue on the DRAM/HBM side grew by +196% year-on-year, and Western Digital and Seagate's revenue on the HDD side grew between 44-45% year-on-year. NAND and DRAM represent the explosive segment in this round, HDD represents the steady growth segment, with a 4 to 5 times difference between the two segments.

The gross margin segmentation is even more pronounced. Micron's Q2 FY26 gross margin is 74.4%. This is an extreme number that a chip factory can achieve, meaning that for every $100 of DRAM and HBM sold, $74 goes into the profit statement. Seagate's 47% gross margin, although its historic high, is still an order of magnitude lower compared to DRAM manufacturers. This difference is due to the supply structure. HBM production capacity is concentrated among three companies (SK Hynix, Samsung, Micron), all of which have sold under long-term contracts until the end of 2026. HDD production capacity is evenly distributed between Seagate and Western Digital, with relatively dispersed pricing negotiation power.

The pricing end provides the same signal.

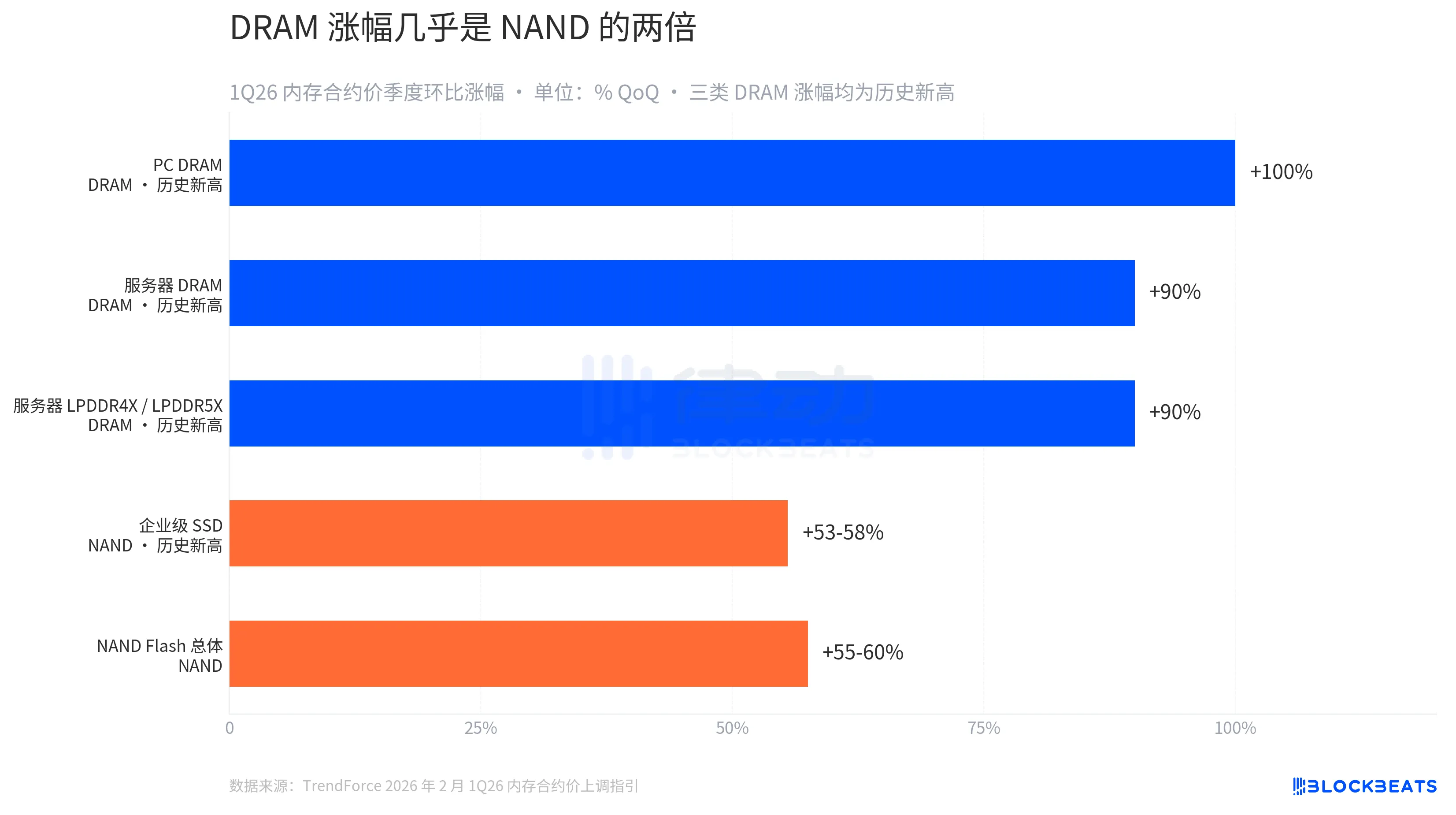

According to TrendForce's revised 1Q26 memory contract price guidance on February 2, the quarter-on-quarter increase is approximately +100% for PC DRAM, around +90% for server DRAM, and about +90% for server LPDDR4X/5X, all of which are historical highs. On the NAND Flash side, enterprise SSDs have increased by 53% to 58% during the same period, while the overall NAND has increased by 55% to 60%, which is only slightly more than half of the increase in DRAM.

This is a scissor gap that can explain everything. AI servers require both NAND and DRAM, but they need more bandwidth (HBM) and storage density (DDR5, LPDDR5X). The supply-demand gap on the DRAM side is much larger than that of NAND. The Micron CEO stated during the Q2 FY26 earnings call, "We're sold out for 2026," telling the supply story quite bluntly. The HBM4 36GB 12H has already gone into mass production for NVIDIA's Vera Rubin platform, and the full-year capital expenditure for FY26 has been raised from $200 billion to $250 billion to accommodate another level in 2027.

Among the four original equipment manufacturers, the most noteworthy is SanDisk.

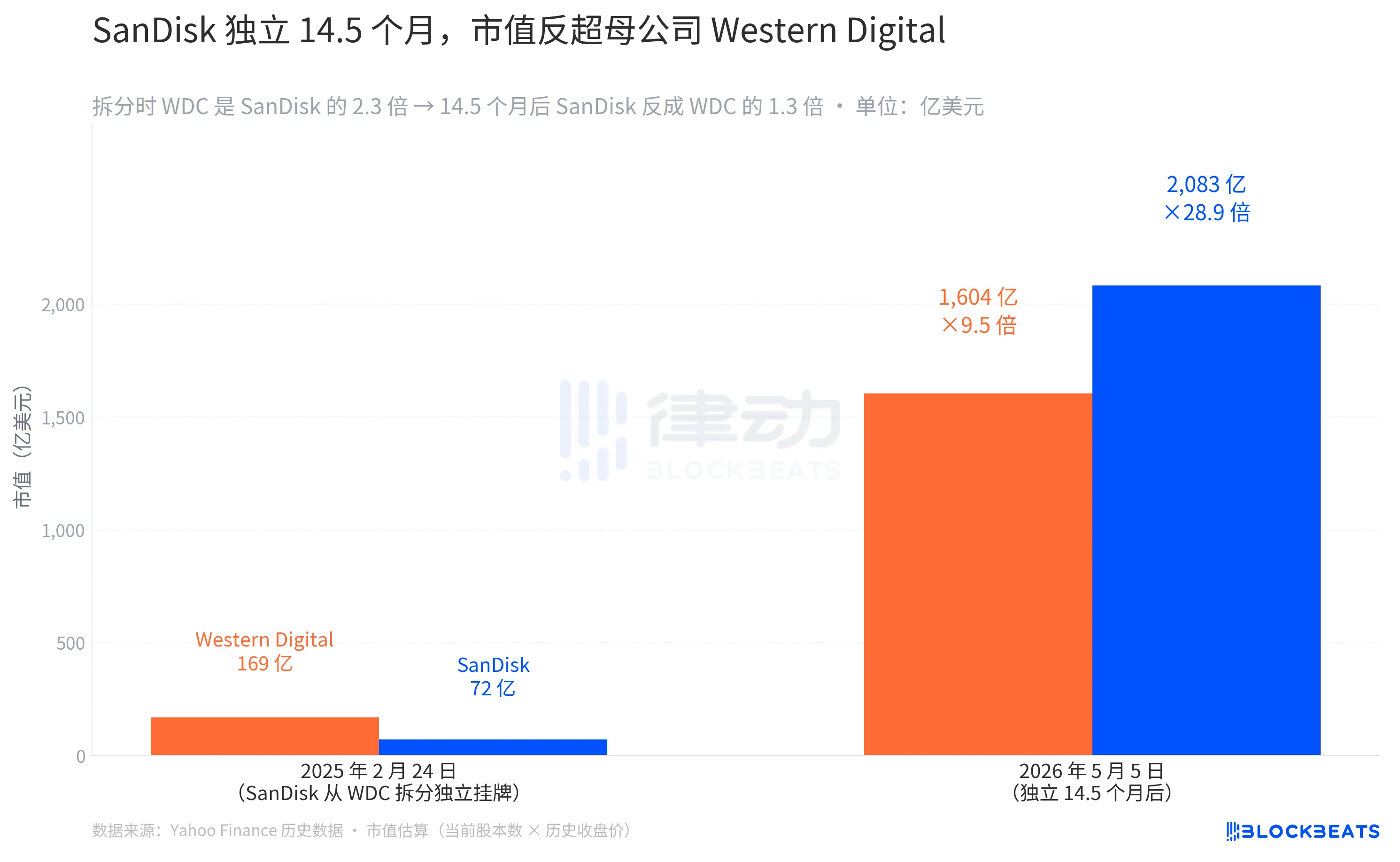

In February 24, 2025, SanDisk was spun off from Western Digital and started trading on the Nasdaq. It opened at $52 and closed at $48.60 on the first day, with a market capitalization of approximately $7.2 billion. On the same day, Western Digital closed at $49.02, with a market capitalization of around $16.9 billion. On the day of the spin-off, Western Digital's size was 2.3 times that of SanDisk.

Today, 14.5 months later, SanDisk has a market capitalization of $208.3 billion, while Western Digital's market cap is $160.4 billion. SanDisk has now surpassed Western Digital by 1.3 times. This kind of reversal is rare in the history of large corporate spin-offs. In most spin-off cases, the subsidiary is still rebuilding investor relations in the first year, and it usually takes 3 to 5 years for the market cap to catch up with the parent company. SanDisk achieved this in 14.5 months.

The reason is that it was spun off at the perfect time. When Western Digital decided to spin off in 2024, the reason given was that "NAND and HDD are in different capital cycles, and separate operations would provide a clearer valuation." This judgment was later proven correct by the market: SanDisk, after becoming independent, focused solely on NAND, perfectly tapping into the surge in demand for enterprise SSDs in AI data centers. Western Digital, focusing solely on HDD, benefited from the structural growth in cloud storage archiving. With the two companies separated, each corresponds to a distinct narrative. If they had not split initially, one company would have housed two businesses with completely different supply cycles, and the capital market would have applied a more conservative valuation multiple somewhere in between.

On May 4, Bernstein raised SanDisk's target price from $1,250 to $1,700, citing the visibility of its data center SSD business. SanDisk's financial reports have revealed that it has signed five long-term contracts, received $11 billion in financial guarantees, and locked in over one-third of NAND bit supply for the fiscal year 2027. This is a track traditionally treated as a commodity cycle, and for the first time, it has adopted a "long-term contract + customer prepayment" structure similar to advanced process node foundries.

Overall, money is flowing from the GPU end to the memory end, where DRAM is the true alpha of this round. HDD represents a different rhythm of structural long-distance running. SanDisk, a company that has only been independent for 15 months, relies on the NAND data center sector. It has surpassed its parent company, Western Digital, in market value.

On the same trading day, May 5th, NVIDIA fell by 1.03%, TSMC fell by 1.79%, and SanDisk rose by 11.98%. Also part of the "AI Beneficiary" group, the market has been voting with its feet, distinguishing which segment of the supply chain is the scarcest.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia