Perpetual Contract Genesis: Pricing Liquidity with a Magic Formula, Transparency Prevents it from Reaching its Full Potential

Original Title: LONG READ: The untold story of how crypto's hottest derivative came to be

Original Author: IZABELLA KAMINSKA, The Peg

Translation: Peggy, BlockBeats

Editor's Note: Perpetual futures are often seen as one of the most speculative trading tools in the crypto market, and both its inventor and the exchange that nurtured it have long been surrounded by controversy. BitMEX was once the global hub for crypto derivatives trading, but also faced regulatory scrutiny due to anti-money laundering compliance failures; one of its founders, Ben Delo, was not only the designer of perpetual futures but also found himself in the defendant's seat in the U.S. judicial system. Innovation, expansion, and institutional friction have always been intertwined in this case. This article goes back to the origins of perpetual futures, starting from BitMEX's engineering choices, market constraints, and serendipitous inspiration, tracing how, in the absence of central design, it spontaneously evolved a pricing and clearing mechanism.

Below is the original text:

In September 2015, in the back of a taxi in Shanghai, a young mathematician and his co-founder were trying to solve a long-standing issue for their crypto exchange. What they sketched out was a peculiar, perpetual futures contract.

This invention would later be known as a "perpetual future," a financial instrument that has since grown into one of the most significant and highest-volume derivatives in the crypto market but remains largely unexplored in the traditional financial system.

In recent weeks, a few observers have finally begun to take notice: this tool is starting to have an impact on the evolution of the modern financial system. However, discussions are still limited and superficial, and most importantly, they overlook a key background—the rise of perpetual futures was not an isolated event but coincided with three deep structural shifts:

· Central banks returning to the "scarce reserve" operational framework;

· Unsecured funding as an emergency liquidity source is disappearing;

· The cost of maintaining funds float in the international U.S. dollar payment system is continuously rising.

It is in this context that the rise of stablecoins has created an entirely collateralized, short-term dollar funding source. Interestingly, in this system, there is no central authority determining the pricing and clearing of this liquidity at the margin.

Currently, all of this is primarily achieved through the funding rate of perpetual contracts — as long as stablecoins are trading, this mechanism can operate on its own.

Even more surprising is that: the official financial system once took many years, with multiple regulatory bodies and expert committees conducting repeated studies, negotiations, and designs before finally introducing an alternative to LIBOR (London Interbank Offered Rate); whereas the funding rate generated by perpetual contracts, now settling daily transactions of trillions of dollars in stablecoin funds, is almost entirely a product of natural evolution.

At the same time, an academic debate on the monetary policy operational framework is continuing to ferment within central banks. Central bank officials around the world are gradually realizing that the old system relying on the unsecured federal funds rate to transmit monetary policy and price marginal liquidity is no longer applicable. However, the issue lies in that no one can reach a consensus on which market rates should anchor the "new operational framework."

If LIBOR and the historical experience of the Eurodollar market are still relevant, then the true cost of dollar marginal financing always appears at the intersection of the official system and the unofficial system. Since stablecoins are becoming the new "collateralized Eurodollar," the index most capable of real-time reflecting systemic funding pressure is likely the funding rate of perpetual contracts that help these systems settle.

However, the view that perpetual contracts are now taking on a crucial role in absorbing, pricing, and mitigating liquidity pressure, while traditional mechanisms have struggled to elegantly cope, has still not truly entered the field of vision of central bank decision-makers.

Therefore, it is now especially important to look back at how these tools came into being, what problems they originally tried to solve. Below is a historical narrative, from my unique perspective in the early days of the cryptocurrency industry tracking this field.

The protagonist of the story is Ben Delo: a mathematically inclined, eloquent mathematician trained at Oxford. In 2014, he, along with the straight-talking American from Detroit, Arthur Hayes, and the least publicly visible American, Samuel Reed, founded the BitMEX exchange in Hong Kong.

In 2020, the three were charged by the U.S. Department of Justice for violating the Bank Secrecy Act, as BitMEX, in its rapid growth to become one of the world's largest cryptocurrency derivatives trading platforms, failed to implement sufficient anti-money laundering (AML) mechanisms. In 2025, with Donald Trump unexpectedly issuing a pardon for them, the public once again turned their attention to these three founders.

But before all of these headlines, they were just three entrepreneurs trying to address traders' dissatisfaction with the design flaws of cryptocurrency futures.

My first intersection with any of them was in 2017. At the time, I was still writing for FT Alphaville, a part of the Financial Times, mainly covering the latest frenzy in the crypto industry, Initial Coin Offerings (ICOs).

Someone suggested I should talk to Arthur Hayes. They described Hayes as a highly market-savvy industry commentator who could offer a realistic, pragmatic, and narrative-free perspective.

To be honest, I was cautious at the time. Those years were filled with hype and rug pulls in the crypto world, with almost everyone shilling their position. But Hayes did not disappoint.

Our conversation was remarkably calm and direct. He was evidently very aware of how the real financial markets operated while maintaining a high immunity to the crypto industry's common exaggerated narratives and buzzwords.

Regarding ICOs, he bluntly said: "People were willing to pay for something, but in the end, they didn't really own anything. It was just a promise from a development team, and whether it was actually useful, no one knew." "Interestingly, people could raise $10 million in a few minutes based on a dream."

At that time, I didn't realize that there was an even deeper meaning behind his words.

Back then, BitMEX's profits were undergoing a sharp rise, partly thanks to the all-encompassing ICO narrative. Whimsical projects like "Dentacoin" (a token claiming to be used only for dental payments) caused a frenzy of funds flowing wildly in the crypto ecosystem, with BitMEX naturally benefiting from this revelry.

But for the founders, this glory might have carried a tinge of bitterness.

Just a few years ago, they struggled to even get investors interested in BitMEX.

Ben Delo later told me that from 2014 to 2016, they tried to raise funds multiple times but kept hitting walls. With no outside support, they had to rely on their own savings to keep the project running, working from cafes and apartments, slowly but authentically advancing the product.

BitMEX team in 2017, including Arthur, Ben, Sam, Greg, and Jinming. Image provided by BitMEX

It wasn't until a moment of inspiration struck Delo in September 2015 that their fate was completely altered.

When pondering how to make leverage trading more user-friendly, he came up with a derivative structure with no expiration date — the perpetual contract. By 2019, this innovation had propelled BitMEX into one of the most profitable exchanges in the industry.

It was also during BitMEX's near-peak and pre-pandemic days that I had a completely different encounter with the company.

It wasn't until September 2015 that Delo had a moment of inspiration significant enough to change their fate.

Through much contemplation on how to make leverage trading more accessible to the average user, he gradually envisioned a new derivative structure: a contract with no expiry date, later known as a "perpetual contract." By 2019, this innovation had propelled BitMEX to become one of the most profitable exchanges in the entire crypto industry.

It was also during this time of continuously driving the exchange to new heights, before the COVID-19 pandemic erupted, that I had a unique encounter with BitMEX.

An internal whistleblower from the company proactively reached out to me to disclose BitMEX's alleged violations of regulatory requirements. This person claimed that the founding team, in pursuit of increased profits, knowingly evaded anti-money laundering regulatory obligations. They mentioned that Bloomberg had already reported on regulatory investigations into the company, but many crucial details were still undisclosed, which could be further shared with the Financial Times.

This lead did not progress much further. Just as I was preparing to delve into the investigation, the COVID-19 pandemic hit, swiftly engulfing the entire news agenda. Further exacerbating the standstill, the source began to hesitate, fearing that providing evidence to the media could impact the broader case being pursued by the U.S. Department of Justice and the Commodity Futures Trading Commission (CFTC), and did not provide me with the requested materials to substantiate the allegations. Before The Financial Times team could independently pursue the investigation, the market experienced severe turmoil, and The Financial Times was preoccupied with another major money laundering-related investigation, the Wirecard case.

Nevertheless, the most striking aspect of that contact with the whistleblower was the inherent contradiction presented in their narrative. This individual clearly wanted to expose BitMEX's misconduct, yet at the same time, they consistently held a significant respect for those they accused — repeatedly praising the company's professionalism and, in particular, highly commending Ben Delo's intellectual capabilities, especially his pivotal role in conceiving the "perpetual contract" tool.

It was at that moment that I was firmly captivated by this concept.

Perpetuals? What?

Before that whistleblower reached out to me, I had never heard of the so-called "perpetual contract." This somewhat made me feel a bit embarrassed, considering I had been reporting on commodity futures for many years and considered myself familiar with the derivatives market. However, the operational mechanism of this new type of tool was completely beyond my intuitive understanding. I remember staring at BitMEX's trading interface, trying to decipher the logic behind it, but I clearly felt inadequate.

As I began to experiment with my own meager bitcoin holdings on the platform (worth about $10), the situation gradually became clearer. I began to realize that a perpetual contract was not just a clever cryptographic trading tool. In a sense, it was more like a self-regulating LIBOR, the wholesale funding rate that was proven completely ineffective during the 2008 global financial crisis.

From this perspective, perpetual contracts imply that a new financial architecture is taking shape, one that can bring clear price signals to a previously opaque and long-unexamined funding market, especially in intraday funding pricing.

What is truly striking is that the crypto industry itself has hardly realized what it has created. They evidently also lack knowledge and experience at the central bank level, making it difficult to understand how this tool embeds into the evolving collateralized funding paradigm of the financial system.

I told myself at the time: I must speak directly with Delo. I need to understand how he got to this point and also want to know to what extent he understands the deeper "infrastructure issues" behind the dollar system.

Unfortunately, all my visions for this interview were soon interrupted by reality. Lockdowns, daily editing work, column writing, and taking care of a young daughter consumed all my energy.

The truly decisive turning point came on October 1, 2020. Almost inevitably, things finally reached that point: Delo and his co-founders were formally charged with violating U.S. law, just as the whistleblower had predicted.

Frankly, I don't think the founders of BitMEX were surprised by the "internal whistleblower" fact. U.S. authorities have long operated a transparent whistleblower reward system, and the evidence disclosed in the trial clearly indicates that someone within the company was cooperating with the investigation. Perhaps what truly surprised them was that in the months leading up to the formal indictment, attempts had been made to offer their story to multiple media outlets.

Against this backdrop, I continued to track any possibility of this story, which no longer exists. BitMEX found itself deep in legal trouble, and the founders were bound to fade from the public eye. Delo eventually surrendered to New York in March 2021 and pled not guilty to the related charges. In February 2022, in a criminal proceeding related to the Bank Secrecy Act, all three individuals ultimately chose to plead guilty. As per the final settlement terms, each person paid a $10 million fine, while Delo was also sentenced to 30 months of probation.

This was not the worst outcome. BitMEX had to fully implement a KYC/AML system to continue operating, but the three founders were able to retain a substantial amount of wealth accumulated over the past few years.

By February 2022, I had left the Financial Times and founded Blind Spot. This meant that, after nearly a year, or even longer, of restricted story choices, I could finally push forward with my own editorial plans freely.

The new project took several months to gradually take off, but eventually, I was able to return to this story. By that time, BitMEX's legal issues had largely been settled, seemingly making it the right time to reach out to Delo. I reached out to him, and although he was initially hesitant, he eventually agreed to the interview.

So, on June 28, 2022, I sat in Delo's modestly furnished office in Westminster, listening to him recount how he invented the perpetual contract. As we conversed, an antique grandfather clock rhythmically chimed in the background.

The conversation lasted for nearly two and a half hours (or at least through three chimes of the clock), almost entirely revolving around the convoluted technical details of the perpetual contract's inception.

It has been over three years since that conversation. Readers might reasonably wonder why it is only now that they are seeing this complete story. Frankly, the blame lies mainly with me and the various real-world demands brought about by the entrepreneurial process.

To do justice to this subject, I repeatedly postponed formal writing, always thinking I could finish it in some never-arriving "10% time." What made it more complicated was my prior commitment to Bloomberg to provide them with the key parts of this story—because I believed Delo's experience deserved a broader dissemination than Blind Spot.

The Bloomberg piece was finally published on August 31, 2022. It was not the full narrative I had hoped to write, but it did at least reassure me that the most critical facts had entered the public record, allowing me to save the complete version for a time when I could truly dedicate myself to it.

Incredible as it may seem, that moment, until this weekend finally arrived, the reason for it will soon become apparent.

From some perspectives, such a delay may not necessarily be a bad thing. Compared to years past, the fragments of the story I now possess are much more complete. Furthermore, as Douglas Adams, the author of The Hitchhiker's Guide to the Galaxy and a famous procrastinator, once said: for a creator, the hardest part to finish is often the last mile.

Origin

As mentioned earlier, the exploration of the "ultimate derivative" began fittingly in the back seat of a Shanghai taxi in September 2015. At the time, Delo and Hayes were in China for a startup accelerator program, simultaneously troubled by the increasing user complaints about BitMEX's perpetual futures contracts. Although both were quite familiar with the traditional derivatives market, they gradually realized that crypto traders hated any tool with a fixed expiration date and were extremely averse to forced liquidation or rollover.

As someone with a background in mathematics and engineering, Delo has always placed a high value on speed, determinism, and market structure.

Prior to founding BitMEX, he worked as a financial engineer, building trading algorithms and data systems at GSA Capital and J.P. Morgan. During his time at GSA, he worked directly with Alex Gerko—a Russian-born math genius who later became one of the wealthiest people in the UK.

Delo's interest in Bitcoin began around 2013, more out of intellectual curiosity than ideological fervor. He told me that his initial purchase of Bitcoin was motivated by a desire to better understand how the system worked. "As a new technology, it was very appealing to me, and I wanted to delve into it."

But this curiosity quickly collided with the harsh reality of the early crypto infrastructure. The exchanges he encountered were slow, fragile in structure, and often faced catastrophic failures. Too many platforms were severely damaged by operational mistakes or direct hacking attacks, trust was repeatedly eroded, making the entire market almost unusable for anyone accustomed to professional trading standards. Delo quickly realized that the technological potential of this industry was being choked by its own terrible "infrastructure."

For a long time, Delo tried to avoid these risks. His preferred way of acquiring Bitcoin was through LocalBitcoins, an early peer-to-peer trading platform that matched buyers and sellers offline face-to-face, thus circumventing many systemic vulnerabilities. It was also on LocalBitcoins that Delo met Arthur Hayes: a trader with a background in stock derivatives trading at Deutsche Bank and Citibank, and a finance degree from the Wharton School.

The two almost immediately clicked because they shared a highly aligned assessment of the deepest structural flaws in the crypto market and understood well what it would take to fix them.

Both of them noticed a fact that was largely overlooked by most: hardly any existing exchanges truly grasped the concept of margin trading. And they quickly realized that this meant a huge opportunity.

Shortly thereafter, Hayes proposed to Delo: establish a derivatives exchange that would bring the mature margin discipline from traditional finance into the crypto market.

The two agreed on clear division of labor: Delo would be in charge of building the system's technology and underlying mechanisms, while Hayes would handle financing and marketing. However, they still needed a software engineer, which is why Sam Reed, who was then based in Hong Kong, was invited to join the team and become the third co-founder of BitMEX.

In 2014, the three of them co-founded HDR Global Trading, the parent company of BitMEX, with 'HDR' representing Hayes, Delo, Reed.

In this sense, Delo noted, BitMEX's birth was always shrouded under the shadow of the Mt. Gox collapse. This early crypto exchange "lost" 850,000 bitcoins in 2014 and remained unaware of the issue for a considerable amount of time.

Although the full picture was not immediately clear to outsiders at the time, Mt. Gox's downfall was not due to a single catastrophic hack but rather years of accumulated operational flaws. It was launched in 2010, originally as a modified website for trading Magic: The Gathering cards, and then rapidly expanded in an immature infrastructure environment. Its matching engine and wallet system were notorious for their fragility, and from 2011 to 2013, accounting loopholes, unrecorded withdrawals, and exploitable system bugs (the most famous being the 'transaction malleability' issue) gradually led to a massive yet almost invisible gap in customer assets.

On February 28, 2014, Mt. Gox filed for bankruptcy, revealing a loss of approximately 650,000 to 850,000 bitcoins, shaking the entire crypto community. Initially, almost everyone suspected either fraud or a hacking attack—including the exchange's owner himself. But as the investigation deepened, it became apparent that these losses were actually the result of slow accumulation over the years, caused by 'drip-feed theft,' human error, and poor reconciliation mechanisms.

The founders of BitMEX thus agreed: their trading platform had to be designed tightly enough so that another Mt. Gox could never happen.

To this end, Delo proposed a core principle: BitMEX's system must be able to settle to zero at any moment. "I designed BitMEX's trading engine to ensure that it never loses a single cent," he explained, emphasizing that to this day, the system has never lost even a single satoshi. "If it's not zero-sum, then it means you've magically created or destroyed Bitcoin, which is impossible."

To achieve this, BitMEX introduced a real-time auditing mechanism to ensure that at any given time, the amount of Bitcoin recorded by the trading engine matches exactly what is held in the exchange's wallets.

In theory, such a rigorous design should have easily impressed investors.

However, when the trio attempted to raise external financing, they found themselves at the worst possible time to launch a crypto exchange. It was the trough of the 2014 "Crypto Winter," where venture capital had almost entirely exited exchanges and anything related to Bitcoin. The most popular narrative at the time was "enterprise blockchain," not exchange infrastructure, so hardly anyone was willing to bet on them.

Reflecting on a face-to-face interview in 2022, Delo recalled, "When we came out in 2014, the exchanges already existed, and VCs had invested early. Arthur went to see investors, and they solemnly said, 'Oh, no, we are no longer investing in Bitcoin; we are investing in blockchain.' We asked, 'So what exactly is blockchain?' and they couldn't explain it themselves."

In a situation of scarce funds and almost zero attention, the founders had no choice but to dig into their own savings and rely entirely on self-funded BitMEX's launch.

The team visited Sam Reed in Milwaukee. Image provided by BitMEX.

Ironically, the absence of external capital later turned into an advantage. Unlike most exchanges, BitMEX remained almost entirely in the hands of the founding team. By 2018, when the platform's annual profit was nearing $1 billion, the true beneficiaries were not a myriad of venture capital firms but the three founders themselves.

By 2019, BitMEX's annual trading volume reached $1 trillion, and Delo's 30% stake was valued at $3.6 billion.

In 2014, Arthur Hayes, Ben Delo, and Sam Reed at the Web Summit conference. Image courtesy of BitMEX.

However, the founding team's first major breakthrough actually did not directly come from perpetual contracts, but rather from something more rudimentary, yet more intuitive: extreme leverage.

Delo and Hayes were well aware that in the traditional financial markets, retail traders usually could only use 2 to 3 times leverage—put in $1,000, and often only be able to open a position of $2,000 or $3,000. However, they believed that the crypto market could fully withstand a more aggressive risk exposure without compromising the overall security of the account.

This judgment ultimately gave birth to the design of "isolated margin": each trade would be isolated in an independent margin pool, completely separated from the rest of the account funds.

In this mode, a failed trade no longer had the possibility of wiping out the entire account. As a result, a trader with only $100 could also control a $10,000 position; even if the market trend was unfavorable, the loss would be strictly limited to the margin already invested. Even a slight fluctuation in the Bitcoin price could either create or wipe out a fortune, but the risk boundary was always clear.

This safety net seemingly conservative in logic, actually encouraged more aggressive bets and significantly increased trading frequency. For BitMEX, this was crucial, as most of the platform's revenue came from trading fees.

Delo recalled that on the day BitMEX officially increased the leverage limit from 50 times to 100 times, trading volume experienced explosive growth. It was also on that day that the exchange finally became profitable.

The core of this "magic formula" lies in Delo's real-time margin system design.

"Every time the mark price changes, we immediately recalculate the margin status of each position and each trader," he explained, "We can instantly determine if a position needs to be liquidated. If necessary, the liquidation will occur immediately—not finalized minutes later through a manual process, but before the price further moves in an unfavorable direction."

Many exchanges at the time already had a forced liquidation mechanism, but BitMEX's key innovation was to make the liquidation process cheaper and more orderly. Particularly important was that the trigger for liquidation was not BitMEX's internal price—which could be distorted due to insufficient liquidity—but an independent third-party price index. This design effectively prevented cascading sell-offs and spared the platform from being bitten back by its own market impact.

“Nobody likes to be liquidated,” Delo said, “but we try to explain the rules as clearly as possible, achieve transparency, so that at least there are no surprises.”

This system quickly gave rise to the phenomenon of “involuntary liquidation.” In the crypto community, it is more commonly known as “rekt,” and gradually spawned its own set of meme culture.

Moving Towards Perpetual

Although high-leverage products were successful in the early days, by 2015, this futures-oriented exchange still faced another type of problem. Part of it came from the complexity of derivatives themselves.

Retail crypto traders were not accustomed to the fixed expiration date of futures contracts. Initially, BitMEX, like the traditional markets, introduced bitcoin futures with different expiration cycles, similar to how crude oil can have June delivery, December delivery. However, like all futures markets, the prices of these contracts would deviate from the spot price over time, reflecting market expectations of future supply and demand, as well as costs such as storage, financing, etc. In traditional finance, the futures premium over spot, is called the “basis.”

However, despite these mechanisms being commonplace in traditional markets, the founders of BitMEX quickly realized that many traders did not understand these dynamics. What's worse, this understanding barrier was becoming a limiting factor for further user engagement in trading.

It was during that aforementioned taxi ride in Shanghai, as Delo and Hayes reviewed product flaws and discussed user feedback, that Delo began to repeatedly ponder a question: Do futures contracts really have to expire?

He gradually realized that traders simply did not want to think about rolling over contracts or understand the basis. What they wanted was exposure to the Bitcoin price that was clean, continuous, and uninterrupted.

If that's the case, why not just create a perpetual futures contract that never expires?

On the surface, this idea seemed almost absurd. Delo presented this idea to a quant friend and immediately faced skepticism: a contract with no expiration date would theoretically have infinite fair value. “You have to take the interest rate factor out of it,” the friend told him immediately.

However, this statement triggered a deeper level of thinking in Delo. Since traders did not want the financing cost to be reflected in the Bitcoin price, why not completely separate it? In his view, the cleanest way was to match each position with a dynamically changing funding rate.

The ensuing question was: how should this rate be determined?

Delo realized that to make this mechanism work, it was necessary to introduce a market-driven reference rate — some kind of benchmark rate playing a role similar to LIBOR in the crypto market. However, in 2015, such a thing did not yet exist. The closest alternative was the lending rate on spot exchanges like Bitfinex and Poloniex: users lending dollars or bitcoins on these platforms to provide funding for long and short trades. It was not perfect, but at least it could serve as a starting point.

This was the initial breakthrough that allowed perpetual contracts to truly take off.

When the first version of perpetual contracts launched in May 2016, traders poured in almost frenziedly. The trading volume quickly hit record highs. Many people saw this product as a kind of almost “magical” existence: having all the leverage advantages of futures without having to endure any funding hassles. Compared to previous complex derivatives, its operational logic was much more intuitive.

At the same time, the series of futures contracts originally offered by BitMEX with weekly and daily settlement dates, bearing complex codes like XBT 7D, XBT 48h, XBT 24h — became redundant.

“We cut all of these, leaving only one contract named XBTUSD,” Delo recalled.

This simplification also brought an unexpected positive effect: liquidity became highly concentrated, BitMEX's market depth significantly increased, trading efficiency improved as well, truly killing two birds with one stone.

Pricing for Liquidity

No doubt, traders loved this product very much. The issue was they loved it a bit too much.

Despite the introduction of the funding rate adjustment, the perpetual contract price continued to persistently trade above the spot price, sometimes even reaching a premium of 5% or more. This indicated that the funding rate based on third-party lending data was starting to lag behind the actual market conditions.

In Delo's view, this brought about a serious problem: traders who only used 1% margin to establish long positions in the perpetual contract were at high risk of liquidation as soon as the perpetual contract price quickly dropped back to the spot level. What's worse, these traders might think their liquidation was triggered by a “disconnected price,” thus questioning the fairness of the system.

To address this issue, Delo's initial response was to approach market makers, reminding them that when the perpetual contract deviated from the spot by 5%, shorting and pulling the price back on track represented an almost risk-free arbitrage opportunity. However, market makers were not convinced, believing that the premium could very well expand further to 10% or even higher.

At this point, Delo realized that the real issue was not whether arbitrage opportunities existed, but rather that the funding rate itself was not sufficient to attract enough short positions.

He needed to design a new mechanism to allow the rate to adapt to market deviation.

The specific approach involved: measuring the perpetual contract price deviation from the spot price on a minute-by-minute basis. This deviation value was later referred to as the "premium index" and was used to determine the funding rate. The rate was updated every 8 hours and automatically settled at the end of each period, payable in Bitcoin or stablecoins.

"This was the first time we used our own market data to construct an index," Delo said.

In the mechanism, the funding rate was jointly determined by the BitMEX perpetual contract price and its premium to the spot index. However, to enhance robustness, Delo did not simply rely on the transaction price but instead calculated a depth-weighted spread based on the entire BitMEX order book's mid-price. This value was then hedged against the contract's current "fair price"—the latter derived from the Bitcoin spot price plus the implied basis calculated from the previous period's funding rate.

This system essentially anticipated the funding rate for the next 8 hours. In most cases, the rate remained positive, reflecting both the market's natural long bias and attracting short positions through economic incentives to correct price deviations.

This resulted in a positive feedback loop.

As longs drove the perpetual contract price above the spot, the holding cost quickly rose; when shorts dominated, the funding rate would subsequently decrease.

Delo described this mechanism as a "dynamic mechanism for pricing liquidity": when market demand tilted in one direction, the funding rate would urge traders to take opposite actions, bringing the price back to a reasonable range, thus keeping the perpetual contract in line with the spot.

"If you break down this system mathematically," he explained, "we effectively eliminate Bitcoin's overnight rate and the dollar's overnight rate. They are just shadows left over from the system's evolution. Eventually, the funding rate is entirely determined by the product's premium to the spot. That's dynamic pricing."

For BitMEX, the perpetual contract quickly became its signature innovation.

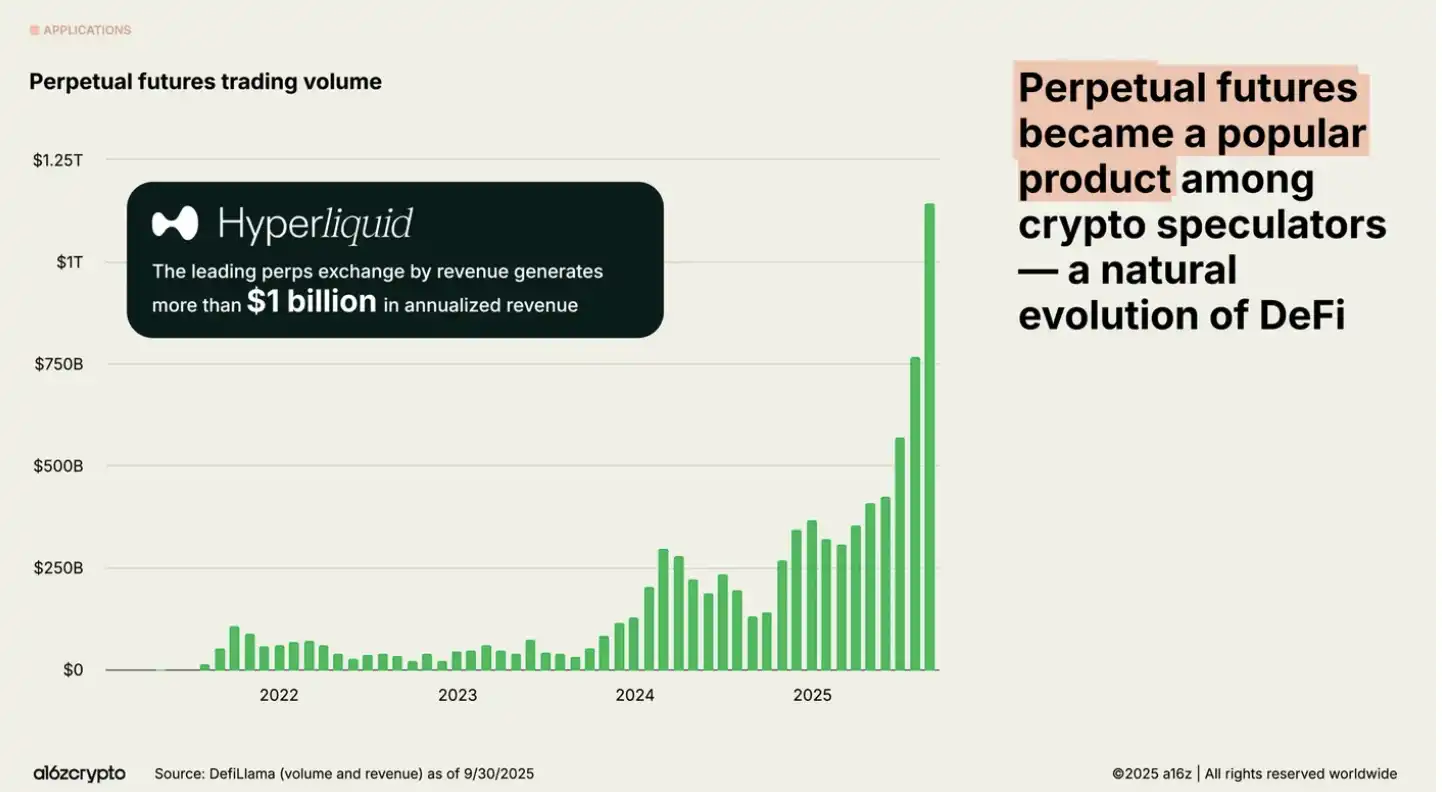

Transaction activity has exploded. In just a few short years, "perp" has evolved from a niche experiment to a market standard tool. Initially just BitMEX's flagship product, it was quickly copied by the entire industry and eventually became the default way for traders to leverage in the crypto market.

As illustrated in the chart below from a16zcrypto, perpetual contracts have now become the fundamental trading unit in the DeFi industry, daily carrying out transactions worth trillions of dollars.

A Shadow Interest Rate?

For quite some time, Delo did not think about the broader application of perpetual contracts from a macro perspective.

"We were just trying to solve a user problem at that time," he said, mentioning that after the concept took shape, he only took a three-hour flight from Singapore to Hong Kong to write the entire mechanism. "Once this thing was invented, it worked so smoothly that I could hardly believe it didn't exist before," he recalled.

In Delo's view, perpetual contracts themselves do not possess any intrinsic attribute that must be based on Bitcoin. The same structure can be applied to stocks, gold, oil, or any other asset with sufficient spot liquidity, including the dollar itself — for example, in a form similar to an overnight index swap (OIS).

In all these scenarios, a similar outcome will eventually emerge: a nominally "collateralized" but highly leveraged offshore funding rate. In theory, it can be applied to any asset class with an active spot market.

The operational logic is highly consistent across asset classes: when the funding rate of a perpetual contract significantly rises, the market is actually signaling that by standing on the other side of the trade, one can receive a return.

This means that in the offshore system, the demand for leveraged exposure is exceeding the system's available dollar liquidity; and anyone willing to provide this liquidity can therefore earn significant returns.

The key is that, since this demand itself is highly leveraged, when it emerges, a new type of demand for U.S. Treasuries, beyond the traditional lendable fund supply constraint, is also synchronously created.

The deeper implication is this shadow-like "liquidity price" exists entirely outside the control of the Fed.

Therefore, as long as the funding rate of the perpetual contract is significantly higher than the Fed's policy rate, the arbitrage path is clear: borrow dollars at the lower policy rate within the banking system, convert them into stablecoins, then capture higher synthetic yield in the perpetual contract market. This process will attract new demand into the stablecoin system, flow through its reserve managers, and further into U.S. Treasuries (especially short-term Treasury bills).

Conversely, if the Federal Reserve were to raise the policy rate above the perpetual contract funding rate, the incentive would reverse: stablecoins would be redeemed, issuers would have to sell treasuries to meet withdrawal demands, and the marginal buyers of short-term government debt would disappear as a result.

In this sense, the perpetual contract funding rate could serve as both the "floor" and the "ceiling" of U.S. monetary policy, a shadow rate reflecting the true marginal cost of dollar liquidity faced by any trader able to access the stablecoin system.

When it is relatively high compared to the policy rate, it will draw liquidity away from the banking system, towards the crypto market and treasuries; when it is too low, it will trigger deleveraging and a counterimpact on the treasury market.

Furthermore, if an exchange were to launch a perpetual contract with the U.S. dollar itself as the underlying asset, its funding rate would become a pure measure of the "USD scarcity based on stablecoins," a crypto-native LIBOR. It may be technically "unsecured," but its level would be shaped by the collateral conditions in a highly leveraged market. It would not converge to the Federal Reserve's policy rate but would reveal the true marginal cost of offshore dollar liquidity, beyond the direct control of the Federal Reserve.

Of course, in the long run, markets tend to equilibrium. If the perpetual contract funding rate, supported by stablecoins, remains significantly higher than the policy rate over the long term, arbitrage activity should eventually draw enough liquidity away from the core banking system into the stablecoin-perpetual contract structure, gradually converging the two. However, this convergence comes at the expense of the Federal Reserve's regulatory capacity as liquidity begins to flow towards jurisdictions not bound by the Basel Accords.

The more likely scenario is that the Federal Reserve will do everything it can to restrict this arbitrage pathway, as it did with the European dollar market after the financial crisis. If the U.S. Treasury also refuses to issue additional treasuries to the market beyond its own funding needs or debt ceiling constraints, then the offshore perpetual contract funding rate will be structurally maintained at a higher level.

In such an environment, the only entities capable of expanding the "synthetic dollar supply" would be those foreign official or semi-official institutions that already hold large amounts of U.S. treasuries—such as China, Japan, and other countries. If the perpetual contract funding rate remains high for an extended period, they will be strongly incentivized to issue their own USD stablecoins and lend them to the perpetual contract market to liquidize reserve assets and engage in arbitrage.

If, through some unexpected channel, the two systems do achieve a covered interest rate parity (i.e., aligning the perpetual contract funding rate with the Federal Reserve policy rate), then the power of perpetual contracts would appear even more pronounced outside the crypto market.

Using gold as an example: If a perpetual contract is launched with XAUT or another tokenized physical gold as the underlying asset, the forward rate generated by its funding rate may be more accurate and transparent compared to the opaque system currently constituted by CME futures pricing and private over-the-counter precious metal lending quotes. The true, collateralized gold funding cost within the London Bullion Market Association (LBMA) is still largely hidden behind the scenes, and for the first time, it will be exposed in real time to the public eye.

From Delo's perspective, this transparency is the reason why most traditional financial platforms are hesitant to embrace the perpetual contract model. It will not only squeeze their profit margin but also subject the economic structure of their own financing market to public scrutiny.

"The truly unique thing about this contract is that it is a market in itself, a dynamic market," Delo said. "It does not require the platform itself to inject capital or act as a market maker. It will naturally attract market makers, buyers and sellers, longs and shorts, price acceptors and price makers, bringing everyone together into one system."

The ultimate irony is that a mechanism originally designed to keep derivative prices in line with spot prices may, in the future, exert gravitational pull on the entire US dollar system itself.

Champion of Free Speech

This is not the end of my story with Ben Delo.

Many readers may know that I have long been involved in the free speech community. In my view, this is an issue that a journalist can openly support without worrying about compromising professional neutrality. Because free speech itself does not deviate from the most basic responsibility of the news profession.

Therefore, when in the summer of 2023, still feeling guilty for not completing this article for a long time, I walked into Delo's Westminster office again, I was somewhat surprised. This time, I was invited to attend a free speech-themed gathering, and what shocked me even more was that the event's host was none other than Delo himself. Before that, I had no idea he had been quietly funding this cause behind the scenes. Frankly, the embarrassment of that moment left me feeling utterly ashamed.

Fortunately, The Daily Telegraph has done a much better job of telling his story than I have. Just last week, they provided a timely and comprehensive report on Ben Delo's work in the field of free speech, which ultimately spurred me to finally make up my mind to complete this long-delayed article.

If there must be a reason for this delay, it is probably this: The suppression faced by today's writers does not only come from government orders, defamation threats, or legal battles but also from the scarcity of time itself. When you must "sing for your supper" in institutions to pay the bills and follow their editorial priorities, those writing projects born out of passion are bound to be continuously postponed.

Sometimes, it's not the censorship regime that prevents a story from being told, but the cost of life itself.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia