Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Standard & Poor's has issued its first-ever credit rating for a cryptocurrency treasury, so why did industry leader Strategy only receive a B-?

Original Title: "S&P Rates Strategy B-, Why is the DAT Leader Considered Junk by Institutions?"

Original Author: Azuma, Odaily Planet Daily

On October 27th, Eastern Time, S&P Global conducted its first rating of the Bitcoin treasury company Strategy (formerly Microstrategy, stock code MSTR).

To the embarrassment of the absolute leader in the DAT field, Strategy only received a B- issuer credit rating—In other words, in S&P's view, Strategy is considered a high-risk "junk" in terms of default.

S&P and Its Rating System

S&P, along with Moody's and Fitch, are known as the world's three major rating agencies and are currently among the most authoritative credit rating agencies in the international financial market.

According to S&P's official introduction, its credit ratings mainly reflect the institution's forward-looking opinion on the issuer and its debt credit condition. During the rating process, the analysis usually focuses on the issuer's ability and willingness to fulfill its financial commitments. The so-called credit condition covers various factors, including the likelihood of default, potential external support, payment priority, and recovery rates.

S&P's ratings for long-term credit usually have ten main grades, from highest to lowest: AAA, AA, A, BBB, BB, B, CCC, CC, C, D. Except for AAA and CC and below grades, each grade can also use the "+" or "-" sign for fine-tuning to indicate different levels within the same grade.

Under common understanding, the two subdivided grades, BBB- and BB+, are considered a dividing line. BBB- and above are classified as "investment-grade," while BB+ and below are classified as "speculative-grade," more bluntly referred to as "junk bonds."

Evidently, the B- received by Strategy is still far from BB+...

Why Doesn't S&P Recognize Strategy?

In its credit rating article on Strategy, S&P elaborated on the reasons for giving a B- rating.

According to S&P, Strategy faces issues such as high business concentration, a too-large allocation to Bitcoin, insufficient USD liquidity, and an extremely weak risk-adjusted capital postion. Despite the company having strong access to capital markets and managing its capital structure prudently, it is not enough to offset the aforementioned negative impacts. Taking all factors into consideration, S&P provided a B- rating.

S&P emphasized that Strategy's Bitcoin strategy results in a natural currency mismatch issue—holding a significant amount of Bitcoin (long position) while its debts and dividend obligations are denominated in USD (short position). When facing debt maturities, interest payments, and preferred stock dividends, Strategy needs to make payments in USD, but its primary asset is Bitcoin. While Strategy maintains a certain USD balance on its balance sheet, it is mainly used to support operational expenses of its software business, and the remaining cash is entirely invested in Bitcoin.

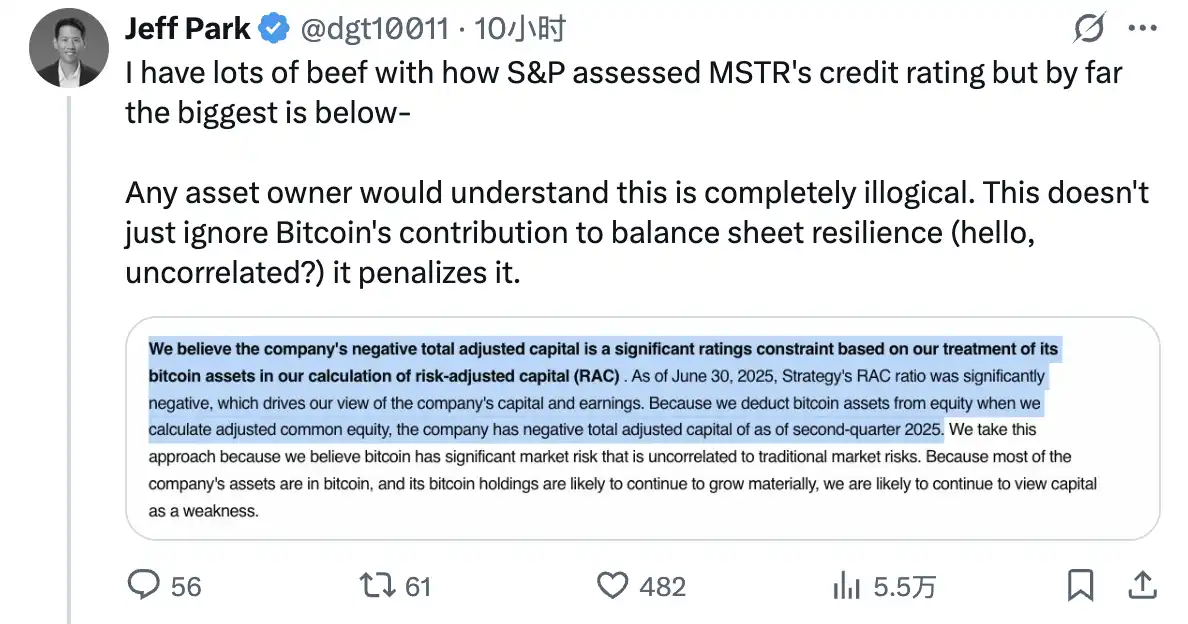

Furthermore, based on S&P's treatment of Bitcoin assets in calculating Risk-Adjusted Capital (RAC), Strategy's RAC is negative, which is a key factor leading to S&P's somewhat negative view of its capital and earnings outlook. S&P explained that in calculating adjusted common equity, it deducted Bitcoin assets from equity because it considers Bitcoin to have significant market risk unrelated to traditional market risks. Considering that most of Strategy's assets are Bitcoin and its holding size is expected to continue growing, S&P believes that the capital issue will remain a primary weakness for the company.

S&P also mentioned that Strategy had a negative $37 million operating cash flow in the first half of 2025. The company's main source of profit is the appreciation in the value of its held Bitcoin, as its Bitcoin assets do not generate cash flow, and its software business is roughly breakeven in terms of profitability and operating cash flow. In the foreseeable future, S&P believes this situation is unlikely to change.

At the end of the rating, S&P also added the potential for a rating adjustment for Strategy.

Within the next 12 months, a rating downgrade may occur under the following circumstances:

Strategy's capital market financing capability is hindered (either due to a significant decrease in Bitcoin valuation or other reasons); we see an increase in the risk related to managing out-of-the-money convertible bond maturities.

The possibility of a rating upgrade within the next 12 months is low. In the long term, a rating upgrade may happen under the following conditions:

Strategy has significantly improved its US dollar liquidity; reduced the use of convertible bonds; and has been able to maintain strong capital market financing capability even in the face of pressure in the Bitcoin market.

Strategy and Market Reaction

In response to the clearly negative bias in the rating given by S&P, Strategy was overwhelmingly optimistic.

Strategy's founder, Michael Saylor, featured the related news prominently on his personal Twitter account, celebrating that "Strategy has become the first digital asset treasury company to receive a rating from a mainstream credit rating agency."

However, some financial institutions deeply involved in the cryptocurrency field were not very satisfied with S&P's rating.

Matthew Sigel, Director of Digital Asset Research at VanEck, stated that while Strategy's business model is indeed vulnerable to (price volatility) shocks, the company's current solvency is not in question.

Jeff Park, an advisor at Bitwise, had a more direct opinion, believing that S&P's calculation method for Strategy's Risk Adjusted Capital (RAC) is unreasonable. The core business of Strategy is to hold appreciating assets such as Bitcoin, so it does not make sense to deduct Bitcoin assets from capital.

Overall, although cryptocurrency has begun to gradually integrate into the traditional financial world, there are still many frictions surrounding issues such as accounting methods and rating treatments. These contradictions will require more time to collide and resolve.

What is worth celebrating at present is that digital asset treasury companies have opened the doors to mainstream rating agencies, as getting a rating is often a necessary step for many pension funds and other institutional investors to enter the investment scene. While Strategy is currently rated as "junk," there is still potential for an upward revision, which may be an opportunity to attract more new capital.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia