Forum

Forum OPRR

OPRR Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

Not Compensating Domestic Victims, How Much Money Did FTX's Bankruptcy Lawyer Make for Himself

On July 4, 2025, Sunil, the representative of FTX's creditors, posted a screenshot of an FTX bankruptcy liquidation document on social media. The document indicated that FTX would seek legal advice and that if users were from a restricted foreign jurisdiction, their claim funds might be confiscated.

Sunil also revealed a piece of data: 82% of the claim funds from "restricted countries" came from Chinese users.

However, because cryptocurrency trading is not allowed domestically, these users may be classified as "illegal," thereby forfeiting their claim eligibility. This means that these users not only cannot recover their losses, but their assets will also be "legally confiscated."

The community erupted in anger, questioning the liquidation team's compliance justification as merely a scapegoat. Some have referred to FTX's decision as "American-style robbery," lamenting that "Chinese people are worse than dogs," expressing profound disappointment and helplessness between the lines. Some believe that despite China's strict restrictions on cryptocurrency trading, user funds should not be directly confiscated, and FTX's decision lacks clear legal basis.

Following such a statement that could reshape the global understanding of creditors' rights, what the outside world is most concerned about is not only whether FTX is "acting in accordance with the law," but also who is making the decisions, based on what standards, and who ultimately benefits.

Who is Taking Over?

Taking over this ruins is a bankruptcy restructuring team from Wall Street: led by restructuring veteran John J. Ray III as CEO and spearheaded by the longtime law firm Sullivan & Cromwell (hereinafter referred to as S&C), forming the liquidation team.

John J. Ray, a seasoned professional in handling corporate carcasses. He previously took over the Enron bankruptcy case, bringing nearly $700 million in revenue to S&C in that "Trial of the Century."

This time, he, with the same legal team, took on FTX.

A high salary is not the issue; the question is, how high is too high? According to public records, S&C partners command an hourly rate of up to $2000, and John Ray himself charges $1300 per hour. According to Bloomberg's data, as of early 2025, in the FTX Chapter 11 bankruptcy proceedings, S&C has accumulated declared legal service fees totaling $249 million.

The asset that should have belonged to all the creditors is being sliced away piece by piece by a "professional team." This is also why FTX creditors have been accusing: "They are replaying the Mt. Gox playbook."

What also feels eerie is the speed at which FTX announced bankruptcy. It wasn't until the full transcript of SBF's congressional testimony was leaked that we found out how he was "hunted" in the two days leading up to the bankruptcy filing.

A draft of the testimony prepared by SBF (Sam Bankman-Fried) to be submitted to Congress reveals that FTX.US's General Counsel, also from S&C, Ryne Miller, closely collaborated with the liquidation team, forcing SBF and his management to swiftly enter Chapter 11 bankruptcy proceedings.

SBF wrote in the testimony, "People from Sullivan & Cromwell and Ryne Miller sent me a lot of threats; they even harassed my friends and family... Someone came crying to find me."

But he had no chance to turn back. The five emails he sent were never replied to by John Ray.

He was just the first character in this elaborate looting.

The bankruptcy application was pressed amidst overnight bombings, panic, and isolation. He had intended to continue fundraising, trying to turn things around, but was prematurely ousted from the stage by the legal counsel he had brought in.

And the real game—about who will take over this company, who will take a piece of its legacy—has only just begun.

Who is Carving Up FTX's Legacy?

The disposition of FTX's historical investment portfolio by this bankruptcy liquidation team is enraging and perplexing.

These portfolios were once vital pieces in SBF's layout of the "effective altruism" dream and were also considered a valuable reserve for FTX's resurgence, but they were almost entirely liquidated by the John Ray team in a "fire-sale" manner, with most sale prices far below their true value.

These three most glaring transactions are enough to glimpse the absurdity of the entire liquidation:

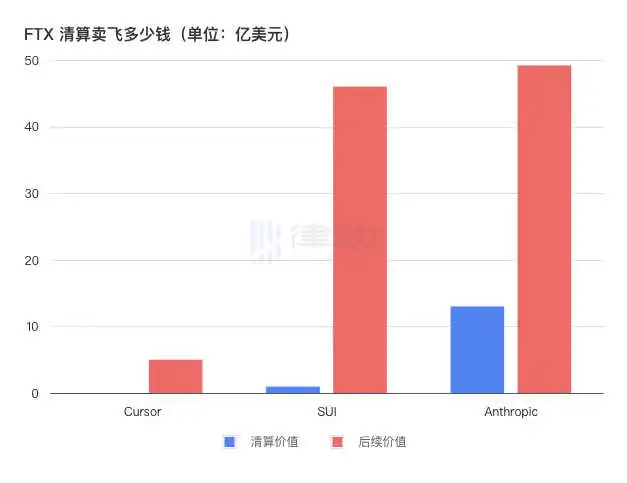

1) Cursor: A $200,000 investment exchanged for a $500 million sigh

Cursor, hailed in the AI circle as the "Vibe coding artifact," received a $200,000 seed round investment from FTX, sold at the original price during liquidation. While it may seem like no loss on the surface, considering Cursor had been reported by prestigious media such as TechCrunch and Bloomberg to have a valuation of up to $9 billion, the sale price can be described as outrageous.

Based on conservative estimates, FTX could have reclaimed at least a $5 billion-level equity return but instead relinquished it under the operation of the legal team. The industry even saw ironic comments such as "BitTrump makes money faster," directly pointing to this asset being "specially dumped".

2) Mysten Labs / SUI: Selling a $46 Billion Public Chain Dream for $96 Million

Mysten Labs and its developed SUI chain, hailed as the next Solana, have extremely high public chain scalability.

FTX acquired Mysten's equity and 8.9 billion SUI tokens for approximately $100 million in 2022, but the liquidation team disposed of this asset in 2023 for $96 million, citing "fast fund retrieval."

At its peak, the value of this batch of SUI tokens once exceeded $46 billion, meaning that the $96 million at the time was only equivalent to 2% of the future value.

The community once joked that if SBF saw the SUI price while in prison, he would probably be furious.

3) Anthropic: Selling a $615 Billion Behemoth for $13 Billion

Anthropic, founded by a former OpenAI executive focusing on AI safety, received a $500 million investment from SBF, holding approximately 8% of the shares.

The liquidation team sold all the shares in two installments in 2024, totaling $13 billion in return. Initially considered a decent cash-out performance by the public, less than a year later, Anthropic's valuation surged to $615 billion. Therefore, FTX's 8% stake was worth close to $50 billion.

This means that the bankruptcy liquidation team missed out on at least an additional $37 billion in returns.

FTX's investment vision was correct, which almost no one would deny. They took the shot before the trend arrived, invested in these companies at their most overlooked moments, and obtained core stakes.

However, after FTX collapsed, these bets were treated as scrap metal.

In addition to these three typical cases, the FTX liquidation team also caused huge controversy by consistently executing "fire sales" in transactions such as LedgerX, Blockfolio, and bulk SOL token auctions.

For example, during the 2024 liquidation auction of SOL tokens, institutions like Galaxy Trading and Pantera Capital swept up tokens at a low price. Subsequently, the price of SOL skyrocketed, allowing them to cash out with incredible profits, while the original creditors could only watch as the opportunity slipped away. According to reports from the Financial Times, Cointelegraph, and others, FTX is believed to have missed out on potential appreciation of tens of billions of dollars in the disposal of quality assets.

Why did this concentrated and rapid "liquidation dump" occur? John Ray's explanation was to "secure funds promptly and avoid price volatility." However, industry analysts pointed out that such a reason cannot explain why the significant discounts were only offered to familiar institutional friends and why many assets saw a substantial increase in value in less than six months.

Conspiracy theories emerged, suggesting that the liquidation team quickly sold all the good assets to friendly funds, allowing themselves to collect exorbitant legal fees, settle cases swiftly, and ultimately make a huge profit. Assets that originally belonged to creditors were, under the guise of "fair and compliant" practices, transferred at a low price to those closer to the centers of power.

The value of the shares, tokens, and options that were sold off cheaply continues to grow, while those who should have enjoyed this growth can only watch as their future is seized by others through publicly disclosed PDFs.

Bankruptcy Liquidation or "Legal Plunder"?

No industry is better at forgetting than the cryptocurrency industry. The market has now re-immersed itself in the pursuit of AI, stablecoins, and RWAs. The crisis of 2022 seems to have passed, but this liquidation process is far from over.

Over the past three years, FTX's assets have been meticulously dissected, packaged, and auctioned off, stripping the platform of all its future, leaving behind only a shell.

The scale and complexity of FTX's bankruptcy liquidation are sufficient to be recorded in the global crypto history books, but what is truly worth recording in textbooks is the collective disillusionment of creditors towards the legal trust system.

On one hand, the liquidation legal team represented by John Ray and S&C legally received astronomical rewards, almost immune to judicial accountability. On the other hand, they protected themselves through indemnity clauses, meaning they would not be held responsible even if they were accused of "malicious liquidation" in the future.

For the tens of thousands of retail investors who were plundered by FTX's bankruptcy, this is not redemption but a second injury. You might have missed the market trend, but being deprived of the opportunity for fair recovery is the most brutal outcome.

Currently, the FTX bankruptcy estate is expected to be globally liquidated with a total amount of $145 billion to $163 billion. However, if users from regions such as China are ultimately unable to successfully claim their assets, it will signify another unresolved tragedy: some individuals will be completely excluded from the legal system, while their funds will be consumed by the intricate procedures of the law and the gray areas of bankruptcy lawyers.

What's more, hidden within the new proposal submitted to the bankruptcy court by the FTX team is a provision absolving advisors of liability, making it nearly impossible for creditors to sue or appeal.

Perhaps for the industry, FTX's collapse is just another trough in the cycle, but for those trapped in it, especially the tens of thousands of Chinese retail investors, this is not only a loss of funds but also the end of hope.

Those dubbed the "professional liquidation team" of lawyers and advisors can now determine the fate of billion-dollar assets with just a few lines, leaving no opportunity for these ordinary investors to overturn the situation.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia