SemiAnalysis Insights: Meta Signs Contracts for Over 5GW in Six Months, Potential Misdirection with "Cloud Business" Sell-Off

TL;DR

· In the first half of the year, Meta secured over 5GW of capacity in the cloud and hosting, excluding self-built data centers with synchronous acceleration.

· Additional computing power could be directed towards MSL training, ad recommendations, Claude private instances, and short-term high-value external transactions.

· CoreWeave, Nebius's RPO may benefit, but MSL catch-up and contract flexibility remain risks.

The Neocloud sell-off sparked by Meta may have been a misstep. A report by SemiAnalysis on July 2 stated that in the first half of 2026, Meta had signed contracts for over 5GW of IT capacity in the cloud services and hosting sector, a figure that does not include self-built data centers with synchronous acceleration.

This is contrary to market concerns in recent days. According to Bloomberg on July 1, Meta is developing a cloud business to sell excess AI computing power, with plans still evolving and strategies possibly changing. Following this news, stocks of Neocloud companies like CoreWeave and Nebius experienced a sell-off as investors worried that Meta, once a major customer, could now become a potential competitor, leading to a rapid oversupply of AI data center capacity.

The main argument presented by SemiAnalysis offers a different interpretation: Meta is not reducing outsourcing but is obtaining capacity faster through third-party Neocloud providers. Since early 2024, Meta has accumulated contracts for nearly 10GW, with most of the new capacity still being achieved through third parties. For suppliers like CoreWeave and Nebius, Meta's orders may actually continue to raise their remaining performance obligations (RPO).

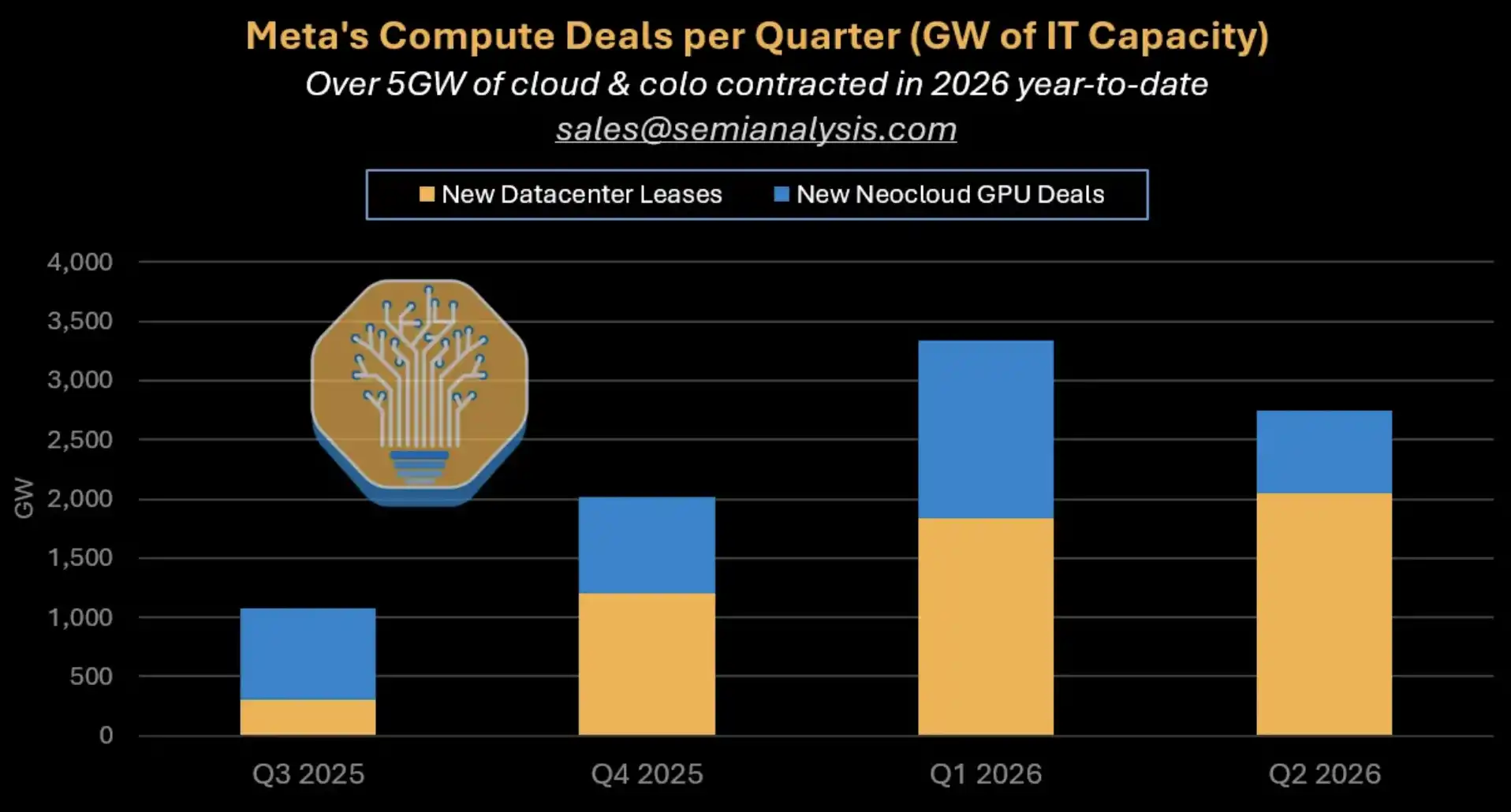

Meta Quarterly Computing Power Transaction Breakdown: Cumulative 5GW+ Cloud and Hosting Contracts in the first half of 2026, distinguishing between new data center leases and Neocloud GPU transactions.

Market Concerns about Meta Selling Off Capacity, Report Sees a Larger Buyer

The crux of this controversy is not whether Meta will engage in cloud computing power resale but rather which entity will actually build, absorb, and bear the revenue risk of the massive influx of computing power.

If Meta is merely subleasing GPUs and becomes a roughly 30% gross margin bare-metal IaaS provider, concerns in the market about the valuation of Neocloud are justified. When major customers switch to become suppliers, the bargaining power of existing providers weakens, potentially leading the industry into a phase of low-price competition.

However, within SemiAnalysis's framework, Meta's additional capacity looks more like an "optional computing power pool." It can be allocated between internal cutting-edge models, ad recommendations, enterprise-grade model services, and short-term high-value external transactions, rather than just being able to sublet GPUs at a low price.

This is also a key point in refuting the claim that "only 5GW of data centers are under construction in the U.S." Just Meta's two largest under-construction campuses alone correspond to approximately 2.5GW of capacity. When third-party cloud and hosting contracts are added on top, the actual construction intensity is higher than some pessimistic estimates.

To put it more directly, the market now needs to assess not whether Meta will buy computing power, but whether this much capacity can be absorbed by high-value scenarios.

Four Paths to Absorb Additional Computing Power, MSL Not the Only Outlet

The first priority for Meta's additional computing power is still Meta Superintelligence Labs, or MSL, used for cutting-edge model training. This is the most direct capital expenditure narrative: for Meta to catch up with OpenAI and Anthropic, it needs a large enough training cluster, talent, and room for trial and error.

But even if MSL's progress does not fully meet expectations, Meta does not have to only rent out GPUs at a low price.

The second path is the ad recommendation system. Meta's official financial report shows that in the first quarter of 2026, ad impressions increased by 19% year-on-year, while the average unit price increased by 12% year-on-year. Meta Engineering previously explained that the GEM-related training stack effectively increased FLOPs by 23 times, MFU by approximately 1.43 times, and GPU scale expanded by 16 times; after doubling GEM's training GPUs, the conversion rates of Instagram and Facebook Feed ads increased by 5% and 3%, respectively.

This path is easier for investors to understand: if more computing power can improve ad conversion rates, it is not just about "burning money to buy GPUs," but rather a part of ad revenue and pricing capability. As for the magnitude of improvement in some of the ranking indicators mentioned in the report, publicly independent metrics are limited and are more suitable as SemiAnalysis model assumptions rather than facts that have been fully confirmed by Meta.

The third path is the model service platform, similar to AWS Bedrock or Google Vertex. SemiAnalysis states that Meta is in negotiations with Anthropic regarding Claude private instances and is trying to build a "token-as-a-service" platform. This type of capacity can be used internally as well as for SaaS sales and external distribution, but such transactions still need to be viewed as "potentially materializing" and cannot be considered realized revenue.

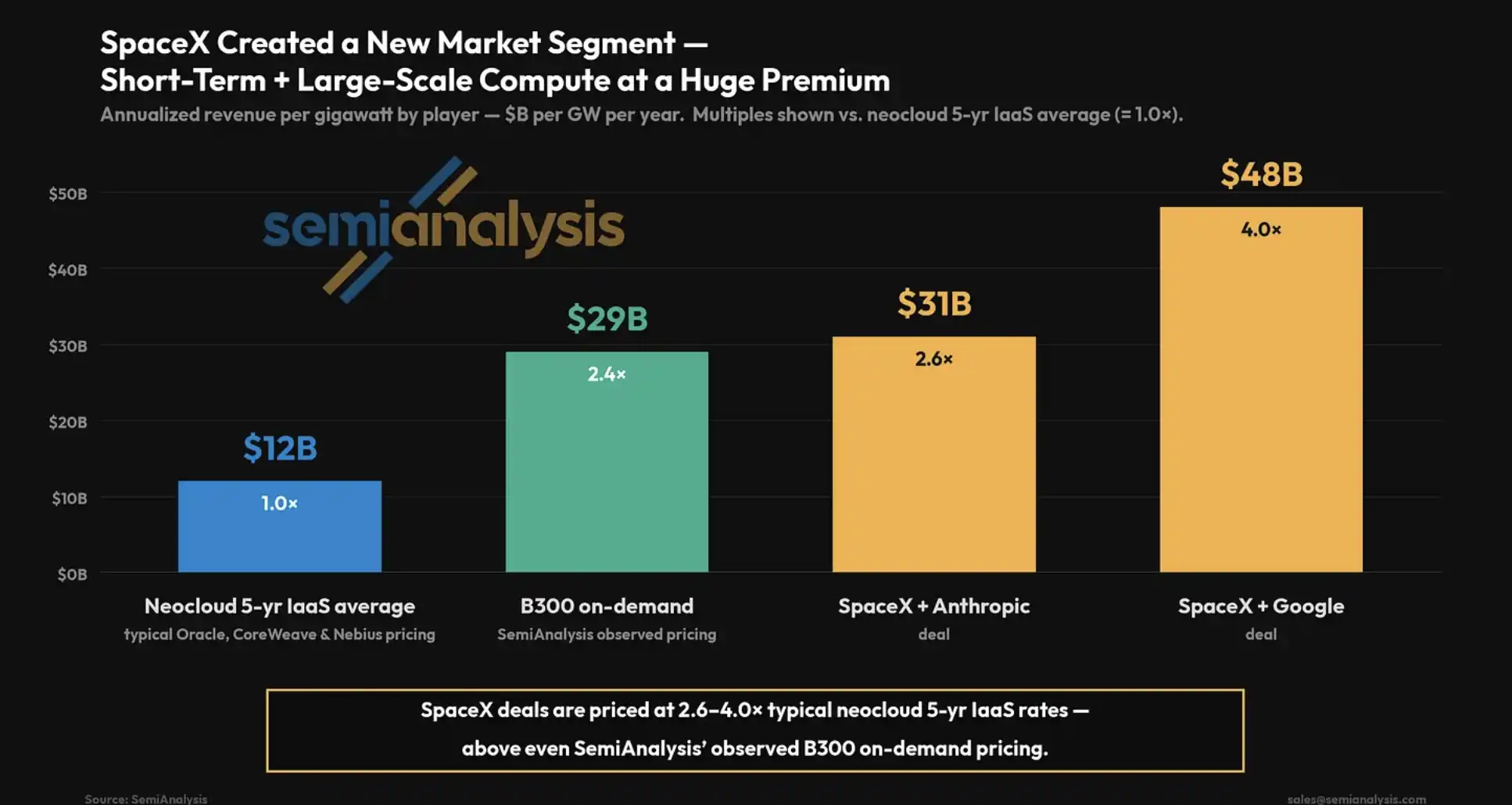

The fourth pathway is a large-scale, short-term, high-premium on-demand compute trading model similar to SpaceX. This is also the most impactful set of numbers in the report.

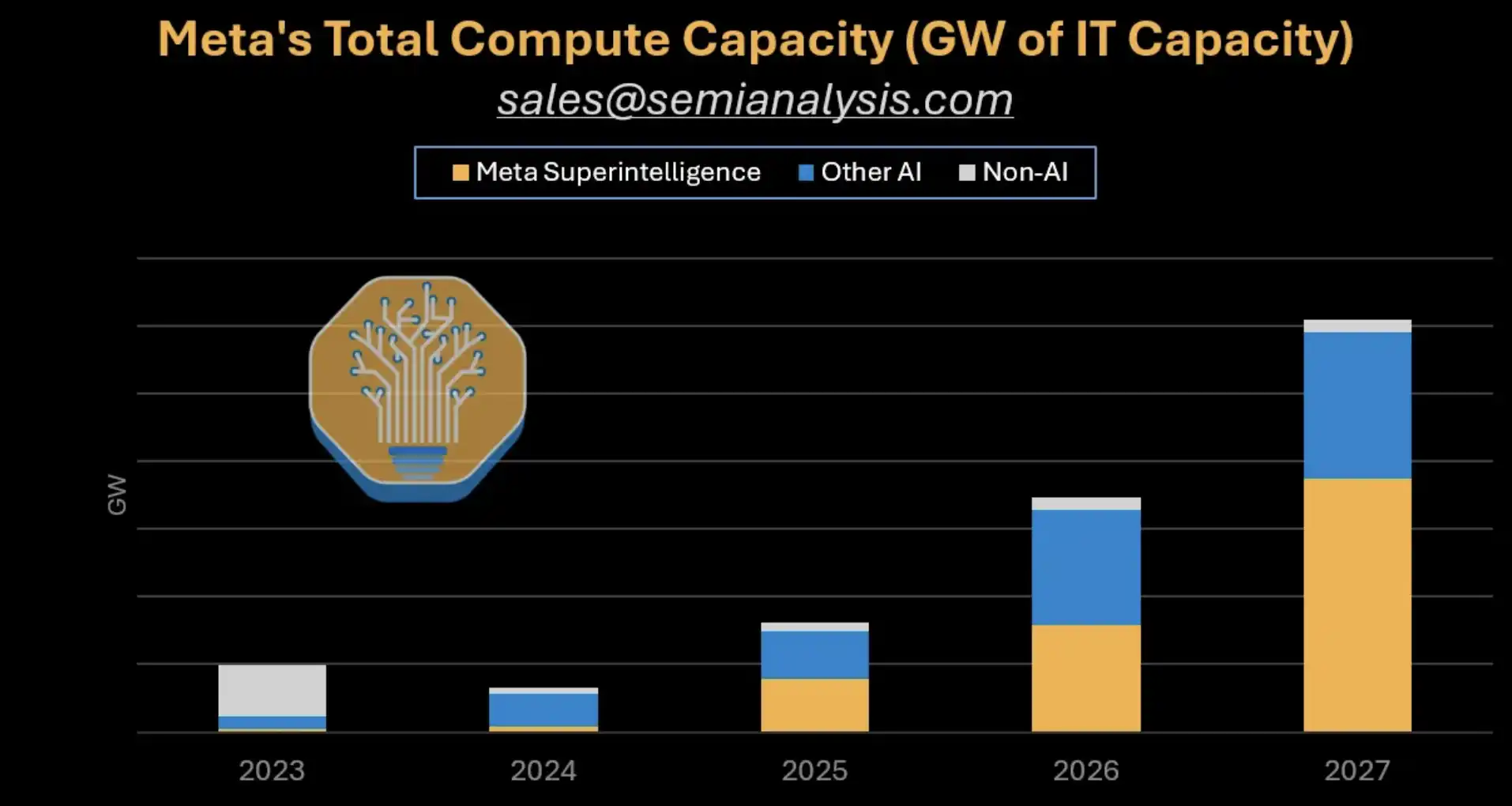

Meta's total compute capacity forecast: A stacked bar chart from 2023 to 2027 distinguishing between MSL, Other AI, and Non-AI, with a significant capacity expansion in 2026 to 2027.

High-Premium Short Orders are Changing the Revenue Narrative of "Selling Compute"

The key to SpaceX-style trading is not just "renting GPUs" but rather a different pricing and contract structure.

According to SemiAnalysis, the annualized revenue per GW traded between SpaceX and Anthropic is approximately $3.1 billion, which is 2.6 times the average five-year IaaS price of Neocloud. The trade with Google is even higher, at around $4.8 billion/GW/year, equivalent to 4 times. Independent publicly available sources have limited confirmation of these contract details, making these numbers more suitable as a report scenario to illustrate the possibility of a high premium for short-term scarce compute.

If Meta were to only allocate 200MW for similar external trades, based on the calculations on a public page of the report, the annualized revenue could exceed $10 billion. This scale is enough to alter the market's intuition about "Meta's external compute sales." It may not necessarily be a low-margin subleasing operation, but could also involve selling time windows of quickly onboarded data center capacity to top-tier customers in urgent need of compute power.

The report also mentions that Meta's rapidly onboarded data center design is tailored for such trades. Its value lies not in the lowest-cost long-term leasing, but in the ability to deliver more quickly when model companies, AI applications, or large clients temporarily need extensive compute power.

However, this is still an optional pathway, not a guaranteed revenue stream. Meta's ability to replicate parts of the high-premium trading structure does not mean it has already transformed into a SpaceX-style compute seller.

SpaceX Pricing Premium Comparison: Typical Neocloud five-year IaaS at around $1.2 billion/GW/year, SpaceX with Anthropic at around $3.1 billion, SpaceX with Google at around $4.8 billion.

CoreWeave, Nebius—Pressure Doesn't Necessarily Arise from Demand Disappearance

For companies like CoreWeave and Nebius in the Neocloud ecosystem, the market's previous concern was: if Meta self-builds or resells computing power, the original external procurement would decrease, and industry orders could be diverted.

However, from existing contracts, Meta is still accelerating its use of third-party Neocloud. Public information shows that CoreWeave has a $21 billion contract with Meta, and Nebius has a contract with Meta worth up to $27 billion. In Nebius's Q1 2026 shareholder letter, it mentioned signing a second major deal with Meta, with a contract capacity exceeding 3.5GW, and referenced commitments from Microsoft and Meta customers.

Meta is willing to pay a premium for speed, which is also a reason why third-party suppliers are still valuable. As long as Meta believes that computing power can be absorbed by MSL, the advertising system, model services, or short-term high-value transactions, there is a reason to let Neocloud build the cluster first, rather than wait for self-built projects to be delivered slowly.

"Overcapacity" cannot only be seen in the total GW number. The truly scarce part of AI data centers is often not the theoretical power but the available GPUs, network, data center delivery speed, customer migration costs, and contract flexibility. If Meta needs to quickly obtain production capacity, third-party Neocloud is still useful.

This does not mean that Neocloud companies are without risks. Their valuation still depends on customer concentration, financing costs, GPU depreciation, long-term contract quality, and whether customers will actually take up future capacity. If Meta's RPO growth corresponds to high capital expenditures and high customer concentration, the market will still discount them.

If MSL Falls Behind, 5GW Will Become a Capital Expenditure Pressure

The most critical aspect of this report is to not portray every optional path for Meta as already successful.

There is still considerable uncertainty about whether MSL can catch up with OpenAI and Anthropic. The competition for cutting-edge models cannot be solved solely by GPU quantity; data strategy, research teams, training stability, product distribution, and inference costs will all affect the outcome.

Contract terms will also affect the size of the risk. SemiAnalysis stated that transactions similar to SpaceX usually include 90-day mutual cancellation clauses. This arrangement gives both parties flexibility: if a team is not making progress, computing power can be quickly reallocated; if there is a change in demand, it will not be locked in long term. Details of such clauses lack publicly verifiable independent confirmation and are more suitable for consideration as report assumptions.

For Meta, flexibility is valuable in itself. It can initially allocate enough power and GPU to MSL for cutting-edge experiments, while redirecting some capacity to ad recommendations, Claude private instances, or high-priced shorts.

Conversely, if Meta ends up signing a large number of long-term compute deals without flexible exit arrangements, the risk increases. If the cutting-edge models fail to deliver as expected, and ad and model services cannot absorb the additional capacity, over 5GW of new outsourced compute power could directly translate into capital expenditure pressure.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia