Rising Ever Higher: The Systemic Risk Behind SpaceX's Soaring Valuation

Original Title: SpaceX Could Get Dangerously Systemic

Original Author: Quoth The Raven

Translation: Peggy, BlockBeats

Editor's Note: After SpaceX's post-market valuation surpassed $3 trillion, this article raises a sharper question than "how much is it really worth": when a company can increase its market value by hundreds of billions of dollars in a single day due to the combined effect of limited float, options trading, and market sentiment, is the capital market still conducting price discovery, or has it turned into a self-reinforcing speculation machine?

The author's core judgment is not to deny SpaceX's business prospects. SpaceX may still be one of the world's most important space infrastructure companies and may have a high long-term growth potential. However, the real focus of this article is on another matter: if the stock price is mainly driven by call options buying, market maker hedging, momentum fund chasing, and passive fund allocation, then valuation is no longer just about "reflecting value" but starts to "create value." Price appreciation itself becomes a new reason to be bullish, while fundamentals are pushed to a secondary position.

The repeatedly mentioned gamma squeeze (market makers being forced to buy stocks due to hedging, further driving up the stock price in a feedback loop) is key to understanding this article. Over the past few years, similar mechanisms have repeatedly appeared in Tesla, some meme stocks, and high-momentum tech stocks. The author is concerned that if SpaceX follows this path, and continues to rise due to its own narrative intensity, float restrictions, and Musk's personal influence, it could transition from an overvalued stock to a systemic variable in the entire market.

The more dangerous part lies in indexing and passive investing. When a company's market capitalization is large enough, it will be included in major indices and passively held by ETFs, pension funds, retirement accounts, sovereign wealth funds, and institutional portfolios. At this point, the bubble is no longer just a few traders' gamble but enters ordinary investors' long-term asset allocations. The higher it rises, the harder the market can avoid it; and the harder the market avoids it, the more likely funds will continue to flow into it.

Therefore, this article is not really about whether SpaceX will become a $5 trillion or $10 trillion company, but about a structural paradox in modern capital markets: when market mechanisms themselves can amplify narrative, leverage, and liquidity to the point of overwhelming fundamentals, can the so-called "price discovery" still hold? SpaceX is just an extreme case, but the issues it exposes may be more widespread—in today's US stock market, systemic risk sometimes does not start from bad companies but from the most popular, most undeniable companies.

The following is the original text:

“Things can only get weirder and weirder and weirder, until finally, they’re so weird people have to start discussing: Just how weird is it, anyway?”

——Terence McKenna

For the past few years, I've been asking: How absurd do things have to get before we admit that the stock market is fundamentally broken? Seeing SpaceX's surge in after-hours trading today, the answer seems pretty clear to me: the market has long been broken. The real question is just how ridiculous things have to get before everyone else notices.

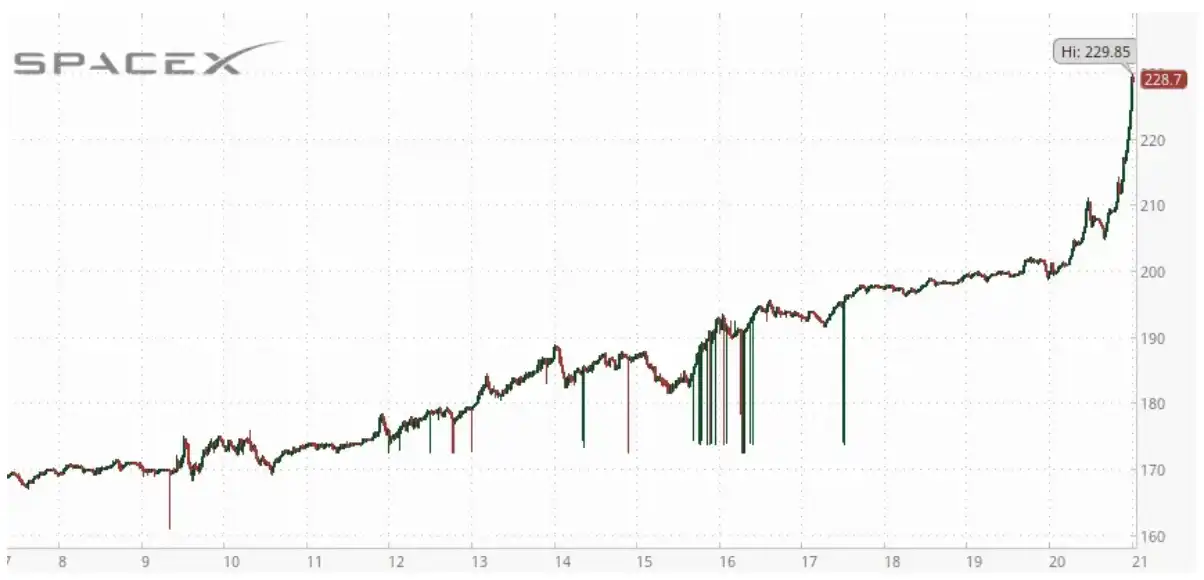

In after-hours trading, SpaceX's market value crossed $3 trillion. This means its valuation has now exceeded that of Amazon and Microsoft. Microsoft generates hundreds of billions of dollars in revenue annually, with annual profits exceeding $100 billion. Amazon has annual revenue of over $700 billion and profits in the billions. And now, SpaceX has been given a higher valuation than them.

SpaceX's relatively limited float makes it a prime target for a manipulative short squeeze. As the after-hours trading neared its end, its stock price briefly surged to nearly $230 per share. In a single day, a company that still loses billions of dollars annually magically added around $650 billion in market value.

$650 billion. Not in a year. Not in a decade. Just one day. And tomorrow, SpaceX options will start trading. As I predicted before, I bet it could be pushed even further into a short squeeze.

And that's where the real unease sets in. Because I've been writing for years: when options activity starts to become the main driver of price action, what happens to the market.

We've seen this play before: call option buyers pile in, market makers are forced to hedge, stock goes up, momentum traders chase, more call options are bought, and the loop goes on, reinforcing itself.

As of 10:30 a.m. Eastern Time, on SpaceX options trading debut day, over 500,000 contracts have been traded, representing a notional size of about 50 million shares.

At a two-day expiration with a strike price of $380, the out-of-the-money call options—currently the deepest out-of-the-money contracts available to buy—are the second most popular strike among this week's expiring call options and were briefly the hottest strike in early trading.

At some point, price no longer reflects value but starts creating value. Valuation itself becomes the bullish thesis. The company's industry attributes and fundamentals become entirely irrelevant. This is when the market officially starts doing what it shouldn't.

That's why tomorrow is so important. Because a company that has already displayed strong short squeeze characteristics will begin options trading. And its "sister company" has experienced a similar situation before.

For the past few years, I have been writing that the modern market is increasingly driven by mechanical forces rather than by fundamental analysis. Tomorrow may become one of the clearest examples of this trend.

My expectation is that the launch of SPCX options trading will not improve price discovery, but rather further distort it. If aggressive call option buying activity emerges, market makers' hedging behavior could create a self-reinforcing feedback loop, similar to the mechanisms that have driven spectacular yet completely illogical rallies in momentum stocks like Tesla over the past decade.

By then, price movements will have no connection to business fundamentals and will depend entirely on market structure. If SpaceX does indeed experience the kind of gamma squeeze that many traders anticipate, I believe this will further demonstrate that the modern market has become utterly useless and incredibly dangerous for the average person's retirement account.

Because the market should be responsible for capital allocation, for facilitating price discovery. It should link valuations—no matter how imperfect—to economic reality. The market should not become a self-reinforcing feedback machine that can add hundreds of billions or even tens of trillions of dollars in market capitalization to a company based solely on mechanical fund flows.

The issue is not whether SpaceX is a good company. The issue is whether the market structure around it is healthy.

Because if a company can become more valuable than Microsoft and Amazon, with only a fraction of their revenue and profit, and potentially surpass Nvidia tomorrow, then where are the limiting factors? What can prevent it from becoming a $5 trillion company? And what can stop it from becoming a $10 trillion company?

Image Source: Zero Hedge Twitter

If the same type of options-driven feedback loop that propelled Tesla to skyrocket after the end of 2019 occurs here, then these numbers are no longer as unimaginable as they once seemed. And that's the part that no one is willing to discuss.

Everyone wants to discuss how high SpaceX can still rise. No one wants to discuss: what happens if it actually reaches that level.

If SpaceX's market cap reaches $10 trillion, it would mean that one company's valuation is approximately one-third of the U.S. GDP. It will be large enough to dominate passive indices, retirement accounts, ETFs, pensions, and institutional portfolios. Its every move will increasingly dictate the overall market performance—and at the same time, it hasn't even turned a profit yet. It will become the greatest and most dangerous speculative machine in human history.

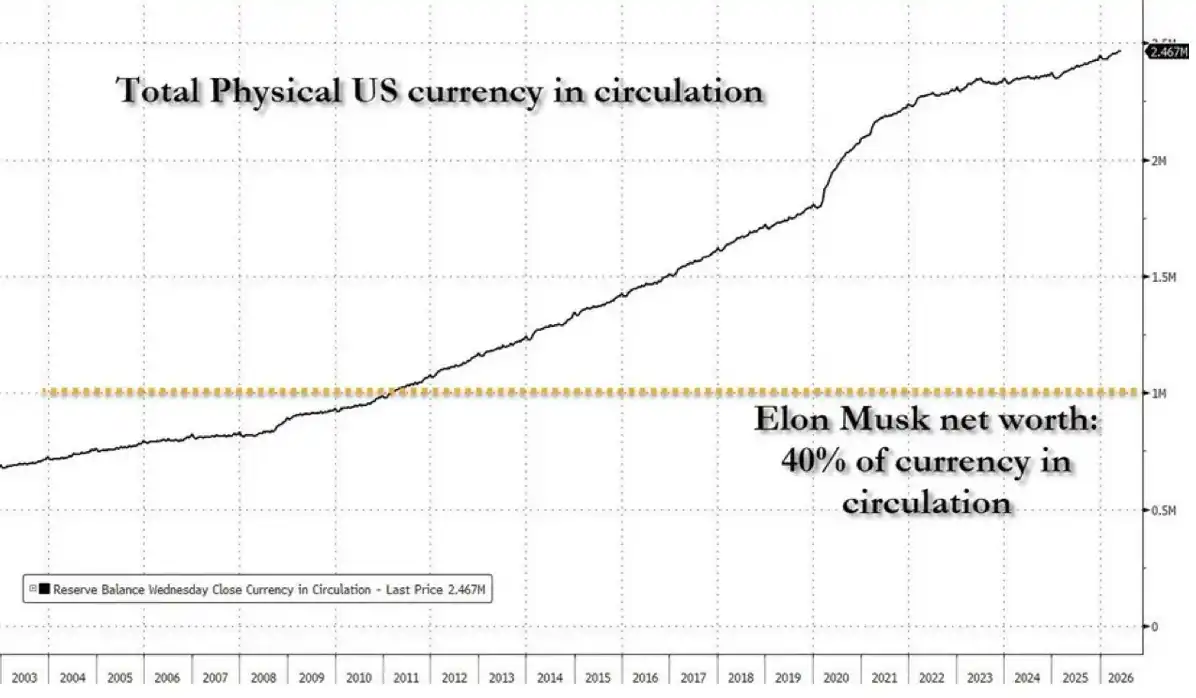

Think again about what this means for Elon Musk. If SpaceX were to reach a $10 trillion valuation, Musk's personal wealth would enter a territory unseen in modern history. His net worth already equals about 40% of the total money supply in circulation.

Image Source: Zero Hedge

Moreover, he wouldn't just be wealthier than the second richest person. He could soon be about ten times richer than the second wealthiest individual.

The gap between Musk and other billionaires could surpass the total wealth of some developed countries. At that point, we would no longer be discussing wealth creation in the conventional sense.

If SpaceX's market cap were to somehow skyrocket to $28 trillion due to a gamma squeeze event, what would happen? That would roughly equate to the annual economic output of the United States. Would people finally begin to question the market at that point? Or would they continue to find new reasons to rationalize it all?

Because that's how every bubble in history has operated. Every new high is taken as evidence that the previous high was too low. Every speculative mania is packaged as innovation—just ask the so-called "innovation expert" Cathie Wood. Every short squeeze is explained away as brilliance. Every warning is turned into evidence that the skeptics don't understand the future.

The most astonishing thing about SpaceX surpassing a $3 trillion valuation is not the valuation itself.

It's that if it continues to rise, it will become too big to ignore. At some point, we will have to stop discussing SpaceX itself and start discussing the system that created it: a speculative machine completely detached from its original purpose.

The danger is that once a company reaches a big enough size, the distortion itself becomes a systemic risk. Every passive fund must hold it. Every major index will depend on it. Pension funds, retirement accounts, sovereign wealth funds, insurance companies, and institutional portfolios will be increasingly intertwined in the same trade. The higher it goes, the more inescapable it becomes.

This is the part that nobody truly understands.

If SpaceX eventually hits $10 trillion through the combined effects of hype, narrative, mechanical fund flows, and option-driven feedback loops, it will no longer be just a story about SpaceX. It will become the entire market. Its trajectory will increasingly dictate the performance of retirement accounts in indices, ETFs, and the entire financial system. The market will effectively turn into a referendum on a single stock.

And that's how a bubble turns into systemic risk. Not when it's small enough to be laughed off, but when it's big enough that everyone is forced to participate. The same mechanisms driving up prices today will eventually create the unstable conditions of tomorrow. When trillions of dollars of wealth are tied to a valuation that has never been truly anchored in fundamentals, even a moderate pullback could have consequences far beyond the stock itself.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia