Snowflake's stock price has surged by 33%, AI Infrastructure Transitioning from Chips to the Data Layer

Original Title: Snowflake jumps as AWS deal, upbeat forecast lift lagging sentiment

Original Authors: Kanishka Ajmera, Deborah Mary Sophia, Reuters

Translation: BlockBeats

Editor's Note: The narrative of AI adoption is expanding beyond chips and models to the data infrastructure layer.

After facing pressure on its stock price since the beginning of the year, Snowflake surged over 33% in a single day due to raising its full-year revenue outlook and securing a $6 billion five-year partnership deal with AWS. The core of this market reaction is not just the better-than-expected earnings report, but investors starting to reassess Snowflake's position in the enterprise AI implementation chain.

Over the past year, a common question among enterprise software companies has been: Will AI be a growth engine or will it weaken their existing business models? Snowflake's latest performance and AWS partnership provide a relatively clear answer—when enterprises begin large-scale AI deployment, data storage, processing, analysis, and model deployment capabilities become even more critical.

In this collaboration, AWS Graviton chip supply addresses the compute power constraint issue, while Snowflake's platform further integrates with AWS AI workloads, pointing to deeper enterprise needs: companies are not simply "using AI," but they need to plug their data into AI workflows to build operable, manageable, and scalable application systems.

This is also the reason Snowflake is being reintegrated into the "AI winner" narrative. AI software stocks previously experienced a sell-off, with the market full of doubt about "whether AI can truly contribute to revenue." However, Snowflake's case demonstrates that once AI transitions from concept demonstration to actual revenue growth, market sentiment can quickly reverse. With at least 30 analysts raising their target prices, it clearly indicates that the capital market is reassessing the value of data platforms in the AI infrastructure cycle.

Of more significance, this deal also strengthens AWS's presence in the self-developed chip ecosystem. From Anthropic, OpenAI, Meta, Uber to Snowflake, Amazon is embedding itself deeper into AI infrastructure through cloud, chips, and enterprise software collaborations. For Snowflake, this means it is not just an enterprise data warehousing company but is becoming a critical data layer in the enterprise AI application implementation process.

The following is the original text:

The logo of Snowflake Inc. appeared on a banner at the New York Stock Exchange (NYSE) to celebrate the company's IPO.

On May 28, Snowflake's stock price surged over 33% on Thursday. Prior to this, the company had raised its full-year revenue outlook and struck a $6 billion deal with Amazon, boosting investor confidence in its role as a major beneficiary of the AI boom.

This five-year agreement with Amazon Web Services (AWS) will provide Snowflake with crucial AWS Graviton chip supply. Currently, as AI usage is significantly increasing, computing resources are becoming increasingly scarce.

The agreement will also further deepen the integration of Snowflake's data storage, processing, and analytics products with AWS cloud-based AI workloads. As businesses rapidly scale their AI applications, Snowflake is poised to capture more demand. Currently, most of Snowflake's customers run on AWS.

Following the announcement, at least 30 analysts raised Snowflake's target price, boosting the median target price from $230 before Wednesday's earnings report to $280. The stock most recently traded at $233.50 in the premarket.

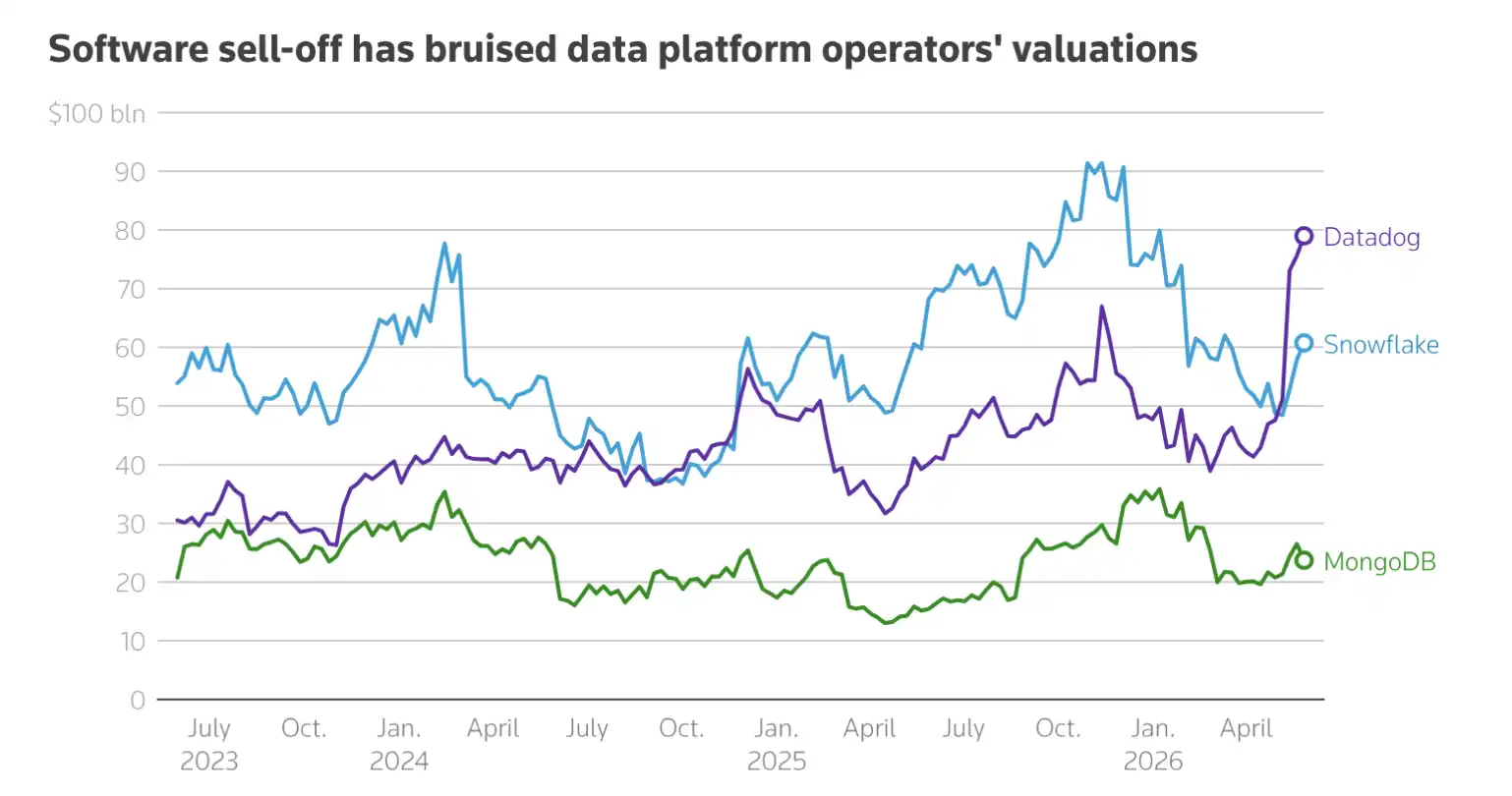

If the current gains hold, Snowflake's market capitalization would increase by around $20 billion from its original $60.75 billion.

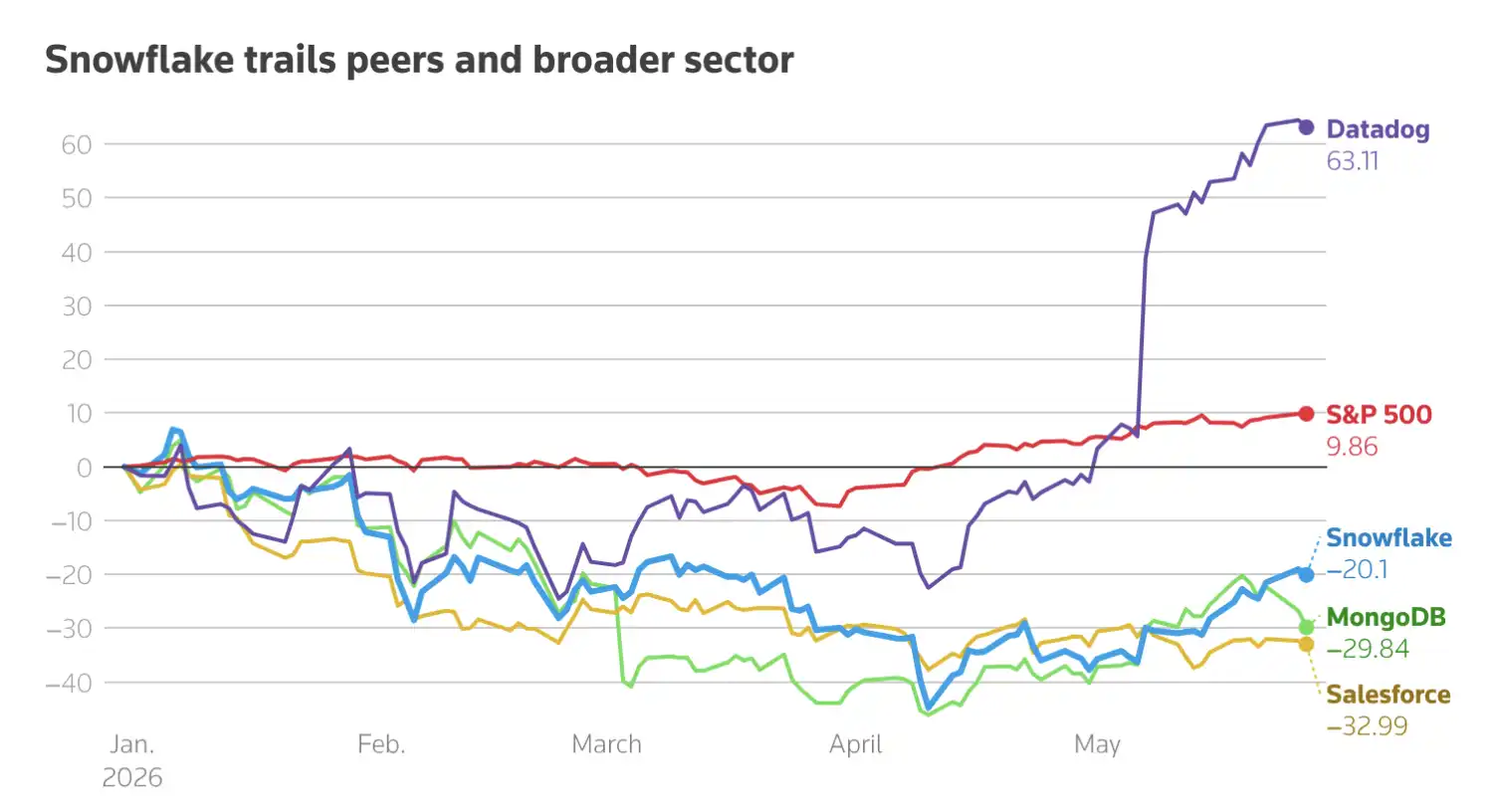

Senior Equity Analyst at Hargreaves Lansdown, Matt Britzman, commented that the significant jump in Snowflake's stock price – which had dropped 20% year-to-date as of the previous trading day's close – "shows just how strong the skepticism built up in the market as data companies have been dragged down by the wider AI software sell-off."

"But it also demonstrates just how quickly sentiment can turn once a company proves that AI is driving revenue growth, not just decorating PowerPoint slides."

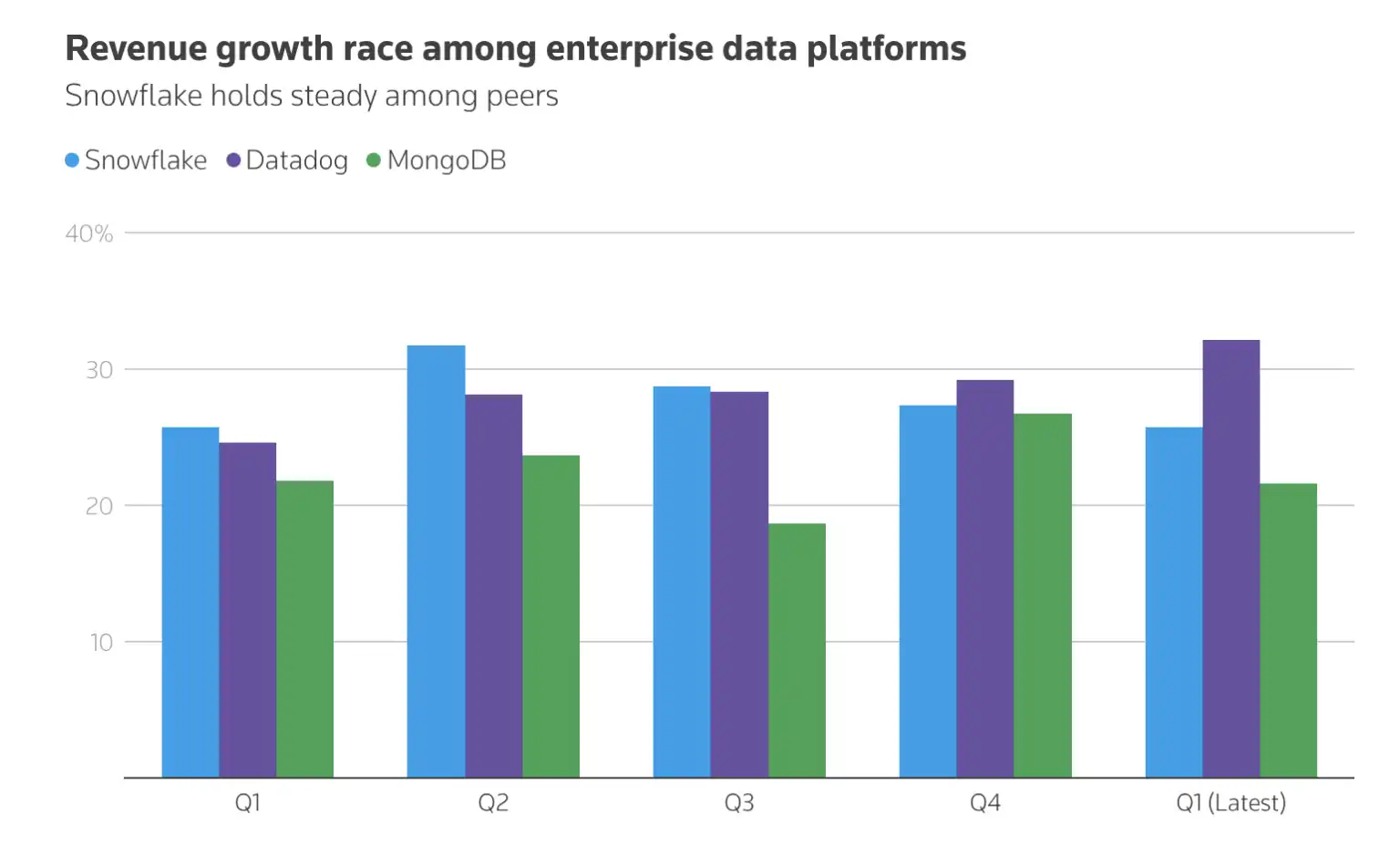

Currently, Snowflake has a forward 12-month P/E ratio of 85.21, compared to Datadog at 85.19 and MongoDB at 47.17. A higher P/E ratio typically indicates that investors are betting more strongly on its future growth.

Previously, the market was concerned that AI would disrupt enterprise software, putting pressure on Snowflake. Now, the company is embedding AI into its platform to help companies integrate data from multiple sources, analyze it, and build AI tools.

"We believe this performance will clearly slot Snowflake into the 'AI winner' camp and justify a higher valuation multiple," said Scotiabank equity research analyst Patrick Colville. He added that this clearly demonstrates Snowflake's benefiting from the growth of enterprise AI adoption.

Snowflake helps companies store, manage, and analyze all data on one platform. Its AI tools such as Cortex Code and Snowpark are seeing strong adoption, enabling companies to build generative AI applications based on their own data and deploy machine learning models.

This deal also once again validates Amazon's in-house chip business. Over the past few months, Amazon has secured deals with several key clients, including Anthropic, OpenAI, Meta (Facebook's parent company), and Uber.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia