A Deep Dive into On-Chain Treasuries: Eight Major Tracks, Who is Rising and Who is Declining?

Original Title: Vaults: The Infrastructure Layer for Institutional Finance Onchain

Original Source: Castle Labs

Original Translation: Jiahuan, ChainCatcher

Vault Classification

This section of the report provides a quantitative analysis of the vault landscape to offer a comprehensive view of the sector and its evolution. We analyze the ecosystem by category, tracking the TVL migration of different vaults and curators.

We dissect curator concentration and provide insights into major fund flows, placing this year's structural shift in vaults into a specific context.

Vaults should not be seen as a singular, all-encompassing market, but should be assessed based on their various implementation methods, each with different parameters, risk vectors, and responses to stress tests. Aggregated data can only provide a partial picture, highlighting the need for a more nuanced analytical perspective.

Before diving into the analysis, it is important to define the term "vault" as the foundation of our methodology.

Our definition is based on the deployment path. Vaults are classified as "tools for users to actively earn yield". Any asset purely wrapped off-chain is excluded from our analysis.

Maple's syrupUSDC meets the vault criteria: users deposit stablecoins into the protocol, which lends them to institutional borrowers, accumulating APY through token issuance credit activity.

Lido's stETH is a vault: users deposit ETH, and the protocol earns staking rewards, which are distributed through a rebase token. Centrifuge's JAAA is a vault: users earn AAA-rated CLO yield through tokenized wrapping, generating revenue from its credit position.

BlackRock's BUIDL does not fall under this vault definition: it involves direct token issuance, representing a 1:1 claim on an off-chain US Treasury bond fund.

We apply this perspective to define eight structural categories: Lending Vaults, Liquidity Pools, Reinvestment Vaults, Risk Curator Vaults, Vault Infrastructure Providers and Yield Optimizers, RWA Credit Vaults, Perpetual Contract LP Vaults, Option Vaults.

For the purposes of this analysis, we treat Risk Curator Vaults as a separate category to better understand their dynamics and growth.

Before delving into each of these categories, let's first take a closer look at the overall performance of the Treasury.

Treasury Ecosystem Overview

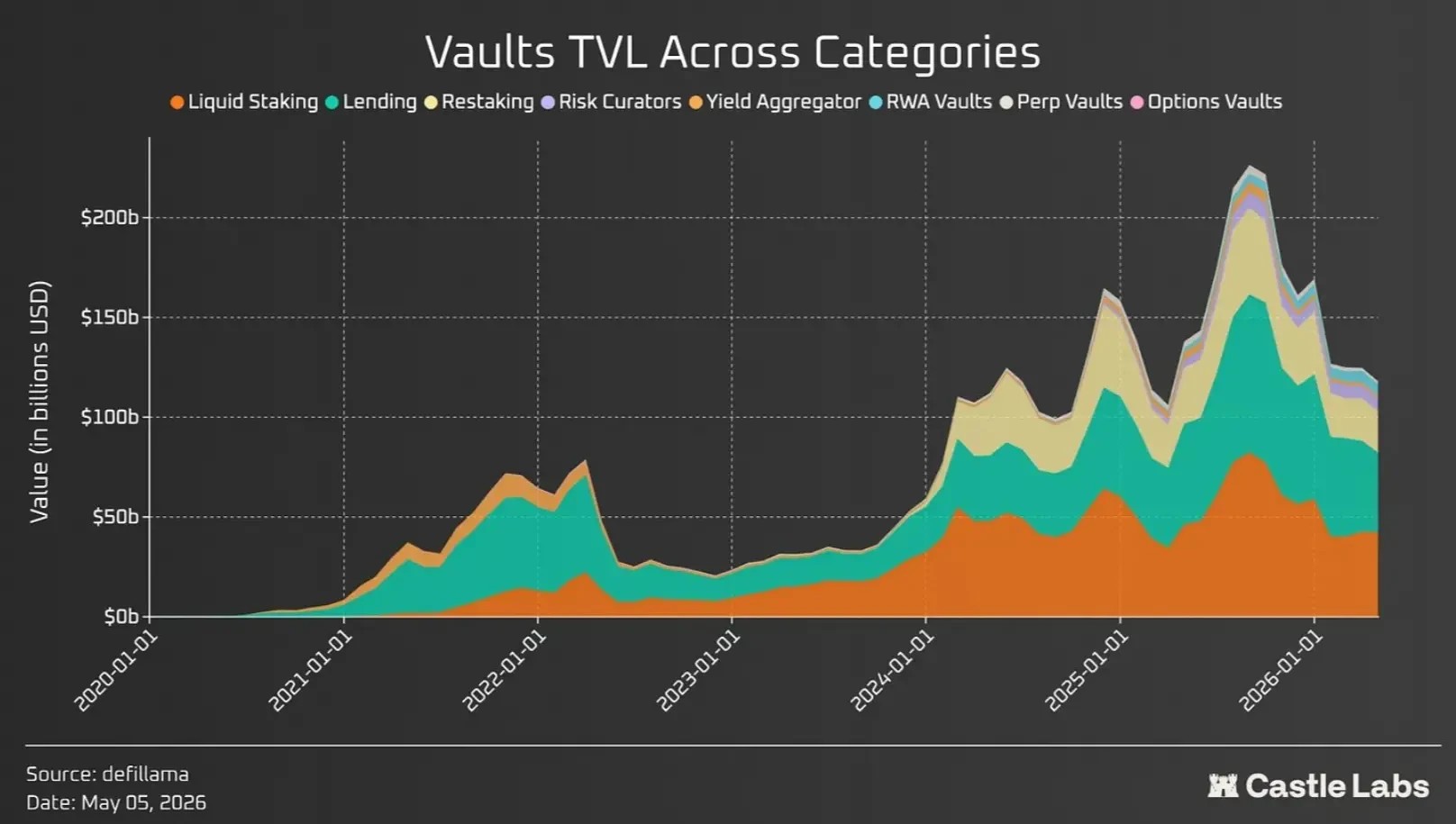

The combined net TVL of all defined Treasury categories is $120.4 billion, down approximately 50% from the peak of around $241.0 billion in October of last year. The downward trend post-October peak was driven by the "October Liquidation Event," which triggered a cascade of liquidations across the entire DeFi space.

Due to overlap, the Treasury TVL figure is higher than the current DeFi TVL (around $86.0 billion). For example, protocols like @LidoFinance have issued stETH, a rebase asset representing staked ETH rewards, which is used as collateral in lending protocols such as @Aave and @Morpho.

If we switch to a category-level analysis, the overall landscape changes significantly. Recent events have led to TVL outflows, prompting a broader reality check across the industry in terms of security and risk management (and a shift towards a security-first approach).

Categories such as Lending, Liquid Staking, and Rehypothecation were hit the hardest as they have the highest on-chain asset exposure and drive on-chain economic activity; while RWA Treasuries, due to their non-crypto asset exposure, continued to show unrelated growth.

Categories like Options Treasuries peaked in April 2022 and have since struggled. Due to the "October Liquidation Event," risk-curated Treasuries suffered a blow similar to other major categories. Their TVL peaked around the end of October and then declined following the Stream Finance collapse.

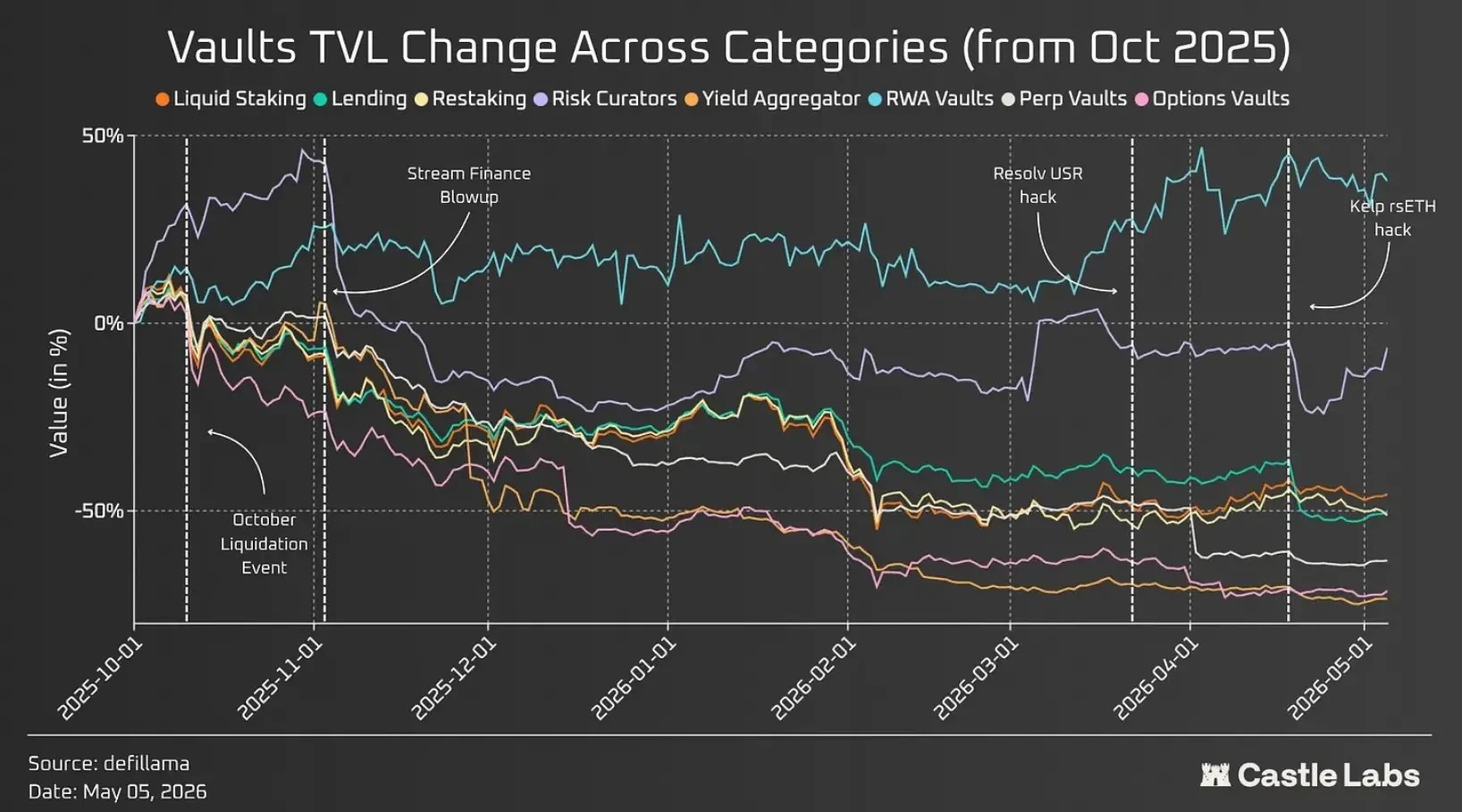

The three events between October 2025 and May 2026 (Stream Finance, Resolv, and Kelp hacks) provided a good stress test window as these collapses/vulnerabilities had cascading effects on the entire DeFi space.

In the chart below, we focus on the TVL history of these categories during this specific period. As mentioned earlier, most performed poorly, with only RWA Treasuries seeing a 37.8% growth during the same period, while other categories experienced significant pullbacks.

Next, we will continue to analyze the growth of each treasury category, focusing on recent trends and shifts.

Lending Treasury

Lending is the largest treasury category, occupying the majority of DeFi TVL. Last year marked a widespread shift towards curated treasuries, driven by products like Morpho that helped expand this trend.

On Morpho, curators can create their own treasury that can be exposed to multiple markets and earn yield for depositors. These treasuries can ultimately be curated by any provider, including traditional financial institutions.

Morpho's recent Vaults V2 upgrade has provided curators with additional features, including the ability to embed batch adapters to source yield from multiple origins, fine-grained risk controls (such as setting absolute or relative limits on treasury risk exposure), built-in KYC controls, and other functionalities.

In a similar vein, Aave also launched its V4 version, introducing a Spokes and a Unified Liquidity Hub architecture. Spokes offer enhanced functionality through custom risk parameters, isolated collateral types, and oracle configurations for each market.

Where it differs from Morpho's curator-led model is that Aave's governance still requires review and approval of these Spokes implementations, while Morpho is permissionless. This marks Aave's shift from monolithic lending to modular lending.

The curator model has seen Morpho amass over $7.5 billion in TVL on the Ethereum mainnet and Base. Base has significantly contributed to Morpho's growth, growing from $604 million to over $2.8 billion.

This demonstrates the power of the distribution partnership approach that Morpho has pursued, such as its collaboration with Coinbase: currently, approximately 40% of TVL in USD terms is cbBTC, while it has facilitated over $1 billion in loans for Coinbase users.

As a response to the curator model finding product-market fit (PMF) among institutional investors, Aave is competing in the institutional track through Horizon, which has accumulated over $3.5 billion in TVL since its launch.

In addition, over the past few months, Aave has seen many changes, including service providers like BGD and ACI leaving Aave Labs, as well as the announcement and approval of the "Aave will Win" framework, allocating all revenue from Aave's products to token holders.

These events have not had a direct impact on Aave users. The only impact has been on the price performance of the Aave token. However, the recent KelpDAO attack changed the situation: Aave lost over $12 billion in TVL, bringing its TVL closer to its competitor Morpho.

The ratio of Aave's TVL to Morpho's TVL has been between 5 to 6 times in the past, but due to this event, it has now dropped to below 2.

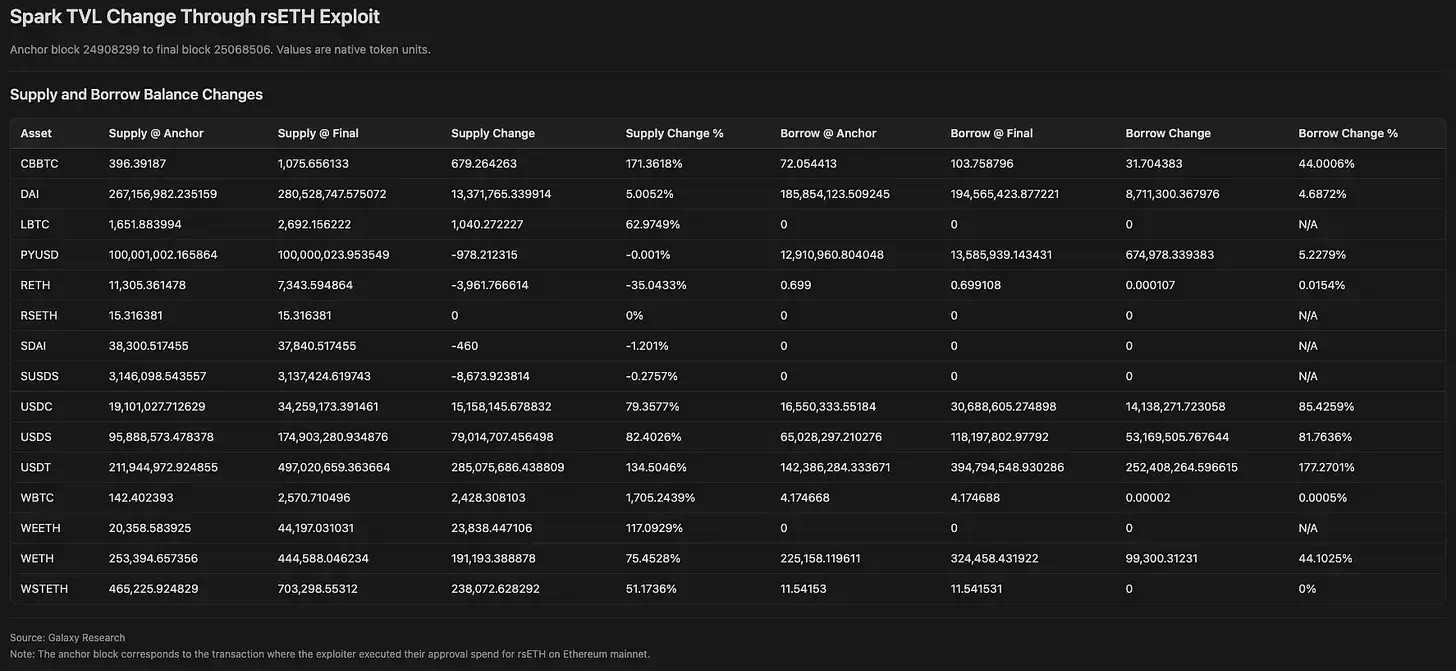

@sparkdotfi is part of the Sky ecosystem and is one of the leading lending protocols to benefit most from inflows after the rsETH hack.

The following graph shows the protocol's TVL changes:

Most notably, the Bitcoin supply nearly tripled, stablecoin borrowing increased by 78% to $752 million, utilization remained within manageable levels, and WETH borrowing increased by 44.1% to 325,000 WETH.

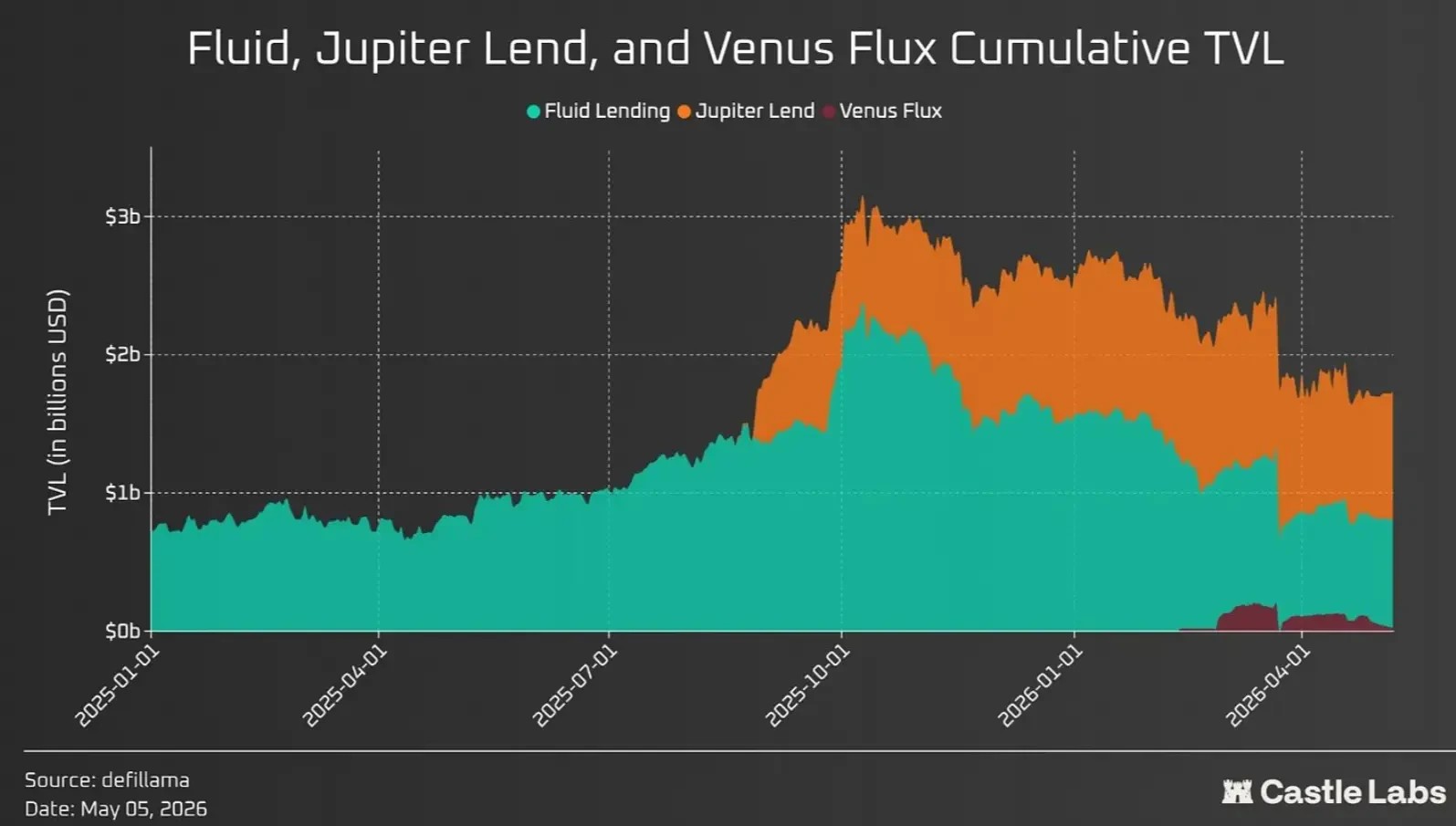

@0xfluid's Unified Liquidity Layer also introduced a different liquidity design approach, where lending, borrowing, and DEX share the same funds. Users collateralize assets in Fluid DEX as LPs (Liquidity Providers), earning transaction fees, while borrowed funds are smartly deployed into the DEX pool to earn fees and offset borrowing interest costs.

Another interesting move by Fluid is its partnerships with protocols like @JupiterExchange and @VenusProtocol, through which it has launched white-label products such as JupLend (Solana) and Venus Flux (BSC), with TVL currently reaching $926 million and $21 million, respectively.

This stems from Fluid's broader positioning to work with key players in each chain and gain more market share, with these participants sharing fees with Fluid.

It is worth mentioning the @kamino Treasury, which is the primary lending stack on Solana, with over $1.6 billion TVL. The protocol has seen significant growth through its K-Lend model (equivalent to Morpho on Solana), allowing Kamino to collaborate with established curators like Gauntlet and target institutional integration.

The largest vault on the platform is currently @SentoraHQ PYUSD, with over $219 million TVL, followed by RockawayX's RWA USDC vault at only $33 million, indicating that Kamino and the entire Solana ecosystem still have significant room for growth.

Liquidity Staking and Restaking

Liquidity staking and restaking account for a large share of the vault TVL, with $42.4 billion and $20.6 billion, respectively.

The main participants in liquidity staking are Lido ($21.8 billion), Binance Staked ETH ($8.9 billion), @Rocket_Pool ($1.2 billion), and @Coinbase cbETH ($320 million).

Over time, Lido has maintained its dominance, with its issued asset stETH being highly composable across DeFi. However, Lido's leading position also signals centralization risks.

They expanded their product line by introducing Earn, which acts as an aggregation layer, depositing users' funds across DeFi to earn yield. Nevertheless, due to the risk exposure to $rsETH, the product suffered a blow following a recent exploit in the Kelp DAO.

Binance Staked ETH leveraged Binance's user base, growing by 121.8% since last year.

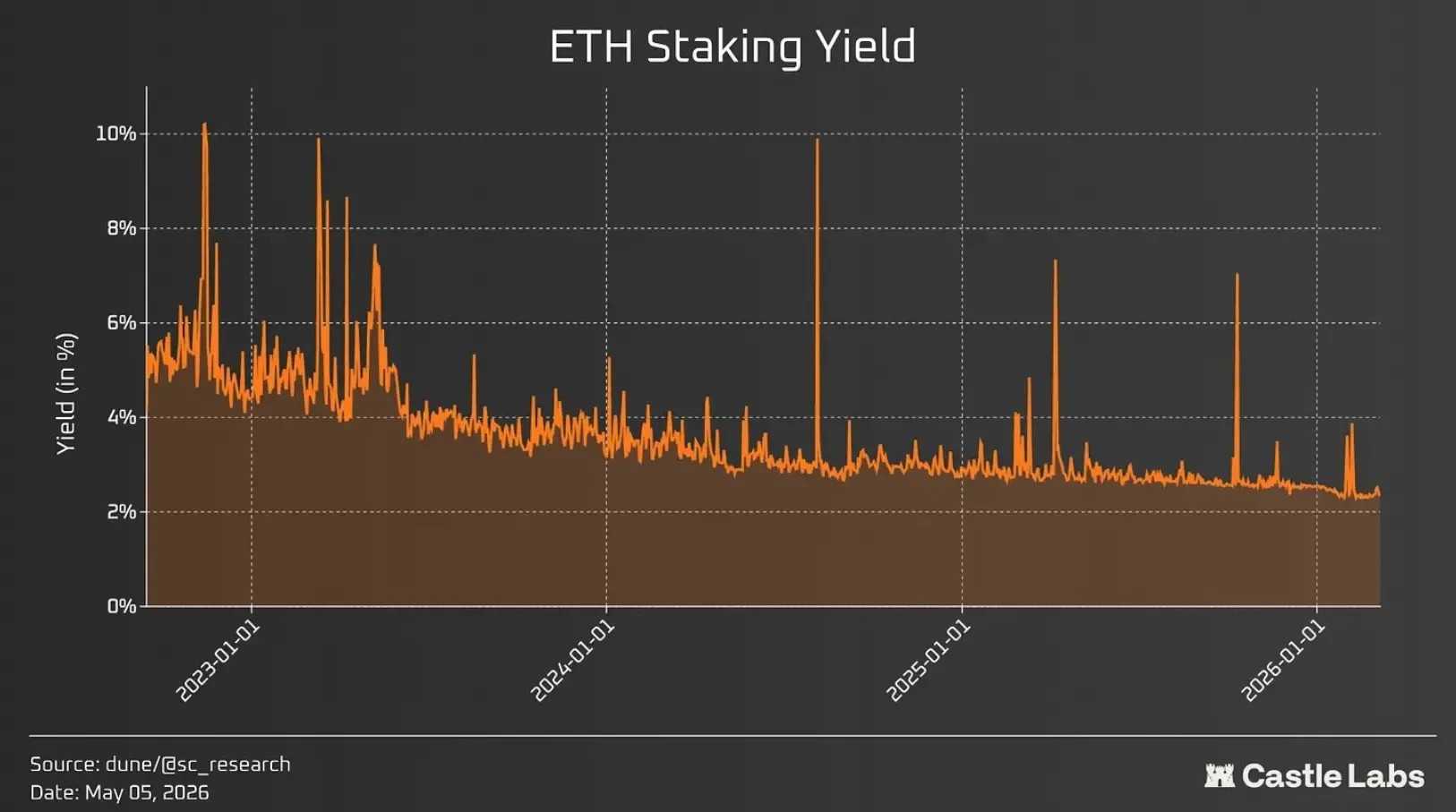

For other protocols and the entire category, growth has been sluggish, and at the expense of diluting staking rewards, the current staking yield stands at around 2.5%.

On the other hand, restaking and liquidity restaking have emerged as a category to boost earnings from liquidity staking.

@KelpDAO was once a liquidity restaking protocol, with its hack and the broader DeFi flash loan exploit highlighting the composability risks these assets bring as they are accepted as collateral across DeFi, where, in this case, it was more of a vulnerability than a feature.

The key players in staking and yield farming are @EigenCloud ($7.8 billion), @ether_fi ($5.7 billion), Kelp DAO ($1.6 billion), and Renzo ($167 million).

Staking products like EigenCloud and EtherFi have expanded over time to encompass more services.

In 2025, EigenCloud's rebranding helped position itself as the AWS of the crypto space, driving the development of verifiable computation.

Eigen's data availability layer, EigenDA, is used by multiple L2s, including @megaeth, @Mantle_Official, and @Celo. Data published on EigenDA has exceeded 1.8 TB, generating approximately $90,000 in total fees.

EigenCloud's Total Value Locked (TVL) has remained stable in ETH terms over the long term but recently experienced a decline post the Kelp hack as users tend to withdraw funds in uncertain times.

Similarly, EtherFi has expanded into a neobank, with thousands of active card users who have collectively spent around $440 million through their products.

Additionally, they have a Liquid product (don't forget EtherFi was initially launched as a liquidity staking protocol) supporting multiple strategies to enhance overall DeFi yields. One of their top ETH yield vaults has a TVL of $177.5 million.

Risk Strafe Vaults

Risk strafe vaults are one of the fastest-growing categories, reflecting a shift from monolithic lending to modular lending. They offer strafe vaults on platforms like Morpho to earn performance and management fees, operating similar to traditional financial funds by deploying user capital across various strategies to generate returns.

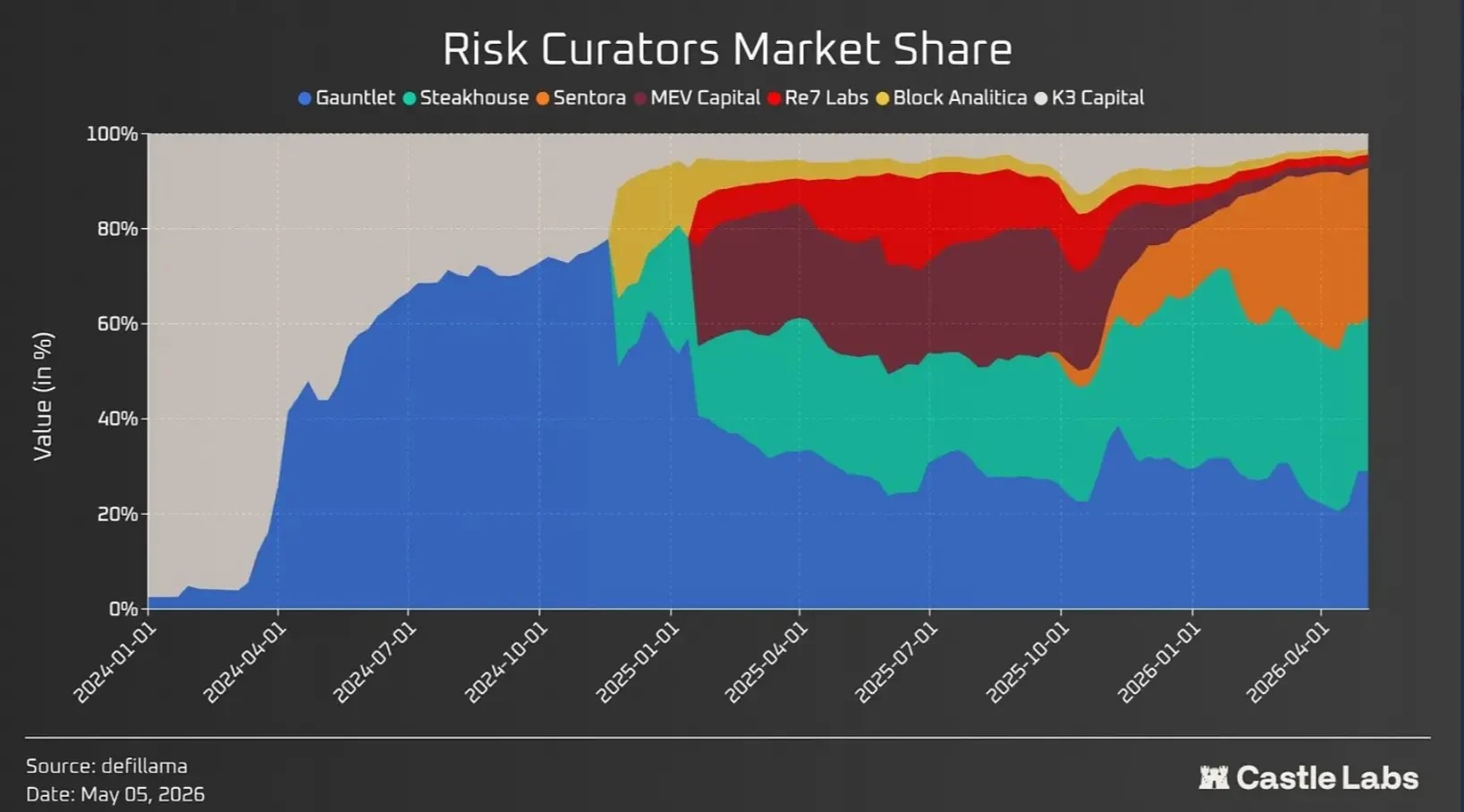

The current TVL of this category is around $6.5 billion, with 75% held by three strafe vaults: Sentora ($1.85 billion), @SteakhouseFi ($1.63 billion), and @gauntlet_xyz ($1.5 billion), indicating relatively low competition in this category.

These risk orchestrators charge lower fees compared to traditional financial hedge funds and venture capital funds, which typically charge a management fee (usually around 1-2% of total AUM) and a performance fee (typically around 10-20% of earnings).

For example, the highest-earning orchestrator, Steakhouse Financial, generates $3 million in annual revenue on a $21.3 billion AUM (an annualized fee rate of approximately 0.14% of total AUM).

These orchestrators usually only charge a performance fee, with some cases also including a management fee, but these fees are currently much lower. This is a result of the competitive landscape, as orchestrators strive to offer the lowest fees to attract the most TVL.

However, despite this, risk orchestrators are concentrated at the top, with dominance split among three main providers, which is better than liquidity staking, where Lido is far ahead.

Furthermore, what does this concentration mean? The Steakhouse team states: "Concentration may follow a power law similar to what is found in traditional asset management analogs (e.g., ETFs), where a significant portion of AUM concentrates around leading managers."

This is not necessarily a bad thing, but a reflection of compounding scale and trust towards leading managers, who compete on performance, product range, and fee loads.

The benefit of DeFi is that the playing field is open. Anyone can come in to compete. We expect top-tier concentration to persist, with healthy competition at the margins and room for specialization."

Following the Stream Finance incident, concentration dynamics have recently shifted, with MEV capital and Re7, which previously peaked at $1.49 billion and $830 million, respectively, shrinking, and Sentora emerging as the second-largest orchestrator.

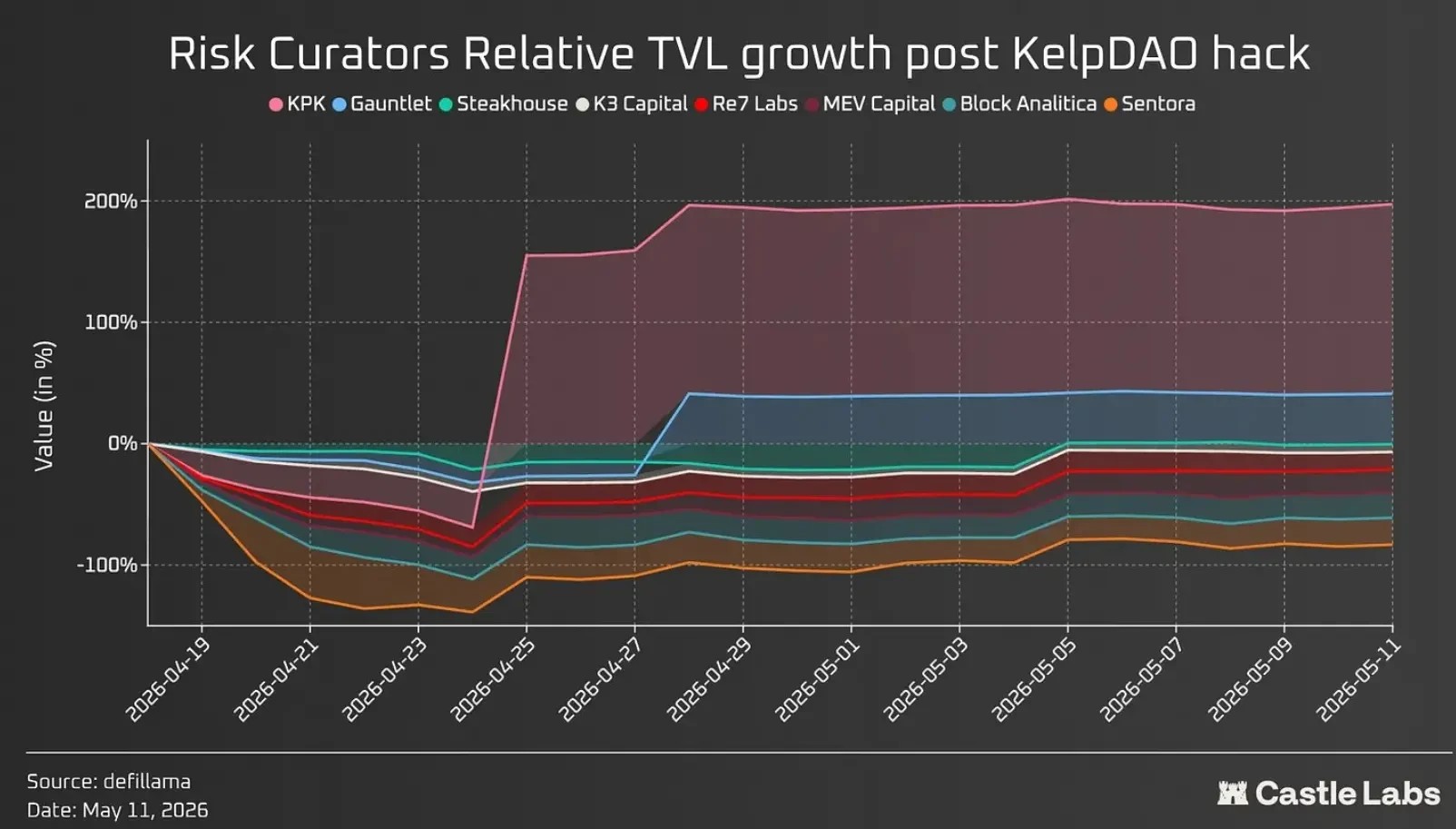

Additionally, following the KelpDAO hack, the impact on risk orchestrators is evident, but a few winners, such as @kpk_io (+159.6%) and Gauntlet (+42.7%), have seen net positive inflows.

For KPK, this growth stems from their recent launch of the Morpho V2 vault, which attracted deposits from entities like ensdomains, CoWSwap, and NexusMutual.

They integrated agent-driven automation for rebalancing and treasury yield farming, enhancing their risk management. For Gauntlet, growth came from the expansion on its BSC chain and its collaboration with the Lista DAO lending protocol, attracting new capital inflows.

As highlighted by Sentora's Juan Pellicer, 「DeFi insurance is also becoming a real part of the institutional landscape. The ability to provide economic cover is changing the calculus for a treasury or asset manager who must answer to an investment committee; this is a structural unlocking」.

Multi-Strategy Vaults

The yield optimizer as a category is maturing and seeing a plethora of new entrants. With the increase in on-chain revenue sources, optimization or aggregation models will become a better vault model, providing depositors with comprehensive yield optimization.

Protocols such as @Veda_labs ($1 billion), @upshift_fi ($380 million), and Fluid Lite Vault ($164 million) lead the pack in the overall category.

Each protocol offers a different model, but the goal remains to seamlessly integrate yield optimization vaults and provide their depositors with the best available yield across DeFi. Due to ongoing market drawdowns and the pressure period since last October, they are currently well off their peaks.

It's best to view providers like Veda and Upshift not just as aggregators but as the infrastructure for building isolated yields products. Upshift uses its proprietary strategy engine to execute vault authorization rules and ensure self-custodial properties, restricting deployments to whitelisted chains/protocols/tokens/smart contract calls.

Furthermore, Upshift is better classified as a multi-strategy vault as its vault offers broad DeFi strategy exposure, including lending, basis trading, yield curve trading, liquidity providing (LPing), RWAs, among others.

Veda leverages a modular architecture, separating operations into a "boring" vault whose sole purpose is to hold assets, with any specialized tasks carried out by external modules. The protocol employs a Merkle tree to enforce permissions by whitelisting specific vault operations.

Infrastructure providers enable institutions to very easily start from a single integration, allocate to a lending protocol, and progressively add more complex strategies as the product offerings expand for higher returns and deeper liquidity.

Products such as Fusion ($30 million) from @ipor_io and Gearbox Protocol ($29 million) have also emerged as yield optimization layers. For example, Fusion focuses on on-chain treasury infrastructure, enabling standalone entities like curators and asset managers to build and operate yield strategies such as leverage loop lending and carry trades.

Each Fusion treasury is unique in curation, strategy, and allocation. Automation is built at the strategy level with different triggers for optimization, leverage maintenance, liquidation risk management, routing, and more.

For instance, executing swaps during negative carry, using flash loans to migrate leverage positions across markets, or exiting during a risk event. As highlighted by the Fusion team, "This automation was crucial in the recent rsETH/Aave crisis, where the mainnet's IPOR DAO stETH loop treasury was among the first to fully close out the Aave v3 core exposure."

Overall, automation and execution enable curators to swiftly manage risk when quick actions are most needed."

Among all protocol-managed fund categories, leverage loop lending holds the largest share at around $80 million. This number is higher as TVL is an insufficient metric for yield optimizers.

Instead, these providers should be analyzed based on their Asset Under Management (AUM) as they allocate funds to other protocols, making their TVL not reflective of actual growth.

Gearbox introduced a treasury structure targeting passive lenders and active borrowers.

The protocol's core is to provide access to leverage or Delta-neutral exposure for strategies around liquidity mining or liquidity provisioning. While most treasury mechanisms are built around curator asset management, Gearbox focuses on lender-side risk management infrastructure.

Borrowers can open credit accounts to interact with Gearbox and external protocols while keeping funds non-custodial. V3 introduced strategy-level firewalls to protect the protocol in case of credit account or strategy failures.

In case of incidents, they are unable to drain funds beyond what is allocated to their shared liquidity pool, safeguarding passive lenders from contagion.

Recently, the protocol also announced a focus on RWA loop lending treasuries.

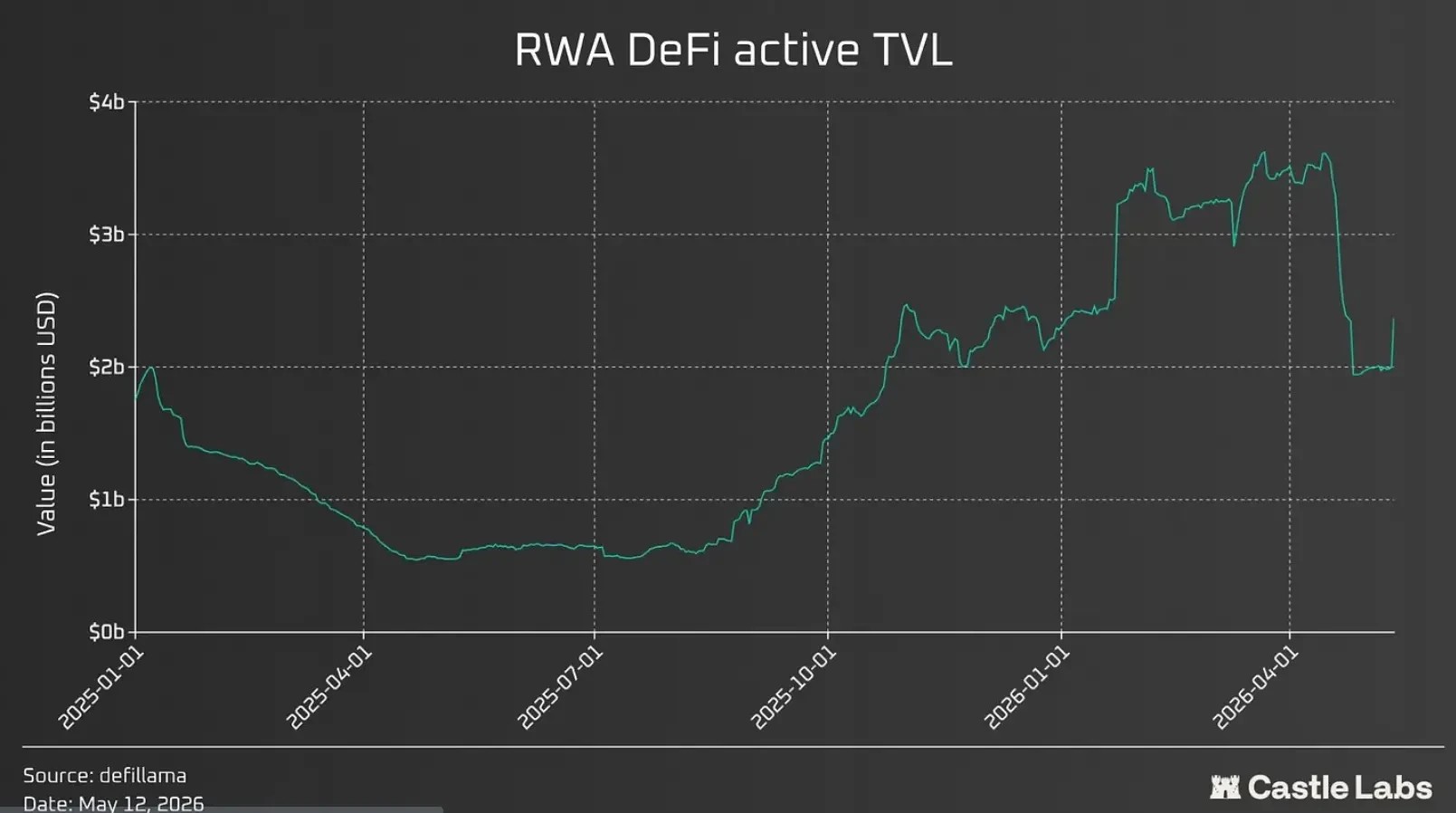

RWA Vault

The RWA Vault has seen consistent growth over the past 5 years, with a Compound Annual Growth Rate (CAGR) of 231.3%, reflecting increasing interest from retail and institutional investors in RWA yield farming. Even after the recent @ResolvLabs and Kelp exploits, the RWA Vault category has shown resilience due to limited on-chain exposure and has not experienced significant volatility.

The largest participants in this category are @maplefinance ($21 billion), @centrifuge ($16 billion), @anemoycapital ($11 billion), and @re ($2.63 billion).

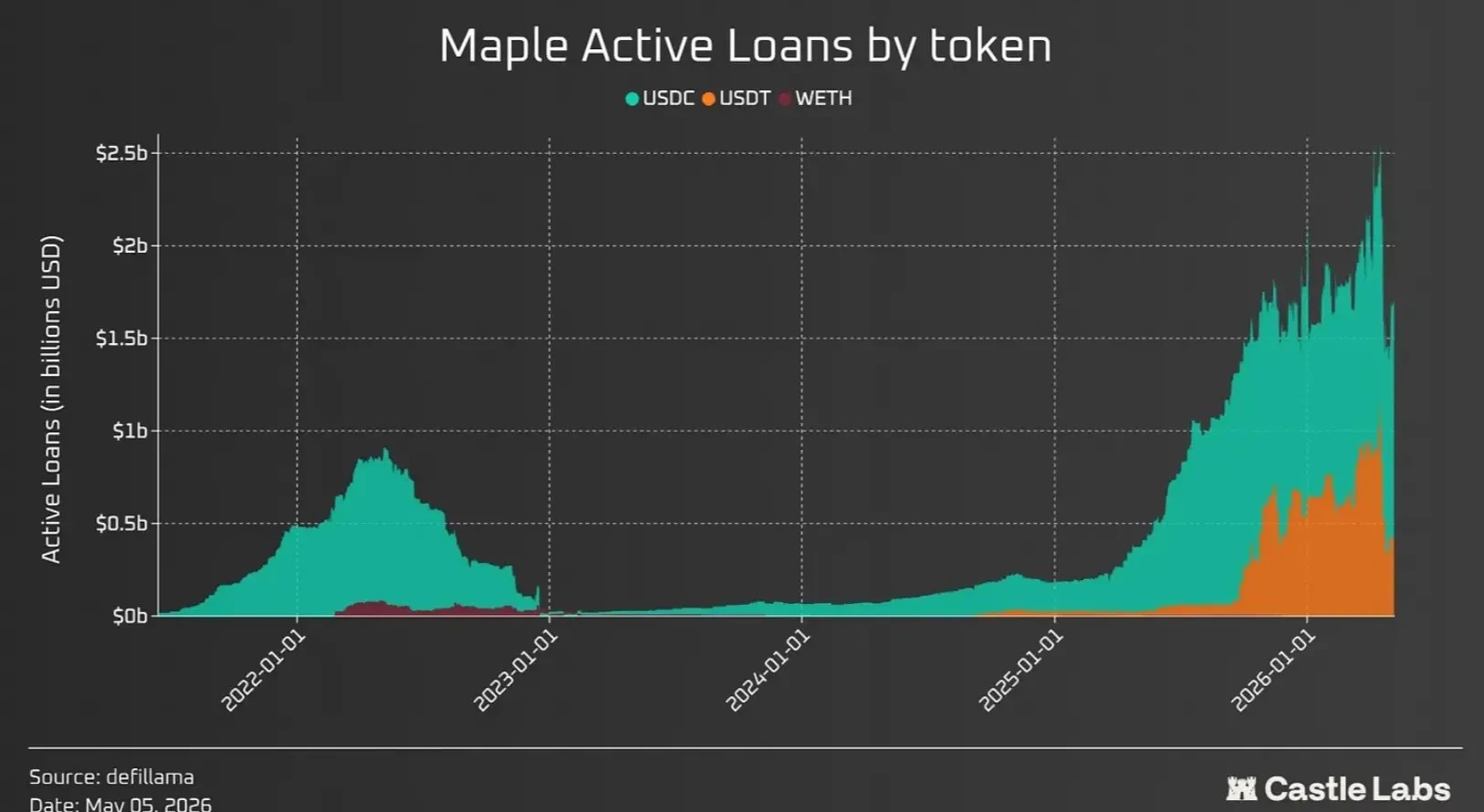

Maple Finance has experienced rapid growth in the past year, with TVL increasing nearly 10x since the beginning of 2025. This growth can be attributed to various factors, including the launch of Syrup as part of the protocol's transition from a purely institutional model.

This launch opened the door to products aimed at retail traffic (such as SyrupUSDC and SyrupUSDT), which are highly composable in DeFi. DeFi's composability and deep liquidity allow assets to be leveraged through recursive lending protocols and integrated with products like @pendle_fi, fueling the growth flywheel.

In line with the demand for these products, the platform's current active loan volume is approximately $17 billion. These loans are predominantly in USDC, accounting for about 75% of the total active loans, followed by USDT and the remaining portion.

Other products have also witnessed significant growth. For example, Centrifuge positions itself as a private credit infrastructure protocol. Its collaboration with Anemoy resulted in an $11 billion national debt pool running on Centrifuge infrastructure. Centrifuge was also recently selected by Coinbase as its tokenization partner.

Products like Re introduce reinsurance underwriting risks to the blockchain, allowing users greater exposure to real-world yields. Additionally, the Upshift USDC Vault provides loans to overcollateralized institutional funds, enabling depositors to access institutional lending opportunities.

Despite witnessing all this growth in DeFi, RWA still represents only a small fraction of the tokenized on-chain value. Currently, the active RWA DeFi TVL accounts for approximately 1/10 of the total RWA value.

The significant difference between these two values is because these assets belong to different categories, going beyond the usual considerations for traditional assets, as they involve redemption periods, compliance, and liquidity issues in certain cases.

For any asset to scale in DeFi, it requires active redemption and secondary liquidity, as users may need to sell these assets to regain liquidity. In the case of lending protocols, liquidators may repay loans and sell assets close to the mark price to make a profit. However, given all the restrictions brought by RWAs, these mostly become more challenging to achieve.

Furthermore, interest-bearing assets like RWAs have another key element in their growth flywheel: looping.

RWA looping involves borrowing stablecoins against tokenized government bonds as collateral and repeatedly redeploying them into a yield farm. With a 4-5% base treasury yield, under 2-3x leverage, it can generate a return of 7-12%. However, this is only achievable when the borrowing cost remains low (around 1%).

On-chain stablecoin rates are highly volatile and could significantly compress this spread. The leverage used to execute such transactions amplifies liquidation and oracle risks, and this strategy relies on the stability of RWA collateral values. As a result, some RWAs settle on T+1, while others settle on T+5, adding to the redemption issue.

To address this problem, there are currently several solutions:

ERC-7540: Introducing an asynchronous ERC-4626 treasury so users can use their redemption claims as liquidity while the underlying asset settles off-chain. Centrifuge is one of the primary examples of ERC-7540 in production, employing synchronous deposits and asynchronous redemption to resolve the tension between DeFi and traditional finance T+ settlement. These hybrid treasuries are becoming a template for any involving off-chain asset treasuries.

Securitize Treasury Registrar: When using RWAs in DeFi, this ERC maps each investor to their identity, ensuring protocol compliance with all the regulatory and asset-specific requirements.

Redstone Liquidation Flows: They execute RWA liquidation by introducing auction-based liquidation and connecting positions to KYC-verified solvers receiving the underlying assets off-chain and closing them on-chain.

Upshift Clear: Upshift is partnering with Superstate to release its new product to achieve instant RWA redemption, allowing users to swap their RWA for USDC at the current reported price, with a 5 bps redemption fee.

Another protocol in this category is 3F, a platform for on-chain leverage of RWAs (@3f_xyz). It currently has a $7 million TVL and addresses RWA asset issues in a way distinct from other solutions in DeFi.

It seeks to externalize various factors, including Bridge Facilitators and Liquidity Integrators. The former provides initial liquidity to cover the exposure users intend to take on their base capital.

For example, if a user's target exposure is $3 million with a $1 million deposit, they can obtain the remaining $2 million in liquidity from a Bridge Facilitator, allowing them to achieve a 3x leverage on the entire position.

Likewise, when a user intends to close out their position, the facilitator provides the required liquidity, addressing redemption delays. The latter, Liquidity Integrators, offer immediate liquidity when users seek to exit promptly.

Because even with Bridge Facilitators, the user's $1 million deposit must undergo the entire redemption process, these Integrators provide much-needed liquidity.

Both approaches leverage market efficiency, akin to the liquidation role in lending, with proactive on-chain participants filling the gap required in the RWA circular lending to earn profits.

Over time, such systems become more easily scalable as each participant benefits from the process: redeemers experience smooth exits, and facilitators earn profits by providing liquidity and enabling quicker redemptions for users.

As mentioned in the previous section, Gearbox also plans to introduce "Retokenisation": a feature allowing for leveraged minting and redemption of non-atomic-tokenized assets natively in the infrastructure, without the need for secondary liquidity or redemption delays.

In practice, Gearbox's contract will merge with the RWA issuer's contract, creating a seamless, composable system that achieves RWA leverage directly at the issuer level, making Gearbox the sole protocol offering RWA-native leverage on the EVM.

Perpetual Contract LP Treasury

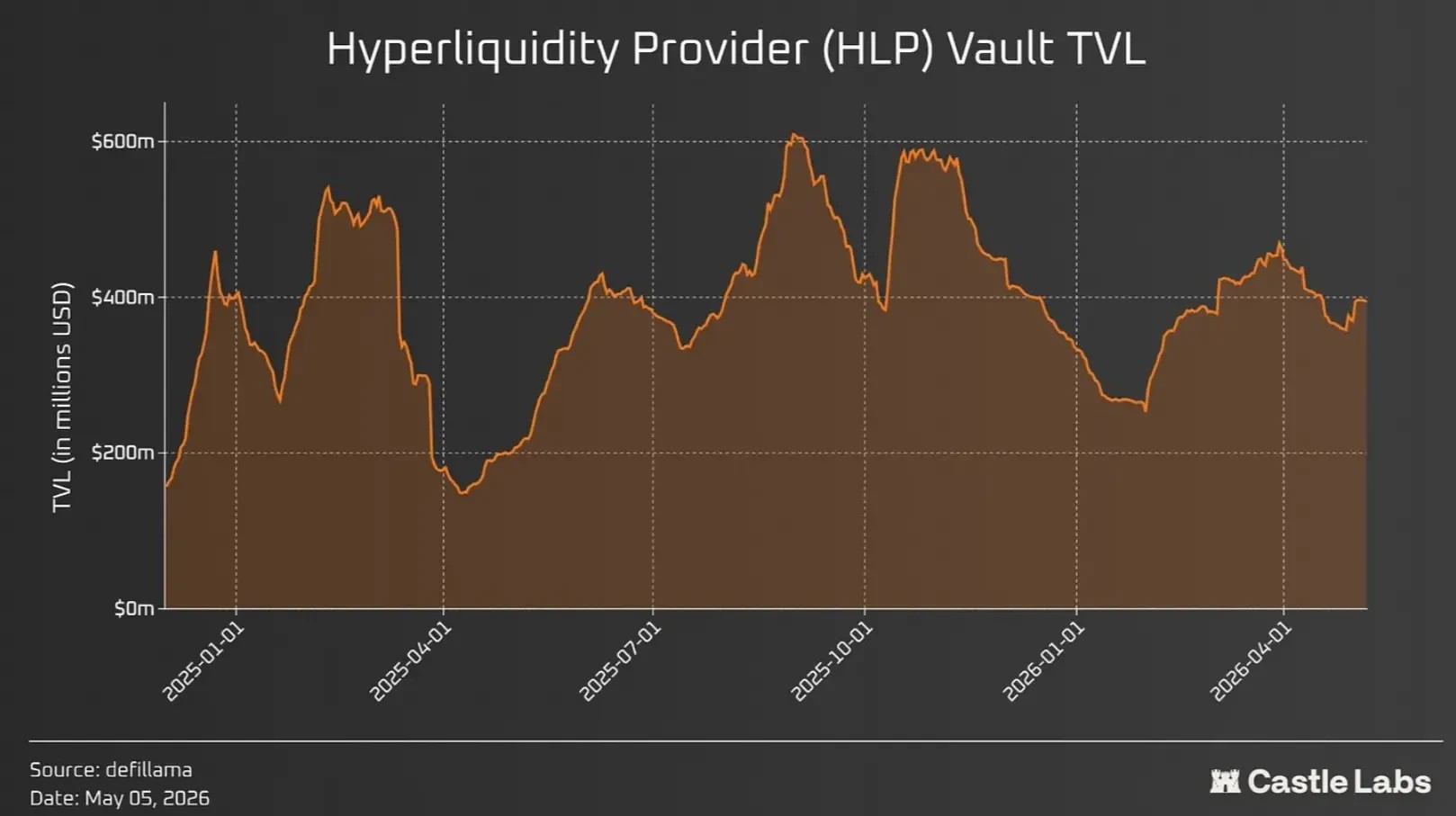

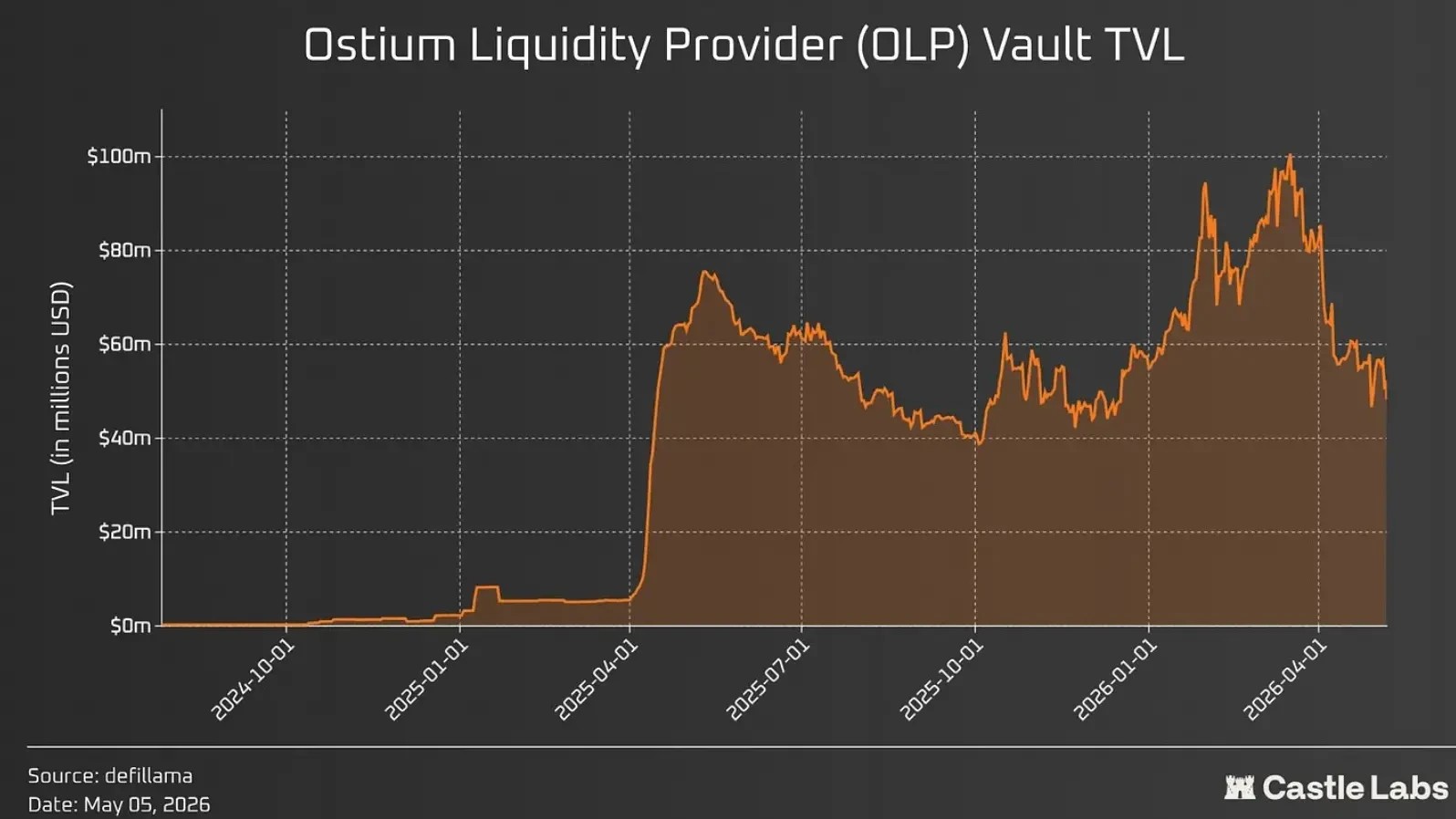

Representatives of the Perpetual Contract LP Treasury include Jupiter Perps ($7.15 billion), @HyperliquidX HLP ($3.96 billion), @DriftProtocol ($2.56 billion, recently decreased due to a hack), @GMX_IO ($2.42 billion), and @Ostium ($51 million).

Jupiter's JLP remains the largest perpetual treasury in TVL terms, but has lost over half of its value since a liquidation event in October last year.

HLP has performed better in terms of maintaining value, decreasing by 30% from its peak of $6 billion in September last year. Hyperliquid's treasury has experienced continual fluctuations, often driven by its HLP floating yield, which is influenced by its structure and market conditions. Therefore, high-yield cycles attract capital, while low-yield or losing periods drive it out.

A major loss event occurred in March 2025 when a trader took a significant short position on the Jelly token, then withdrew collateral, triggering a forced liquidation and prompting HLP to take over the position.

Such losses to the treasury have led depositors to develop a structural bias against it, often categorizing HLP as a higher-risk treasury. However, Hyperliquid has reduced the leverage allowed for such tokens to avoid such situations, thus amplifying losses.

Products like Ostium OLP provide exposure to RWA perpetual contracts and offer users varying configurations of yield, but their TVL has dropped by approximately 50% from its peak. This drawdown is a result of broader market movements and Ostium's yield cycles.

Additionally, Ostium has recently introduced structural changes, making OLP the first tier and never taking on the first risk of intraday settlement layer. This contrasts with the HLP model: depositors looking for the directional exposure OLP used to provide may leave, but at the same time, in this new model, it becomes a passive source of income for risk-averse depositors.

Options Treasury

The DeFi Options Treasury (DOV) as a category has gradually faded over time, peaking in 2022. DOV provides exposure to covered call options and cash-secured put options strategies, but lacks capital efficiency, carries higher risk, and over time, as crypto users tend to be drawn to perpetual contracts, it has attracted a diminishing audience.

However, the options treasury has been continuously improving and solidifying its use case, at least for more sophisticated users.

The Options Treasury no longer exists in its previous format. Instead, they are structured differently, more user-friendly, and delivered through products like @DeriveXYZ and @ryskfinance. Today, the Options Treasury is executed through a Request for Quote (RFQ) system, with market makers handling the backend.

Derive is an options and perpetual contract trading platform that, after the launch of V2 in March 2025, experienced accelerated growth due to enhancements such as the use of CLOB and enabling institutional-grade features like OTC custody and support for multiple collateral types, processing $12 billion and $16 billion in perpetual contract and options trading volume, respectively.

Derive V1 has active vaults that provide users with exposure to various strategic options and create delta-neutral positions for its depositors to maximize annualized returns. These vaults currently hold approximately $2.4 million in Total Value Locked (TVL).

On the other hand, products like Rysk provide options exposure to retail users through covered call options and cash-secured put options. Launched on Hyperliquid, with a focus on HYPE's covered call options, it currently has around $56 million TVL and has processed $975 million in notional options trading volume.

In addition, they also offer Rysk Premium, a flagship product that serves as a treasury for savvy allocators, deploying funds across different options strategies and generating continual returns for depositors.

The new treasury focuses on addressing some of the past issues with existing products. These issues include poor strategy design, short time frames as low as 7 days, executing trades at fixed intervals creating front-running opportunities, and enabling users to customize their scale, strike price, or expiry date.

Options Treasury providers are now more attuned to the market pulse, understanding which assets to list to capitalize on new opportunities in the yield-bearing asset space.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia