DeFi Options Survival Guide: From Premium to Volatility, the Underlying Logic of Preserving Capital in a Bear Market

Original Title: "Options: If You Don't Understand, Your Money Is Just the Project Team's Yacht Model"

In a bear market, many people will choose to put their money into financial management.

However, in the current environment, rug pulls of DeFi projects have become the norm.

If you don't understand what kind of magic the project team is playing, you are essentially just the meat on their cutting board.

Therefore, this time, I want to start from the very, very basic logic to learn about the underlying options of DeFi.

Table of Contents

1. How Did Humans First Buy a Option for the Future

2. A Piece of Contract, Why Can It Trade the Future

3. When Do People Need Options

4. Call, Put, Buyer, Seller

5. From Wall Street to Coin Circle: IV, Greeks, and the True Core of Option Risk

1. How Did Humans First Buy an Option for the Future

Imagine, go back thousands of years to the ancient Middle Eastern desert.

The protagonist of the story is Jacob. He traveled a long distance to the home of his uncle Laban and fell in love with Laban's younger daughter, Rachel. Jacob was eager to marry Rachel, but he was a penniless fugitive at the time and could not produce the generous bride price required by society.

If we follow the usual spot transaction (paying on the spot for goods), Jacob is not qualified to negotiate this marriage. Furthermore, if he spends several years slowly saving money, the beautiful Rachel may have already been betrothed to another wealthy young man.

Facing the enormous risk of the "uncertain future," what should Jacob do?

He made a proposal to Laban: "I am willing to work for you for seven years for free in exchange for the right to marry Rachel seven years later."

One day, Laban said to him, "Although we are close relatives, I cannot let you work for me without pay. Tell me, what do you want as recompense?"

Laban had two daughters. The older one was Leah, and the younger one was Rachel. Leah had weak eyes, but Rachel was lovely in form and beautiful.

Jacob was in love with Rachel and said to Laban, "I'll work for you seven years in return for your daughter Rachel."

Laban replied, "It is better that I give her to you than to some other man. Stay here with me." So Jacob served seven years to get Rachel, but they seemed like only a few days to him because of his love for her.

Laban agreed, and both parties entered into a contract defying time and the future.

These are actually the four key elements of an option contract:

Buyer: Jacob.

He is the one seeking to control the future.

Seller: Laban.

He accepted the benefit and promised to fulfill his obligation in the future.

Underlying Asset:

The right to marry Rachel. In modern times, this could be a stock in Bank of America, Bitcoin, or gold.

Premium:

Seven years of free labor. Jacob had to pay a price upfront to "buy this right." This is similar to the premium we pay for insurance, which once paid, cannot be refunded but provides security in the future.

Expiration Date:

After seven years. The contract specifies the exact time when the commitment will be fulfilled.

Through this contract, what problem did Jacob solve?

He used his current labor (rights fee) to lock in a future price and right, eliminating the risk of Rachel marrying someone else during these seven years. That is the most appealing aspect of an option:

It empowers people to combat the uncertainty brought by time.

The Earliest DeFi Incident: Counterparty Risk

What is interesting about this story is that, in the latter part of the story, it casually inserts the most primitive DeFi exploitation event, where the counterparty was stealthily changed.

After the seven years had passed (the expiration date had come), Jacob was ready to exercise his right (demand Rachel's hand in marriage). However, the cunning seller Laban actually breached the contract on the wedding night! He secretly switched the eldest daughter Leah with Rachel to marry Jacob.

The next morning, Jacob realized he had married Leah and said to Laban, "What is this you have done to me? Was it not for Rachel that I served you? Why have you deceived me?"

Laban said, "It is not our custom here to give the younger daughter in marriage before the older one. Finish this daughter's bridal week; then we will give you the younger one also, in return for another seven years of work for me."

This is Counterparty Risk, where the other party in the contract does not act in good faith, leading to the contract not being fulfilled as agreed.

It is also the earliest DeFi incident.

II. A Contract on Paper—How Can It Trade the Future?

In Jacob's case, he used seven years of labor to lock in a future commitment. The mechanism of the modern financial market transforms this kind of verbal commitment into standardized contracts, which are strings of code in computer systems. As for why a contract can be used to trade the future, even with significant price fluctuations, this can be understood through the everyday act of ordering a house purchase.

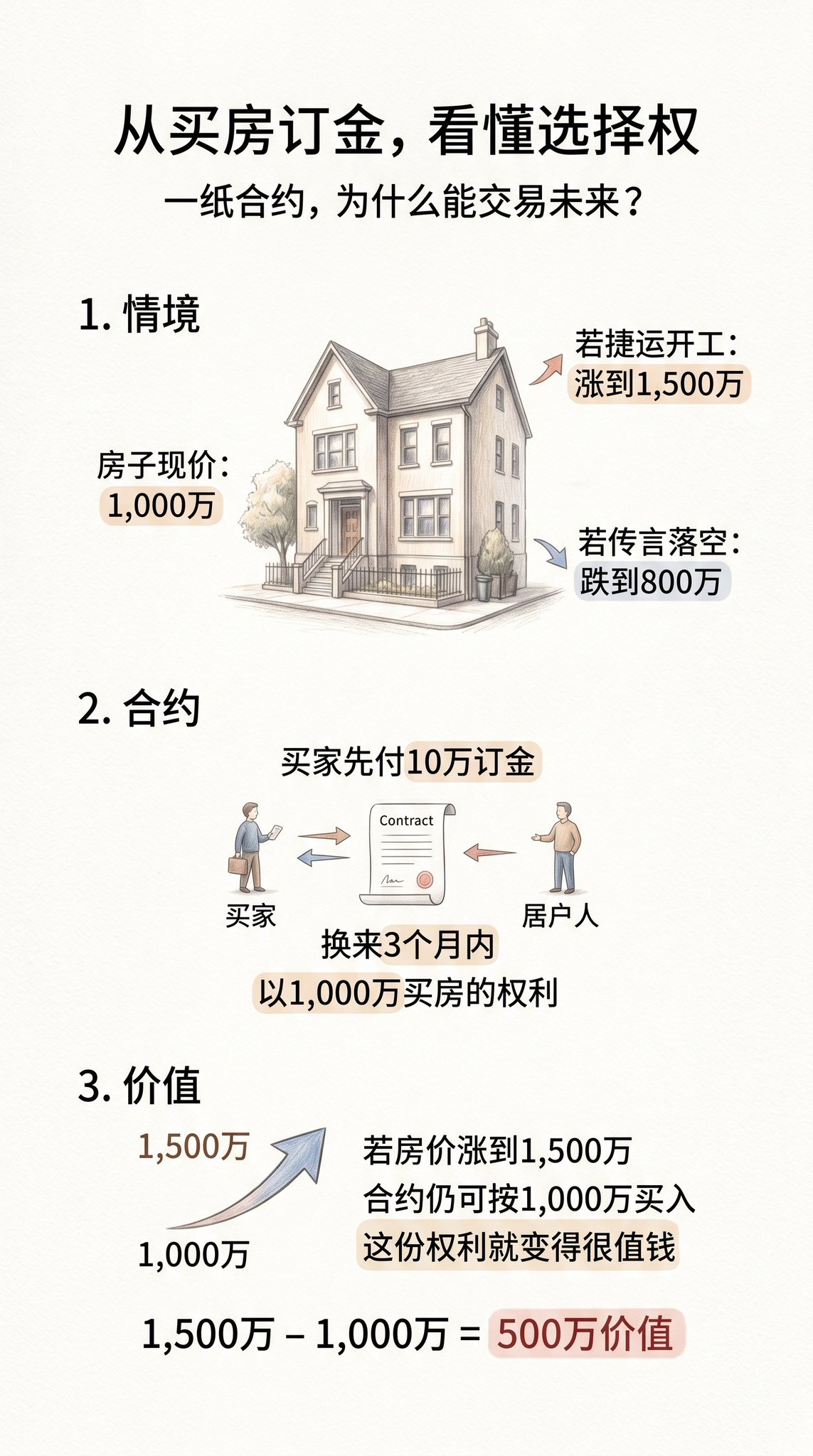

Understanding the Essence of an Option from a House Down Payment

Let's assume someone is interested in a downtown house worth $10 million. Rumors in the market suggest that a subway station may be announced nearby next month. If the subway station is confirmed, the house price may soar to $15 million; if the rumor turns out to be false, the price could drop to $8 million.

The buyer is short of funds or unwilling to bear the risk of a house price drop. So, they propose a solution to the homeowner: pay 100,000 RMB upfront, which is non-refundable. In exchange, the homeowner must provide a contract, promising that within three months, no matter how much the house price goes up, the buyer has the right to buy the house for 10 million RMB.

The homeowner, considering the current market conditions, sees the 100,000 RMB as guaranteed cash flow. Even if the buyer backs out of the purchase after three months, the house will still be retained, and the 100,000 RMB will be in hand. Therefore, the homeowner agrees to sign. This model is a standard Call Option transaction in the financial market.

Why Is This Contract Valuable

Suppose that a month later, a subway station is confirmed to be constructed, causing the house price to soar to 15 million RMB. At this point, this contract undergoes a qualitative change. According to the contract, the buyer has the right to buy a house worth 15 million RMB for 10 million RMB. By simply executing the contract and reselling the house, a net profit of 5 million RMB can be made. This means that the value of this contract itself is at least 5 million RMB.

Here, two core characteristics of the option are demonstrated:

First, it separates rights from obligations.

Typical purchase contracts involve mutual obligations, but options are unidirectional. The buyer has the right but not the obligation, while the seller has the obligation but not the right. If the subway construction does not proceed and causes the house price to fall to 8 million RMB, the buyer can simply choose not to execute the contract, with the maximum loss being the 100,000 RMB option premium paid initially. The buyer assumes limited loss risk while retaining the potential for profit.

Second, one can participate in price fluctuations without holding the asset, creating a leverage effect.

The buyer did not actually use 10 million RMB to purchase the property but controlled the price increase of a 10 million RMB asset with a 100,000 RMB contract. The actual return of 5 million RMB on a house purchase is a 50% return, but through the option, earning 5 million RMB with 100,000 RMB results in a 50-fold return. This illustrates why options have a high leverage feature of gaining big returns with a small investment.

III. When Do People Need Options

Building on the previous section's question, since the buyer enjoys the advantage of limited losses and unlimited gains, why would anyone in the market be willing to take on the role of the potential infinite risk seller? The answer lies in the fact that when faced with market uncertainty, participants have vastly different financial plans and needs.

The operation of the Options Market is mainly driven by three primary motives: Hedging, Speculation, and Generating Additional Income.

The first demand is for Hedging, essentially akin to the concept of buying insurance.

Suppose you hold a large amount of cryptocurrency spot on a trading platform. You believe in the long-term potential of these assets but are concerned that short-term overall economic changes or regulatory policies may cause a sharp market downturn. Selling spot directly would mean missing out on the long-term upside, but holding onto it poses the risk of a significant drop in asset value.

At this point, you can choose to buy a Put Option. This contract gives you the right to sell your assets at a predetermined price at some point in the future. If the market indeed crashes, although your spot holdings may show paper losses, the value of the put option contract in your possession would increase significantly, effectively offsetting the drop in spot value.

Conversely, if the market continues to rise, you would at most lose the premium paid for the contract, while your spot holdings would still benefit from the appreciation. It's like buying a price drop insurance for your investment portfolio, exchanging a fixed cost for protection against downside risk.

The second demand is for Speculation, leveraging controlled risk to amplify potential returns.

For traders who do not wish to commit a large amount of capital to buy spot, options provide high capital efficiency. For example, observing a significant upgrade approaching for a blockchain network (such as the Base ecosystem), with expectations of a related token experiencing explosive growth. Buying in on spot in the market would require a substantial capital outlay. By purchasing a Call Option, however, one can control an equivalent amount of assets and participate in the uptrend profits by paying a relatively small premium.

If the market analysis is correct, the increase in contract value could be several times that of spot; if incorrect, the maximum loss is limited to the initial premium paid. Unlike futures contracts, option buyers do not face the pressure of margin calls (liquidation) due to insufficient funds, making it a powerful tool to define absolute risk boundaries.

The third demand is for Generating Income, which is precisely why sellers are willing to assume obligations.

In the financial markets, being an option seller is akin to running an insurance company. From a statistical perspective, the vast majority of option contracts hold no intrinsic value at expiration and end up worthless. The seller's business model revolves around continually collecting premiums paid by buyers by assuming the risk of low-probability extreme events.

Additionally, many large institutions or long-term holders employ the Covered Call strategy. If they already hold a significant amount of spot and anticipate the price to consolidate rather than surge in the short term, they might opt to sell call options.

As long as the asset price does not exceed the agreed-upon strike price at expiration, the seller can easily earn this premium. During a period of sideways price movement, this practice effectively generates additional cash flow from idle assets.

The options market is precisely formed by the intertwining of these three demands. Hedgers seek protection, speculators seek leverage, and sellers provide liquidity while earning value from the passage of time. Once we understand the fundamental motivations of participants, we can further break down the four basic trading aspects within the contract and their respective rights and obligations.

Four: Call, Put, Holder, Writer: Rights and Obligations of Options

Upon entering the options market, the four fundamental quadrants often appear confusing. However, once we separate the types of contracts from the roles of participants, the logic behind it becomes very clear. The myriad variations in the options market are all composed of two types of contracts and two types of actors.

First, let's differentiate the types of contracts. A Call is known as a right to buy and grants the holder the right to "buy" the underlying asset at a predetermined price in the future. It can be seen as a call option. A Put is known as a right to sell and grants the holder the right to "sell" the underlying asset at a predetermined price in the future. It can be seen as a put option or a put purchase contract.

Next, let's distinguish the roles of the participants. The holder pays a premium to acquire the rights stipulated in the contract. The holder possesses absolute decision-making power and can choose whether to exercise the contract when the time comes. The writer receives the premium and undertakes the obligations specified in the contract. The writer is in a passive position and must cooperate unconditionally once the holder decides to exercise.

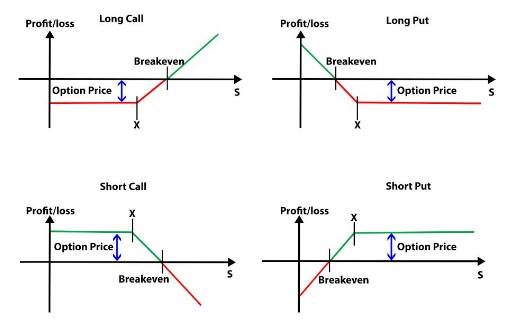

By combining the above two elements, the four basic strategies of options are formed:

· Long Call

An investor pays a premium and obtains the "right" to buy the underlying asset at a predetermined price in the future, with a bullish market view.

· Short Call

An investor sells a call option, receives a premium, and undertakes the "obligation" to potentially sell the asset at a predetermined price in the future.

· Long Put

An investor pays a premium and obtains the "right" to sell the underlying asset at a predetermined price in the future, usually used to anticipate a market decline or hedge against downside risk.

· Short Put

An investor sells a put option, receives the option premium, and takes on the obligation to potentially "buy" the asset at the agreed-upon price in the future.

1. Buy Call: Bullish Strategy

This is the most straightforward way to go long. When a trader is very bullish on the future price of an asset but does not want to commit the full amount of capital, they will buy a call option. For example, they anticipate an asset to rise from the current $100 to $150.

The trader can pay a $5 premium to buy a call option with a strike price of $110. If the price does increase to $150, the trader has the right to buy at $110, subtracting the $5 cost, resulting in a net gain of $35. If the price falls below $110, the trader can abandon the contract, with a maximum loss of only $5. This is a typical limited risk, unlimited reward scenario.

2. Buy Put: Bearish Bet or Hedge

This is akin to buying insurance for an asset. When a trader anticipates a market crash or wants to protect their current spot position, they will buy a put option. Assuming they hold an asset worth $100 and are concerned about a sharp decline next month, the trader pays $5 to buy a put option with a $90 strike price.

If the market crashes to $50, the trader still has the right to sell the asset at $90. The value of the put option will surge as the underlying asset price drops. This is also a strategy with limited risk but significant profit potential.

3. Sell Call: Neutral Strategy

This is one of the premium collection strategies, usually used when expecting the price to range-bound or experience a mild decline. The seller receives the premium paid by the buyer and commits to selling the asset to the buyer at a specified price if it exceeds the strike price.

If one sells a call option without holding the underlying asset (naked short), they will face unlimited loss if the asset price skyrockets. Therefore, institutional investors typically employ covered call strategies by holding the underlying asset to generate additional income during sideways market movements.

4. Sell Put: Neutral-to-Bullish or Position Initiation Strategy

This is a strategy that is often overlooked but widely used by many value investors or quantitative traders. When expecting the price not to experience a significant drop, or when hoping to buy an asset at a lower target price, one would sell a Put. For example, if an asset is currently priced at $100 and a trader believes $80 is an excellent entry point.

They can sell a Put with a strike price of $80 and immediately receive a premium. If the price does not drop below $80 by the expiration date, the contract expires worthless, and the trader earns the premium. If the price falls below $80, the trader is obligated to fulfill the contract by buying the asset at $80, which aligns with their plan to open a position at $80. Additionally, since they have already received the premium, the actual purchase cost will be lower than $80.

These four quadrants form the foundation of all complex derivative financial instruments. The buyer trades limited risk for leverage and choice, while the seller assumes extreme risk in exchange for a fixed income as time passes.

However, in the real trading world, the pricing of a contract is not solely based on price movements. The value of an option also involves market volatility and the passage of time. This leads to the core of Wall Street and crypto quant models, a threshold that many advanced traders must cross.

Five, From Wall Street to Crypto: IV, Greeks, and the True Core of Option Risk

When this sophisticated financial instrument of options moved from the traditional trading floors of Wall Street to the 24/7, highly volatile cryptocurrency market, the rules of the game fundamentally changed.

In the traditional stock market, an investor may patiently wait for a quarter for TSMC's financial report, and market volatility is relatively predictable. But in crypto, a weekend's breaking news could cause Bitcoin or Ethereum to have a double-digit percentage swing. In this extreme environment, merely speculating on price movements is far from sufficient when engaging in quantitative arbitrage or establishing defensive positions.

If you imagine yourself standing in front of a huge blackboard, trying to break down all the variables affecting the contract price, you will find that the pricing model of an option is essentially a set of multi-dimensional calculus equations. To decipher these variables, financial mathematicians have developed a system of indicators called "the Greeks."

The true starting point of this system is Implied Volatility (IV).

Implied Volatility: Pricing Fear and Greed

Before understanding Greek letters, one must first understand IV. IV is not a historical seismic amplitude but a collective consensus of market participants on the extent of future volatility.

When the market anticipates a major event (such as a significant upgrade to a Layer 2 network or an impending interest rate announcement by the Federal Reserve), everyone goes crazy buying options for speculation or hedging. This buying frenzy drives up the option's price. We take this inflated price and reverse it into the pricing formula, and the resulting value is IV.

In simple terms, IV is the fear and greed index of the options market. The higher the IV, the more turbulent the market is expected to be, and the higher the option premium; the lower the IV, the cheaper the option premium.

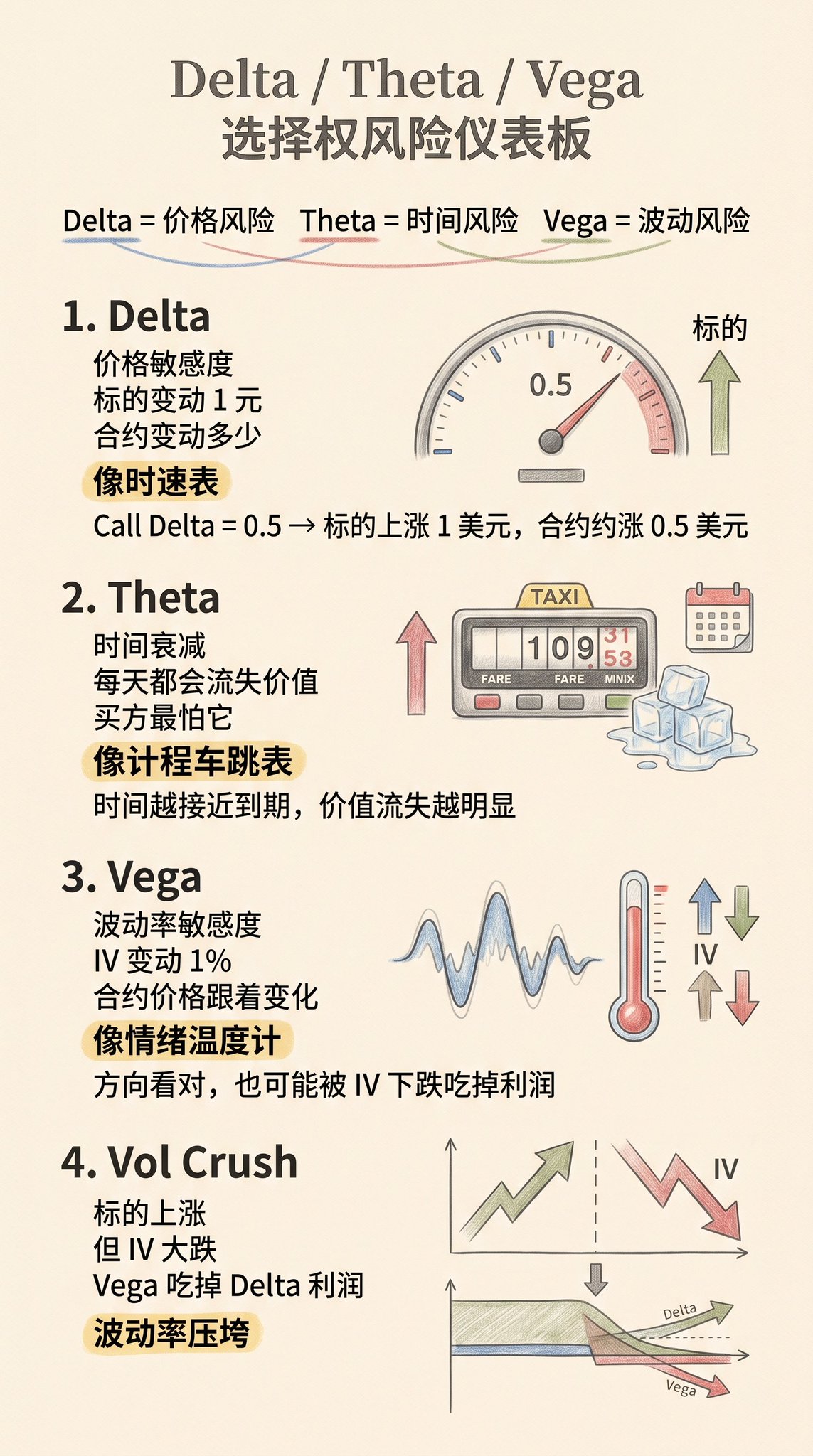

First-Level Risk Dashboard: Delta, Theta, Vega

With the concept of IV, we can now open the options risk control dashboard. The three core indicators correspond to price, time, and volatility.

Delta represents price sensitivity, also known as directional risk. It is defined as the amount the option price will change when the underlying asset's price moves by 1 dollar. You can think of Delta as a speedometer while driving. If your call option Delta is 0.5, this means that for every $1 increase in Bitcoin's price, your contract value will increase by $0.5.

Theta represents time decay, also known as time risk. Options are assets with an expiration date, and Theta measures how much value your contract loses each day under unchanged conditions. For the buyer, Theta is like a relentless taxi meter deducting money every day, as if holding a melting ice cube; but for the seller, Theta is like daily interest automatically credited to their account.

Vega represents volatility sensitivity, also known as emotion risk. It measures how much the contract price will change when implied volatility (IV) changes by 1%. In the crypto world, Vega's influence often overshadows Delta.

Sometimes, even when you have predicted the direction correctly and Bitcoin has indeed risen, if the market sentiment cools significantly from extreme euphoria, causing IV to plummet, the loss from Vega outweighs the profit from Delta, a phenomenon known on Wall Street as "Volatility Crush."

Advanced Fine-Tuning Gears: Speed, Color, Ultima

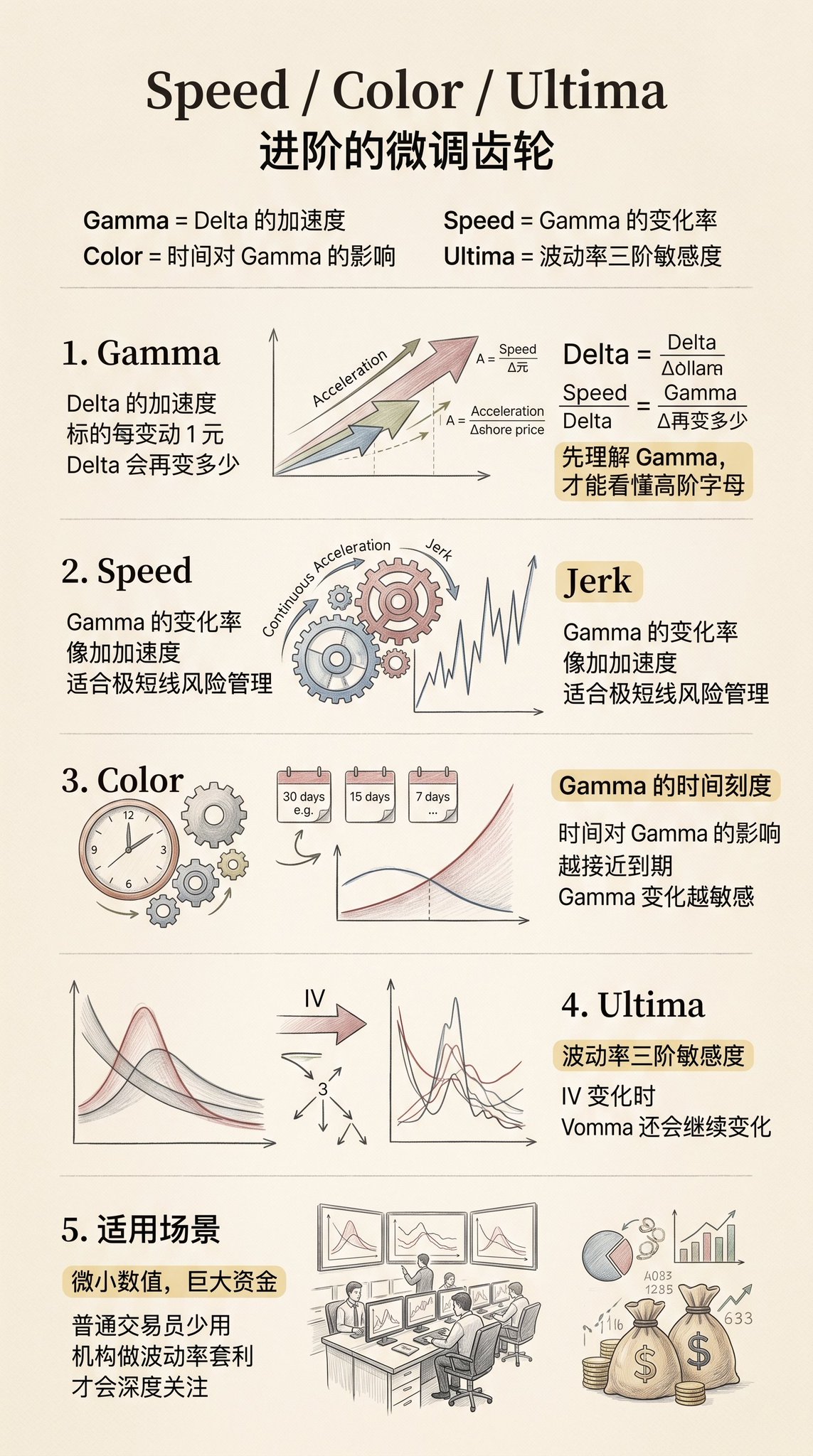

If the financial market were only affected by the above three variables, quantitative trading would be too simple. The reality is that when market prices change, Delta, Theta, and Vega also change accordingly. To address this dynamic variation, higher-order Greek letters have been derived.

To understand the higher-order letters, we first need to mention Gamma. Gamma is the acceleration of Delta. It measures how much Delta itself changes when the asset price moves by $1.

Speed is the rate of change of Gamma. In physics, if Delta is velocity and Gamma is acceleration, then Speed is jerk. It measures how Gamma itself changes as the underlying asset price continues to move. This is crucial for managing ultra short-term, highly volatile high-frequency positions.

Color measures the impact of time on Gamma. As the contract nears its expiration date, the value of Gamma changes. Color informs traders how your acceleration (Gamma) will change each day.

Ultima is the third-order derivative with respect to volatility. When IV changes, Vega changes, and the indicator measuring the rate of change of Vega is called Vomma. Ultima further measures how Vomma will change when IV changes again. These extremely small values are typically used by institutions managing billions of dollars, engaging in the ultimate volatility curve arbitrage.

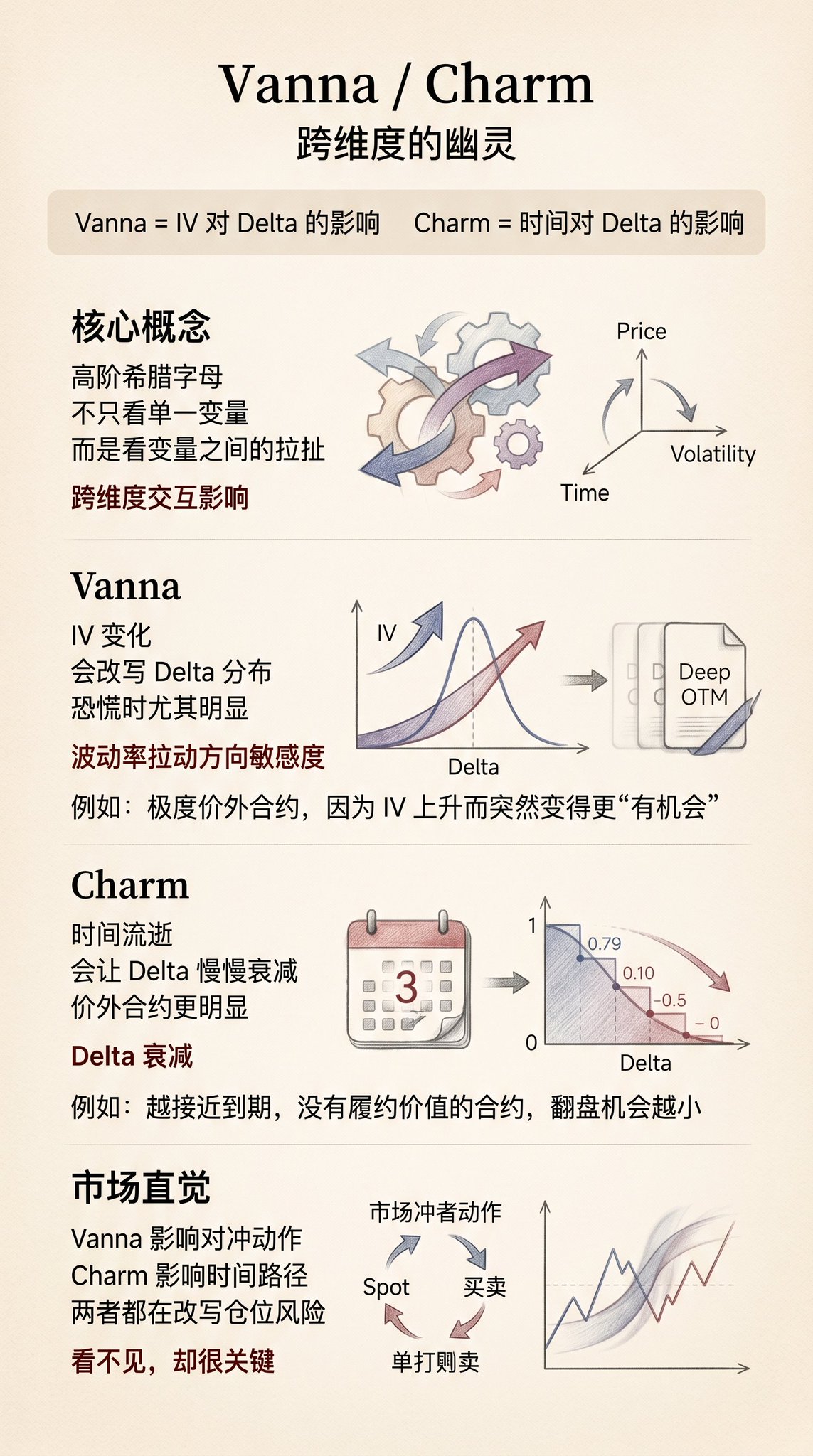

The Cross-Dimensional Ghosts: Vanna and Charm

In modern quantitative research, what truly fascinates advanced traders are the Greek letters that capture the cross-dimensional interaction effects, with the most famous being Vanna and Charm.

Vanna measures the impact of volatility (IV) changes on Delta. This sounds counterintuitive: why would a change in volatility affect my sensitivity to price direction? Because when market panic (rising IV) occurs, the previously out-of-the-money, far-out contracts suddenly become "in-play."

This expansion of possibilities shifts the entire portfolio's Delta distribution. During extreme market events like the crypto market cascading liquidations, Vanna is often the hidden force driving market makers to frantically buy or sell spot to hedge risks.

Charm measures the impact of time passing on Delta, also known as Delta decay. As each day goes by, an out-of-the-money option contract without intrinsic value becomes less and less likely to turn profitable. Charm describes how this contract's Delta decays to zero day by day.

The True Essence of Option Risk

From the fundamental Delta to the complex Vanna, these letters reveal the ultimate truth of options trading: what you buy or sell is never a one-dimensional asset but a four-dimensional space woven by price, time, volatility, and probability.

Beginners perish due to direction (misreading Delta), veterans perish due to time (worn down by Theta), while masters often perish due to volatility (bitten back by Vega and Vanna).

Of course, the purpose of writing this article is not just to teach everyone about hedging, but it is more about empowering everyone to understand the rug pulls of DeFi projects.

He Wants Your Interest, You Want His Principal

The key to self-preservation in a bear market lies in seeing through those complex structured products and protecting oneself.

Of course, the complexity of options is challenging to cover in just one article.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia