IOSG: Rising in Silence, Is Circle Underestimated in the Stablecoin Red Sea?

Original Title: "IOSG Weekly Brief | Rising in Silence, Under the Stablecoin Red Sea, Is Circle Underestimated?"

Original Author: Frank, IOSG Ventures

Circle vs Tether: Full-scale War in 2026

On December 12, 2025, Circle obtained conditional approval from the Office of the Comptroller of the Currency (OCC) to establish a national trust bank — First National Digital Currency Bank. Once fully approved, this key milestone will provide top-tier global institutions with entrusted digital asset custody services, fueling the stablecoin market cap to accelerate to $12 trillion within three years. With this momentum, Circle successfully went public in 2025, coupled with the accelerated circulation of USDC, making it the stablecoin issuer most closely connected to institutional investors. As of now, its valuation has reached $230 billion.

▲ Source: IOSG Ventures

While the stablecoin market leader Tether still maintains a high profitability of over $13 billion, its parent company faces ongoing business reputation and regulatory pressures, such as S&P recently downgrading Tether's reserve rating from "strong" to "weak," and Juventus Football Club rejecting its acquisition offer. On November 29, the People's Bank of China held a special meeting to crack down on virtual currency trading, clearly pointing out the deficiencies of stablecoins in customer identification and anti-money laundering, and their frequent use in money laundering, fraud, and illegal cross-border fund transfers. Regulatory focus essentially targets the offshore stablecoin system represented by USDT. USDT dominates in emerging markets such as Asia, Latin America, and Africa, especially with a market share of over 90% in East Asia. Its significant circulation occurs in off-chain P2P and cross-border fund activities, long operating outside the regulatory system, regarded by regulators as a "grey dollarization system" exacerbating capital outflows and financial crime risks.

▲ Source: Visa Onchain Analytics

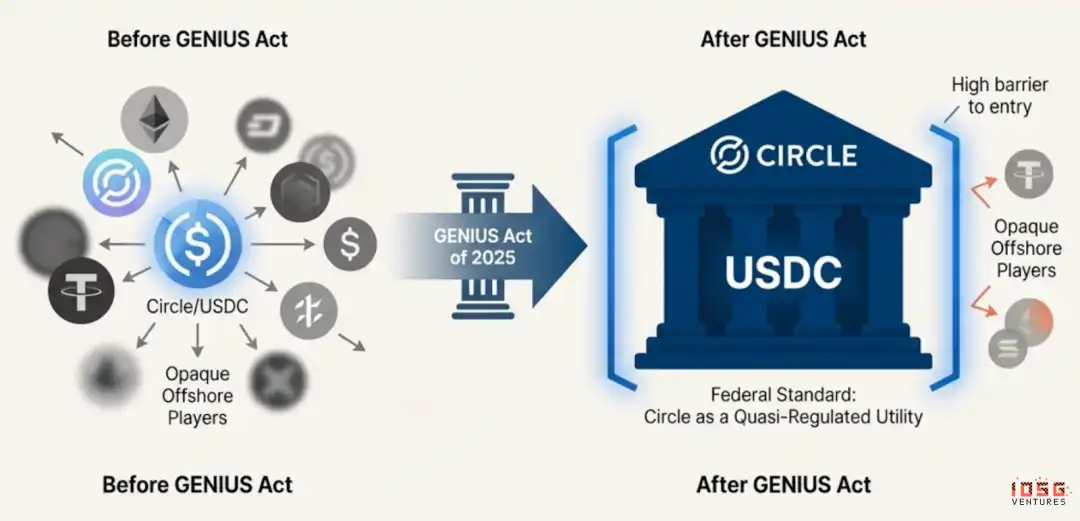

In contrast, the approach taken by the United States and the European Union is not a comprehensive crackdown, but rather integrating stablecoins into the regulatory framework through high compliance standards. For example, the U.S.'s GENIUS Act clearly requires stablecoins to establish a 1:1 high-quality reserve, undergo monthly audits, obtain a federal or state license, and prohibits the use of high-risk assets such as Bitcoin or gold as reserves.

In other words, China aims to compress the "offshore stablecoin shadow USD system" from its source, while Europe and the U.S. are attempting to establish a "controllable, compliant, and regulation-friendly digital USD system." The common point between these two paths is: both are unwilling to let opaque, high-risk, unauditable stablecoins occupy a systemic position. This means that compliant issuers like Circle can enter the financial system, while offshore stablecoins like Tether will gradually be phased out in developed markets. This is also why Tether has recently begun to vigorously develop its USAT, its first U.S.-compliant stablecoin.

▲ Source: Artermis

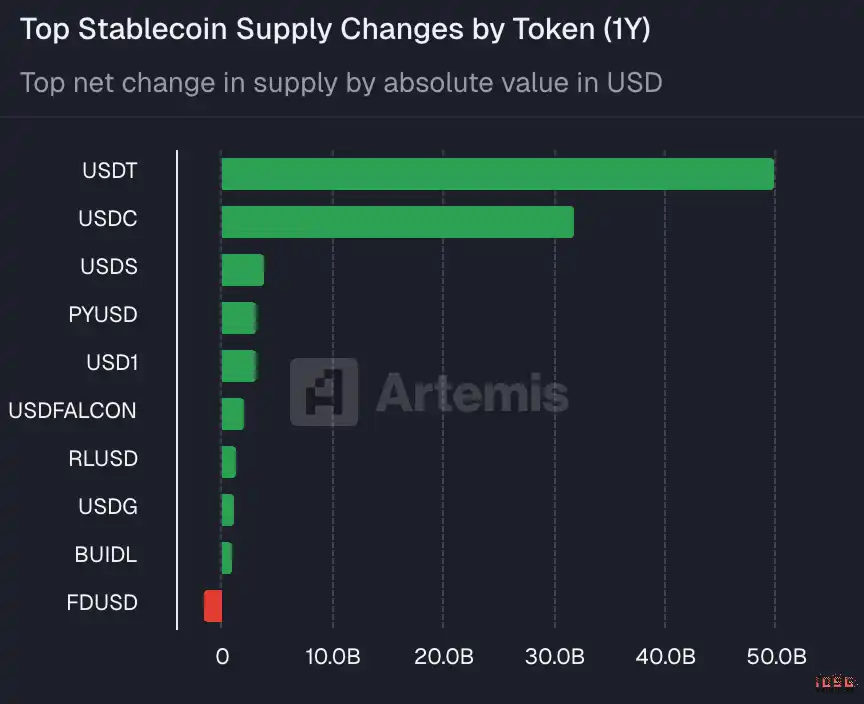

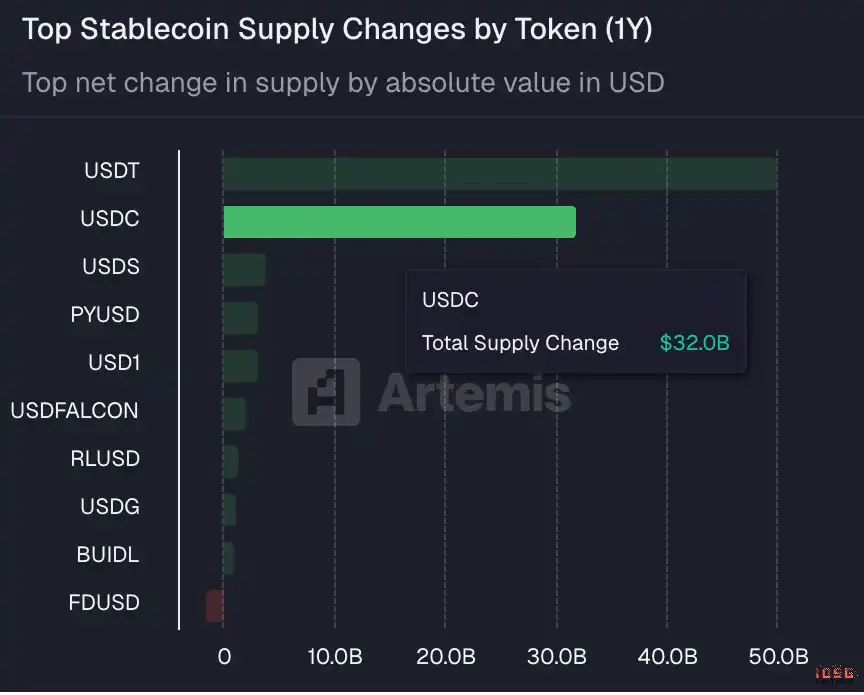

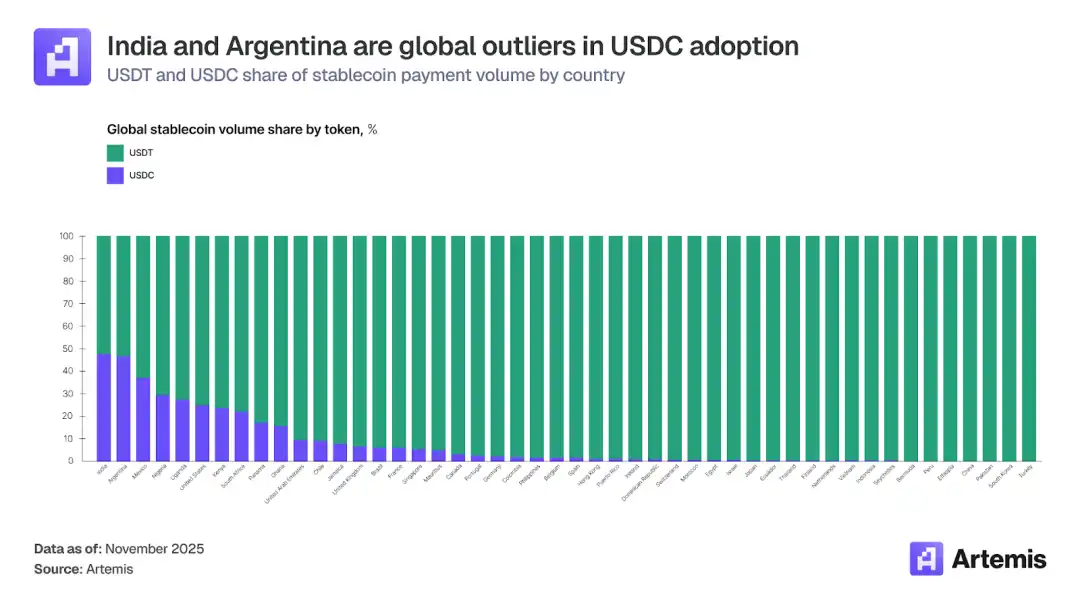

While Tether may still maintain its dominance in offshore and emerging markets, over the past year, Circle's USDC has also increased its net supply by $32 billion, second only to USDT's $50 billion.

However, Circle has made significant progress in challenging Tether in offshore and emerging markets, with its market shares in India and Argentina reaching 48% and 46.6%, respectively. The primary reason USDC's position in these offshore markets has increased is due to the explosive growth of its crypto card business over the past few years.

▲ Source: Artermis

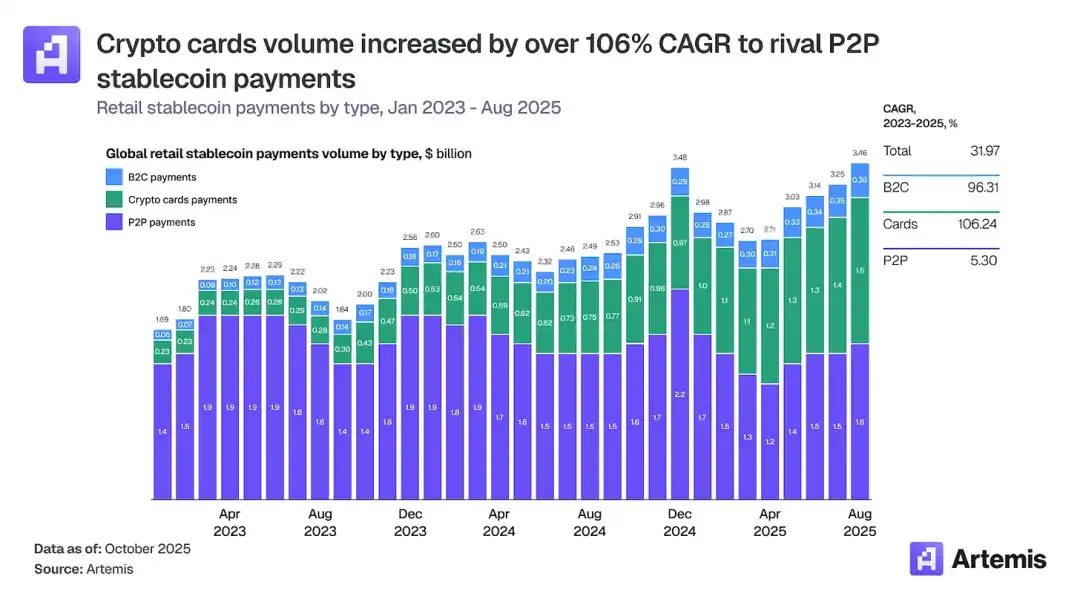

Crypto cards allow users to spend stablecoins and cryptocurrency balances at traditional merchants and have become one of the fastest-growing submarkets in the digital payment space. Transaction volumes have grown from approximately $100 million per month in early 2023 to over $1.5 billion by the end of 2025, with a compound annual growth rate of 106%. On an annual basis, the market size now exceeds $18 billion, comparable to peer-to-peer stablecoin transfers ($19 billion) that have only grown by 5% during the same period.

▲ Source: Artermis

The opportunity of a stablecoin card lies in addressing a genuine need in many offshore markets, rather than just being a gimmick. In India, many users still lack access to credit through traditional banks, and a cryptocurrency-backed credit card precisely caters to this need. Meanwhile, the people of Argentina face severe inflation and currency devaluation. A stablecoin debit card helps individuals preserve their wealth by holding an asset pegged to the dollar.

Due to the requirement of accessing the Visa or Mastercard network to transact with local merchants, USDC naturally emerged as the most suitable compliant stablecoin, thus gaining a significant transaction volume share in these offshore regions and countries where these stablecoin cards are popular. Therefore, we also see Circle and Tether intensifying their competition in areas where they excel, and in the short term, it is difficult to determine who has the upper hand in this competition.

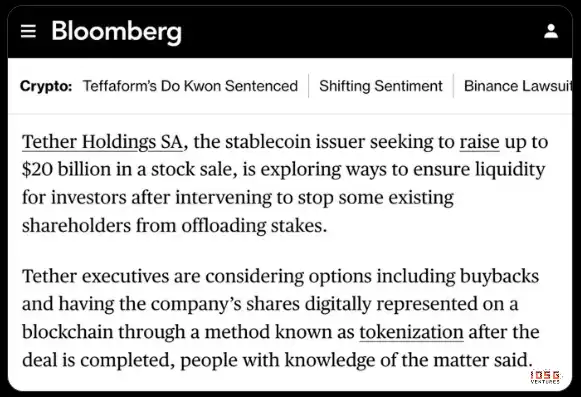

Of course, from a valuation perspective, the two are not in the same league at all. USDT's OTC Valuation has reached 300 billion, and there is also news from Bloomberg reporting a recent 200 billion financing round at a valuation of up to 500 billion. Meanwhile, Circle's latest market price is only 18.5 billion.

▲ Source: Bloomberg

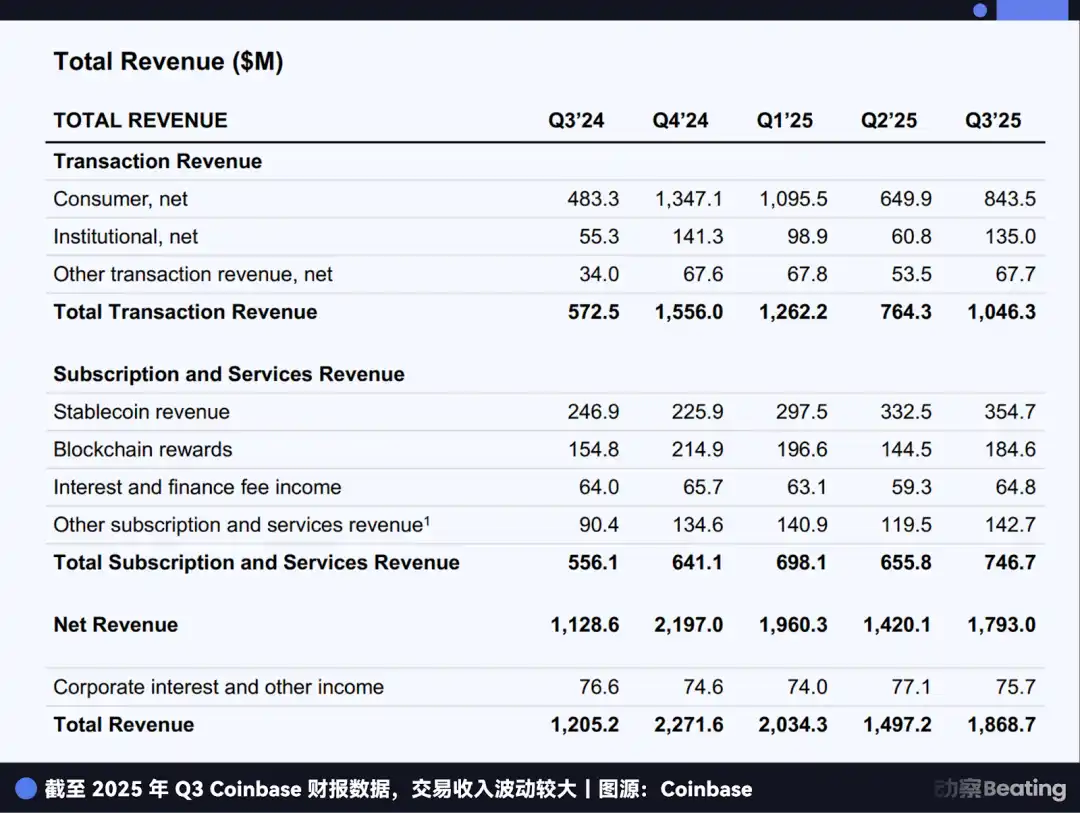

In addition to its market monopoly position, the premium in Tether's valuation is influenced by many other factors, but the primary factor is the advantage of Tether's business model, which does not require profit-sharing with companies like Coinbase as Circle does. According to Circle's S-1 filing, Coinbase can earn a 100% reserve yield on the USDC held on its platform. For USDC held off-platform, such as on other exchanges, DeFi protocols, or personal wallets, the interest income generated is split equally 50/50 between Circle and Coinbase.

▲ Source: Beating

According to data compiled by Dune Analytics, Coinbase's revenue in Q3 2025 reached 354.7 million, which is 50% of Circle's own interest income of 711 million during the same period. In other words, for every 2 dollars of interest earned by Circle, 1 dollar has to be shared with Coinbase.

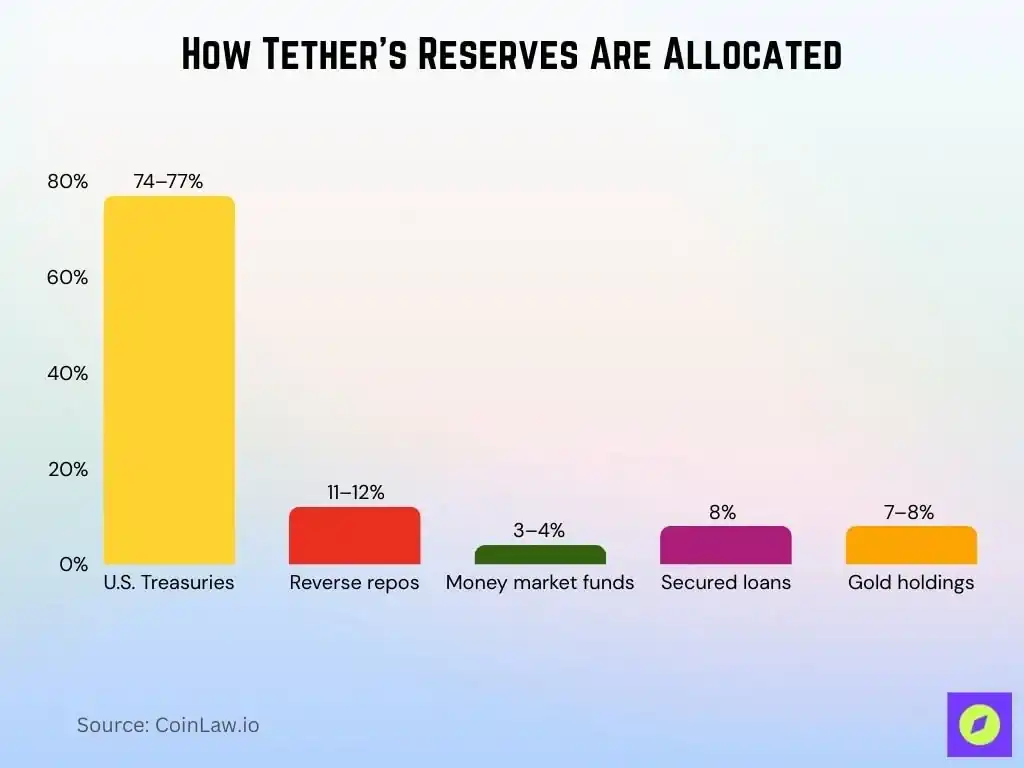

In addition to not having to share revenue, Tether's USDT has a huge advantage in not needing to adhere to collateral restrictions. If Circle adopts an extreme reserve "conservative strategy": 85% is short-term U.S. Treasuries with a maturity of no more than 90 days and overnight repurchase agreements, and 15% is cash and cash equivalents, all held in custody by BlackRock or BNY, with monthly audit reports provided by the accounting firm Grant Thornton LLP, ensuring a 1:1 cover between circulation and reserves that can be real-time verified.

▲ Source: CoinLaw

In comparison, we can see that USDT's collateral is more diversified compared to Circle, which will also lead to higher reserve income, especially in the context of market risk aversion and the continuous rise in the price of gold, making it more important.

This inevitably raises the question: If we follow the path of "highly compliant + regulatory whitelist," is a compliant stablecoin itself really a good business?

Circle Financial Report: Comprehensive Growth in Q3

First, let's review Circle's primary revenue model and revenue situation as a stablecoin company. Circle's stablecoin is backed 1:1 by cash and short-term U.S. Treasuries and issued as collateral. In a high-interest rate environment, these collateral reserves can generate significant interest income.

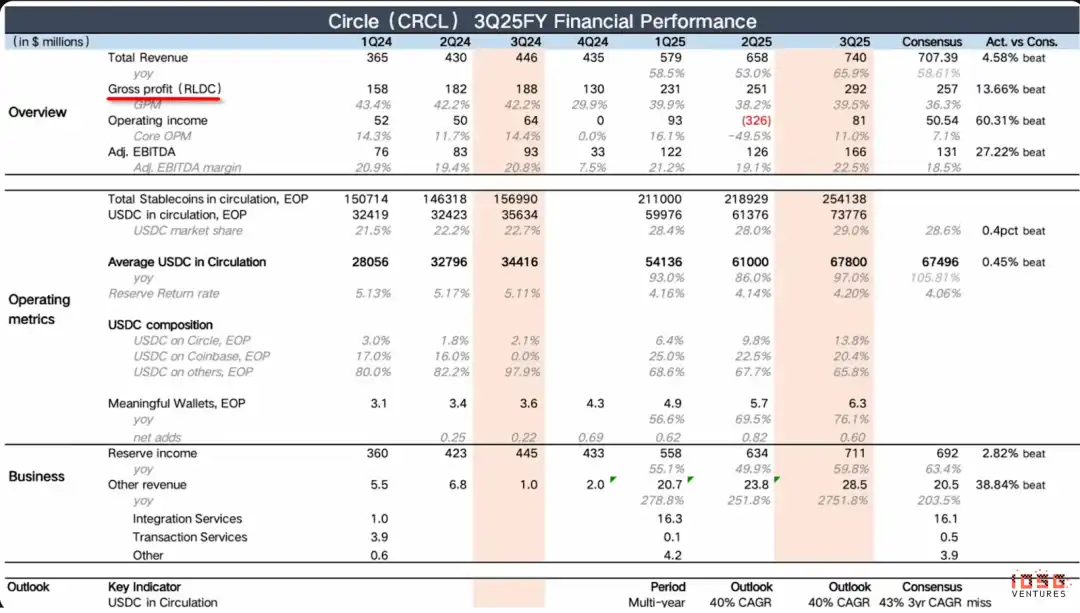

In the third quarter of this year, Circle's revenue reached 740 million dollars (of which 711 million dollars were solely from interest income), surpassing the expected 707 million, growing by 66% YoY, although the MoM growth rate has slightly decreased, from 13.6% in the previous quarter to 12.5% this quarter, but overall, it is still at the same level.

The USDC circulation almost doubled, and the Adjusted EBITDA profit margin reached 22.5%. This growth, combined with profitability, represents a rare combination, making it stand out in the fintech sector as one of the few examples with high growth and high profitability.

▲ Source: Circle Q3 Earnings

During this quarter, the company's Revenue Less Distribution and other Costs (RLDC) reached $292 million, significantly exceeding market expectations, with its growth rate staying largely in line with the previous two quarters. RLDC (Revenue Less Distribution and other Costs) is calculated as total revenue minus profit from distribution, transactions, and other related costs. The RLDC Margin is the percentage of RLDC in total revenue, used to measure the profitability of the core business.

Operating Income also significantly outperformed market expectations. The previous quarter's Operating Income was negative, mainly due to one-time equity incentives totaling $424 million in Stock-Based Compensation (SBC) and a $167 million Debt Extinguishment Charge. Therefore, for better comparability, we use Adjusted EBITDA to add back non-core, one-time expenses such as depreciation, amortization, taxes, and equity incentives to reflect the recurring operational performance of the core business. Looking at the performance of Adjusted EBITDA, both year-over-year and quarter-over-quarter growth rates accelerated, with a 78% YoY increase and a 78% QoQ increase, surpassing market expectations by 31% YoY.

We can see that Circle's primary source of revenue comes from interest generated by reserve assets. However, this revenue model is very fragile and directly impacted by macro interest rates. Therefore, Circle's main challenge is whether it can quickly transition from a single, fragile stablecoin revenue model to a diversified income stream.

▲ Circle Q3 Earnings

Therefore, in this financial report, the focus is on the growth rate of other income and the percentage increase of other income in overall revenue; as long as these two continue to grow, it indicates that Circle's revenue model is improving. Conversely, if the growth rates of these two aspects decline, it would be a more bearish signal.

We can see that other income is $28.5 million, significantly surpassing market expectations. However, considering that the base figure for the same period last year was only $1 million, the year-over-year data has limited reference significance. More practically meaningful sequential data shows a growth rate of 20% this quarter, accelerating from 15% in the previous quarter, indicating that this revenue segment is indeed growing rapidly. However, currently, "other income" accounts for less than 4% of total revenue, indicating that changing Circle's single revenue structure will take time.

Nevertheless, this is still a positive signal. Expecting a fundamental shift in the revenue model to be completed in just six months is unrealistic. The current robust QoQ growth has laid a solid foundation for future diversification.

▲ Source: Circle Q3 Earnings

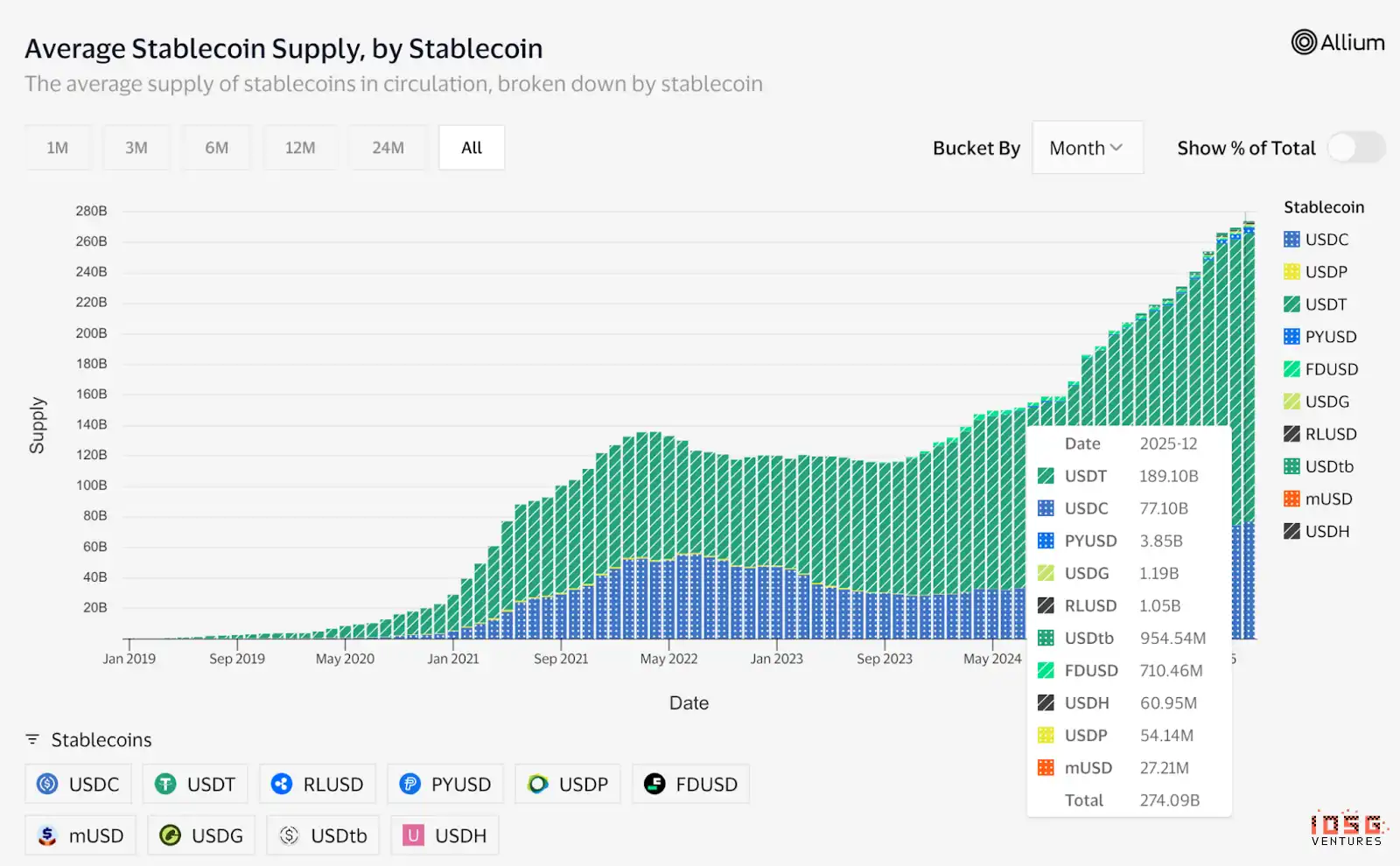

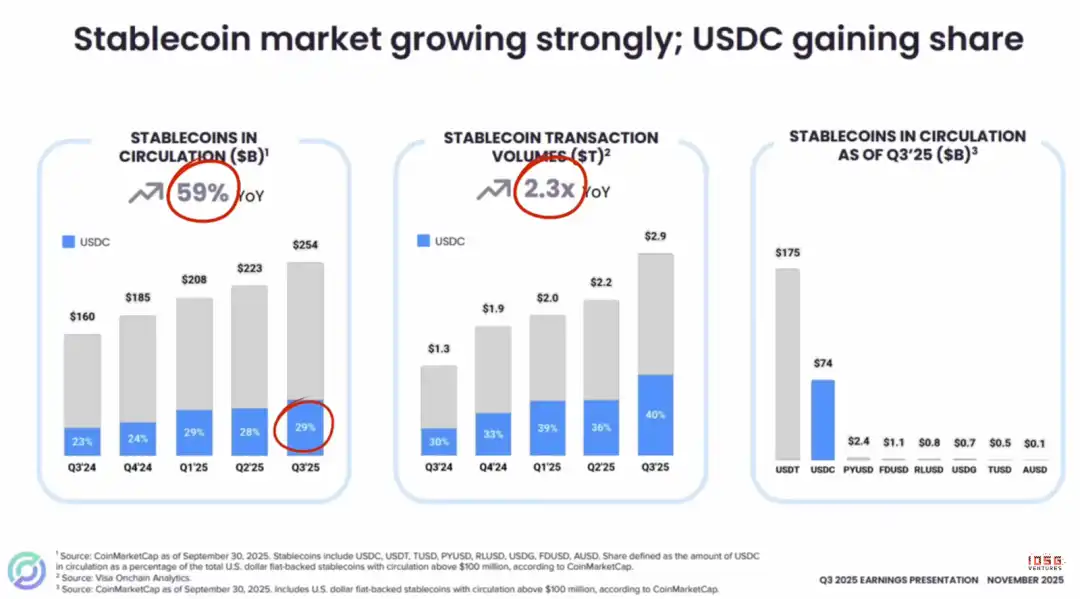

From a more macro perspective, the stablecoin market is experiencing rapid growth, with its total supply increasing by 59% YoY, and on-chain transaction volume reaching 2.3 times that of the same period last year, demonstrating significant market potential.

In this context, USDC's performance is particularly outstanding, with its market share steadily climbing to 29%. It is worth noting that even in the face of recent competition from emerging stablecoins like Phantom $CASH, USDC's upward trend has not been interrupted.

There is a common concern in the current market: Will the increasing issuance of stablecoins lead to USDC no longer being the best choice for a stablecoin? From platforms offering "Stablecoin Issuance as a Service" (such as from Bridge to M0 to Agora) to numerous enterprises entering the field, these phenomena seem to foreshadow an industry engulfed in excessive competition (internal strife), eroding long-term profitability. However, this view largely overlooks a key market reality.

The growth in USDC's market share is mainly attributed to a favorable environment created by regulatory developments such as the "Genius Bill." As a leader in compliant stablecoins, Circle occupies a unique strategic position. Globally, in regions where stablecoins are already regulated, such as the United States, Europe, Asia, as well as in the UAE and Hong Kong, mainstream institutions tend to view Circle as the preferred partner due to its trustworthiness, transparency, and liquidity in compliance infrastructure; otherwise, their relevant businesses may struggle to operate.

Therefore, regarding concerns that emerging stablecoins in the market may challenge USDC's market dominance, we believe this view is difficult to substantiate. On the contrary, USDC not only can solidify its second position for a long time but also has the strength to challenge the market leader with its unparalleled compliance advantage. The network effects barrier to entry may last for 2-3 years.

▲ Source: Circle Q3 Earnings

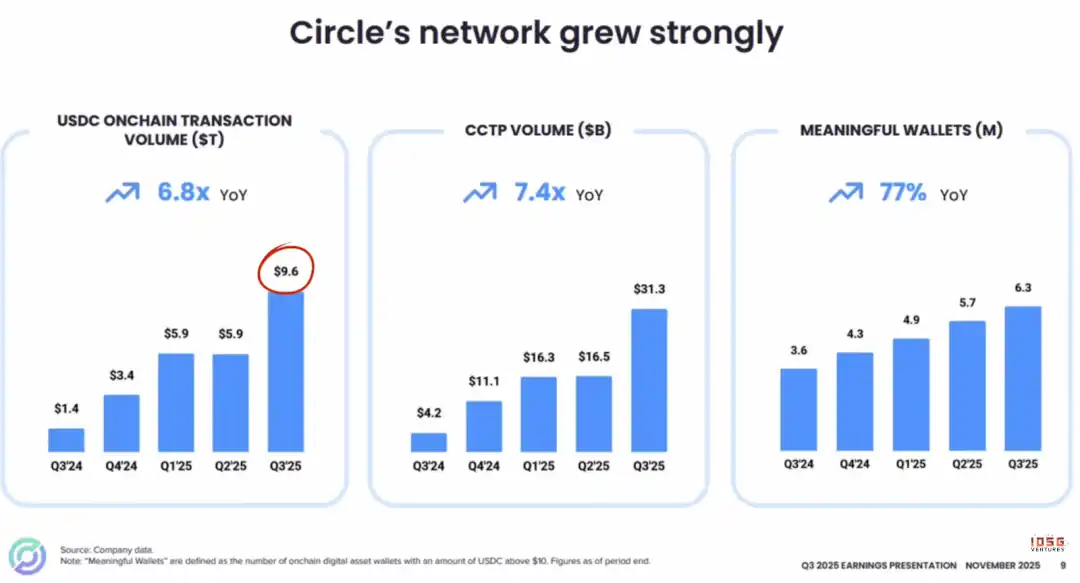

USDC on-chain activity is experiencing explosive growth. Its on-chain transaction volume has surged to $9.6 trillion, a 6.8x increase from the same period last year.

This growth is fueled by the success of its Cross-Chain Transfer Protocol (CCTP). The CCTP enables seamless and uniform circulation of USDC across different blockchains through a process of burning on the source chain and minting natively on the destination chain, avoiding the complexity and risks of traditional cross-chain bridges.

Overall, whether it's on-chain transaction volume, CCTP usage data, or the growth in active wallets (balance greater than $10), all indicators clearly point to the same conclusion: USDC's adoption and network speed are continuously and significantly expanding.

▲ Source: Visa

In terms of ecosystem partnerships, Visa announced on December 16th its launch of USDC settlement capability on the USDC network, allowing US financial institutions and their customers (with Cross River Bank and Lead Bank as the first adopters) to settle in USDC via the Solana blockchain with Visa.

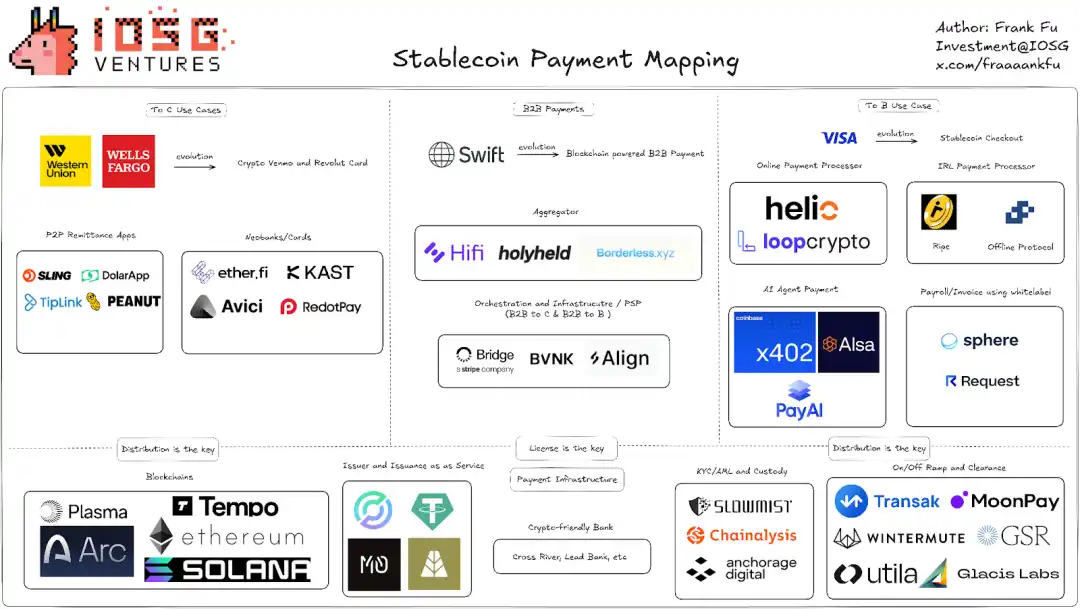

· For those familiar with the B2B Payment Landscape of stablecoins, Cross River Bank and Lead Bank are among the most crypto-friendly banks in the US. For example, Cross River Bank and Lead Bank serve as Sponsor Banks to support companies like Baanx and Bridge, enabling fintech firms without banking licenses to "borrow" their qualifications to issue bank cards and even launch white-label card issuance services. For B2B stablecoin payment companies, this allows access to traditional payment networks such as Visa/Mastercard Principal Membership and the use of VisaNet, MastercardNet, ACH, FedWire, RTP, and other traditional payment channels for fiat currency clearing and settlement.

▲ Source: IOSG Ventures

The significance of this collaboration is to allow Visa partner institutions to convert all settlement transactions of their Visa cards to USDC at the settlement layer, resulting in an enhancement that enables banks and fintech firms to settle transactions 7 days a week, replacing the traditional 5-day settlement window, thus accelerating fund movement speed and liquidity. Previously, while Visa could authorize transactions 24/7 at 1.5 billion merchant locations worldwide, settlement was still restricted by bank hours, wire transfer cutoff times, and holiday schedules. With authorizations on Friday and banks closed on Monday, settlement could only be completed by Tuesday.

For Visa, stablecoins and blockchain could be not a threat but a new strategic entry point. Visa's logic is simple: aggressively promote Stablecoin-linked Visa cards. Because, regardless of changes in payment methods, consumers ultimately have to convert stablecoins to fiat to make a purchase, and this "fiat landing" process must first go through the VisaNet network for clearing before fiat interbank settlement.

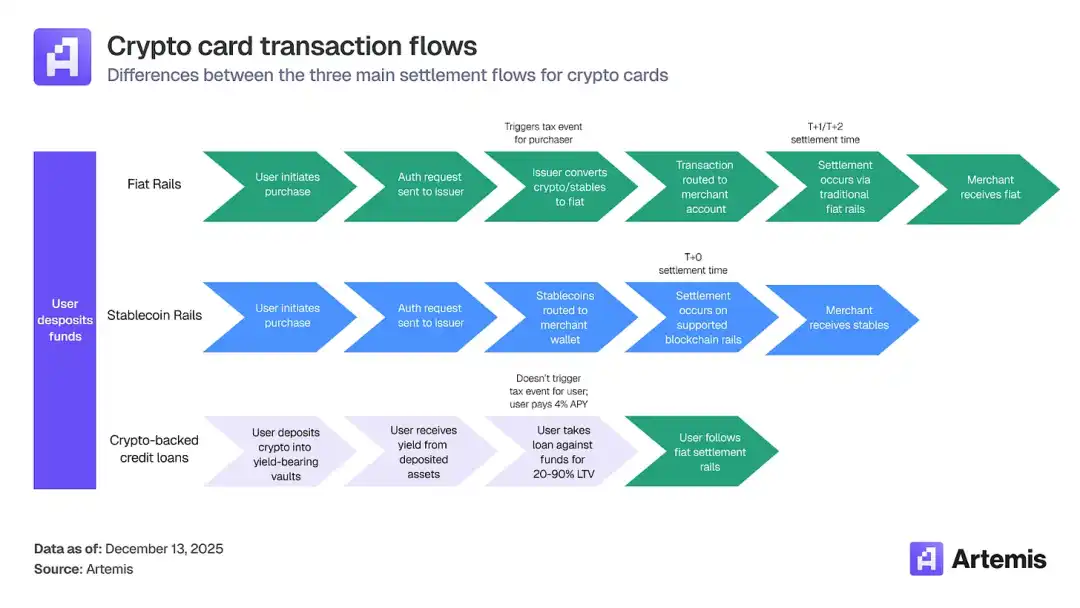

Currently, the vast majority of cryptocurrency card transaction volume is settled through fiat clearing (the first method in the next image), where 24/5 settlement remains the default option as it requires no merchant integration. The conversion from cryptocurrency to fiat is completed before settling on the payment network, so when the transaction reaches the network, the transaction from the cryptocurrency card is no different from any other card payment transaction. From the merchant's perspective at the clearing layer, there is no change—both are fiat currencies. The advantage lies in the user deposit side, where they can spend crypto and deposit without relying on SWIFT.

▲ Source: Artermis

Even if Visa begins a USDC settlement pilot to achieve 24/7 settlement, this is not a threat to Visa but aligns with its strategic interests. The integration of stablecoins has not altered its underlying business logic. All stablecoin card transactions still need to pass through VisaNet and pay a "toll." Visa's core revenue model relies on three main sources: charging interchange fees to issuing banks, collecting acquirer service fees from acquiring banks, and collecting network clearing fees through VisaNet. Therefore, Visa has no need to issue stablecoins itself. Its strategy is clear: continuously onboard more stablecoin issuers (such as Bridge, Rain, Reap, etc.), support more stablecoin currencies (such as USDC, EURC, USDG, PYUSD), and bridge more blockchain networks (Ethereum, Solana, Stellar, Avalanche).

error2026 Strategic Transformation: From "Minting" to "Ecosystem"

▲ Source: Circle's 2025 Year in Review

In the previous analysis of the financial report, we mentioned that Circle's urgent need is to expand its other income and briefly mentioned CCTP. From Circle's strategic layout announced in 2026, we can clearly see its innovative strategy.

Among them, the two categories I personally believe are most likely to see short-term improvement in other income are:

· Transaction Service Fees: This includes minting/redeeming fees, large transfer fees, and more. To understand the potential of this revenue stream, we must look at the macro data behind it: this year, the total transaction volume on the USDC stablecoin network reached an astonishing $46 trillion. Through Circle Mint providing large-scale minting and redemption services for USDC to trading platforms and institutions, charging a transaction fee of 0.1%-0.3%, this business generated revenue of $3.2 million in Q3 2025. The in-house developed CCTP cross-chain and technical services have already supported seamless transfers of USDC on 23 public chains, charging a fee of 0.05% of the cross-chain amount, contributing $2.8 million in revenue in Q3 2025.

· RWA Tokenization Service: by acquiring Hashnote and launching the tokenized sovereign debt fund USYC, charging a 0.25% annual management fee. Currently, the AUM has reached $15.4 billion. When the acquisition was just made in January last year, more than 97% of the tokenized sovereign debt fund USYC was purchased and held by Usual Protocol as the reserve asset for their USD0 stablecoin. However, after the acquisition, Circle is introducing USYC to more trading platforms and distribution channels, amplifying its role as a compliant interest-bearing asset.

One of the most notable recent developments is Deribit integrating USYC. As a leading crypto derivatives trading platform, Deribit now supports USYC as collateral for trading futures and options.

This integration brings several advantages:

· Collateral generates income while securing trading positions

· Lower opportunity cost compared to using non-yielding stablecoins

· Collateral Appreciation may reduce overall transaction costs

· Maintain liquidity, withdraw at any time when needed

For active traders, this means that your "idle" trading funds can continue to earn you returns even as collateral—a feature not possible in traditional margin models.

Looking further ahead, the two most promising revenue categories for Circle are:

First, Circle's proprietary Arc Blockchain: The ARC public testnet is now live, with over 100 global enterprises participating in the testing, including many well-known large institutions. Management anticipates the mainnet to launch in 2026. All participants in the developer ecosystem will be able to seamlessly access this infrastructure, which will also be deeply integrated with Circle's various platforms. Additionally, management is actively exploring the possibility of introducing the ARC native token.

▲ Source: Circle Q3 Earnings

Its core significance is:

1. Vertical Integration: Transaction Medium (USDC) + Channels (Coinbase, Visa) + Settlement Layer (ARC Blockchain)

2. Value Capture Takeback: Previously, USDC ran on Ethereum, Solana, where Gas fees, MEV, and ecosystem value were taken by other blockchains; ARC allows Circle to reclaim this value.

▲ Source: Circle

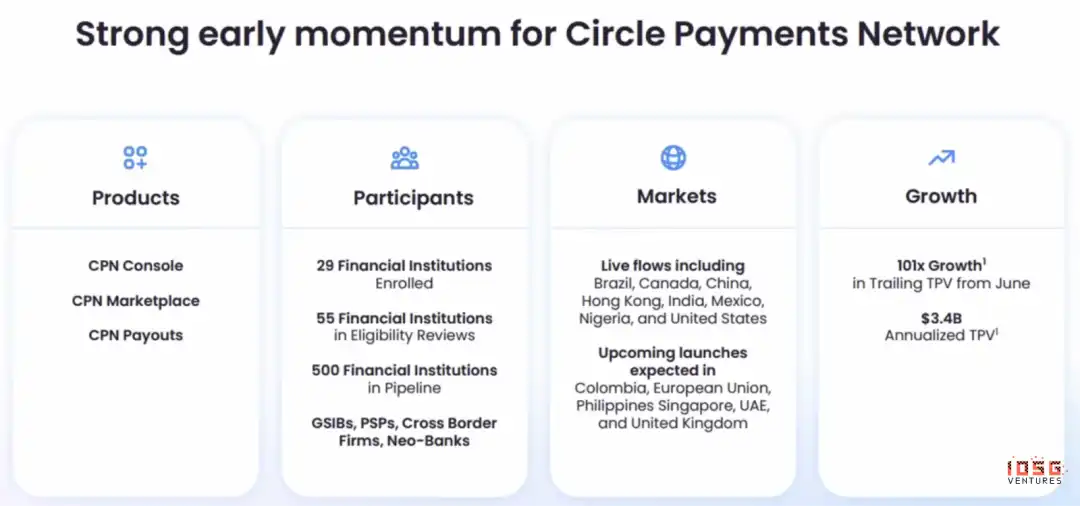

Second, CPN (Circle Payments Network): A B2B payment network for institutions, providing cross-border payment and settlement services based on USDC to large enterprises and financial institutions.

If ARC is considered the underlying operating system, then CPN is the top-level application. CPN has already launched three major products: CPN Console, CPN Marketplace, and CPN Payouts.

What is CPN set to disrupt?

· Traditional Cross-Border Payment Chain: SWIFT + Correspondent Bank + Local Clearing System (e.g., US ACH)

· If settled using a stablecoin, all the intermediate steps mentioned above can be eliminated — CPN maintains the ledgers of all participants directly within the network

· In contrast, while Airwallex bypasses SWIFT and correspondent banks (by using prefunded pools in each country), it still relies on local clearing systems and requires the opening of bank accounts

· CPN's ultimate vision: not even needing a bank account

Although CPN has already attracted around 500 potential customers, the management clearly states that the current focus is not on monetization but on user quality and expanding the network continuously. Once network effects are established, there will be plenty of room to charge fees significantly lower than the traditional model — this is precisely the core of Circle's Second Growth Curve.

Conclusion: Circle's Moat and Long-Term Value

Circle has shown a significant competitive advantage in the stablecoin field, with its core value stemming not only from USDC itself but also from the payment and settlement ecosystem it has built. In the future, the stablecoin market may witness a "Winner takes most" scenario, and Circle has already solidified its leading position through three major moats:

1. Network Effects: USDC has the broadest coverage and best interoperability, forming a powerful ecosystem flywheel. If users or businesses do not access USDC, they may miss out on significant opportunity costs.

2. Liquidity Network: USDC boasts the most comprehensive and extensive integrated liquidity network, providing strong support for transactions and settlements.

3. Regulatory Infrastructure: Circle has obtained 55 regulatory licenses, making it the most compliant stablecoin currently and constructing a robust compliance moat. In the US, legislation like the "Genius Act" and clear regulatory frameworks provide Circle with substantial compliance certainty, which many other crypto companies lack.

▲ Notebook LLM Generated

With the stablecoin market expected to reach a total issuance of $20 trillion by 2030, Circle is poised to maintain its leading position in the digital dollar ecosystem, leveraging its core moats and execution capability. Despite facing challenges such as a low-interest-rate environment, a single revenue model, and high margin costs, Circle is transitioning its business model from a simple spread revenue model to a network services and infrastructure model centered around USDC. While its highly compliant path may increase operational costs in the short term, in the long run, it will solidify regulatory advantages, enabling it to capture the value of the global traditional financial and institutional markets.

This logic is similar to China's mobile payment landscape: WeChat Pay and Alipay dominate almost all daily payment scenarios. If a merchant does not integrate these two major payment tools, they will miss out on a large number of customers, severely impacting revenue. This also explains why emerging payment methods, such as Douyin Pay, find it difficult to expand rapidly in a short period of time—even if the product is powerful, without a user base and merchant network integration, it is difficult to reach a critical mass and initiate an ecosystem flywheel.

Likewise, USDC has already established a similar "first-mover advantage" in the digital dollar payment and settlement ecosystem, where its network effects and interoperability make it difficult for new competitors to challenge its existing position. For merchants and institutions, integrating with USDC is not only transactionally convenient but also a necessary condition for market access.

In other advantageous aspects, Circle's own business model possesses very high marginal efficiency and scalable revenue.

The interest income generated by the stablecoin's reserve will scale rapidly with its issuance, while the growth rate of its operating costs will be much slower, resulting in high marginal profits.

Furthermore, Circle's leadership has repeatedly demonstrated crisis management capabilities, earning recognition for its team. During the 2023 SVB-induced USDC decoupling crisis, Circle proved its strong crisis management and execution capabilities. When Silicon Valley Bank (SVB) collapsed in 2023, and since a portion of USDC's reserve was held at SVB, the market was briefly concerned about the security of USDC's 1:1 dollar reserve, resulting in USDC briefly decoupling (falling below $1). Some of Circle's key actions at that time were:

· Quickly disclosing the facts: Clearly stating how much funding was exposed at SVB, rather than being ambiguous

· Continuously updating information: Consistently providing the latest developments to the market, rather than going "silent"

· Clearly committing to the outcome: Emphasizing that even with losses, Circle would still back USDC's 1:1 redemption

The team successfully stabilized market confidence through decisive and transparent communication. The company has also been recruiting some experienced leadership teams, with its most recent 2025 president being the former CFTC chairman, Heath Tarbert, who, before joining Circle, held high-level government positions such as Assistant Secretary of the U.S. Treasury.

From a short-term perspective, Circle still faces certain structural and market-level pressures. Firstly, as global monetary policies gradually enter a rate-cut cycle, the downward movement of interest rates will directly squeeze Circle's core income source based on reserve interest, significantly increasing its sensitivity to macro interest rate changes in the short term; at the same time, the company's current revenue model is relatively singular, with a high reliance on USDC scale and interest rate levels, lacking sufficient diversification of non-interest income buffers. Secondly, to maintain the circulation scale and network effects of USDC, Circle needs to pay a relatively high percentage of revenue-sharing costs to distribution channels such as trading platforms and payment platforms, which may further erode profit margins during a period of slowing growth.

At the market level, the stock price has recently continued to weaken and is trading below the 50-day moving average, holding at $80 per share, reflecting a cautious short-term fund sentiment, with technical pressure still evident. The main reason is due to the lock-up period after December 2, 2025, i.e., 180 days after the IPO. The lock-up scale is very large, representing an impact at the fully diluted level. Before the lock-up period, the market's floating shares accounted for only about 17.2% of the total share capital. After the lock-up period, theoretically almost all shares can be traded on the market, instantly increasing the float by nearly 400%. The selling pressure after the lock-up mainly comes from early investors and management, with most of their holdings acquired at a cost of $10 or less. Insiders can continue to divest through 10b5-1 trading plans. For example, Director Patrick Sean Neville sold 35,000 shares at $90/share on December 12, 2025.

In addition, Circle's biggest short-term risk is that many investors may choose to short Circle during a period of falling interest rates, using Circle as a hedge against interest rates. However, Circle's potential growth lies in its diversified ecosystem. Circle is not just the issuer of USDC; it is also building a comprehensive financial technology ecosystem that includes payment, trading, and Web3 services, which helps diversify its sources of revenue and engage users.

Overall, Circle's long-term value proposition is clear, but short-term volatility must be tolerated, as technical factors and macro uncertainty may continue to bring about fluctuations. From a holistic perspective, Circle's current stock price is somewhat undervalued compared to its intrinsic value. Currently, Wall Street's DCF model gives an intrinsic value range of $142 per share, higher than the current market price, indicating a certain margin of safety at the fundamental level. It is worth noting that due to Circle's stable cash flow, clear regulatory position, and relatively manageable risk exposure, Circle's WACC is only 4.02%, a level more akin to low-risk, highly cash-generative utility companies rather than typical high-volatility tech or crypto firms, reflecting that the capital market views its core cash flows as stable and defensive assets.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia