Coin Launch at Year End, What Makes Lighter Stronger than Hyperliquid

Recently, several addresses suspected to be associated with Lighter team members bought $125,000 worth of "YES" shares in the polymarket's "Will Lighter TGE Before End of Year" market. A few days ago, Coinbase also announced the addition of LIGHTER to its listing roadmap. All signs indicate that Lighter's TGE is indeed imminent.

The market will eventually punish every arrogant bystander, just as many habitually viewed Hyperliquid as a performance-enhanced but more centralized GMX initially, many people instinctively see Lighter as yet another imitator of Hyperliquid.

However, Lighter differs vastly from Hyperliquid in terms of business model, development strategy, and technical architecture. These differences suggest that Lighter will become the first real threat to Hyperliquid outside of centralized exchanges. Every participant in the crypto market may need to ask themselves if they truly understand Lighter.

Trading Time for Money

Hyperliquid uses a fee structure graded by trading volume, making it difficult for low-volume retail traders to enjoy fee discounts. In contrast, Lighter does not charge any fees to standard accounts, with users only incurring slippage costs, making Lighter more competitive for retail and high-frequency traders.

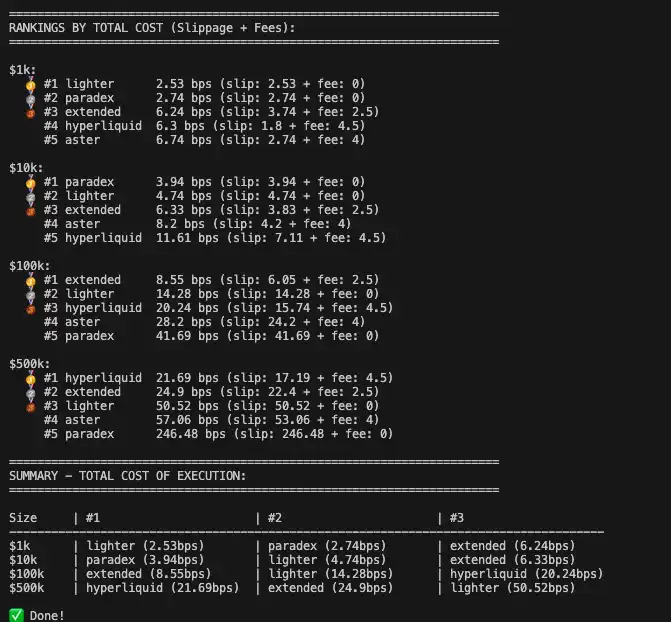

According to community user @ilyessghz2's calculations, Hyperliquid's low fee advantage mainly benefits large funds of over $500,000. For regular traders with capital between $1,000 and $100,000, Lighter's total execution cost (slippage + fee) is significantly lower than Hyperliquid.

Comparison of slippage and fees for different trading amounts on 5 Perp DEXs

But there's no such thing as a free lunch. Behind the 0 fees, Lighter essentially adopts a "trading time for money" business model.

Lighter does not directly route order flow to specific market makers like Robinhood does, nor does it allow market makers to front-run user orders. Instead, it charges fees to professional market makers and institutions to provide a lower-latency trade execution channel. In contrast, free standard retail accounts experience a small execution delay (300 milliseconds).

This mechanism creates an asymmetric market environment: traders using the zero-latency channel can take advantage of speed to respond more quickly to market signals.

For retail traders, the additional cost of latency (slippage or worse execution price) is still much lower than the trading fees on most platforms, and most retail traders do not mind if their orders are executed 300 milliseconds later; market makers are willing to pay for this speed advantage, as in extreme market conditions with a significant price swing within a very short time (such as breaking news), speed advantage can directly translate into profit.

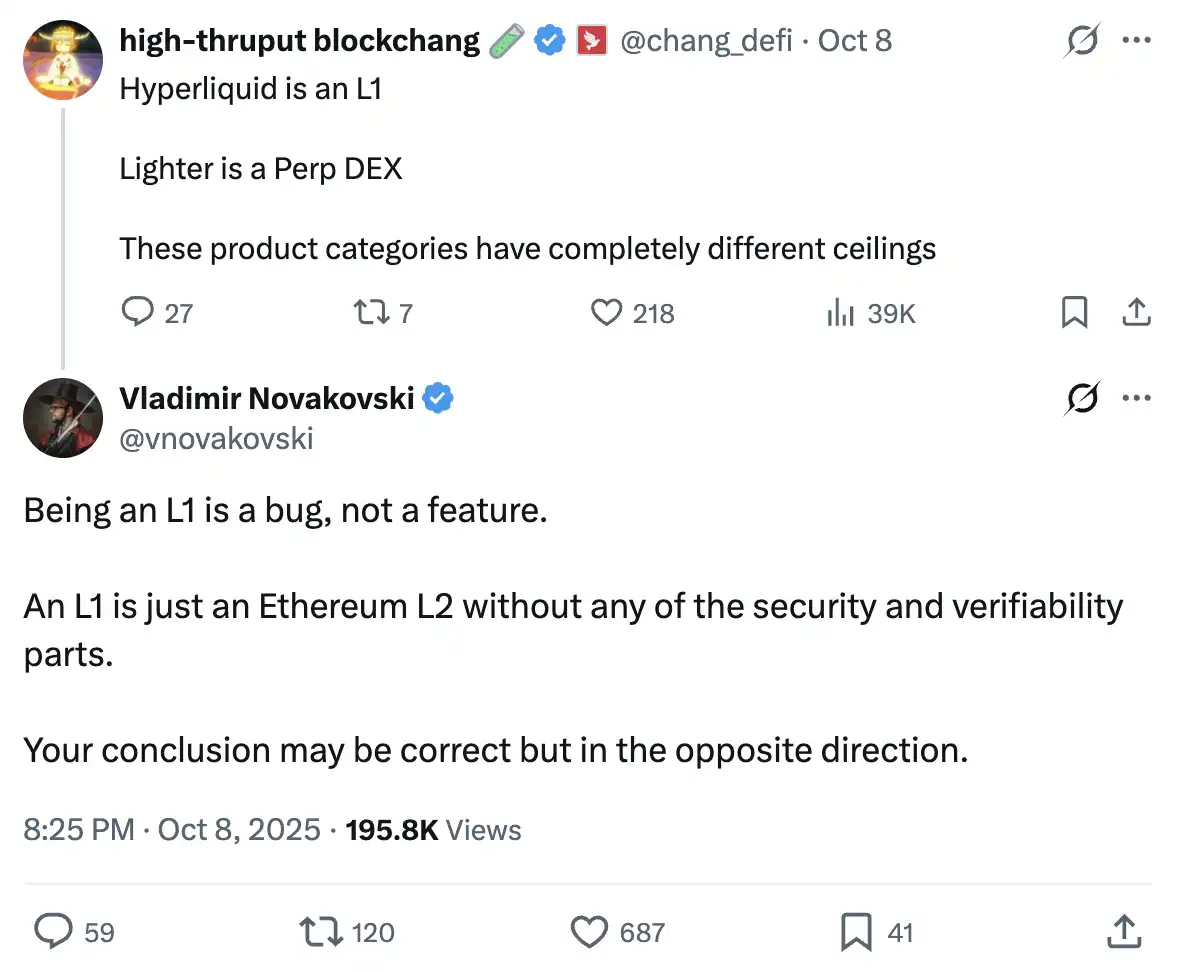

「L1 Is a Bug」

Lighter's founder's statement that "L1 is a bug, not a feature" once put himself in the spotlight, but this statement indeed hinted at Hyperliquid's pain points.

As a monolithic application chain, Hyperliquid requires institutions to bear additional trust costs for the cross-chain bridge nodes and the chain's security itself.

In the "JellyJelly Attacks HLP" event, the team protected HLP's funds in a "cut the network cable" manner. The "formalism" of validator voting cannot cover up the platform's centralization flaws.

At the same time, Hyperliquid's spot trading relies on HyperUnit, a multisig cross-chain bridge controlled by a few nodes. The dark history of multisig cross-chain bridges like Ronin, Multichain, repeatedly proves that no matter how sophisticated the multisig design is, as long as it involves human trust, there is a risk of being 51% attacked by hackers through social engineering.

In comparison, choosing to become an Ethereum L2 allows Lighter to not rely on third-party trust assumptions. After entering Stage 1 of L2 in the future, even if Lighter's sequencer behaves maliciously or crashes, users can still force withdrawals through the ETH mainnet contract.

In addition to trust issues, another benefit of becoming an L2 is the ability to tap into Ethereum mainnet liquidity. The crown jewel of the Lighter tech stack is a "universal full-collateral system" supported by "bridge-less cross-chain" technology.

The liquidity in DeFi is fragmented. User deposits on Aave, LP tokens on Uniswap, stETH staked on Lido cannot be directly used as trading collateral.

Using ZK technology, Lighter enables users to lock assets from the Ethereum mainnet (such as stETH, LP tokens, or even future tokenized stocks) in an L1 contract while directly mapping them to collateral on L2, without relying on a separate cross-chain bridge. This means users can hold stETH on the mainnet to earn staking rewards while using it as collateral to open contracts on Lighter and settle in real-time on the mainnet, achieving "yield stacking" and maximizing capital efficiency.

This mapping capability gives Lighter a level of security that other L1 Perp DEXs cannot reach, making it a key advantage when attracting institutional funds.

Feudalism vs. Unification

When it comes to building an EVM-compatible solution, Lighter has chosen a different path from Hyperliquid. HyperEVM and HyperCore operate on a single consensus mechanism (HyperEVM's execution environment is integrated into its L1 cache), where the generalized computation of the EVM easily competes with the core transactional engine (HyperCore), leading to performance bottlenecks.

LighterEVM adopts a horizontal architecture. Lighter's core transaction engine (LighterCore) runs on a custom ZK circuit, focusing on ultimate matching efficiency, while general smart contracts run on a parallel LighterEVM (based on zkVM). The two are logically separated but can atomically share state.

Source: https://x.com/0xJaehaerys/status/1983251296095482338?s=20

This "storefront vs. factory" design brings two main advantages:

First is performance isolation, ensuring that no matter how congested on-chain lending protocols or NFT markets are, the core order book's matching speed remains unaffected.

Second is atomic composability, allowing developers to build complex structured products on LighterEVM (such as automated options vaults or prediction markets). These contracts can directly read LighterCore's order book and execute hedging trades without the need for cross-chain operations or delays.

In terms of liquidity, Hyperliquid delegated market deployment rights to external teams through HIP-3, bringing prosperity to the ecosystem and strong buying pressure on HYPE. However, this also led to liquidity fragmentation. For example, TSLA's perpetual contract exists simultaneously on two different exchanges, Felix and Trade.xyz. Furthermore, the compliance responsibility in this model is blurred, making it challenging to meet regulatory requirements.

Lighter adheres to a monolithic unified architecture, avoiding the issue of liquidity fragmentation. Additionally, with endorsements from top-tier venture capitalists with political and business resources such as Founders Fund and a16z, Lighter is also more likely to be accepted by traditional financial institutions on a compliance level.

Hyperliquid's transparent trading feature is a clear disadvantage for large fund users. On-chain data will publicly reveal the entry price and liquidation point of all large positions, exposing large holders to the risk of front-running or targeted liquidation.

Lighter can conceal users' trading and holding data. Aside from advertising and ego satisfaction purposes, well-capitalized traders are not willing to expose their hand in front of their counterparty. For large funds and institutional investors, anonymity is a basic requirement when conducting large transactions.

As the on-chain derivatives market matures, platforms that can effectively protect user transaction privacy will have a better chance of attracting core liquidity.

The New "Iron Triangle," or Another TGE Curse?

An "Iron Triangle" consisting of "Robinhood-Lighter-Citadel" seems to be emerging.

Lighter's founder, Vladimir Novakovski, previously worked at Citadel, the world's largest market maker, and served as an advisor to Robinhood. Robinhood is the most widely used retail brokerage for US stocks, Citadel is Robinhood's largest market partner, and Robinhood is a direct investor in Lighter.

In an ideal scenario, this could become a perfect business loop. Robinhood is responsible for frontend customer acquisition, bringing tens of millions of US stock retail investors into the crypto world; Lighter acts as the backend execution engine, responsible for matching and clearing, providing a Nasdaq-level trading experience and the security brought by ZK-rollup; Citadel is responsible for providing liquidity.

Once Citadel decides to make Lighter its primary venue for hedging and trading tokenized stocks, stock perpetual contracts, and RWAs, downstream brokers dependent on its liquidity are highly likely to follow suit for access. In this narrative, Lighter becomes the interface connecting traditional finance with the on-chain world.

However, TGEs are often a watershed moment for the fate of a Perp DEX. The key to Hyperliquid's success lies in its ability to achieve organic growth in trading volume after the end of the incentive program, breaking the curse of "mine and dump."

Lighter, with a clearly defined VC unlock schedule, faces a more severe test. After the airdrop expectations are met, will users flow to the next Perp DEX? With worsened slippage due to loss of liquidity, the trading experience is directly impacted, potentially triggering a negative loop of continued volume contraction.

Shifting focus away from localized games of stock, a broader narrative is unfolding.

A year ago, few could have predicted that Hyperliquid would truly challenge centralized exchanges. From this perspective, Lighter and Hyperliquid are comrades in the same trench. They both point to that old order that has long dominated the crypto world.

The war of Perp DEX against CEX has only just begun.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia