Forum

Forum OPRR

OPRR Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Data

Data

The Stablecoin's Secret Goldmine: How to Profit from US Treasuries and Interest Rates?

Summarized by AI

Summarized by AI

Original Article Title: How Stablecoins Profit From U.S. Debt & Interest Rates

Original Article Author: @threesigmaxyz

Original Article Translation: zhouzhou, BlockBeats

Editor's Note: This article explores how stablecoins such as USDT and USDC generate billions of dollars in revenue by investing their reserves in U.S. Treasury securities, with their income closely tied to the Federal Reserve interest rate. If interest rates were to drop to zero, their profitability could plummet. As demonstrated by USDC in the 2023 Silicon Valley Bank incident, fiat-backed stablecoins face regulatory challenges and the risk of being uncoupled, while algorithmic stablecoins like USDe rely on crypto-native yield, making them less sensitive to interest rate fluctuations. Tether's $20 billion war chest ensures a decades-long runway, but Circle's $1.68 billion in revenue in 2024 and limited liquidity make it vulnerable with a sustainability window of only 18-25 months.

The following is the original content (lightly edited for clarity):

The Shift Toward Stability in Cryptocurrency

Initially, Bitcoin was seen as an alternative for traditional currency, a decentralized, borderless, censorship-resistant form of money. However, due to its high volatility (price fluctuations) and evolution into a speculative asset and store of value, along with high blockchain transaction costs, it is no longer suitable as a day-to-day payment tool or stable store of value.

This limitation has driven the rise of stablecoins. Stablecoins aim to maintain a fixed value, usually pegged to the U.S. Dollar, providing transactional stability and efficiency that Bitcoin cannot achieve.

The development of the crypto ecosystem reflects a pragmatic shift. Despite Bitcoin's initial ideal of replacing traditional currency, the need for stability has led to the widespread adoption of stablecoins (often backed by traditional assets), becoming a cornerstone of the entire ecosystem.

These stablecoins act as a bridge between the real-world traditional financial markets and the crypto ecosystem, on one hand promoting the adoption and application of cryptocurrency, and on the other hand raising questions about people's decentralized crypto ideals. For example, stablecoins like Tether (USDT) and USD Coin (USDC) are issued by centralized institutions, with their reserve assets held in traditional banks, which is seen as a compromise between ideology and reality.

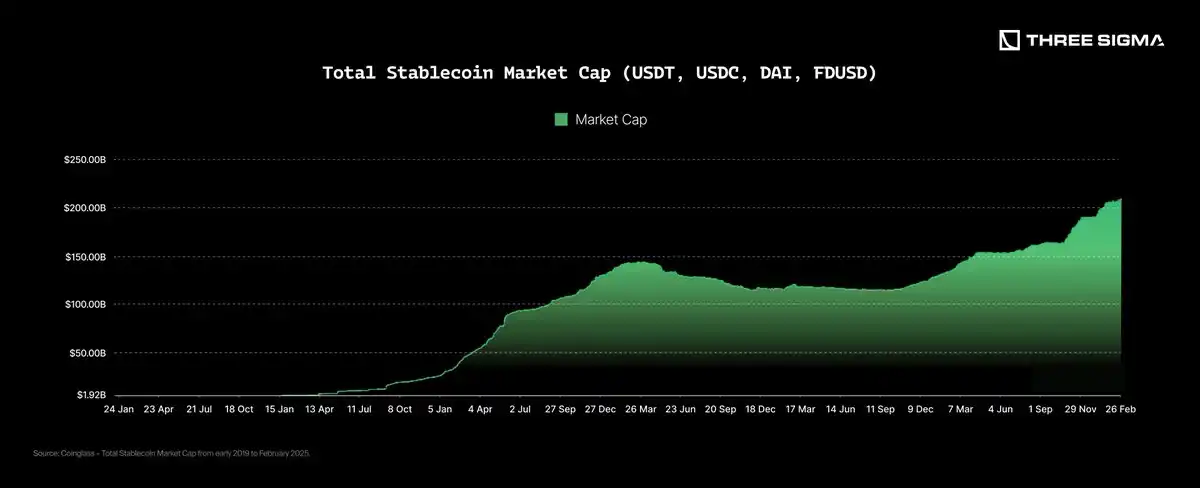

Over the years, the adoption of stablecoins has significantly increased. In 2017, their total market capitalization was less than $30 billion, but by March 2025, it had grown to around $2,280 billion. Stablecoins now represent about 8.57% of the entire crypto market and are an essential tool for trading, cross-border payments, and hedging during market turbulence.

This growth trend highlights the role of stablecoins as a key bridge connecting the traditional financial market and the crypto world. A chart from Coinglass clearly shows the steady and substantial growth in the total market capitalization of major stablecoins from early 2019 to date.

What Is a Stablecoin?

A stablecoin is a type of cryptocurrency designed to maintain its value by pegging it to some external asset, such as a fiat currency or commodity. For example, Tether (USDT) and USD Coin (USDC) are both stablecoins pegged to the U.S. dollar at a 1:1 ratio. The goal of stablecoins is to provide the advantages of digital currency, such as fast, borderless transactions on the blockchain, without the price volatility risk associated with Bitcoin.

Stablecoins strive to maintain price stability through holding reserve assets or employing other mechanisms, making them more suitable as a daily transaction tool or a store of value in the crypto market. In fact, most mainstream stablecoins achieve price stability through a collateralization mechanism, where each issued stablecoin is backed by an equivalent amount of reserve assets.

To ensure the stability and credibility of stablecoins, clear regulations are necessary. Currently, the U.S. lacks comprehensive federal legislation, relying mainly on state-level rules and some proposed bills under review; the EU has implemented strict reserve and audit requirements through the MiCA framework; Asia shows diverse regulatory strategies: Singapore and Hong Kong enforce strict reserve requirements, Japan allows banks to issue stablecoins, and China has mostly banned stablecoin-related activities. These differences reflect the balancing act between "innovation" and "stability" in different regions.

Despite the lack of a globally unified regulatory framework, the use and adoption of stablecoins continue to grow steadily year by year.

Why Were They Issued?

As mentioned earlier, the initial purpose of stablecoins was to provide users with a reliable digital asset for payments or as a value store linked to major global currencies (especially the U.S. dollar). However, their issuance was not for altruistic reasons but rather a highly profitable business opportunity, with Tether being the first company to identify and exploit this opportunity.

Tether launched USDT in 2014, becoming the first stablecoin and pioneering an extremely profitable business model, especially from a "per capita profit" perspective, making it one of the most successful projects in history. Its business logic is very simple: Tether mints 1 USDT for every $1 received and destroys the corresponding amount of USDT when users redeem dollars. The received dollars are then invested in secure short-term financial instruments (such as U.S. Treasury bonds), and the resulting returns belong to Tether.

Understanding how stablecoins make money is key to grasping the economic logic behind them.

Although the business model of stablecoins seems very simple, Tether cannot control its main source of income—the interest rates set by central banks worldwide (especially the Federal Reserve). When interest rates are high, Tether can earn significant profits, but when rates are low, profitability can decrease significantly.

Currently, a high-interest-rate environment is very favorable for Tether. But what if rates fall again in the future, even approaching zero? Will algorithmic stablecoins also be affected by interest rate fluctuations? Which type of stablecoin may perform better in such an economic environment? This article will further explore these questions and analyze how the stablecoin business model can adapt to the constantly changing macroeconomic environment.

2. Types of Stablecoins

Before analyzing the performance of stablecoins under different economic conditions, it is crucial to understand the operational mechanisms of different stablecoin types. Although all stablecoins share the common goal of maintaining a stable value pegged to real-world assets, each stablecoin responds differently to changes in interest rates and the overall market environment. Below, we will introduce several main types of stablecoins, their mechanisms, and their responses to different economic changes.

Fiat-backed Stablecoins

Fiat-backed stablecoins are the most well-known and widely used stablecoin type, essentially tokenizing the dollar in a centralized manner.

Their operational mechanism is very simple: whenever a user deposits $1, the issuer mints 1 corresponding stablecoin; when a user redeems dollars, the issuer destroys the equivalent tokens and returns the same amount of dollars.

The profit model of fiat-backed stablecoins is mainly hidden behind the scenes. The issuer invests users' deposits in various short-term and secure financial instruments, such as government bonds, collateralized loans, cash equivalents, and sometimes allocates to higher volatility assets such as cryptocurrency (e.g., Bitcoin) or precious metals. The returns generated from these investments constitute the issuer's primary source of income.

However, high returns come with significant risks. One ongoing major challenge is compliance issues. Governments in many countries have rigorously scrutinized fiat-backed stablecoins, arguing that they are essentially equivalent to issuing a "digital currency" and thus must comply with strict financial regulatory requirements.

While most stablecoin issuers have successfully addressed regulatory pressures without major business interruptions, significant challenges still arise. A notable example is the European MiCA (Markets in Crypto-Assets) regulation, which recently banned USDT (Tether) from circulating in certain markets due to non-compliance with its stringent regulatory requirements.

Another key risk is "depegging risk." Stablecoin issuers typically invest a large portion of reserve assets in various investment instruments. If a large number of users simultaneously request token redemptions, the issuer may have to quickly sell off these assets, potentially resulting in significant losses. This scenario could trigger a chain reaction similar to a "bank run," making it difficult for the issuer to maintain the token's peg to the dollar, or even lead to bankruptcy.

The most prominent case occurred in March 2023, involving USDC (issued by Circle). At that time, Silicon Valley Bank (SVB) collapsed, and market rumors quickly spread that Circle had a significant reserve held in SVB, raising concerns about Circle's liquidity and whether USDC could maintain its peg. These concerns caused USDC to briefly depeg. This event highlighted the risks when stablecoin reserves are held in centralized banks. Fortunately, Circle resolved the issue within a few days, restored market confidence, and re-stabilized USDC's peg.

Currently, the two most significant fiat-backed stablecoins in the market are USDT (Tether) and USDC (Circle).

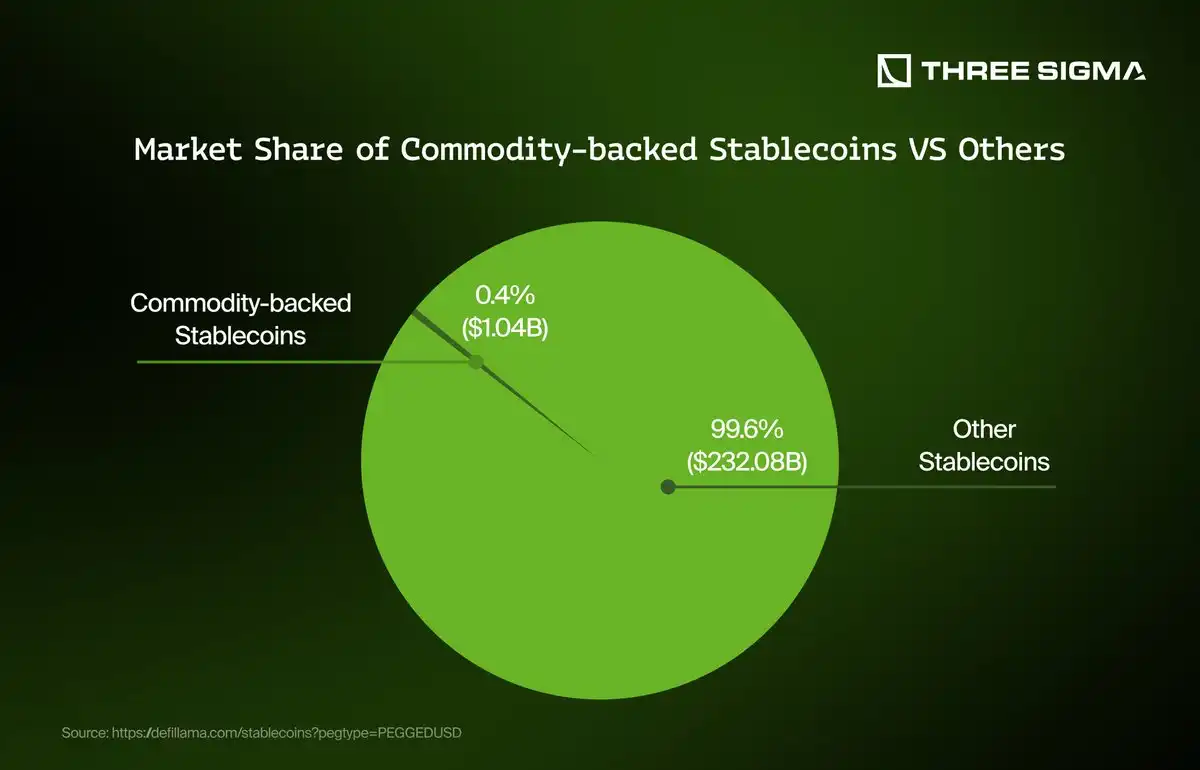

Commodity-backed stablecoins are an innovative category within the stablecoin ecosystem. They issue corresponding digital tokens by collateralizing tangible real-world assets (usually precious metals like gold and silver, or commodities such as oil and real estate).

The operation mechanism of this type of stablecoin is similar to fiat-collateralized stablecoins: for every unit of real-world asset deposited, the issuer mints an equivalent token. Users can usually redeem these tokens for the underlying asset itself or equivalent cash, at which point the corresponding tokens are burned.

The issuer's revenue primarily comes from token minting (creation) and redemption (destruction) fees. For example, Pax Gold (PAXG) charges a small fee when handling token creation and redemption, although Paxos currently does not charge storage fees for the gold it holds. In addition, the issuer may also profit by providing services for transactions and exchanges between the token and the US dollar or real-world assets.

Similarly, Tether Gold (XAUT) generates revenue from fees related to redemption and delivery. Users redeeming XAUT tokens for physical gold bars or converting gold to cash through Tether are charged relevant fees. For instance, during the redemption process, a fee of 25 basis points (0.25%) is charged based on the gold price, and if opting for physical delivery, shipping costs are also incurred. If users choose to sell the redeemed gold bars in the Swiss market, an additional 25 basis points fee is applied.

However, this type of stablecoin also faces risks, especially the volatility of commodity prices, which can affect the token's stable peg. Moreover, compliance issues are a significant challenge. Commodity-backed stablecoins are typically subject to strict regulatory requirements and must have transparent and secure custody arrangements.

Currently, successful commodity-backed stablecoins in the market include Paxos's Pax Gold (PAXG) and Tether's Tether Gold (XAUT), both backed by gold reserves, providing investors with convenient digital exposure to commodities.

In summary, commodity-backed stablecoins bridge traditional commodity investments with digital finance, offering investors stability and exposure to physical assets, while also emphasizing regulatory compliance and transparency.

Crypto asset-backed stablecoins are an important category within the stablecoin ecosystem, maintaining a stable value pegged to fiat currency (usually the US dollar) through cryptocurrency collateral. Unlike fiat or commodity-backed stablecoins, these tokens rely on smart contract technology, establishing a transparent and automated system.

The basic mechanism is as follows: users lock up crypto assets (often overcollateralized) in a smart contract to mint stablecoins. The overcollateralization design can buffer the price fluctuation of the crypto assets, ensuring that the stablecoin maintains its set pegged value. When users redeem the stablecoin, they return the equivalent stablecoins, and after the system burns the tokens, the initially collateralized crypto assets are released.

The profit model of an algorithmic stablecoin mainly includes:

Charging interest to stablecoin borrowers;

Charging liquidation fees to users whose collateral falls below the liquidation line;

Protocol-defined governance rewards to incentivize holders and liquidity providers.

Represented by DAI (now called USDs), issued by MakerDAO (now rebranded as SKY), it is primarily collateralized by crypto assets within the Ethereum ecosystem. MakerDAO's revenue sources include charging a stability fee (interest) to USDs borrowers and collecting penalties when liquidation is triggered. These fees together support the stable operation and sustainable development of the protocol.

Another example is the HONEY stablecoin issued by Berachain, currently mainly collateralized by USDC and pYUSD. HONEY's revenue sources include redemption fees: when users redeem HONEY and retrieve their collateral assets (USDC or pYUSD), Berachain charges a 0.05% fee.

Although these stablecoins are classified as "crypto asset-backed," in practice, most of them are more like wrapped versions of fiat-backed stablecoins, such as USDC. While the initial goal was to rely entirely on native crypto assets as collateral to maintain stability, achieving true stability without relying on fiat stablecoins remains very challenging in practice.

Of course, these assets also come with inherent risks. For example, price volatility of the underlying crypto assets can pose significant challenges — such as triggering large-scale liquidations during sharp downturns, potentially breaking the stablecoin's peg mechanism. In addition, smart contract vulnerabilities or protocol attacks can also pose a severe threat to the overall system's stability.

In summary, crypto asset-backed stablecoins like USDs and HONEY have played a significant role in providing decentralized, transparent, and innovative financial solutions. However, despite being nominally crypto-collateralized, they often heavily rely on fiat stablecoins in practice, requiring more robust risk management mechanisms to maintain their resilience and credibility.

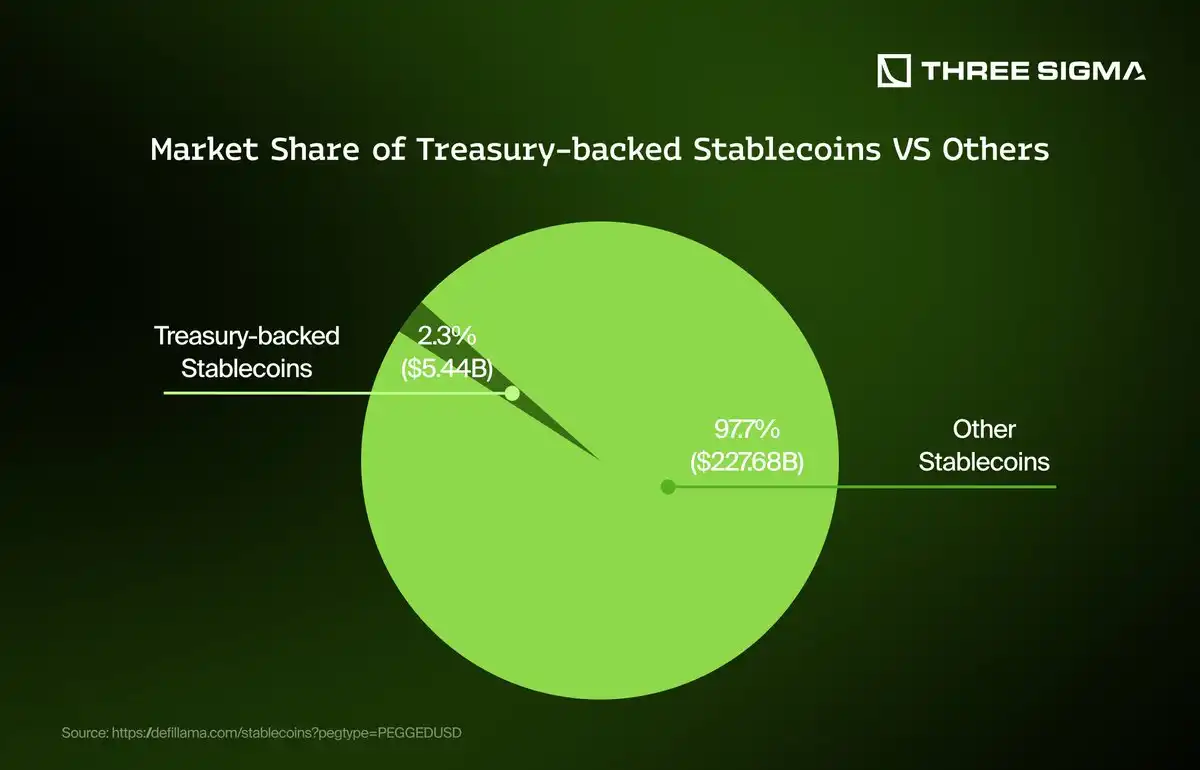

A sovereign-bond-backed stablecoin is a type of stablecoin supported by government bonds (especially U.S. Treasury bonds) as collateral. These stablecoins are usually pegged to the dollar and, while providing value stability, can also offer passive income to holders through the interest income from the underlying government bonds. Therefore, they are more like an interest-bearing investment token, combining the stability of traditional stablecoins with investment characteristics.

For example, Ondo's USDY (USD Yield Token) is referred to as a tokenized note backed by short-term US treasuries and bank demand deposits. Its goal is to provide non-US individual and institutional investors with stablecoin-like utility while offering high-quality USD-denominated yield. After investors purchase USDY, the funds are used to buy US treasuries and partially deposited in banks, with the generated interest being proportionally distributed to token holders. USDY is a "bearing asset," meaning it passively appreciates with the interest generated from the underlying assets, resulting in the token's value increasing over time.

Another example is Hashnote's USYC (USD Yield Coin), which represents Hashnote's Short Duration Yield Fund (SDYF) on-chain. It invests in short-term US treasuries and participates in the repo and reverse repo markets. The return level of USYC is tied to the short-term "risk-free rate," combining the speed, transparency, and composability advantages of blockchain while minimizing protocol, custodial, regulatory, and counterparty credit risks. Users can swap USYC for USDC or PYUSD on the same day (T+0) or the next day (T+1), enabling on-chain direct minting in an atomic and instantaneous process. Like USDY, USYC is also a "bearing asset," accumulating returns passively through the interest generated from the underlying assets.

Despite the dual benefits of stability and yield offered by such stablecoins, they also come with some risks:

· Regulatory Risk: Since these assets are typically targeted at non-US users to circumvent US domestic regulatory requirements, future policy changes may bring uncertainty;

· Custodial Risk: They rely on the issuer to manage and hold the underlying assets properly;

· Liquidity Risk: During market volatility, users' redemption requests may be constrained;

· Counterparty Risk: Especially in repo agreements, default by the counterparty can lead to losses;

· Macroeconomic Risk: Such as interest rate fluctuations, which may affect the overall yield level.

This type of token is often classified into a rapidly growing new category called "Treasury-backed crypto assets."

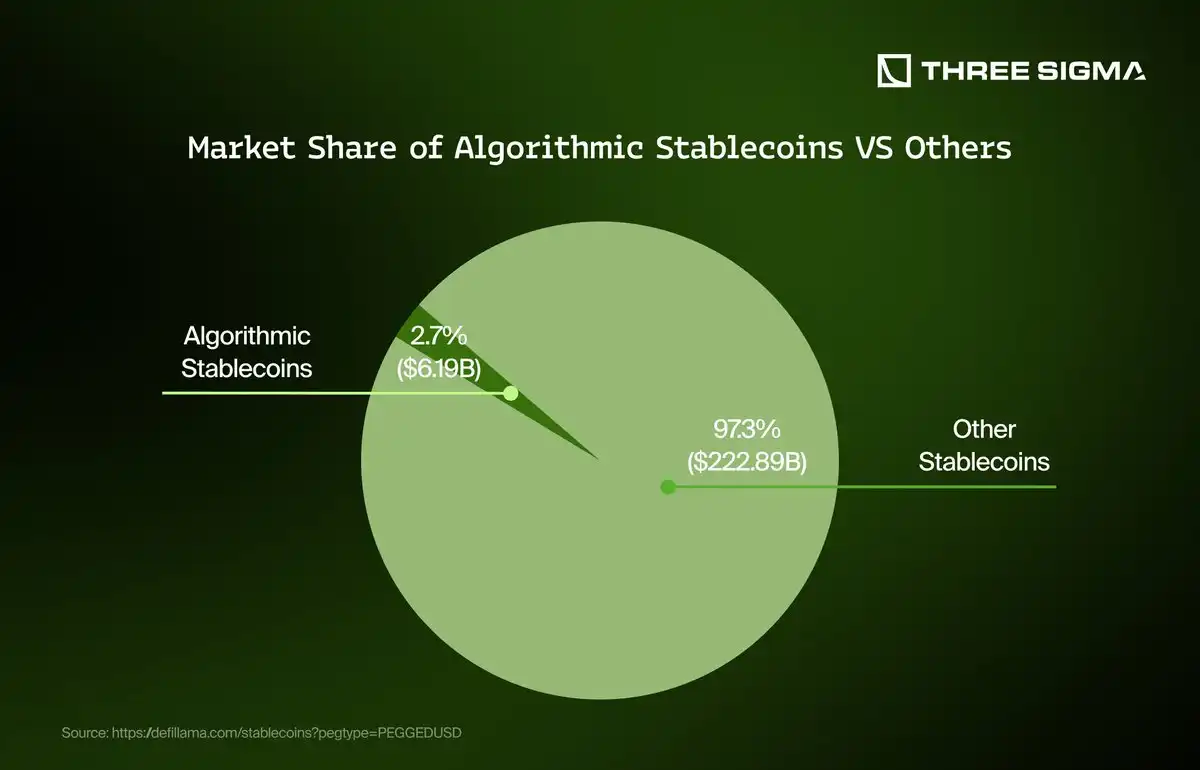

Algorithmic stablecoins are a type of stablecoin that relies on economic mechanisms and market incentives rather than being entirely backed by fiat currency or traditional assets such as treasuries to maintain a stable value. These models typically maintain a pegged exchange rate (such as to the dollar) through a supply-demand adjustment mechanism but often face challenges in extreme market conditions. The fundamental issue lies in the high reliance on sustained market confidence and an effective incentive structure, which can easily fail under severe pressure.

The USDe issued by Ethena is a new type of "quasi-algorithmic" stablecoin, utilizing a hybrid model. It maintains stability through a "Delta Neutral Hedge Mechanism," holding BTC and ETH among other crypto assets as collateral, while simultaneously establishing an equivalent amount of short positions in the derivatives market to hedge against price fluctuations of the underlying assets, thereby maintaining a stable peg to the US dollar. The USDe achieves a 1:1 full collateralization, making it more capital efficient compared to an overcollateralized model. Furthermore, Ethena also includes highly liquid stablecoins such as USDC and USDT in reserves to enhance liquidity and hedging strategies.

Despite various innovations, algorithmic stablecoins still face significant risks: market instability, extreme volatility, or liquidity crises could disrupt their peg maintenance mechanism. Moreover, reliance on derivatives brings counterparty and execution risks, making the system vulnerable to external shocks.

Although new models like USDe attempt to mitigate these issues through structured hedging and diversified reserves, their long-term stability still depends on overall liquidity conditions and the ability to operate effectively in adverse market environments.

3. Current Mainstream Stablecoins

When it comes to stablecoins, USDT and USDC are undoubtedly the dominant forces in the market, serving as centralized liquidity pillars and holding a core position in the crypto market. They have similar structures: both issued by centralized entities, fully backed by fiat reserves, and widely integrated across major exchanges and financial platforms.

USDT, issued by Tether, has the largest market share and is known for its deep liquidity and widespread adoption, especially prevalent in high-frequency trading environments. On the other hand, USDC, issued by Circle, is positioned as a more compliant and transparent option, favored by institutions and companies seeking a regulatory-friendly environment. Despite slight differences in details, their core function is consistent: providing a stable, trustworthy digital dollar that underpins the entire crypto ecosystem.

Contrastingly, there are also USDS, DAI, and USDe, representing the decentralized forces counterpart to fiat-backed stablecoins, albeit varying degrees of decentralization. DAI and USDS essentially stem from the same system—MakerDAO (now rebranded as Sky). Among them, USDS is an evolution of DAI and a key part of Sky's long-term roadmap.

DAI has historically been more decentralized, relying on overcollateralization of crypto assets to maintain its pegged exchange rate; whereas USDS reflects Maker's trend towards a more structured, strategic direction, prioritizing efficiency over pure decentralization.

At the same time, USDe is also a significant decentralized stablecoin competitor but has taken a completely different path. In contrast to Maker's model of overcollateralization and governance mechanisms, USDe has introduced a yield-generating structure, using its collateral assets to provide additional returns to holders.

USDT

When discussing stablecoins, USDT naturally emerges as a dominant force, playing a crucial role as the centralized liquidity backbone in the crypto market. USDT issued by Tether holds the largest market share and is known for its deep liquidity and wide adoption, especially crucial in high-frequency trading environments. It provides a stable and trusted digital dollar, supporting the operation of the crypto ecosystem and serving as a key medium for trading pairs, arbitrage opportunities, and cross-exchange liquidity provision. Its widespread acceptance consolidates its role in both centralized and decentralized finance.

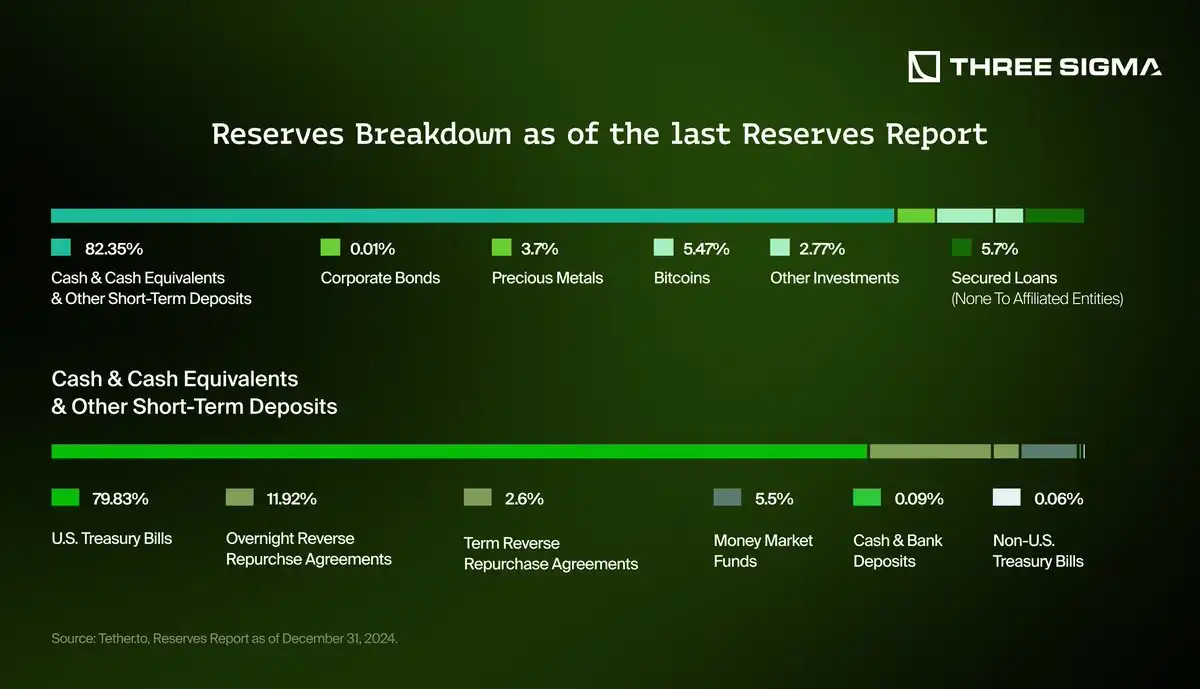

Tether's revenue mainly comes from its management of vast reserve assets that back each issued USDT token. These reserve assets primarily include cash equivalents such as U.S. Treasury bonds, commercial papers, short-term deposits, money market instruments, and corporate bonds. By strategically allocating these reserves, Tether is able to accumulate interest and investment returns, making a significant contribution to its revenue.

Additionally, Tether occasionally engages in short-term borrowing and other financial instruments' transactions, further diversifying and enhancing its sources of income. Through token issuance, redemption processes, and transaction fees on various blockchain platforms, Tether also generates additional revenue.

Here is its latest reserve report, clearly showing that over 80% of its reserves consist of cash, cash equivalents, and other short-term deposits, with around 80% being specifically invested in government bonds.

Essentially, Tether's revenue relies mainly on central bank-set interest rates, especially the rates of the Federal Reserve System in the U.S., as the appreciation of its most reserve assets is directly linked to these rates. Higher rates can significantly boost Tether's returns from its reserves, while lower rates can markedly reduce its income potential.

Importantly, unlike some other stablecoins, all of the revenue generated by Tether is retained by the issuer and not distributed to USDT token holders. This is in contrast to yield-bearing stablecoins, which distribute returns directly to holders, highlighting a key difference in stablecoin business models.

Historical Revenue Trends

Historically, Tether's revenue trajectory has closely followed global interest rate trends. During the low-interest-rate period from 2019 to early 2022, Tether's revenue growth was moderate, primarily due to its conservative investment strategy with limited returns.

However, starting from mid-2022, as major central banks actively raised interest rates to combat inflation, Tether's revenue saw significant growth. From June 2022 to early 2025, monthly revenue almost increased tenfold, highlighting the high sensitivity of Tether's revenue sources to macroeconomic changes and monetary policy decisions. This trend demonstrates the effectiveness of Tether's revenue model in a rising interest rate environment.

Nevertheless, revenue is not entirely dependent on interest rates. Even in a decreasing rate environment, as long as the supply of USDT increases significantly, Tether may still achieve revenue growth. A larger supply means more assets under management, which can offset lower yields and maintain or even increase overall revenue.

USDC

USDC, issued by Circle, is one of the most trusted centralized stablecoins in the market. Known for its compliance and transparency, it is widely used in decentralized finance, institutional payments, and cross-chain applications. Its presence on multiple blockchains enhances its composability and ecosystem coverage.

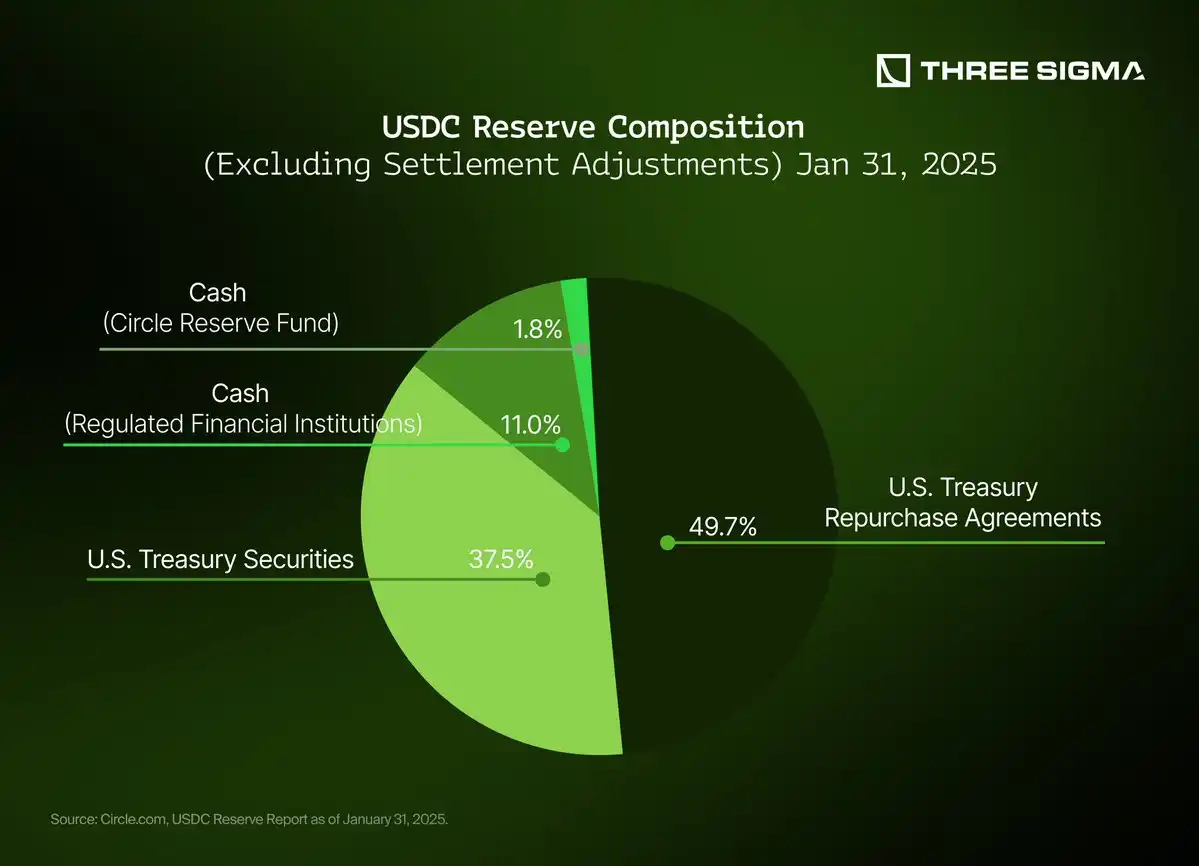

A key feature of USDC is Circle's strict reserve structure and public disclosures. As of January 31, 2025, USDC's circulation exceeds $53.2 billion and is fully backed by $53.28 billion in reserves, verified by an independent accounting firm. These reserve funds are divided into the following parts:

Circle Reserve Fund: a government money market fund holding $47.26 billion in U.S. Treasuries and repurchase agreements.

Segregated Bank Accounts: holding an additional $6.02 billion, deposited in regulated financial institutions.

Circle generates revenue by managing these reserve assets, primarily relying on interest income from U.S. Treasuries and overnight lending arrangements. Although structurally similar to Tether's model, Circle stands out with its fund structure, representing 100% reserve fund equity for USDC holders. This not only provides clearer regulatory separation but also may allow for more flexible future product integrations.

Unlike decentralized alternatives, USDC does not directly distribute earnings to users. Instead, the income belongs to the issuer, prioritizing simplicity, compliance, and capital preservation.

Historical Revenue Trends

Circle's revenue trajectory is closely tied to the overall interest rate environment, as its conservative investment strategy focuses mainly on short-term government debt.

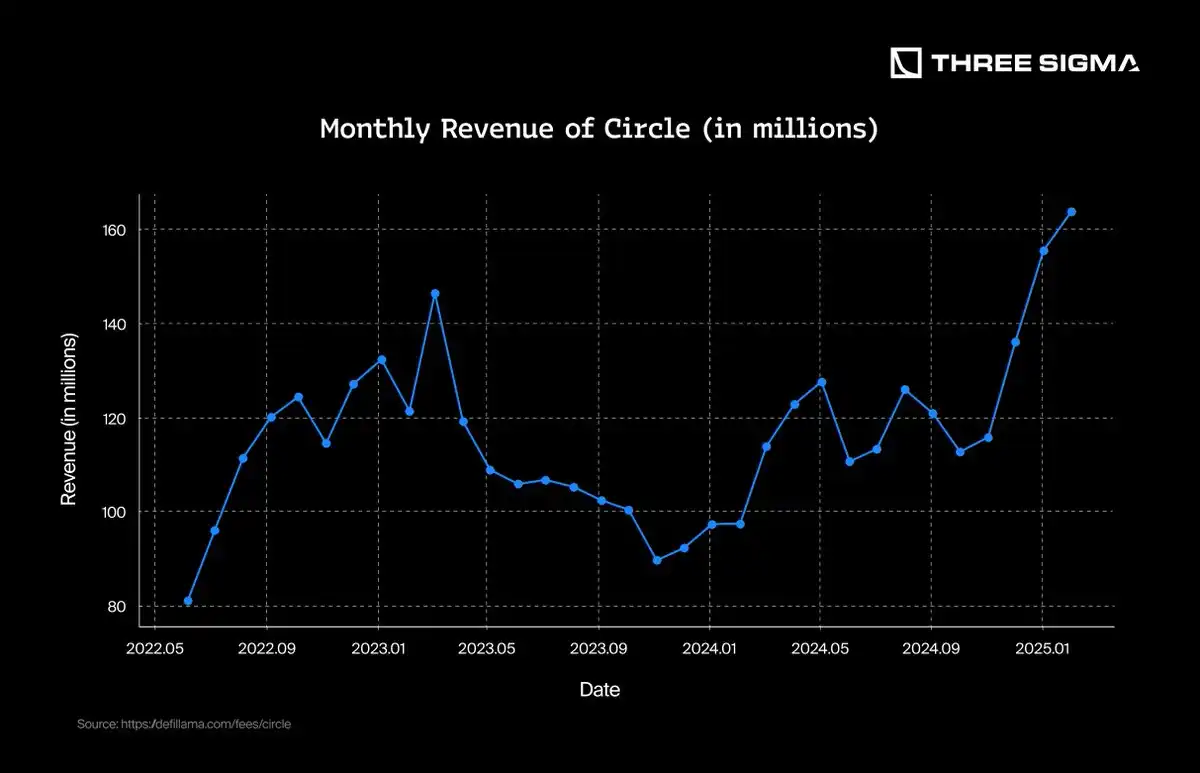

In 2022, due to the Federal Reserve raising rates, Circle's revenue steadily grew, peaking at $1.465 billion in March 2023. However, later that year, pressure from competing stablecoins, blockchain reliability issues (especially on Solana), and reputation fluctuations with banking partners led to a gradual revenue decline. By the end of 2023, monthly revenue had dropped to below $90 million.

In 2024, as redemption volumes decreased, cryptocurrency activity rebounded, and the continued high-rate environment, Circle's revenue started to recover, reaching $1.26 billion in August and ending the year on a strong note. In February 2025, Circle set a new record for monthly revenue, hitting $1.637 billion.

This trend highlights the resilience of USDC and the close relationship between stablecoin revenue models and monetary policy. Circle's sustained recovery underscores its ability to maintain user trust and liquidity dominance throughout market cycles.

USDS/DAI (SKY)

USDS is the current evolution of DAI, which was the first major decentralized stablecoin issued by MakerDAO, aiming to provide an anti-censorship alternative for fiat-backed assets. While both are part of the Maker ecosystem, they have structural differences in collateral models and target use cases.

DAI is an overcollateralized stablecoin backed by a mix of cryptocurrency, RWAs, and stablecoin collateral. Users mint DAI by depositing collateral such as ETH, stETH, or USDC into Maker Vaults, ensuring it remains fully collateralized at all times. This design gives DAI strong anti-risk capabilities but also limits its scalability.

On the other hand, USDS represents the evolution of MakerDAO towards a more traditionally finance-compatible stablecoin. While USDS remains overcollateralized, it follows a structured reserve approach, including tokenized short-term US Treasury bonds. This aligns it with institutional demand, positioning it as a competitor to stablecoins like USDT and USDC while maintaining MakerDAO's decentralized governance model.

The transition from DAI to USDS reflects a shift towards broader institutional adoption. While DAI initially started as a crypto-native stablecoin primarily backed by decentralized assets, USDS optimized its collateral structure by introducing more RWAs, especially US Treasury bonds.

Furthermore, USDS enhances stability through a direct convertibility mechanism, making it easier to maintain its peg to the US dollar. Unlike DAI, which relied on external DeFi incentives early on, USDS was designed from the start to provide built-in yield through the DSR, making it more attractive in both DeFi and TradFi environments. This structure aligns with the increasingly popular RWA yield DeFi strategies projected for 2025.

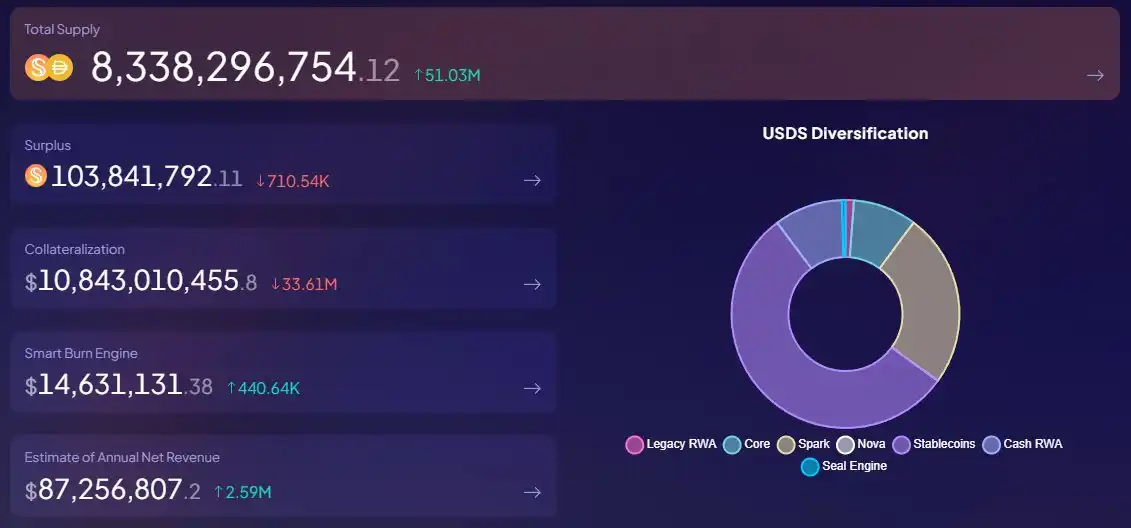

Transparency is fundamental to the Sky ecosystem's design, serving not only as a tool to maintain the anchoring mechanism but also as a prerequisite for building trust, attracting institutional participation, and responsibly allocating capital. In an environment managing billions of dollars in assets, both users and institutions require clear visibility into where these funds are held, how they are used, and the system's endorsement.

Hence, Sky provides a public real-time dashboard that clearly displays USDS's endorsement, distribution, and yield. However, transparency alone is insufficient to stabilize a currency; anchoring is maintained through overcollateralization, risk-managed asset allocation, and protocol-level mechanisms.

USDS always maintains more collateral than its supply. As of now, USDS's total collateral base exceeds $10.8 billion, with a supply of around $8.3 billion, ensuring an ample buffer to withstand market fluctuations or redemptions. Its collateral is sourced from several key outlets:

·Stablecoin (54.8%): Mainly supported through the LitePSM module, which is an anchoring stability module that allows for a 1:1 exchange between DAI and USDC to support the anchoring of USDS.

·Spark (24.7%): Sky's lending and liquidity protocol, using high-quality, yield-generating collateral to mint USDS.

·Cash RWA (9.7%): Fully held in BlockTower Andromeda, which is a short-term US Treasury bond investment strategy, providing low-risk real-world yield.

·Core (9%): Sky's overcollateralized Vault system, where users can mint USDS using assets like ETH and stETH under strict collateral thresholds.

These mechanisms together ensure that USDS remains stable, overcollateralized, and backed by a range of liquid and yield-generating assets, with transparency ensuring anyone can verify this at any time.

Historical Revenue Trend

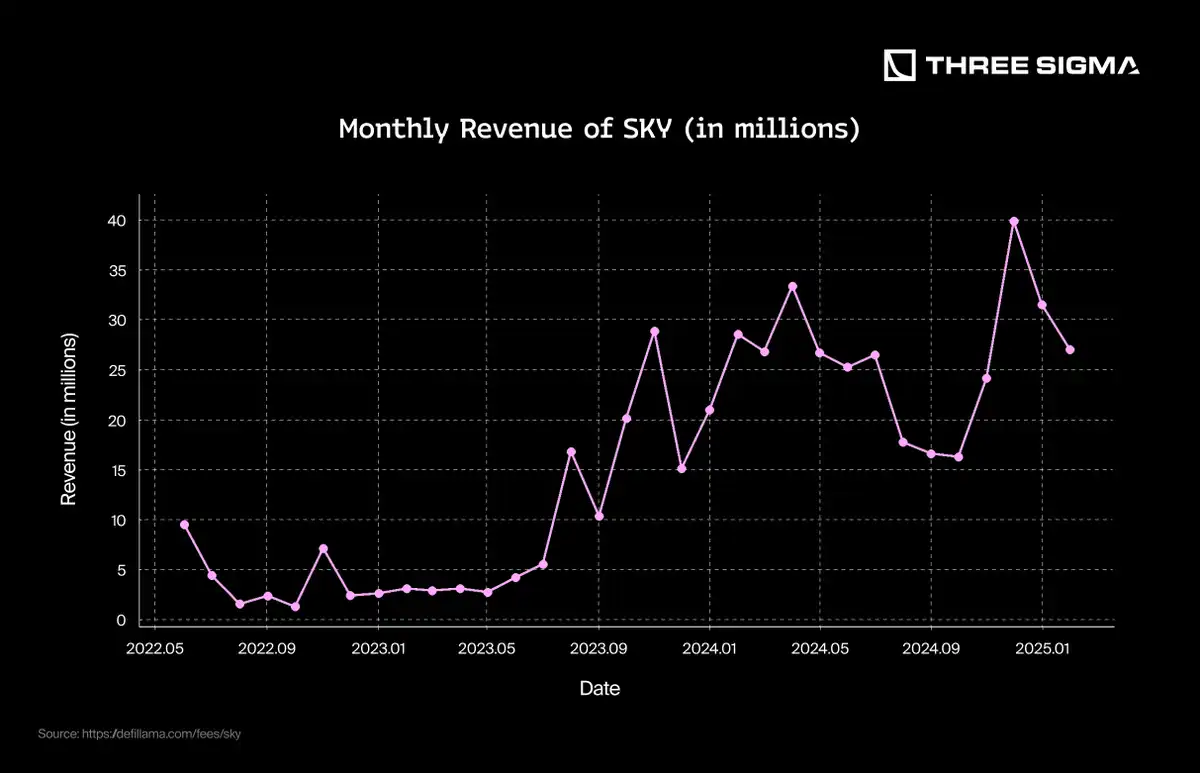

The above chart shows the Sky protocol's cumulative revenue from mid-2022 to early 2025. While revenue steadily grew in the initial months, by the end of 2023, with the expansion of DeFi integrations, increased adoption of USDS, and deeper engagement with real-world assets (such as short-term US Treasury bonds), revenue growth significantly accelerated, coinciding with rising interest rates. By early 2025, cumulative revenue had exceeded $500 million, reflecting Sky's ability to capture yield in both crypto-native and institutional strategies while sustainably scaling.

USDe

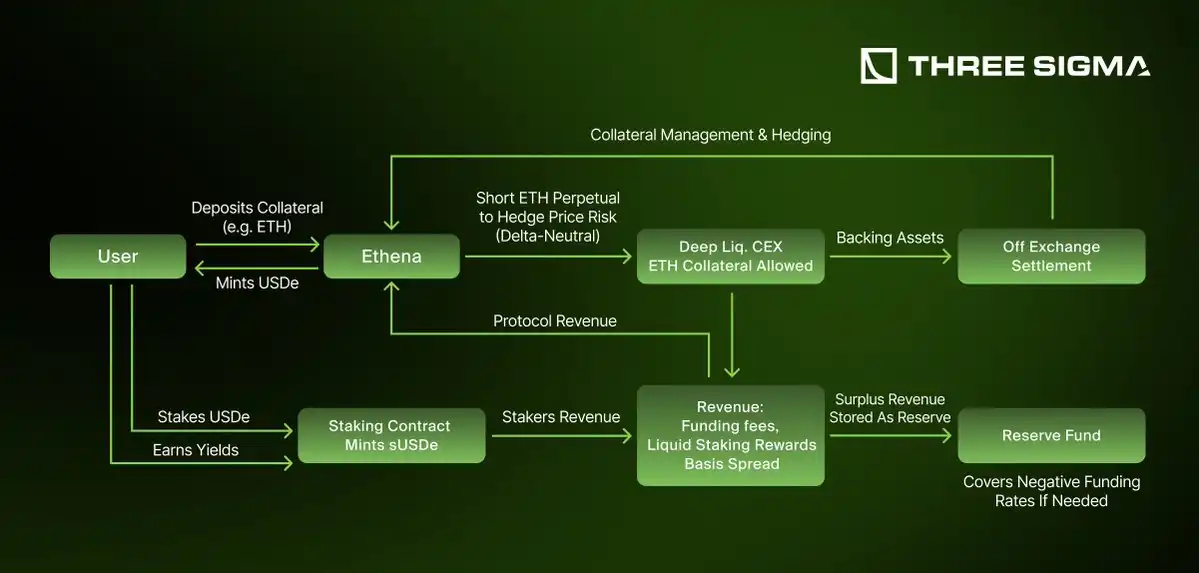

USDe is a delta-neutral synthetic dollar stablecoin adopting a synthetic dollar structure maintained through perpetual futures, developed by Ethena Labs. Unlike traditional stablecoins backed by fiat reserves or overcollateralized crypto assets, USDe maintains its peg to the dollar through automated hedging strategies. This gives it fully backed, scalable, and censorship-resistant characteristics. Ethena also offers sUSDe, a yield-bearing version of USDe capable of earning rewards through liquid staking assets and futures market funding rate arbitrage.

Since its public launch in early 2024, Ethena has rapidly expanded, reaching a $60 billion supply within ten months, making USDe the third-largest USD-denominated asset in the crypto space. It has also become a fundamental part of DeFi, integrated into major protocols like Pendle, Morpho, and Aave, with its adoption driving significant growth. Beyond DeFi, USDe has penetrated CeFi, currently integrated as collateral on about 60% of centralized exchanges, surpassing USDC balances on Bybit in less than a month.

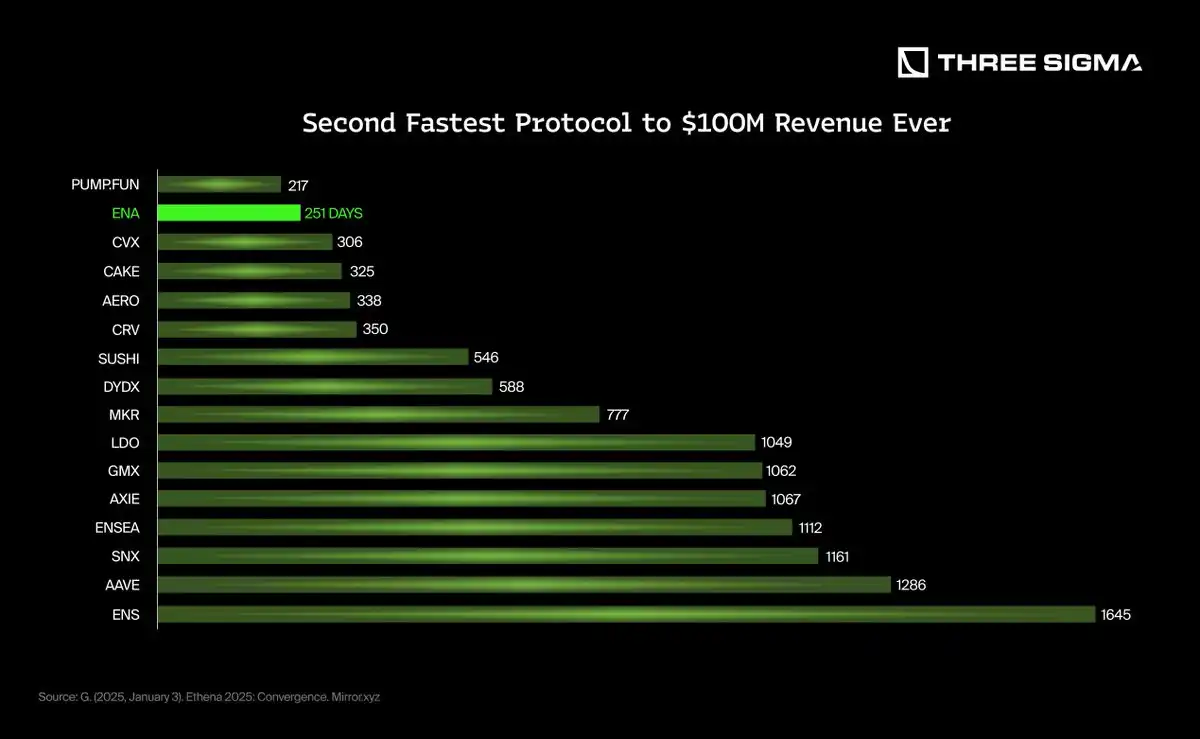

If we delve into revenue, Ethena has also excelled, becoming the second-fastest dApp in history to reach $100 million in revenue (second only to Pump.fun), achieving this milestone in 251 days. In 2024, Ethena has emerged as a dominant force in DeFi, with its assets representing over 50% of Pendle TVL, around 30% of Morpho TVL linked to Ethena-related assets, and becoming the fastest-growing new asset on Aave, reaching $1.2 billion in deposits in just three weeks.

The next phase for Ethena is defined by Convergence, aiming to achieve the convergence of DeFi, CeFi, and TradFi through USDe. By introducing iUSDe, a wrapped version of sUSDe designed for institutional adoption, Ethena plans to offer a high-yield, crypto-native dollar product tailored for asset managers, private credit funds, and exchange-traded products. By facilitating capital flow and interest rates across various financial systems, Ethena positions USDe as a cornerstone of the evolving digital dollar space.

How Does USDe Work?

USDe maintains stability through a delta-neutral hedging strategy, ensuring its value is unaffected by market fluctuations. When users mint USDe, the collateral received by Ethena can include ETH, BTC, LSTs, USDT, USDC, and SOL, among others. To hedge price risk, Ethena opens a perpetual futures short position for each received collateral. For instance: if the collateral is ETH, Ethena will short an ETH perpetual future.

This mechanism ensures that any price fluctuations in the collateral are hedged by the corresponding futures position. If the collateral appreciates, the short position incurs a loss, which is offset by the collateral's appreciation. Conversely, if the collateral's price drops, the short position gains, mitigating the depreciation of the collateral. This mechanism ensures that USDe remains stable, immune to market volatility.

Unlike other synthetic stablecoins, Ethena does not utilize additional leverage, only using the leverage naturally applied by derivative exchanges to evaluate collateral. This minimizes liquidation risk, ensuring that each short position is fully backed by assets on a 1:1 basis.

For enhanced security, Ethena's collateral assets are held on-chain and custody through an off-chain settlement system to mitigate counterparty risk. Ethena never fully relinquishes control of the assets to the derivative platform but uses them solely as collateral for its short hedge positions, ensuring decentralized and transparent asset management.

Ethena generates revenue by capturing a portion of the returns from its delta-neutral strategy, including:

Funding Rate Arbitrage: Ethena profits when the funding rate of perpetual futures is positive.

Liquid Staking Rewards: Staking rewards generated by the collateralized LSTs, of which a portion is retained by Ethena.

Basis Trading Profits: Ethena benefits from the efficiency difference between the spot and futures markets.

Protocol Fees: A portion of the overall returns is allocated to the reserve fund and protocol treasury to ensure long-term sustainability.

While USDe's delta-neutral strategy minimizes exposure to price fluctuations, it is still susceptible to funding rate fluctuations, market imbalances, and counterparty risks. If the funding rate remains negative for an extended period, Ethena's reserve fund will absorb the loss, but prolonged negative rates could put pressure on the system.

A liquidity crisis or extreme volatility could lead to temporary deviations from the peg if there is a disconnect between the spot and futures markets. Additionally, relying on centralized exchanges for hedging introduces counterparty risk, but Ethena mitigates this risk by keeping assets on-chain and settling off-chain.

Historical Revenue Trends

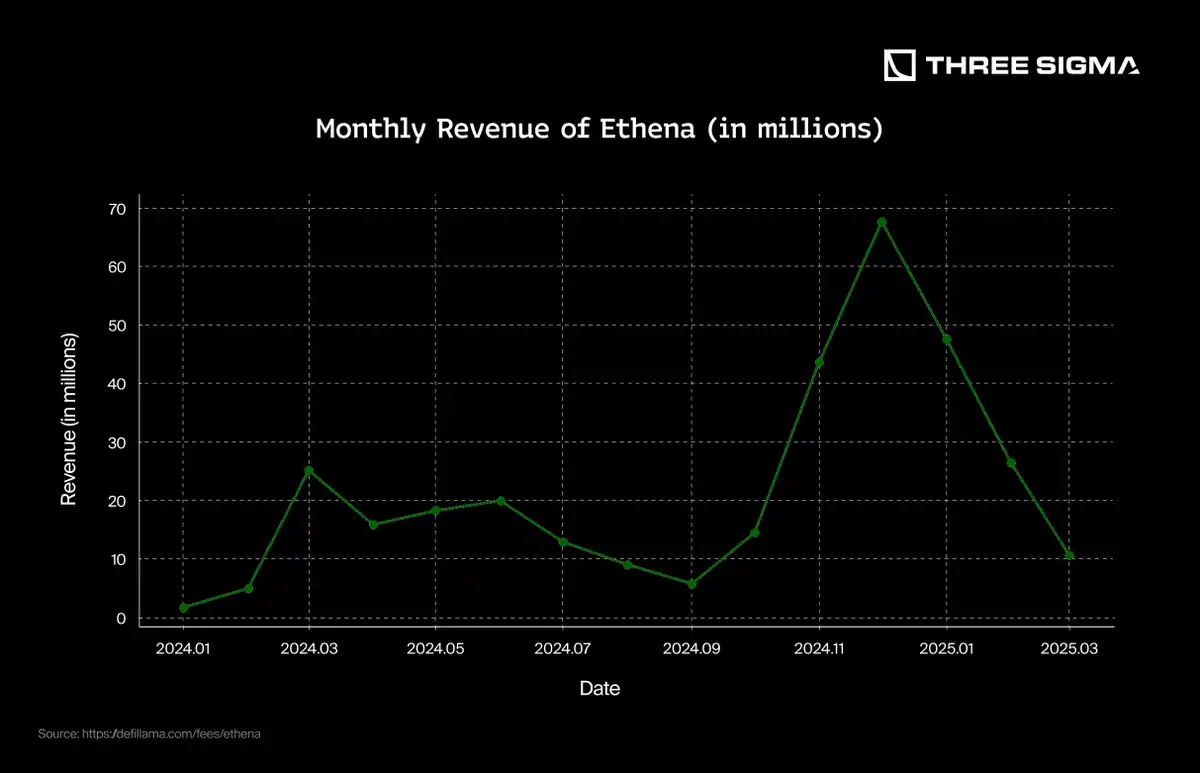

Ethena launched to the public on February 19, 2024, allowing users to mint USDe by depositing stablecoins and staking them as sUSDe to earn rewards. In less than a year, the protocol's cumulative revenue exceeded $320 million, making it one of the fastest-profit curves in DeFi history.

The steady growth in revenue in the first half of 2024 reflects the continuous increase in USDe supply and widespread adoption on DeFi and CeFi platforms. However, the sharp acceleration in revenue began in October 2024, coinciding with the following events:

USDe and sUSDe have been integrated into major lending markets such as Aave and Morpho.

The increase in market volatility has brought about a surge in fund rate arbitrage opportunities.

The launch of new institutional products such as iUSDe has expanded Ethena's influence into the TradFi space.

By the first quarter of 2025, the protocol's total revenue has surpassed $300 million. Despite being launched for less than 15 months, Ethena has already positioned itself at the forefront of revenue generation in the crypto space. This rapid growth demonstrates strong market demand and validates the sustainability of USDe's delta-neutral model.

However, after reaching a peak at the end of 2024, the monthly revenue in the first quarter of 2025 experienced a sharp decline. This decline is associated with a reduction in fund rate arbitrage opportunities as the perpetual futures funding rates on major exchanges trended towards normalization. With reduced volatility and a more neutral funding environment, one of Ethena's key revenue sources temporarily weakened, highlighting the model's sensitivity to market conditions.

4. Interest Rates and Revenue Correlation

Interest rates have a significant impact on stablecoins and are one of the most decisive factors in their revenue performance. As mentioned earlier, stablecoins generate revenue through various mechanisms, including interest-bearing reserves, market arbitrage, and other income-generating strategies. Since the assets held by many stablecoins are affected by changes in interest rates, their revenue potential is often influenced by macroeconomic conditions.

To better understand this relationship, we adjust the revenue by dividing it by the supply. This normalization process makes comparisons more accurate because an increase in stablecoin supply naturally leads to greater potential revenue generation. By focusing on revenue per unit of supply, we can isolate the direct impact of interest rate fluctuations on the profitability of stablecoins.

USDT

In-depth chart analysis vividly illustrates the positive correlation between Tether revenue and interest rate fluctuations. Historical charts compare Tether's quarterly revenue with interest rate changes, showing a clear synchronicity and highlighting the almost real-time response of revenue to rate adjustments.

These visual representations effectively emphasize Tether's sensitivity to the interest rate environment, providing predictive insights into potential future performance scenarios. They underscore the importance of proactive financial and reserve management strategies to mitigate revenue risks associated with interest rate fluctuations or downturn cycles.

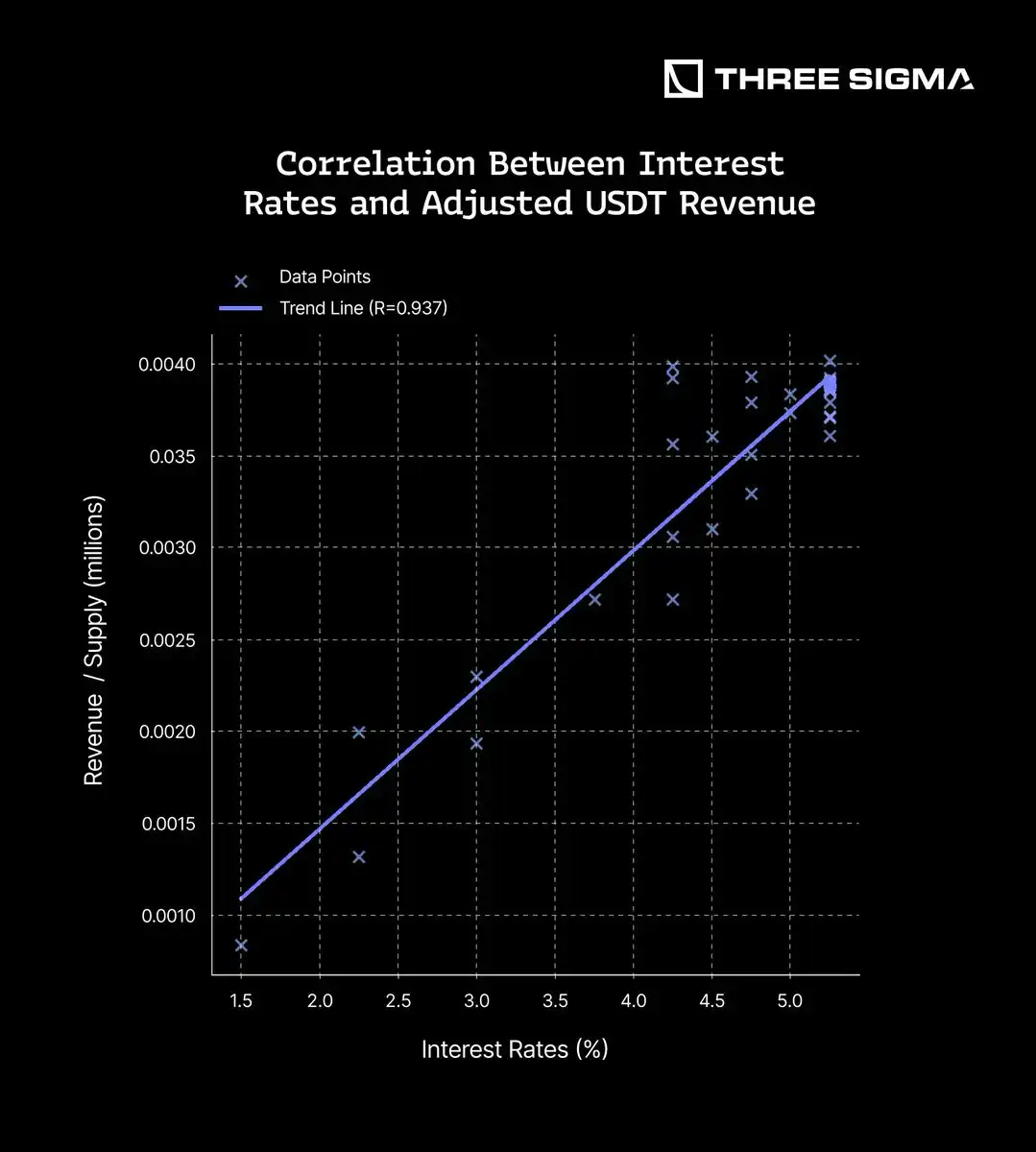

The following chart illustrates the correlation between interest rates and adjusted stablecoin income. Each chart shows the relationship variation between stablecoin supply per unit (y-axis) and interest rates (x-axis).

The chart further highlights a strong positive correlation (R = 0.937) between interest rates and USDT's adjusted per-unit supply income. This indicates that as interest rates rise, USDT's per-unit supply income also increases, reflecting the yield growth of USDT in U.S. Treasury investments. As interest rates increase, the yield of these Treasury securities rises, directly impacting USDT's overall income.

This correlation underscores how USDT effectively manages its reserve assets, benefiting from changing economic conditions, especially in a high-yield environment. It reflects USDT's flexible financial strategy and its strong positioning during interest rate hikes, enhancing its economic stability and role as a reliable digital asset. As mentioned earlier, 100% correlation is not possible as 80% of the reserves are held in cash and Treasury securities, with 80% specifically allocated to Treasury bills.

USDC

USDC's economic strength is reflected in its strategic reserve management. With rising interest rates, USDC benefits from its significant holdings in U.S. Treasury securities, which offer higher returns. USDC invests 75%-80% of its reserves in Treasury securities, maintaining stability while generating additional income as bond yields rise. The direct correlation to interest rate fluctuations allows USDC to benefit in a rising rate environment, further solidifying its position as an income-generating stablecoin.

The trendline shows a strong positive correlation (R = 0.889), indicating that as interest rates increase, USDC's per-unit supply income correspondingly rises. This is in line with expectations, as like other reserve-backed stablecoins, USDC derives income from high-yield assets such as U.S. Treasury securities.

This correlation highlights USDC's ability to optimize reserves and adapt to economic changes. It also emphasizes how reserve-backed stablecoins leverage interest rate hikes to enhance income generation, further solidifying their role in the digital asset ecosystem.

While this correlation is strong (R = 0.889), it is lower than that of USDT, mainly due to reserve composition differences. USDT holds a larger portion of reserves (approximately 80%) in short-term U.S. Treasury bills, which are highly sensitive to interest rate changes. In contrast, USDC's reserves are more diversified, with only 37.5% in Treasury bonds and nearly 50% allocated to repo agreements, which react more indirectly to interest rate fluctuations. This diversification enhances liquidity and stability but slightly diminishes the direct impact of rate hikes on income, resulting in a weaker correlation.

In summary, the direct comparison of USDT and USDC income highlights the impact of reserve composition and income strategies.

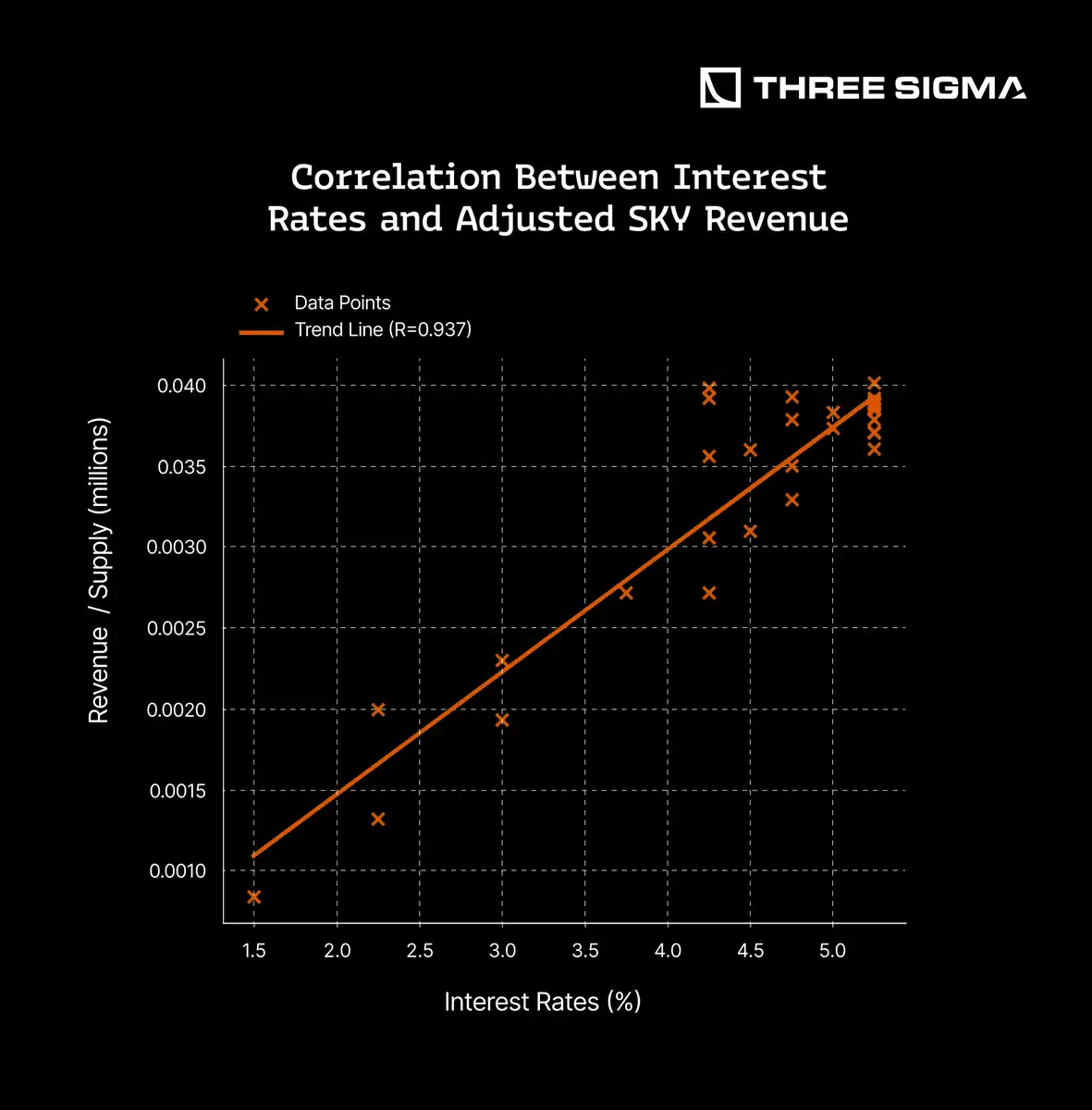

SKY (DAI/USDs)

The economic strength of SKY is reflected in its strategic reserve management. As interest rates rise, the SKY stablecoin (USDS and DAI) benefits from its exposure to yield-generating assets.

Unlike USDC and USDT, which are traditionally backed by institutional reserves, DAI has historically relied on cryptocurrency collateral assets such as ETH. However, in October 2022, MakerDAO began allocating a significant portion of DAI's reserve to U.S. treasuries and other real-world assets (RWAs) to capture higher yields. As of July 2023, over 65% of DAI's reserve is pegged to RWAs, making its income more sensitive to interest rate fluctuations. This shift has made DAI's behavior more similar to institutional stablecoins, directly benefiting from interest rate increases.

As expected, the change in DAI's reserve composition has led to a strong positive correlation between interest rates and the income per unit of the SKY stablecoin (R = 0.937). Data confirms that higher interest rates help increase income generation, further affirming that the SKY stablecoin now behaves more like yield-optimized institutional stablecoins.

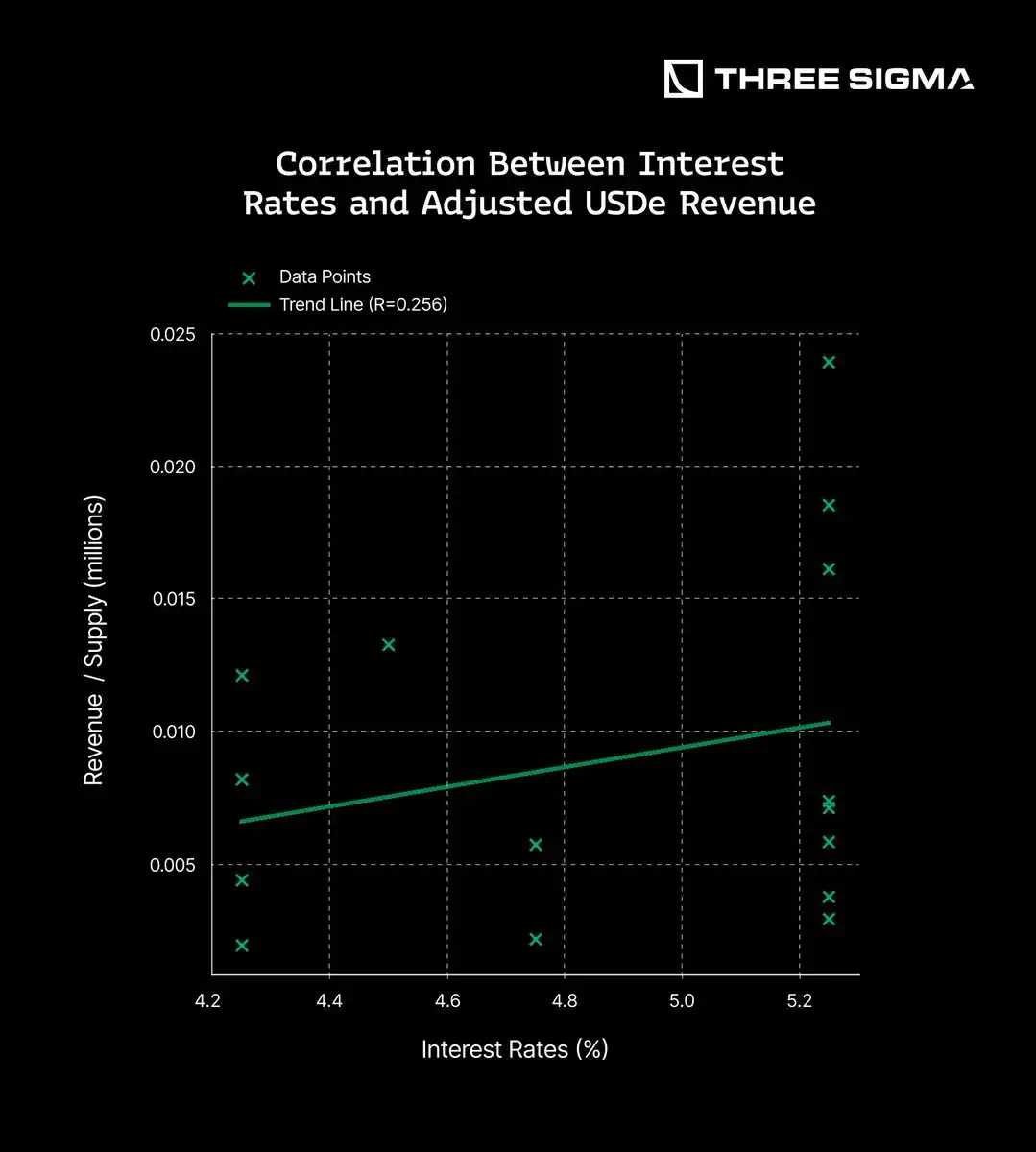

USDe

The income model of USDe is primarily based on funding rate arbitrage in the perpetual futures market, rather than traditional interest-bearing assets like U.S. treasuries. As we have observed, its hedging strategy involves holding short positions in perpetual futures, profiting from fees paid by long traders when there is an imbalance in open contracts.

When the demand for long positions increases, the funding rate rises, making holding long positions more expensive, while providing revenue opportunities for short traders (including USDe). However, this income model is less directly influenced by traditional interest rate changes and relies more on market volatility, trader positions, and the overall leverage demand in the crypto market.

The trendline shows a weaker positive correlation (R = 0.256), indicating that although higher interest rates may have some impact on USDe's income, this relationship is not particularly strong.

This is in line with expectations, as USDe's income model is primarily driven by the conditions of the perpetual futures market rather than interest rate changes. Funding rates and leverage demand play a much larger role in income generation than traditional interest rate hikes.

This correlation highlights that USDe's revenue relies on traders' behavior rather than being directly exposed to real-world interest rate changes. Although lower interest rates may encourage greater risk-taking and leverage in the crypto market, USDe's profitability remains closely tied to the imbalance in funding rates in perpetual futures trading.

5. Impact of Interest Rates Reaching 0%

Interest Rates

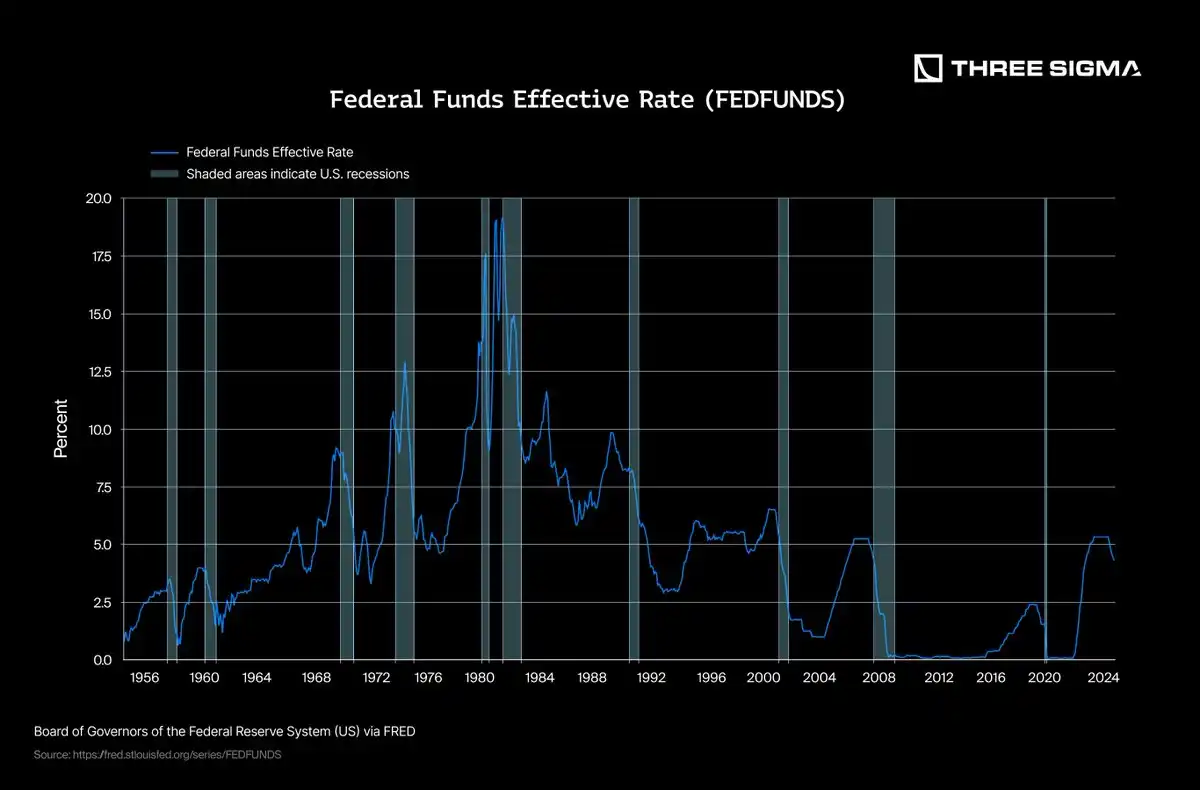

Interest rates represent the cost of borrowing or, conversely, the return received from lending or depositing funds. Central banks, such as the U.S. Federal Reserve, set benchmark rates (e.g., the federal funds rate) to manage economic growth, control inflation, and stabilize the financial system. Lower rates typically encourage borrowing, stimulating economic activity, but can also fuel inflation.

Conversely, higher rates discourage borrowing, slow down economic expansion, but help to alleviate inflationary pressures. Historically, rates fluctuate sharply based on the economic cycle and crises, often nearing zero during economic downturns (e.g., the 2008 financial crisis, COVID-19 pandemic) and spiking during inflationary periods (e.g., post-pandemic 2022-2024). Rate fluctuations directly impact the yields of Treasury bills and bonds, which are crucial for stablecoin issuers reliant on these investment returns.

Historical Rates

The most closely watched rate is the rate set by the U.S. Federal Reserve, particularly the federal funds rate, due to the global dominance of the U.S. dollar as the primary reserve currency and its widespread impact on international financial markets. Changes in U.S. rates have significant implications on global economic activity, currency valuations, investment flows, and borrowing costs, making it a key benchmark for global financial stability.

Historical charts vividly display several key rate cycles, including the historically high rates set in the early 1980s to combat inflation, followed by a steady decline in rates leading to the low-rate environment of the past two decades. The 2008 financial crisis particularly forced rates close to zero to spur economic recovery.

Specifically, in the previous rate cycle (2010-2020), the Fed kept rates at historic lows (near 0%) for an extended period until gradually raising them as the economy recovered between 2015 and 2018. However, the outbreak of the COVID-19 pandemic in early 2020 once again prompted a significant rate cut to near-zero levels to address the economic slowdown, ensure liquidity, and stabilize the financial markets.

Comparison of Interest Rates and Income Correlation

As we discussed earlier, the income models of certain stablecoins are highly dependent on interest rates, while others have structures to isolate them from these fluctuations.

The provided data clearly demonstrates this difference. The correlation of USDT, USDC, and SKY is very high (R ~0.89–0.94), highlighting their significant reliance on current interest rates. Their income mainly comes from traditional investments such as government bonds, making them face a substantial risk in near-zero interest rate scenarios, which can severely impact their profitability.

In stark contrast is USDe, with significantly lower correlation (R = 0.256), reflecting its entirely different income generation method. USDe's income primarily comes from mechanisms in the crypto market, such as perpetual futures funding rate arbitrage and staking rewards, rather than traditional interest-rate-affected assets.

In conclusion, this data strongly suggests that fiat-backed and treasury-backed stablecoins (such as USDT, USDC, and SKY) face considerable risk in a low-interest-rate environment. Conversely, algorithmic stablecoins like USDe, with their alternative income strategies, demonstrate greater resilience and may serve as a strategically diversified tool in portfolios during interest rate declines, providing relative stability.

Scenario of Interest Rates at 0%

In a scenario where interest rates return to 0%, the impact on stablecoins varies significantly depending on their income model and asset allocation:

Tether

Since USDT generates income primarily through traditional financial assets (such as treasuries), a decrease in interest rates to 0% would greatly reduce its income sources, severely impacting its profitability. However, Tether's strategic diversification into alternative investments, including cryptocurrencies (BTC, ETH) and precious metals, may partially mitigate this impact. Nevertheless, these alternative assets bring higher volatility and risk, which may not fully compensate for the lost interest income, potentially weakening its overall market position.

In 2024, Tether maintained very low operating costs, benefiting from a streamlined structure with fewer than 50 employees, minimal administrative expenses, and transaction fees from USDT token widely covering these operational costs. Legal and regulatory costs are also relatively low, with no significant fines this year, compared to the $18.5 million fine paid to the New York Attorney General in 2021.

Financially, Tether ended 2024 with a strong reserve, with reserves exceeding $7.1 billion beyond USDT holder obligations, and a total capitalization of around $20 billion. Given its conservative annual operating costs (potentially less than $100 million), even if future income drops to zero, Tether can maintain operations for over 70 years, demonstrating its outstanding financial stability and nearly unlimited operational capacity.

Circle

Circle recently filed an S-1 registration statement with the U.S. Securities and Exchange Commission, indicating plans to go public on the New York Stock Exchange under the ticker symbol "CRCL".

In 2024, Circle reported total revenue of approximately $16.8 billion, a 16% increase from $14.5 billion in 2023. It is worth noting that over 99% of this revenue is derived from reserve revenue, primarily interest earned on assets supporting USDC. In 2024, the company's net income was around $156 million, a significant decrease from $268 million in the previous year, largely due to increased operating and distribution expenses.

The total operating expenses for 2024 amounted to approximately $4.92 billion, with most of it allocated to employee compensation ($2.63 billion), general administrative expenses ($1.37 billion), IT infrastructure ($27 million), depreciation and amortization (about $51 million), marketing expenses ($17 million), and digital asset losses ($4 million). Additionally, Circle incurred around $1.01 billion in distribution and transaction costs, with approximately $908 million paid to primary distribution partner Coinbase.

As of December 31, 2024, Circle held $751 million in cash and cash equivalents, with an additional $294 million in other liquid investments, totaling available liquidity of about $1.045 billion. When assessing the financial sustainability of the company in a zero-revenue scenario, it is important to distinguish between these two types of assets:

The $751 million in cash and cash equivalents represent highly liquid, immediately usable funds—suitable for a conservative financial sustainability estimation. Based solely on this and assuming current annual operating expenses of $4.92 billion, Circle's financial runway is approximately 18 months.

If the full $1.045 billion in liquidity (cash and other liquid assets) is considered, assuming these additional assets are readily accessible and unrestricted, the financial runway could extend to around 25 months.

A more conservative approach focuses solely on cash equivalents to avoid reliance on potentially less liquid or restricted assets. However, if Circle can effectively tap into a broader pool of liquidity without issue, it would have greater flexibility.

In a prolonged environment of near-zero interest rates, Circle's heavy reliance on interest income from reserves could significantly impact its revenue source. If unable to diversify income sources effectively, the company's profitability may be adversely affected, potentially necessitating strategic adjustments such as modifying fee structures or exploring new investment avenues.

In a 0% interest rate environment, the Sky Protocol (formerly known as MakerDAO) is indeed facing a significant challenge, especially in terms of its revenue sources and financial sustainability. The protocol relies on US Treasuries, ETH staking rewards, and DeFi income, meaning that a complete lack of interest could greatly impact its revenue.

Pressure on Revenue Sources:

Stability Fees and Borrowing Demand: As borrowing demand decreases, the stability fees for DAI loans may decrease. This decrease, coupled with reduced yields on US Treasuries and other bonds, could exacerbate the protocol's financial pressure.

DeFi Funding Rates: In a low-interest-rate environment, traders may be less willing to engage in leverage, leading to a reduction in DeFi activity's funding rates.

Historically, the Sky Protocol has demonstrated its ability to adapt to a low-interest-rate environment by adjusting parameters such as the Sky Savings Rate (SSR). For example, the SSR was recently reduced to 4.5%, effective March 24, 2025, to align with current market conditions.

The Sky Protocol's total value locked is approximately $220 million and includes the following:

$101 million in DAI – Stable

$82.2 million in SKY tokens – Volatile

$36.4 million in MKR tokens – Volatile

$243,000 in stkAAVE – Volatile

$470,000 in ENS – Volatile

This $220 million total value combines liquidity assets like DAI with volatile tokens such as SKY and MKR, whose values may fluctuate based on market conditions. Liquidity assets are the most readily available source of funds for protocol operations, while volatile tokens constitute a more strategic asset class susceptible to market fluctuations.

The operational runway is the length of time the Sky Protocol can operate without generating new revenue based on its current assets and annual operating expenses. The protocol's estimated annual operating expenses are $35 million. The calculation is as follows:

If considering only liquidity assets (DAI): Runway = $101 million ÷ $35 million = 2.89 years

If considering total assets at current prices (liquidity + volatile assets): Runway = $220 million ÷ $35 million = 6.29 years

At a 0% interest rate, the financial sustainability of the Sky Protocol relies primarily on the value of volatile assets such as SKY and MKR, the fluctuations of which may affect the overall operational period. However, based solely on the surplus of the DAI system, the Sky Protocol can sustain approximately 2.89 years of operation without generating additional revenue. Taking into account the entire asset pool (including liquidity and volatility assets), Sky can sustain around 6.29 years of operation, assuming no other significant market changes.

As a protocol that has historically demonstrated adaptability, the Sky Protocol can adjust its fee structure and make strategic asset allocation adjustments to cope with a long-term low-interest-rate environment.

If the Fed were to lower interest rates to 0%, several factors could affect Ethena's ability to maintain and increase USDe's yield. Lower rates reduce the cost of borrowing, making leverage more attractive to traders and investors. In traditional markets, this usually drives capital into higher-risk assets as the returns on fixed-income instruments decrease, prompting investors to seek higher returns elsewhere. This dynamic also applies to the crypto market, where a lower-rate environment typically leads to capital inflows into cryptocurrencies like Bitcoin and Ethereum.

With more liquidity entering the market, traders are more inclined to take leveraged long positions on crypto assets, expecting prices to continue rising. This creates an imbalance in the perpetual futures markets, with long demand outweighing short demand. As a result, the funding rate increases, making it more costly to hold long positions, while short traders benefit, as is the case with the USDe strategy.

However, this benefit is not without potential risks. If rates remain low for an extended period, USDe's yield may eventually stabilize or even decrease as market participants adjust their strategies to the new norm. This adjustment could involve reducing leverage or altering trading strategies. Additionally, while a low-rate environment initially supported USDe's yield generation through perpetual contract funding rates, the long-term stability of these conditions may incentivize a shift in investor behavior toward assets other than those currently yielding the highest returns.

From a protocol perspective, Ethena is in a favorable financial position. The project has raised over $120 million through venture capital and token sales and maintains a reserve fund of around $61 million, verifiable via the on-chain wallet 0x2b5ab59163a6e93b4486f6055d33ca4a115dd4d5. This reserve fund acts as a buffer in a negative yield environment, supporting the stability of USDe. Ethena also operates with a lean team, estimating annual operating costs between $2 million and $5 million, allowing the project to sustain operations for several years even if protocol revenue significantly shrinks.

In conclusion, while the low interest rate environment has provided a unique opportunity for USDe to maintain attractiveness in the short term, its long-term sustainability relies on the ongoing market activity and volatility. Nevertheless, Ethena's strong reserve position and low burn rate provide a solid financial buffer, ensuring that the protocol can operate stably during a prolonged period of low yields without compromising its core stability.

6. Conclusion

The stablecoin ecosystem is closely tied to macroeconomic dynamics, particularly interest rates. As demonstrated in this analysis, under a scenario of interest rates at 0%, various stablecoin models exhibit significant differences in performance and sustainability.

Most affected:

USDC relies almost entirely on U.S. Treasury bond yields, and without effective diversification, its business model becomes structurally fragile in a long-term low-interest-rate environment. High operational costs and relatively limited treasury reserves further restrict Circle's long-term operational capabilities.

Significantly affected but more resilient:

Both USDT and SKY would also face substantial income compression as they rely on interest-bearing assets. However, they both have certain buffers in place. Tether (USDT) holds a significant treasury surplus, has extremely low operational costs, and is partially invested in diversified assets (such as Bitcoin, gold), allowing it to have a longer financial runway in a zero-interest-rate environment.

SKY (USDS/DAI) faces the risk of declining yields as well. However, it maintains diversified income sources through DeFi native mechanisms (such as protocol fees, cryptocurrency collateral liquidation, and smart contract lending), providing greater operational flexibility. Additionally, the protocol can rely on governance token sales to cover expenses, as proven in past cycles.

Least affected/most adaptable:

Ethena (USDe) stands out with its market-driven crypto-native revenue model that does not rely on interest-bearing instruments. Instead, Ethena captures value through perpetual futures funding rates, staking rewards, and market inefficiency capture. In a world of 0% interest rates, USDe may even benefit from leverage and speculative activity, making it one of the few projects able to thrive while other stablecoins contract.

However, in the long run, a sustained low-interest-rate environment may shift market conditions to neutral or bearish, potentially reducing Ethena's profit-making ability. In fact, when funding rates turn strongly negative for short positions, the protocol may even face short-term losses.

This comparative analysis underscores a key insight: diversification of income streams is no longer optional but critical. In a world where interest rates may return to historic lows, stablecoin issuers that overly rely on traditional financial instruments face significant risks of profit decline. Protocols with flexible crypto-native revenue engines, especially those like USDe, may not only weather the storm but emerge stronger.

Ultimately, the sustainability of the stablecoin market will be determined not only by pegging stability or market acceptance, but also by the resilience across economic systems. Protocols that adapt through product innovation, diversified collateral, or revenue mechanisms will define the next generation of digital dollars.

It is also worth noting that Circle and Tether may already be preparing for a low-rate yield world. Each is actively building or participating in their own blockchain infrastructure: Circle is constructing Cortex, while Tether has Plasma. These efforts appear to aim at diversifying their service offerings and may unlock new revenue streams beyond treasury yields.

Furthermore, Circle's IPO announcement came at the conclusion of our research. The public details align closely with the vulnerabilities and strategic directions we identified, especially the need for diversification and expansion through new ventures. The IPO could be both a liquidity event and a marker of a shift toward a more service- and infrastructure-focused business model.

Lastly, it is hard not to speculate whether Circle holds an ace up its sleeve. Is it quietly preparing to become the official issuer of the digital dollar? While there has been no formal announcement confirming this, such a move would certainly align with its regulatory-first strategy and partnerships in the United States. Who knows.

The key to Web3 success is just a step away—don't let others lead, while you are still lost in the maze.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia